|

市場調查報告書

商品編碼

1850010

美國壓力感測器:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)US Pressure Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

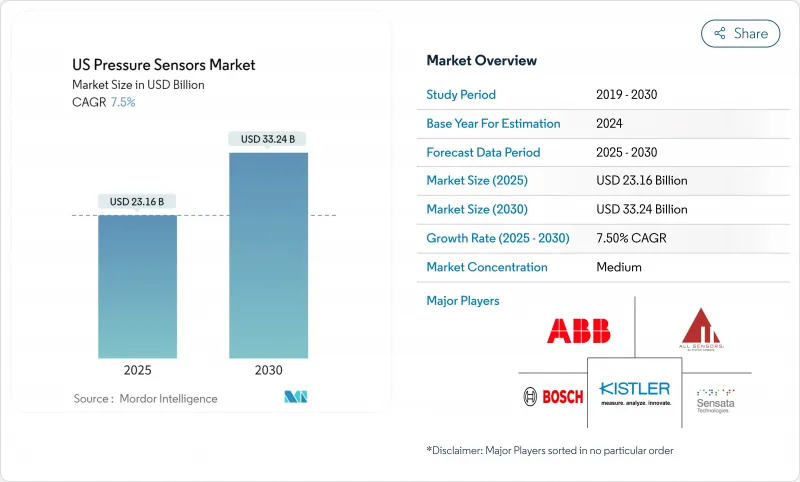

美國壓力感測器市場預計到 2025 年將達到 231.6 億美元,到 2030 年將達到 332.4 億美元,年複合成長率為 7.50%。

半導體製造商正推動這一擴張的很大一部分,因為半導體晶圓廠將真空和氣體控制的公差提高到滿量程的±0.05%甚至更低。儘管汽車、醫療和液化天然氣基礎設施領域安全法規的日益嚴格給供應鏈帶來了壓力,但需求仍然保持強勁。 MEMS和NEMS平台的融合正在重塑成本曲線,奈米級裝置正在樹立新的精確度標準,同時也更容易整合到人工智慧模組中。電池供電的物聯網系統正在推動電容式設計的應用,這種設計兼具低功耗和溫度穩定性。從區域來看,南方地區憑藉其能源成本優勢吸引了新的晶圓廠,而氦氣短缺則迫使封裝技術進行創新,以提高長期密封性。

美國壓力感測器市場趨勢與洞察

胎壓監測系統 (TPMS) 更換週期驅動售後市場需求

隨著第一代胎壓監測系統(TPMS)的使用壽命接近尾聲,感測器供應商正迎來回頭客。 2007年《輪胎磨損法案》(TREAD Act)實施後生產的車輛正進入第二或第三次更換週期,而美國東北部和中西部地區冬季道路融雪劑的使用加速了電池損耗。 Bartec Auto ID 推出的2025款Rite-SensorBlue®專為特斯拉車型設計,並新增了藍牙診斷功能,這標誌著TPMS正朝著延長保養週期的電動車最佳化方向發展。這些設備內建的預測性警報功能正推動售後市場從被動更換轉向定期維護,從而支撐起更高的價格分佈。

醫療保險對家用血壓監測儀的報銷

聯邦醫療保險和醫療補助計劃的覆蓋範圍已擴大,目前已覆蓋84%的家用血壓監測儀,惠及約140萬高血壓患者。密西根州的計畫為每個設備支付最高75美元,樹立了全國價格標竿。這種報銷政策正在推動市場對可靠的低壓感測器的快速需求,這些感測器可以裝入小巧的臂帶中,並將數據傳輸到遠端醫療平台。

智慧型手機市場飽和度

由於氣壓感測器現在幾乎被所有中高階行動電話所採用,限制了消費性電子產品的銷售成長,製造商正專注於差異化功能,例如穿戴式裝置的超低功耗和無人機的高精度高度計,以吸引集中在西海岸供應鏈成熟領域的細分市場。

細分市場分析

到2024年,MEMS將佔據美國壓力感測器市場31.05%的佔有率,為主流汽車和工業設計提供動力。產量比率的矽生產線降低了單位成本,而石墨烯薄膜將靈敏度提升至66µV/V/kPa,提高了高度計和醫療穿戴式裝置的精確度。應變計裝置在石油上游等嚴苛環境中仍備受青睞,碳化矽設計可在600°C下可靠運作。光學感測器在強電磁場環境中具有優勢。

