|

市場調查報告書

商品編碼

1850250

氮化鎵射頻半導體裝置:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)GaN RF Semiconductor Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

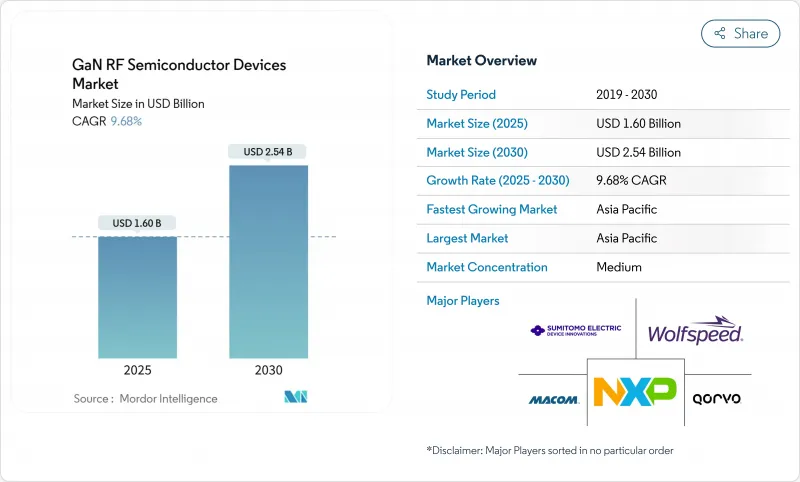

預計到 2025 年,GaN 射頻半導體裝置市場規模將達到 16 億美元,到 2030 年將擴大到 25.4 億美元,複合年成長率為 9.68%。

5G基礎設施、主動電子掃描陣列(AESA)雷達、衛星有效載荷以及79 GHz車載成像雷達等領域對高頻、高功率解決方案的需求不斷成長,使得氮化鎵(GaN)成為通訊、國防和行動通訊生態系統中的主流技術。 GaN-on-SiC仍然是熱穩定性方面的性能標桿,而向200mm GaN-on-Si晶圓的過渡縮小了其與傳統LDMOS的成本差距,從而擴大了其在對價格敏感的寬能能隙以下無線電單元中的應用。在區域層面,GaN射頻半導體裝置市場受益於亞太地區推動半導體自主發展的政策,以及美國和歐盟同時將寬禁帶電子裝置列為國防現代化預算優先事項。垂直整合製造商之間日益激烈的競爭促使企業快速提交專利申請、進行策略性收購並擴大產能,旨在緩解150mm和200mm磊晶圓的瓶頸,並確保新興毫米波和6G研究項目所需的基板容差。

全球氮化鎵射頻半導體元件市場趨勢及洞察

5G宏大型基地台和小型基地台部署加速氮化鎵(GaN)技術的應用

在中國、韓國和日本部署的大規模MIMO基地台架構依賴多達64個功率放大器通道,而氮化鎵(GaN)相比LDMOS實現了15-20%的能源效率提升,從而降低了站點級營運成本。開放式無線存取網路(Open-RAN)標準化將無線電硬體與系統供應商解耦,使得專業的GaN供應商能夠獲得用於遠端無線電站升級的介面。中國移動創紀錄的部署證明了GaN在實際應用中的可靠性,而Qorvo 0.013%的故障率進一步增強了營運商的信心。向200mm晶圓的過渡逐步降低了每瓦美元的功率輸出,使得GaN射頻半導體裝置市場能夠更廣泛地滲透到農村地區和室內小型基地台等更深處。電訊的節能目標,加上GaN的低散熱特性,推動了採購架構更重視效率指標而非組件價格。

