|

市場調查報告書

商品編碼

1849995

家居護理包裝:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Home Care Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

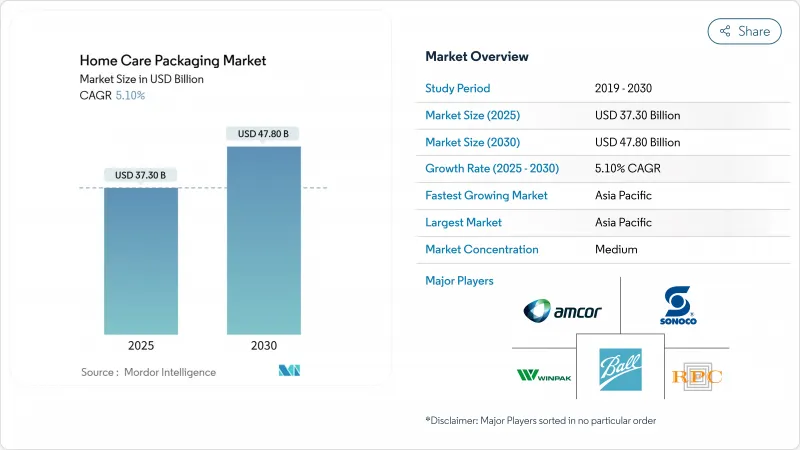

預計到 2025 年,家居護理包裝市場規模將達到 373 億美元,到 2030 年將擴大到 478 億美元,複合年成長率為 5.10%。

這一成長反映了衛生用品需求的穩定、電子商務的日益普及以及對永續解決方案的政策支持。歐盟的《包裝和包裝廢棄物條例》於2025年2月生效,規定到2030年所有包裝都必須可回收。材料價格的波動,尤其是聚乙烯和聚丙烯的價格波動,導致成本波動,但也刺激了輕量化和生物基創新。亞太地區由於都市化進程加快和可支配收入增加而繼續佔據主導地位,而中東地區則在經濟多元化的推動下實現了最快的成長。以安姆科以84億美元收購貝瑞全球為例,企業整合表明,生產商正努力擴大規模,以應對原料價格上漲和即將到來的生產者延伸責任(EPR)費用。

全球居家護理包裝市場趨勢與洞察

提高優質化,以品牌主導的SKU擴張

消費者對高階清潔產品的需求正推動包裝創新超越功能性包裝的範疇。各大品牌正運用先進的阻隔層、智慧封口和獨特的美學設計來支撐其高價格分佈。例如,將於2024年上市的汰漬evo纖維片,採用可溶解的六層纖維結構而非塑膠,旨在吸引注重品質的消費者。預計到2027年,中東地區的美容產品支出將達到470億美元,居家護理包裝的支出也將呈現類似的成長趨勢。分配器和特種封口製造商將從中受益,Silgan公司2024年第四季的銷售額飆升至6.394億美元印證了這一點。優質化同時也推動了更小巧、更具設計感的產品規格的出現,從而增強了利潤率對樹脂成本波動的抵禦能力。這一趨勢正在重塑已開發市場和新興市場家居護理包裝市場的貨架競爭格局。

循環經濟強制要求使用可回收的單一材料包裝

監管機構正敦促生產商設計更易於回收的產品。歐盟的《塑膠包裝再利用條例》(PPWR) 規定,到2030年實現100%可回收, 寶特瓶的回收率需達到30%,這鼓勵了單一材料結構轉變。聯合利華的紙基清潔劑瓶清楚地展示了企業研發如何與即將到來的配額目標保持一致。目前已有63個國家建立了正式的生產者責任延伸制度(EPR),將處置成本從市政當局轉移到生產商,並獎勵可回收設計。專注於單一材料薄膜的加工商將獲得定價權,而多層阻隔膜供應商將被迫重組,否則將面臨訂單量下降。從長遠來看,合規投資有望穩定並支持更廣泛的家庭護理包裝市場的發展軌跡。