隨著代工廠採用共用模具,生產規模將縮小微機電系統(MEMS)與微型機電系統(MEMS)之間的成本差距,並促進其在醫療拋棄式批量生產中的應用。因此,美國壓力感測器市場將逐步融合微型和奈米技術,形成包含人工智慧和資料加密等技術的混合型模組。

到2024年,壓阻式架構將佔據46.00%的營收佔有率,因為該架構允許製造商復用成熟的CMOS後端製程。近期碳化矽技術的改進已將零功耗溫度係數降低至每攝氏度0.08%,滿足了嚴苛的油田和航太應用的需求。 ASIC中嵌入的多項式迴歸演算法將殘差降低至0.008%FS,從而滿足關鍵任務的精確度要求。

電容式感測技術預計將以 10.20% 的複合年成長率成長,其卓越的能源效率對於電池供電的物聯網節點至關重要。 ES Systems 於 2024 年推出的產品總誤差僅為 ±0.25% FS,並提供 I2C、SPI 和類比輸出介面。諧振式真空計仍是一種特殊真空計,用於測量半導體腔室壓力,解析度可達 0.1 Pa。隨著供應商將多種技術整合到單一封裝中,美國壓力感測器市場將出現競爭重疊,這將使 OEM 廠商能夠根據特定應用的需求客製化效能。

美國壓力感測器市場報告按感測器類型(MEMS、應變計、其他)、技術(壓阻式、電容式、其他)、輸出介面、壓力範圍、應用(汽車、醫療、工業、家電、其他)和美國地區(東北部、中西部、其他)進行細分。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 胎壓監測系統 (TPMS) 更換週期驅動售後市場需求

- 醫療保險對家用血壓監測儀的報銷

- OSHA液化天然氣連續測井需求

- 半導體工廠對超高精度的需求

- 市場限制

- 智慧型手機市場飽和度

- 氦氣短缺推高了MEMS封裝成本

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依感測器類型

- MEMS

- 應變計

- NEMS

- 光學

- 透過技術

- 壓阻式

- 電容式

- 共振類型

- 其他

- 透過輸出介面

- 模擬

- 數位式(IC/SPI)

- 按壓力範圍

- 低於 10 kPa(低)

- 10 kPa 1 MPa(中壓)

- 超過 1 兆帕(高)

- 透過使用

- 車

- 醫療保健

- 家用電器

- 產業

- 航太與國防

- 飲食

- HVAC

- 其他

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Honeywell International Inc.

- Sensata Technologies Inc.

- Bosch Sensortec GmbH

- Emerson Electric Co.(Rosemount)

- ABB Ltd.

- Infineon Technologies AG

- STMicroelectronics NV

- Tektronix-Kistler Group

- NXP Semiconductors NV

- Panasonic Industry Co.

- TE Connectivity Ltd.

- Omron Corporation

- Pressure Systems Inc.

- All Sensors Corp.

- Endress+Hauser AG

- Rockwell Automation Inc.

- Yokogawa Electric Corp.

- Siemens AG

- Kulite Semiconductor Products Inc.

- TDK-Invensense Inc.

第7章 市場機會與未來展望

The US pressure sensors market is valued at USD 23.16 billion in 2025 and is projected to climb to USD 33.24 billion by 2030, advancing at a 7.50% CAGR.

Semiconductor manufacturers are driving a large share of this expansion as fabs tighten vacuum and gas control tolerances below +-0.05% full scale. Heightened safety rules in automotive, medical, and LNG infrastructure keep demand resilient even when supply chains face stress. The convergence of MEMS and NEMS platforms is reshaping cost curves, with nanoscale devices setting new accuracy benchmarks while easing integration into AI-ready modules. Battery-powered IoT systems are pushing adoption of capacitive designs that combine low power with temperature stability. Regionally, the South benefits from energy-cost advantages that attract new plants, while helium scarcity is forcing packaging innovation that improves long-term hermeticity.