美國/歐盟AESA雷達現代化推動高功率需求

美國國防部已將氮化鎵(GaN)技術推進至製造成熟度10級,並為其下一代雷達計畫撥款超過30億美元,用於2024-2025年期間的研發。歐洲機構在其遠距監視和電子戰設備的更新換代過程中也採用了類似的策略,GaN卓越的功率密度顯著提升了探測距離和干擾效能。Honeywell公司與美國海軍簽訂的價值2990萬美元的契約,用於對其低頻寬發射機進行GaN維修,這體現了各方對降低設備過時風險和提高頻譜靈活性的重視。能夠承受200瓦/毫米熱通量的封裝技術突破已應用於下游的商用通訊無線電領域,從而將GaN射頻半導體裝置市場拓展至國防領域之外。

成本溢價限制了價格驅動型部署的應用。

2024年,在6GHz以下無線應用領域,GaN功率擴大機的價格仍比LDMOS低40%,減緩了新興市場的轉型步伐。儘管德克薩斯向8吋GaN-on-Silicon製造製程的轉型使晶粒成本降低了10%以上,但宏觀經濟壓力持續抑制著通訊業者的資本支出,尤其是在印度和東南亞部分地區,通訊業者OEM廠商繼續採取雙源籌資策略,維持LDMOS的產量,從而限制了GaN射頻半導體元件市場近期的成長空間。

細分市場分析

到2024年,通訊基礎設施將佔總收入的43.2%,從而支撐氮化鎵(GaN)射頻半導體裝置市場的發展。基地台供應商正在採用GaN技術來縮小裝置尺寸,並將宏無線電單元的汲極效率基準提升至55.2%。這降低了冷卻負荷並減輕了塔頂重量,對於高密度5G部署至關重要。 Soitec的工程基板可降低插入損耗,進而提高每個站點的覆蓋範圍。隨著通訊業者開展基於GaN前端的6G亞太赫茲試驗,GaN射頻半導體裝置市場在2025年之前保持了強勁的成長動能。

汽車雷達市場預計在2024年成長放緩後,到2030年將以18.5%的複合年成長率成長。中國的高級駕駛輔助系統強制令以及韓國的智慧網聯汽車生態系統刺激了對79 GHz成像雷達的需求,而氮化鎵(GaN)技術在不犧牲可靠性的前提下實現了毫米波功率密度。採用GaN功率放大器-低雜訊放大器(PA-LNA)模組的V2X通訊試點計畫提升了其量產前景。 200毫米GaN-on-Si晶圓的成本降低藍圖有望使其與主流汽車電子產品接軌,從而創造一個更廣泛的GaN射頻半導體裝置市場。

在國防和航太,雷達、電子戰和衛星通訊有效載荷正充分利用氮化鎵(GaN)的抗輻射性和輸出功率。在家用電子電器,GaN功率放大器(PA)已被應用於Wi-Fi 7路由器和行動電話前端,檢驗在小訊號傳輸方面的潛力。在工業機器人領域,基於GaN HEMT的6.78 MHz無線充電發射器已被採用,凸顯了其跨行業應用範圍,並有助於實現收入來源多元化。

分離式功率電晶體在2024年佔據了46.4%的市場佔有率,這反映了雷達、廣播和大型基地台無線電等領域成熟的設計週期。 MACOM的產品組合涵蓋2W至7kW的功率範圍,展現了其支援GaN射頻半導體裝置市場的可擴展性。 [2] 散熱增強型螺栓固定封裝支援超過80%的汲極效率,從而在嚴苛的佔空比下延長了裝置壽命。

單晶片微波積體電路功率放大器將成為成長最快的細分市場,預計到2030年將以19.2%的複合年成長率成長。相位陣列模組、空間受限的衛星通訊終端以及毫米波回程傳輸都青睞MMIC,因為它可以將增益級和偏壓網路整合在緊湊的晶粒上。 Qorvo的寬頻QPA2210D正是這一趨勢的典型代表,與分立裝置相比,其功率附加效率提高了6 dB。射頻開關和前端模組採用增強型GaN電晶體來應對熱開關應力,而低雜訊放大器開始在C波段衛星鏈路中取代GaAs,從而拓展了整個產業的格局。

