|

市場調查報告書

商品編碼

2035070

農藥:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Agrochemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

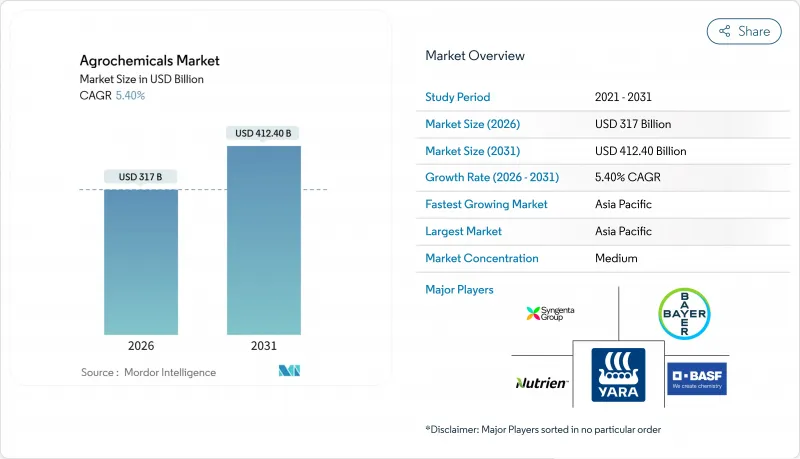

據估計,2026年農藥市值為3,170億美元,預計到2031年將達到4,124億美元。

這相當於年複合成長率為 5.40%。

這一成長不僅得益於銷售量增加,還得益於為對抗抗性雜草而轉向使用高階除草劑,以及逐步淘汰高毒性化學品的監管措施。這些趨勢正在推動對緩釋肥料和先進作物保護解決方案的投資。例如,Nutrien 的碳排放氮肥專案和 Yara 的綠色氨專案等舉措表明,平衡產品性能與永續性的重要性日益凸顯。此外,碳定價、農藥稅和更嚴格的殘留標準等因素正在重塑產品平臺,使可獲得檢驗排放信用的包膜性肥料更具優勢。然而,儘管訴訟風險和重新註冊成本正在縮減產品系列併提高進入門檻,但這對能夠有效管理合規成本的多元化公司而言卻有利。

全球農藥市場趨勢及洞察

抗除草劑雜草的增加推動了對優質除草劑的需求。

目前,長芒莧的爆發影響美國31個州,而抗Glyphosate黑麥草已在澳洲蔓延超過200萬公頃。種植者正從非專利Glyphosate轉向使用優質的15類和27類除草劑,預計這些除草劑的價格將上漲40%至60%。儘管種植面積保持不變,但每公頃處理收入卻在成長,這使得那些在同一種植季內輪換使用多種作用機制的產品系列更具優勢。科迪華公司的Enlist E3大豆性狀-除草劑組合預計到2025年將占美國大豆種植面積的35%,這表明綜合解決方案如何確保持續銷售並遏制抗藥性的演變。監管機構正在加強控制法規,正式強制要求作物輪作和種植替代作物,這增加了對具有多種作用機制的除草劑的需求。因此,種植者優先考慮能夠提供全面抗藥性管理方案的供應商。

精密農業和數據訂閱模式正在全球擴展。

「投入即服務」合約將一次性物料採購轉化為持續的收入來源和資料循環。科迪華的「Granular」平台將在2025年前管理6000萬英畝農田,而雅苒的「Atfarm」將指導歐洲120萬公頃農田的耕作,減少12%的氮肥浪費,同時產生每噸25歐元(27美元)的排碳權。智慧型手機在印度和印尼的普及正在將類似的服務擴展到小規模農戶,而遠端資訊處理技術已使拜耳的「Climate FieldView」在全球400萬個農場得到部署。透過管理處方數據,成熟企業可以主導種子、肥料和作物保護劑的組合,平台的重要性堪比活性成分研發管線,並成為獲利的核心。

歐盟、巴西和中國加速淘汰高毒性活性成分

歐盟提案在2027年前禁用12種新菸鹼類和有機磷類農藥,巴西將百草枯重新歸類為「劇毒」農藥,以及中國禁用41種農藥活性成分,這些措施正在縮減註冊生產商的產品系列。這種產品組合的轉變縮短了替代分子的有效專利期限,迫使企業要麼加快產品上市以保護利潤,要麼轉向生物農藥。規模較小的製劑生產商由於無法獲得重組資金而退出市場,進一步加劇了市場主導地位的集中,這些市場主導地位的鞏固者往往是那些已實現多元化經營以分攤合規成本的老牌企業。