US Pressure Sensors Market Trends and Insights

TPMS Replacement Cycle Accelerates Aftermarket Demand

First-generation mandatory Tire Pressure Monitoring Systems are now reaching end-of-life, creating repeat business for sensor suppliers. Vehicles built after the 2007 TREAD Act are entering second and third replacement cycles, and winter road-salt exposure in the Northeast and Midwest quickens battery depletion. Bartec Auto ID's 2025 Rite-SensorBlue(R), tailored for Tesla models, illustrates the shift toward EV-optimized TPMS that adds Bluetooth diagnostics and extends service intervals. Predictive alerts embedded in these units move the aftermarket from reactive swaps to scheduled maintenance, supporting premium price points.

Medicare Reimbursement for Home BP Monitors

Expanded Medicare and Medicaid coverage now reaches 84% of state plans for self-measured blood pressure devices, opening access for about 1.4 million beneficiaries with hypertension. Michigan's program pays up to USD 75 per device, setting a national pricing anchor. This reimbursement landscape fuels rapid demand for reliable low-pressure sensors that fit in compact arm-cuffs while streaming data into telehealth platforms.

Smart-Phone Barometer Saturation

Nearly every mid-to-high-tier handset now ships with a barometric sensor, capping volume growth in consumer electronics. Manufacturers pivot toward differentiated performance such as ultra-low-power variants for wearables or high-precision altimeters for drones, carving niche gains in an otherwise mature space concentrated in West Coast supply chains.

Other drivers and restraints analyzed in the detailed report include:

- OSHA LNG Continuous-Logging Mandate

- Semiconductor-Fab Ultra-High-Accuracy Demand

- Helium Shortage Inflates MEMS Packaging Cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

MEMS held 31.05% of the US pressure sensors market share in 2024 and underpin mainstream automotive and industrial designs. Yield-optimized silicon lines keep unit costs low, while graphene membranes now lift sensitivity to 66 µV/V/kPa, enhancing resolution for altimeters and medical wearables. Strain-gauge devices remain favored in harsh settings such as upstream oil where silicon carbide variants work reliably at 600 °C. Optical sensors gain ground in environments with strong electromagnetic fields.

As foundries deploy shared tooling, production scale will narrow cost gaps with MEMS, opening broader adoption in high-volume medical disposables. The US pressure sensors market will therefore see a gradual blend of micro and nano formats in mixed-technology modules that embed AI and data encryption.

Piezoresistive architectures led with 46.00% revenue share in 2024 because manufacturers can reuse mature CMOS back-end steps. Recent silicon-carbide revisions cut the temperature coefficient of zero output to 0.08% per °C, fitting harsh oilfield or aerospace needs. Polynomial-regression algorithms embedded in ASICs trim residual errors to 0.008% FS, aligning accuracy with mission-critical expectations.

Capacitive sensing, projected to rise at a 10.20% CAGR, provides superior energy efficiency vital for battery-powered IoT nodes. ES Systems' 2024 release achieves +-0.25% FS total error while offering I2C, SPI, and analog outputs. Resonant techniques stay in specialty vacuum gauges where 0.1 Pa resolution guides semiconductor chamber pressure. The US pressure sensors market will see competitive overlap as vendors integrate multiple technologies into single packages that let OEMs dial performance to application-specific thresholds.

The United States Pressure Sensors Market Report is Segmented by Sensor Type (MEMS, Strain-Gauge and More), Technology (Piezoresistive, Capacitive and More), Output Interface, Pressure Range, Application (Automotive, Medical, Industrial, Consumer Electronics and More), US Region (Northeast, Midwest and More)

List of Companies Covered in this Report:

- Honeywell International Inc.

- Sensata Technologies Inc.

- Bosch Sensortec GmbH

- Emerson Electric Co. (Rosemount)

- ABB Ltd.

- Infineon Technologies AG

- STMicroelectronics NV

- Tektronix-Kistler Group

- NXP Semiconductors NV

- Panasonic Industry Co.

- TE Connectivity Ltd.

- Omron Corporation

- Pressure Systems Inc.

- All Sensors Corp.

- Endress+Hauser AG

- Rockwell Automation Inc.

- Yokogawa Electric Corp.

- Siemens AG

- Kulite Semiconductor Products Inc.