GaN 射頻半導體元件市場按應用(國防和航太、通訊基礎設施、其他)、裝置類型(分離式射頻功率電晶體、MMIC/單晶片功率放大器、其他)、基板技術(GaN-On-SiC、GaN-On-Si、其他)、頻寬(VHF/UHF(低於 1 GHz)、L/S 頻段(VHF/UHF(低於 1 頻段)、L/SS 頻段(VHF/UHF(低於 1 頻段)、L/SS 頻段)。 GHz)、其他)和地區(北美、南美、歐洲、亞太、中東和非洲)進行細分。

區域分析

亞太地區將在2024年以34.1%的營收佔比領跑,預計到2030年將以18.4%的複合年成長率成長。中國5G基地台的快速成長、本土氮化鎵代工廠的建設以及「第三次半導體浪潮」下的政策支持,加速了區域自主發展。韓國專注於人工智慧中心和汽車雷達,而日本則充分利用家用電子電器的傳統優勢和碳化矽基板供應。台灣先進的後端服務加速了矽基氮化鎵(GaN-on-Si)的成本最佳化,從而強化了氮化鎵射頻半導體裝置市場的成長循環。

北美位居第二,這主要得益於美國的國防預算和衛星網際網路衛星群。政府對國內晶圓廠的資助,例如Polar Semiconductor公司在明尼蘇達州的GaN-on-Si計劃,增強了供應鏈的韌性。加拿大電信業的更新換代以及墨西哥汽車和電子產業叢集的發展,使北美大陸的需求多元化,從而使該地區的GaN射頻半導體裝置市場免受單一產業波動的影響。

歐洲將其在汽車雷達領域的領先地位與節能型工業驅動相結合。德國率先部署了79 GHz車載感測器,法國專注於航太有效載荷,英國則優先升級了以頻率為主導的電子戰系統。歐盟的戰略自主方案為合資企業(例如IQE-X-FAB的650V氮化鎵平台)提供了津貼,促進了區域價值鏈的發展,從而支持了該地區氮化鎵射頻半導體裝置市場的擴張。巴西的新增應用、波灣合作理事會智慧城市的部署以及澳洲的低地球軌道回程傳輸試驗,都標誌著這項技術在全球的普及應用。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 亞太地區5G大型基地台及小型基地台部署

- 美國/歐盟AESA雷達現代化改造的資金

- 低/中地球軌道衛星通訊衛星群的有效載荷需求

- 中國和韓國毫米波汽車成像雷達的應用

- 面向工業4.0機器人的高功率無線充電

- 快速採用開放式RAN遠端無線電站

- 市場限制

- Sub-6GHz 基地台的成本溢價和 LDMOS 對比

- 功率超過 3 千瓦的戰術雷達模組中碳化矽的侵蝕

- 外延片和基板供應瓶頸(150mm 和 200mm)

- 溫度控管和可靠性超過 200W/mm

- 價值鏈分析

- 技術展望

- 氮化鎵矽基元件的大規模生產及向200毫米晶圓的過渡

- 監理展望

- 國際電信聯盟和美國聯邦通訊委員會關於 5G/6G 和雷達頻譜分配的公告

- 波特五力分析

- 買方的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- RF-GaN專利概況

- 宏觀經濟因素如何影響市場

第5章 市場規模與成長預測

- 透過使用

- 國防/航太

- 通訊基礎設施

- 消費性電子產品

- 汽車(ADAS、V2X)

- 工業和能源

- 資料中心和高效能電源鏈路

- 依設備類型

- 分離式射頻功率電晶體

- MMIC/單晶片功率放大器

- 射頻開關和前端模組

- 低雜訊驅動放大器

- 透過基板技術

- GaN-on-SiC

- GaN-on-Si

- 氮化鎵/鑽石及先進複合材料

- 按頻寬

- 甚高頻/超高頻(低於 1 GHz)

- L/S波段(1至4 GHz)

- C/ X波段(4-12 GHz)

- Ku/ Ka波段(12-40 GHz)

- 毫米波(40 GHz 以上,包括 5G FR2)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 台灣

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Wolfspeed, Inc.