細分市場分析

2025年,化肥將主導農藥市場,佔銷售額的75%。尿素、硝酸銨和尿素硝酸銨溶液(UAN)等氮肥仍將是亞太和北美地區糧食生產的關鍵要素。相較之下,植物生長調節劑預計將以13.0%的複合年成長率實現最快成長,這主要得益於其在調節開花時間和延長果蔬保存期限方面的應用。除草劑在農藥市場佔有較大佔有率,在嚴格執行零殘留法規的地區,產品系列重組正在進行中。儘管化肥的市場佔有率較小,但它透過減少高達25%的施用量,在維持有效性的同時緩解監管壓力,從而創造了顯著的策略價值。科迪華農業科技公司的吉貝素調節劑ProGibb在2025年實現了可觀的銷售額,反映出除傳統化肥支出之外,對增產分子的需求日益成長。預計化肥產業的農藥市場將穩步擴張,高利潤成長的調節劑和其他與永續發展計劃一致的產品有望推動這一成長。

隨著有毒活性成分逐步淘汰以及包膜製劑的日益普及,企業得以將肥料和作物保護解決方案整合起來。同時提供營養效率和病蟲害防治產品的企業可以在同一耕作面積內進行交叉銷售,加強與銷售管道合作夥伴的關係,並進一步擴大市場佔有率。這些趨勢使得農藥企業即使在通用肥料供需週期波動的情況下也能保持盈利。此外,透過第三方認證證明其環境績效的企業能夠獲得溢價,這預示著市場競爭模式將長期擺脫以銷售為主導的局面。

區域分析

預計到2025年,亞太地區將佔據全球農藥市場佔有率的53%,並在2031年之前以6.6%的複合年成長率成長。支撐基本需求的關鍵因素包括中國旨在穩定化肥用量並維持農業生產力的「化肥零成長」政策,以及印度的尿素補貼計劃,該計劃確保農民能夠負擔得起化肥價格並維持需求。此外,日本的精密農業平台表明,碳貨幣化措施可以透過促進高品質農業材料的使用,進一步推動該地區的市場成長。這些趨勢鞏固了亞太地區作為全球農藥市場關鍵驅動力的地位。

在非洲,數位化諮詢服務的應用正在逐步提升小規模農戶的產量,以應對傳統農業物資匱乏和氣候變遷等挑戰。埃及和南非憑藉其完善的灌溉基礎設施和以出口為導向的園藝產業(支持高價值面積的生產),成為重要的市場。同時,南美市場的成長主要得益於巴西大豆和玉米種植面積的擴大,這得益於有利的氣候條件和政府政策的支持。阿根廷的出口導向農業模式也是成長要素,因為該國優先考慮在全球市場中的競爭力。

在北美,市場成長受到許多挑戰的影響,例如耕地老化和訴訟的影響,但數據平台和碳專案的進步正在為農藥生產商創造新的業務收益機會。歐洲市場成長速度在該地區最為緩慢,主要受「從農場到餐桌」政策下農藥減量目標的限制。然而,在碳邊境調節機制(CBAM)等管理方案的支持下,歐洲在低碳肥料的推廣應用方面正發揮主導作用。在中東,低成本的天然氣資源正被用於生產出口氨,同時也積極探索藍氨和綠氨的生產路線。這些區域趨勢表明,儘管亞太地區在絕對銷售額方面佔據主導地位,但非洲和南美洲也蘊藏著巨大的成長潛力,並正在塑造農藥市場的擴大策略。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 抗除草劑雜草的日益出現推動了對高品質除草劑的需求。