- TDK-Invensense Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 TPMS replacement cycle accelerates aftermarket demand

- 4.2.2 Medicare reimbursement for home BP monitors

- 4.2.3 OSHA LNG continuous?logging mandate

- 4.2.4 Semiconductor-fab ultra-high-accuracy demand

- 4.3 Market Restraints

- 4.3.1 Smart-phone barometer saturation

- 4.3.2 Helium shortage inflates MEMS packaging cost

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Sensor Type

- 5.1.1 MEMS

- 5.1.2 Strain-Gauge

- 5.1.3 NEMS

- 5.1.4 Optical

- 5.2 By Technology

- 5.2.1 Piezoresistive

- 5.2.2 Capacitive

- 5.2.3 Resonant

- 5.2.4 Others

- 5.3 By Output Interface

- 5.3.1 Analog

- 5.3.2 Digital (IC/SPI)

- 5.4 By Pressure Range

- 5.4.1 <10 kPa (Low)

- 5.4.2 10 kPa 1 MPa (Medium)

- 5.4.3 >1 MPa (High)

- 5.5 By Application

- 5.5.1 Automotive

- 5.5.2 Medical

- 5.5.3 Consumer Electronics

- 5.5.4 Industrial

- 5.5.5 Aerospace & Defence

- 5.5.6 Food & Beverage

- 5.5.7 HVAC

- 5.5.8 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Honeywell International Inc.

- 6.4.2 Sensata Technologies Inc.

- 6.4.3 Bosch Sensortec GmbH

- 6.4.4 Emerson Electric Co. (Rosemount)

- 6.4.5 ABB Ltd.

- 6.4.6 Infineon Technologies AG

- 6.4.7 STMicroelectronics NV

- 6.4.8 Tektronix-Kistler Group

- 6.4.9 NXP Semiconductors NV

- 6.4.10 Panasonic Industry Co.

- 6.4.11 TE Connectivity Ltd.

- 6.4.12 Omron Corporation

- 6.4.13 Pressure Systems Inc.

- 6.4.14 All Sensors Corp.

- 6.4.15 Endress+Hauser AG

- 6.4.16 Rockwell Automation Inc.

- 6.4.17 Yokogawa Electric Corp.

- 6.4.18 Siemens AG

- 6.4.19 Kulite Semiconductor Products Inc.

- 6.4.20 TDK-Invensense Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space & Unmet-need Assessment

壓力感測器市場規模、佔有率、趨勢和預測:按產品、類型、技術、應用和地區分類,2026-2034年

壓力感測器市場規模、佔有率、趨勢和預測:按產品、類型、技術、應用和地區分類,2026-2034年 壓力感測器市場:2026-2030年全球市場預測,依產品、類型、技術、壓力範圍、應用和用例分類

壓力感測器市場:2026-2030年全球市場預測,依產品、類型、技術、壓力範圍、應用和用例分類 2026年全球壓電壓力感測器市場報告差壓密度計市場:依產品類型、通訊協定、精確度等級及最終用途產業分類-全球預測,2026-2032年差壓式線上密度計市場:按安裝類型、精度等級、輸出類型、最終用戶產業和應用分類-全球預測,2026-2032年

2026年全球壓電壓力感測器市場報告差壓密度計市場:依產品類型、通訊協定、精確度等級及最終用途產業分類-全球預測,2026-2032年差壓式線上密度計市場:按安裝類型、精度等級、輸出類型、最終用戶產業和應用分類-全球預測,2026-2032年 壓力感測器市場分析及預測(至2035年):依類型、產品類型、技術、應用、材質、最終用戶、組件、安裝類型及功能分類

壓力感測器市場分析及預測(至2035年):依類型、產品類型、技術、應用、材質、最終用戶、組件、安裝類型及功能分類 全球壓力感測器市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球壓力感測器市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 全球壓力感測器市場:產業分析、市場規模、佔有率及預測(按產品、類型、技術、應用、國家和地區分類)(2025-2032 年)2026年全球壓力感測器市場報告2026年全球流體壓力感測器市場報告

全球壓力感測器市場:產業分析、市場規模、佔有率及預測(按產品、類型、技術、應用、國家和地區分類)(2025-2032 年)2026年全球壓力感測器市場報告2026年全球流體壓力感測器市場報告