- Qorvo, Inc.

- Sumitomo Electric Device Innovations

- NXP Semiconductors NV

- MACOM Technology Solutions-GaN-on-SiC

- Broadcom Inc.

- Infineon Technologies AG

- RFHIC Corp.

- Ampleon Netherlands BV

- Mitsubishi Electric Corporation

- Fujitsu Ltd.(GaN RF)

- Northrop Grumman Microelectronics

- Integra Technologies, Inc.

- Analog Devices Inc.

- WIN Semiconductors Corp.

- Finwave Semiconductor Inc.

- Tagore Technology Inc.

- Guerrilla RF

- SEDI-Silent-Solutions Engineering(EU)

- Teledyne e2v HiRel

第7章 市場機會與未來展望

The GaN RF semiconductor devices market size reached USD 1.60 billion in 2025 and is projected to advance to USD 2.54 billion by 2030, delivering a CAGR of 9.68%.

Rising demand for high-frequency, high-power solutions in 5G infrastructure, active electronically scanned array (AESA) radar, satellite payloads, and 79 GHz automotive imaging radar positioned gallium nitride as a mainstream technology across telecom, defense, and mobility ecosystems. GaN-on-SiC remained the performance benchmark for thermal robustness, while the transition to 200 mm GaN-on-Si wafers compressed cost gaps versus legacy LDMOS, amplifying adoption in price-sensitive sub-6 GHz radio units. Regionally, the GaN RF semiconductor devices market benefited from Asia-Pacific's policy-backed semiconductor self-reliance drive and concurrent U.S.-EU defense modernization budgets that prioritized wide-bandgap electronics. Intensifying competition among vertically integrated manufacturers triggered rapid patent filings, strategic acquisitions, and capacity expansions designed to ease 150 mm and 200 mm epi-wafer bottlenecks and secure substrate resilience for emerging mmWave and 6 G research programs.

Global GaN RF Semiconductor Devices Market Trends and Insights

5G macro- and small-cell roll-outs accelerate GaN adoption

Massive-MIMO base-station architectures installed across China, Korea, and Japan relied on up to 64 power-amplifier channels, where gallium nitride delivered a 15-20% energy-efficiency uplift versus LDMOS, cutting site-level operating costs. Open-RAN standardization further decoupled radio hardware from system vendors, enabling specialist GaN suppliers to win sockets for remote-radio-head upgrades. Record deployments by China Mobile validated field reliability, while Qorvo's 0.013% failure rate reinforced operator confidence. Progressive reductions in USD/W output through 200 mm wafer migration positioned the GaN RF semiconductor devices market for broader penetration of rural and deep-indoor small-cell layers. Telecom carriers' energy-saving targets aligned with GaN's lower heat dissipation, catalyzing procurement frameworks that rewarded efficiency metrics over component price.

U.S./EU AESA radar modernization drives high-power demand

The U.S. Department of Defense elevated GaN to Manufacturing Readiness Level 10 and allocated more than USD 3 billion for next-generation radar programs between 2024-2025, triggering multi-year production ramps for high-power monolithic microwave integrated circuits (MMICs). European ministries mirrored this trajectory through long-range surveillance and electronic-warfare refresh cycles, where GaN's superior power density increased detection range and jamming effectiveness. Honeywell's USD 29.9 million contract to retrofit Navy low-band transmitters with GaN exemplified obsolescence mitigation and spectrum agility priorities. Packaging breakthroughs that survived 200 W/mm heat flux migrated downstream to commercial telecom radios, expanding the GaN RF semiconductor devices market beyond defense silos.

Cost premium tempers penetration in price-sensitive deployments

In 2024, GaN power amplifiers carried a 40% price delta over LDMOS for sub-6 GHz radios, delaying transitions in emerging markets, even though energy savings absorbed the gap within 18 months of operation. Texas Instruments' move to 8-inch GaN-on-Si fabrication lowered die cost by more than 10%, but macroeconomic pressures still constrained carrier capex, especially in India and parts of Southeast Asia. Telecom OEMs, therefore, maintained dual-sourcing strategies, sustaining LDMOS volume and limiting near-term upside for the GaN RF semiconductor devices market.