- 精密農業和數據訂閱模式正在全球擴展。

- 主要農藥專利到期(2024-2028 年)將促進低成本非專利藥的普及。

- 透過排碳權將氮高效產品貨幣化

- 緩釋肥和包膜緩釋肥是主流選擇。

- 歐盟的碳邊境調節機制(CBAM)和類似的碳政策將加速低碳氨的採用。

- 市場限制因素

- 歐盟、巴西和中國正在加速淘汰劇毒活性成分。

- Glyphosate價格波動對製藥公司的利潤率帶來了壓力。

- 監管資料包增加和重新註冊成本上升

- 北美維權人士面臨長期訴訟風險

- 監理情勢

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 依產品類型

- 肥料

- 氮基

- 磷酸鹽

- 鉀

- 其他肥料

- 殺蟲劑

- 除草劑

- 殺蟲劑

- 消毒劑

- 其他農藥

- 添加劑

- 植物生長調節劑

- 肥料

- 按作物類型

- 穀物和穀類

- 豆類和油籽

- 水果和蔬菜

- 經濟作物

- 草坪和觀賞植物

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Syngenta Group

- Bayer AG

- BASF SE

- Corteva Agriscience

- Nutrien Ltd.

- Yara International ASA

- Mosaic Company

- CF Industries Holdings Inc.

- UPL Ltd.

- FMC Corporation

- Sumitomo Chemical Co., Ltd.

- Nufarm Ltd.

- K+S Aktiengesellschaft

- ICL Group

- OCP Group

第7章 市場機會與未來展望

The agrochemicals market size is estimated to be USD 317.00 billion in 2026 and is forecast to reach USD 412.40 billion by 2031, reflecting a 5.40% CAGR.

This growth is driven not only by volume increases but also by a shift toward premium herbicides that address resistant weeds and regulatory measures phasing out high-toxicity chemicals. These trends are steering investments toward controlled-release fertilizers and advanced crop protection solutions. Initiatives such as Nutrien's carbon-aligned nitrogen program and Yara's green ammonia projects underscore the rising importance of combining product performance with sustainability compliance. Additionally, factors like carbon pricing, pesticide taxes, and stricter residue limits are reshaping product pipelines, favoring coated fertilizers that enable verified emission credits. However, litigation risks and re-registration costs are narrowing product portfolios, increasing entry barriers, and benefiting diversified companies capable of managing compliance costs effectively.

Global Agrochemicals Market Trends and Insights

Rising Incidence of Herbicide-Resistant Weeds Fuels Demand for Premium Herbicides

Palmer amaranth infestations now span 31 United States states, and glyphosate-resistant ryegrass covers more than 2 million hectares in Australia. Growers are substituting generic glyphosate with premium Group 15 and Group 27 chemistries, commanding 40-60% price uplifts. Revenue per treated hectare is rising even as acreage stays flat, rewarding portfolios that rotate multiple modes of action within a season. Trait-herbicide bundles such as Corteva's Enlist E3 soybean, which reached 35% of U.S. soybean acres in 2025, illustrate how integrated solutions secure recurring sales and temper resistance evolution. Regulators are tightening stewardship rules that formalize rotation and refuge planting, increasing demand for multi-site chemistry access. Growers, therefore, prioritize suppliers able to deliver complete resistance-management programs.

Precision Agriculture and Data Subscription Models Scale Globally

Input-as-a-Service contracts convert one-time input purchases into recurring revenue and data loops. Corteva's Granular platform guided 60 million acres in 2025, while Yara's Atfarm advised 1.2 million hectares in Europe, cutting nitrogen waste by 12% and spawning carbon credits priced at EUR 25 per metric ton (USD 27 per metric ton). Smartphone penetration in India and Indonesia is extending similar services to smallholders, and telematics are embedding Bayer's Climate FieldView across 4 million farms worldwide. Control of prescription data lets incumbents steer seed, fertilizer, and crop-protection mix, positioning platforms as profit centers equal in importance to active-ingredient pipelines.

Accelerating Phase-Outs of High-Toxicity Actives in the European Union, Brazil, and China

European Union proposals to retire 12 additional neonics and organophosphates by 2027, Brazil's reclassification of paraquat as "extremely toxic," and China's ban on 41 pesticide actives are shrinking registrant portfolios. Portfolio churn shortens effective patent lives for replacement molecules, forcing companies to accelerate product launches or pivot into biologicals to protect revenue. Smaller formulators, unable to fund reformulation, are exiting segments, further concentrating market power among diversified incumbents that can spread compliance costs.