Other drivers and restraints analyzed in the detailed report include:

- LEO/MEO sat-com constellation payload demand

- mmWave automotive imaging radar adoption in China and South Korea

- Epi-wafer and substrate shortages create production chokepoints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Telecom infrastructure accounted for 43.2% of 2024 revenue, anchoring the GaN RF semiconductor devices market. Base-station vendors adopted GaN to unlock smaller footprints and a 55.2% drain efficiency benchmark in macro radio units. This translates to reduced cooling loads and lower tower-top weight, critical for dense 5G rollouts. Open-RAN disaggregation encouraged independent power-amplifier specialists to capture design wins, while Soitec's engineered substrates reduced insertion losses, boosting coverage per site. The GaN RF semiconductor devices market retained momentum through 2025 as operators trialed 6 G sub-THz pilots that presupposed GaN front ends.

Automotive radar remained a modest slice in 2024 but is forecast to expand at an 18.5% CAGR to 2030. China's mandatory advanced-driver-assistance mandates and South Korea's connected-car ecosystem spurred demand for 79 GHz imaging radar, where GaN handled millimeter-wave power density without compromising reliability. V2X communication pilots incorporating GaN PA-LNA modules amplify volume prospects. Cost-down roadmaps tied to 200 mm GaN-on-Si wafers promised alignment with mainstream vehicle electronics, creating scale for the wider GaN RF semiconductor devices market.

Across defense and aerospace, radar, electronic warfare, and sat-com payloads drew on GaN's radiation tolerance and output power. Consumer electronics adopted GaN PAs for Wi-Fi 7 routers and handset front ends, validating smaller-signal opportunities. Industrial robotics embraced 6.78 MHz wireless-charging transmitters powered by GaN HEMTs, underscoring cross-sector breadth that diversified revenue streams.

Discrete power transistors captured 46.4% share in 2024, reflecting entrenched design-in cycles across radar, broadcast, and macro-cell radios. MACOM's portfolio spanned 2 W to 7 kW, illustrating scalability that underpinned the GaN RF semiconductor devices market.[2] Thermal-enhanced bolt-down packages supported >80% drain efficiency, extending device lifetimes in harsh duty cycles.

Monolithic microwave integrated-circuit power amplifiers delivered the fastest growth, projected at 19.2% CAGR through 2030. Phased-array modules, space-constrained sat-com terminals, and mmWave backhaul radios favored MMICs that collapsed gain stages and bias networks into compact dies. Qorvo's wideband QPA2210D exemplified this trend, offering 6 dB higher power-added efficiency versus discrete alternatives. RF switches and front-end modules employed enhancement-mode GaN transistors to handle hot-switching stresses, while low-noise amplifiers began displacing GaAs in C-Band satellite links, broadening the GaN RF semiconductor devices industry landscape.

Gan RF Semiconductor Device Market is Segmented by Application (Defense and Aerospace, Telecom Infrastructure, and More), Device Type (Discrete RF Power Transistors, MMIC / Monolithic Power Amplifiers, and More), Substrate Technology (GaN-On-SiC, GaN-On-Si, and More), Frequency Band (VHF / UHF (<1 GHz), L / S-Band (1-4 GHz), and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Geography Analysis

Asia-Pacific led with 34.1% of 2024 revenue and is projected to advance at an 18.4% CAGR through 2030. China's 5 G base-station surge, local GaN foundry build-outs, and policy support under the "third semiconductor wave" catalyzed regional self-reliance. Korea focused on AI-centers and automotive radar, while Japan leveraged consumer-electronics legacy and SiC substrate supply. Taiwan's advanced backend services accelerated GaN-on-Si cost optimization, reinforcing the GaN RF semiconductor devices market growth loop.

North America ranked second, buoyed by the U.S. defense budget and satellite-internet mega constellations. Government funding for domestic fabs, such as Polar Semiconductor's Minnesota GaN-on-Si project, supported supply-chain resiliency. Canada's telecom revamps and Mexico's automotive-electronics clusters created continental demand diversity that insulated the regional GaN RF semiconductor devices market from single-sector volatility.

Europe combined automotive radar leadership with energy-efficient industrial drives. Germany spearheaded 79 GHz vehicle sensor roll-outs, France emphasized aerospace payloads, and the United Kingdom prioritized spectrum-dominated electronic-warfare upgrades. EU strategic autonomy packages channelled grants to joint ventures such as IQE-X-FAB's 650 V GaN platform, nurturing a localized value chain that underpinned the GaN RF semiconductor devices market size expansion in the bloc. Emerging adoption across Brazil, Gulf Cooperation Council smart-city rollouts, and Australia's low-Earth-orbit backhaul trials showcased the technology's global diffusion trajectory.

- Wolfspeed, Inc.

- Qorvo, Inc.

- Sumitomo Electric Device Innovations

- NXP Semiconductors N.V.

- MACOM Technology Solutions - GaN-on-SiC

- Broadcom Inc.

- Infineon Technologies AG

- RFHIC Corp.

- Ampleon Netherlands B.V.

- Mitsubishi Electric Corporation

- Fujitsu Ltd. (GaN RF)

- Northrop Grumman Microelectronics

- Integra Technologies, Inc.

- Analog Devices Inc.

- WIN Semiconductors Corp.

- Finwave Semiconductor Inc.

- Tagore Technology Inc.

- Guerrilla RF

- SEDI - Silent-Solutions Engineering (EU)

- Teledyne e2v HiRel

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G Macro- and Small-Cell Roll-outs across Asia-Pacific

- 4.2.2 U.S./EU AESA Radar Modernization Funding

- 4.2.3 LEO / MEO Sat-Com Constellation Payload Demand

- 4.2.4 mmWave Automotive Imaging Radar Adoption in China and South Korea

- 4.2.5 High-Power Wireless Charging for Industrie 4.0 Robotics

- 4.2.6 Rapid Proliferation of Open-RAN Remote Radio Heads

- 4.3 Market Restraints

- 4.3.1 Cost Premium vs. LDMOS in Sub-6 GHz Base-Stations

- 4.3.2 SiC Encroachment in >3 kW Tactical Radar Blocks

- 4.3.3 Epi-wafer and Sub-strate Supply Bottlenecks (150 and 200 mm)

- 4.3.4 Thermal Management and Reliability at >200 W/mm

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.5.1 GaN-on-Si Mass-Production and 200 mm Transition

- 4.6 Regulatory Outlook

- 4.6.1 ITU and FCC Spectrum Releases for 5G/6G and Radar

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 RF-GaN Patent Landscape

- 4.9 Imapct of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Defense and Aerospace

- 5.1.2 Telecom Infrastructure

- 5.1.3 Consumer Electronics

- 5.1.4 Automotive (ADAS, V2X)

- 5.1.5 Industrial and Energy

- 5.1.6 Data Centers and High-Efficiency Power Links

- 5.2 By Device Type

- 5.2.1 Discrete RF Power Transistors

- 5.2.2 MMIC / Monolithic Power Amplifiers

- 5.2.3 RF Switches and Front-End Modules

- 5.2.4 Low-Noise and Driver Amplifiers

- 5.3 By Substrate Technology

- 5.3.1 GaN-on-SiC

- 5.3.2 GaN-on-Si

- 5.3.3 GaN-on-Diamond and Advanced Composites

- 5.4 By Frequency Band

- 5.4.1 VHF / UHF (<1 GHz)

- 5.4.2 L / S-Band (1-4 GHz)

- 5.4.3 C / X-Band (4-12 GHz)

- 5.4.4 Ku / Ka-Band (12-40 GHz)

- 5.4.5 mmWave (>40 GHz, incl. 5G FR2)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Taiwan

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Wolfspeed, Inc.