Other drivers and restraints analyzed in the detailed report include:

- Controlled-Release and Inhibitor-Coated Fertilizers Gain Mainstream Adoption

- Carbon-Credit Monetization of Nitrogen-Efficiency Products

- Volatile Glyphosate Pricing Squeezes Formulator Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fertilizers dominated the agrochemicals market in 2025, holding 75% of revenue. Nitrogenous grades urea, ammonium nitrate, and Urea Ammonium Nitrate (UAN) solutions remain indispensable in cereal production across Asia-Pacific and North America. In contrast, plant growth regulators are forecast to post the fastest expansion at 13.0% CAGR, propelled by applications that synchronize flowering and extend shelf life in fruits and vegetables. Herbicides constitute a significant portion of pesticide value, reshaping product portfolios in regions with stringent zero-residue mandates. Adjuvants, though a small share, generate outsize strategic value because they reduce spray rates by up to 25%, preserving efficacy while easing regulatory pressure. Corteva Agriscience's ProGibb, a gibberellin-based regulator, recorded significant revenue in 2025, reflecting increasing demand for yield-enhancement molecules beyond traditional fertilizer expenditures. The agrochemicals market size for fertilizers is projected to grow steadily, with discretionary growth likely to center on high-margin regulators and other products that align with sustainability initiatives.

The ongoing phase-out of toxic active ingredients and the increasing preference for coated formulations enable companies to integrate fertilizer and crop protection solutions. Firms offering nutrient efficiency alongside pest control can cross-sell within the same acreage, strengthening relationships with channel partners and capturing additional market share. These trends allow agrochemical companies to maintain profitability despite fluctuations in commodity fertilizer cycles. Additionally, companies that validate environmental performance through third-party protocols are securing pricing premiums, indicating a long-term shift away from volume-based competition.

The Agrochemicals Market Report is Segmented by Product Type (Fertilizers, Pesticides, and More), by Crop Type (Grains and Cereals, Pulses and Oilseeds, Fruits and Vegetables, and Commercial Crops, and More), and by Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 53% of the agrochemicals market share in 2025 and is projected to grow at a CAGR of 6.6% through 2031. Key factors supporting baseline demand include China's zero-growth fertilizer mandate, which aims to stabilize fertilizer usage while maintaining agricultural productivity, and India's subsidized urea program, which ensures affordability for farmers and sustains demand. Additionally, Japan's precision agriculture platforms demonstrate how carbon monetization initiatives can incentivize the adoption of premium agricultural inputs, further driving market growth in the region. These developments position Asia-Pacific as a critical driver of the global agrochemicals market.

In Africa, digital advisory services are increasingly being adopted to enhance yields among smallholder farmers, addressing challenges such as restricted access to traditional inputs and climate variability. Egypt and South Africa stand out as anchor markets due to their well-developed irrigation infrastructure and focus on export-oriented horticulture, which supports higher-value crop production. Meanwhile, South America's market growth is primarily driven by Brazil's expanding soybean and corn acreage, supported by favorable climatic conditions and government policies, and Argentina's export-oriented agricultural practices, which emphasize competitiveness in global markets.

In North America, market growth reflects the challenges of mature acreage and the impact of litigation, yet advancements in data platforms and carbon programs are creating new service revenue opportunities for agrochemical companies. Europe's market growth is the slowest among regions, hindered by the Farm to Fork pesticide-reduction targets. However, the region is becoming a leader in adopting low-carbon fertilizers, supported by regulatory initiatives like the Carbon Border Adjustment Mechanism (CBAM). The Middle East is capitalizing on its low-cost natural gas resources to produce ammonia for export while actively exploring blue and green ammonia production pathways. These regional trends highlight that while Asia-Pacific dominates in absolute sales, Africa and South America offer significant growth opportunities, shaping expansion strategies in the agrochemicals market.

- Syngenta Group

- Bayer AG

- BASF SE

- Corteva Agriscience

- Nutrien Ltd.

- Yara International ASA

- Mosaic Company

- CF Industries Holdings Inc.

- UPL Ltd.

- FMC Corporation

- Sumitomo Chemical Co., Ltd.

- Nufarm Ltd.