- 6.4.2 Qorvo, Inc.

- 6.4.3 Sumitomo Electric Device Innovations

- 6.4.4 NXP Semiconductors N.V.

- 6.4.5 MACOM Technology Solutions - GaN-on-SiC

- 6.4.6 Broadcom Inc.

- 6.4.7 Infineon Technologies AG

- 6.4.8 RFHIC Corp.

- 6.4.9 Ampleon Netherlands B.V.

- 6.4.10 Mitsubishi Electric Corporation

- 6.4.11 Fujitsu Ltd. (GaN RF)

- 6.4.12 Northrop Grumman Microelectronics

- 6.4.13 Integra Technologies, Inc.

- 6.4.14 Analog Devices Inc.

- 6.4.15 WIN Semiconductors Corp.

- 6.4.16 Finwave Semiconductor Inc.

- 6.4.17 Tagore Technology Inc.

- 6.4.18 Guerrilla RF

- 6.4.19 SEDI - Silent-Solutions Engineering (EU)

- 6.4.20 Teledyne e2v HiRel

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

射頻氮化鎵市場:依產品、材料組成、晶圓尺寸、應用和終端用戶產業分類-全球預測,2026-2032年

射頻氮化鎵市場:依產品、材料組成、晶圓尺寸、應用和終端用戶產業分類-全球預測,2026-2032年 射頻氮化鎵(RF GaN)元件市場分析及預測(至2035年):依類型、產品類型、技術、元件、應用、材料類型、製程、部署狀態、最終用戶及功能分類微波氮化鎵 (GaN) 市場分析及預測(至 2035 年):按類型、產品類型、技術、組件、應用、材料類型、裝置、最終用戶、功能和安裝類型分類氮化鎵高頻功率放大器市場分析及預測(至2035年):按類型、產品類型、技術、組件、應用、最終用戶、功能、安裝類型、解決方案和模式分類高頻氮化鎵市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、材料類型、裝置、最終用戶、功能分類

射頻氮化鎵(RF GaN)元件市場分析及預測(至2035年):依類型、產品類型、技術、元件、應用、材料類型、製程、部署狀態、最終用戶及功能分類微波氮化鎵 (GaN) 市場分析及預測(至 2035 年):按類型、產品類型、技術、組件、應用、材料類型、裝置、最終用戶、功能和安裝類型分類氮化鎵高頻功率放大器市場分析及預測(至2035年):按類型、產品類型、技術、組件、應用、最終用戶、功能、安裝類型、解決方案和模式分類高頻氮化鎵市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、材料類型、裝置、最終用戶、功能分類 射頻氮化鎵市場規模、佔有率、成長及全球產業分析:依元件類型、材料類型、應用和地區劃分的洞察與預測(2026-2034 年)GaN基板和GaN晶圓市場(按產品、晶圓尺寸和應用分類)-2026-2032年全球預測

射頻氮化鎵市場規模、佔有率、成長及全球產業分析:依元件類型、材料類型、應用和地區劃分的洞察與預測(2026-2034 年)GaN基板和GaN晶圓市場(按產品、晶圓尺寸和應用分類)-2026-2032年全球預測 GaN射頻元件市場規模、佔有率和成長分析(按元件類型、應用、頻寬、技術和地區分類)-產業預測(2026-2033年)

GaN射頻元件市場規模、佔有率和成長分析(按元件類型、應用、頻寬、技術和地區分類)-產業預測(2026-2033年) 射頻氮化鎵半導體市場-全球產業規模、佔有率、趨勢、機會和預測,按材料、應用、最終用戶、地區和競爭格局分類,2020-2030年預測射頻氮化鎵(RF GaN)市場-2025-2030年預測

射頻氮化鎵半導體市場-全球產業規模、佔有率、趨勢、機會和預測,按材料、應用、最終用戶、地區和競爭格局分類,2020-2030年預測射頻氮化鎵(RF GaN)市場-2025-2030年預測