- K+S Aktiengesellschaft

- ICL Group

- OCP Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence of Herbicide-Resistant Weeds Fuels Demand for Premium Herbicides

- 4.2.2 Precision Agriculture and Data Subscription Models Scale Globally

- 4.2.3 Major Pesticide Patent Cliff (2024-2028) Fuels Low-Cost Generic Uptake

- 4.2.4 Carbon-credit Monetization of Nitrogen-Efficiency Products

- 4.2.5 Controlled-release and Inhibitor-Coated Fertilizers Gain Mainstream Adoption

- 4.2.6 European Union Carbon Border Adjustment Mechanism (CBAM) and Similar Carbon Policies Accelerate Low-Carbon Ammonia Uptake

- 4.3 Market Restraints

- 4.3.1 Accelerating Phase-outs of High-toxicity Actives in the European Union, Brazil, and China

- 4.3.2 Volatile Glyphosate Pricing Squeezes Formulator Margins

- 4.3.3 Rising Regulatory Data-package and Re-registration Costs

- 4.3.4 Chronic Activist Litigation Risk in North America

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Fertilizers

- 5.1.1.1 Nitrogenous

- 5.1.1.2 Phosphatic

- 5.1.1.3 Potassic

- 5.1.1.4 Other Fertilizers

- 5.1.2 Pesticides

- 5.1.2.1 Herbicides

- 5.1.2.2 Insecticides

- 5.1.2.3 Fungicides

- 5.1.2.4 Other Pesticides

- 5.1.3 Adjuvants

- 5.1.4 Plant Growth Regulators

- 5.1.1 Fertilizers

- 5.2 By Crop Type

- 5.2.1 Grains and Cereals

- 5.2.2 Pulses and Oilseeds

- 5.2.3 Fruits and Vegetables

- 5.2.4 Commercial Crops

- 5.2.5 Turf and Ornamental

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Egypt

- 5.3.6.3 Rest of Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Syngenta Group

- 6.4.2 Bayer AG

- 6.4.3 BASF SE

- 6.4.4 Corteva Agriscience

- 6.4.5 Nutrien Ltd.

- 6.4.6 Yara International ASA

- 6.4.7 Mosaic Company

- 6.4.8 CF Industries Holdings Inc.

- 6.4.9 UPL Ltd.

- 6.4.10 FMC Corporation

- 6.4.11 Sumitomo Chemical Co., Ltd.

- 6.4.12 Nufarm Ltd.

- 6.4.13 K+S Aktiengesellschaft

- 6.4.14 ICL Group

- 6.4.15 OCP Group

7 Market Opportunities and Future Outlook

農藥市場:全球市場按產品類型、性質、作物類型、配方和應用進行預測 - 2026-2032年農藥儲槽市場:2026-2032年全球市場預測(依儲槽類型、材質、容量、運作模式、壓力類型、移動性、應用、最終用戶和通路分類)

農藥市場:全球市場按產品類型、性質、作物類型、配方和應用進行預測 - 2026-2032年農藥儲槽市場:2026-2032年全球市場預測(依儲槽類型、材質、容量、運作模式、壓力類型、移動性、應用、最終用戶和通路分類) 農藥市場規模、佔有率、趨勢和預測:按肥料類型、農藥類型、作物類型和地區分類,2026-2034年

農藥市場規模、佔有率、趨勢和預測:按肥料類型、農藥類型、作物類型和地區分類,2026-2034年 農業化學品市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場分類的預測(2026-2033 年)

農業化學品市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場分類的預測(2026-2033 年) 全球農業化學品儲罐市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球農業化學品儲罐市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球農藥市場報告氟嘧啶市場:2026-2032年全球市場預測(按劑型、作物類型、施用方法、分銷管道和最終用戶分類)

2026年全球農藥市場報告氟嘧啶市場:2026-2032年全球市場預測(按劑型、作物類型、施用方法、分銷管道和最終用戶分類) 銅肥市場規模、佔有率和成長分析:按產品類型、配方類型、應用類型、最終用戶和地區分類 - 2026-2033 年產業預測

銅肥市場規模、佔有率和成長分析:按產品類型、配方類型、應用類型、最終用戶和地區分類 - 2026-2033 年產業預測 作物保護市場分析及預測(至2035年):依類型、產品類型、應用、技術、形式、最終用戶、服務、實施類型、功能及解決方案分類全球農業化學品市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

作物保護市場分析及預測(至2035年):依類型、產品類型、應用、技術、形式、最終用戶、服務、實施類型、功能及解決方案分類全球農業化學品市場規模、佔有率、趨勢和成長分析報告(2026-2034年)