石化樹脂價格波動

聚乙烯和聚丙烯價格波動加劇,擠壓加工商的利潤空間,並使定價策略更加複雜。受停產和原物料成本上漲的影響,聚乙烯價格在2024年至2025年間多次上漲,每次上漲幅度為5美分/磅。受熱帶風暴阿爾貝托造成的供應中斷影響,聚對苯二甲酸乙二醇酯(PET)價格上漲了1.1%。小型加工商缺乏避險工具,被迫在家庭護理包裝市場面臨成本轉嫁和利潤壓力。價格波動加速了人們對輕量化和替代基材的興趣。能夠加速向生物基和再生材料轉型的加工商可以緩解石化燃料價格波動帶來的影響。

細分市場分析

到2024年,塑膠將佔據家居護理包裝市場63.00%的佔有率,凸顯其在經濟高效、阻隔性性能優異的應用領域中根深蒂固的地位。該行業持續受益於成熟的供應鏈和多樣化的加工技術。然而,生質塑膠以12.10%的複合年成長率,在設計討論中佔據主導地位,因為監管機構和品牌商都優先考慮可再生原料。

由於紙張和紙板具有高回收性和低碳足跡,它們的重要性再次凸顯,但其重量和對濕度的敏感性使其在液體清潔劑領域仍未廣泛應用。金屬在加壓氣霧劑這一細分市場仍然佔據重要地位,而玻璃則由於在電子商務中易碎而使用較少。生質塑膠的發展勢頭正推動著對聚乳酸(PLA)和聚羥基脂肪酸酯(PHA)樹脂的投資,加工商正在試驗滿足氧氣阻隔要求的單一材料薄膜。隨著再生材料含量法規的日益嚴格,PCR樹脂與生物基樹脂的相容性混合物可以增強市場供應的穩定性和成本競爭力。

到2024年,瓶裝和硬質容器將佔家居護理包裝市場規模的47.00%,這反映了傳統生產線的存在以及消費者對傳統包裝形式的熟悉程度。輕量HDPE和寶特瓶因其優異的抗摔性和品牌識別功能而依然備受歡迎。然而,填充用填充的包裝袋和分配器系統正以9.90%的複合年成長率快速成長,憑藉其材料節約和循環利用的便利性,重新定義了包裝的價值提案。 Aptar公司用於皮膚化妝品的可回收真空瓶和B-CAP公司的環保計量瓶蓋,都展現了技術創新如何使現有包裝形式煥發新生。

包裝袋能夠提高物流效率,減輕貨物重量和體積,這對電子商務的盈利至關重要。可重複使用的分配器和輕巧的填充用小袋能夠減少生命週期排放,並與生產者責任延伸(EPR)收費系統相契合;而金屬罐和條狀包裝則繼續用於需要特殊配送方式的特種清潔產品。在所有類型的包裝中,加工商都在整合QR碼以引導回收,這不僅方便消費者加入循環經濟計劃,還提高了合規指標,從而支持家居護理包裝市場的未來成長。

這份家居護理包裝市場報告按材料(例如塑膠、紙張)、包裝類型(例如瓶裝和硬質容器、軟袋)、產品類型(例如洗潔精、殺蟲劑)、外形規格(例如液體、粉末)和地區對行業進行細分。市場預測以美元計價。

區域分析

受中國、印度和東南亞地區快速都市化、電子商務成長以及中階不斷壯大的推動,亞太地區預計到2024年將佔據全球家居護理包裝市場38.70%的佔有率。中國關於食品接觸塑膠回收的法規即將生效,這將為該地區樹立新的合規標竿。日本人口老化將推動市場對易拉包裝和適合小家庭使用的單劑量清潔劑的需求。預計到2024年,亞太地區包裝器材投資將超過180億美元,有助於加工商擴大生產規模。

中東將成為成長最快的地區,到2030年複合年成長率將達到7.80%,主要得益於海灣合作波灣合作理事會)市場的優質化。到2027年,該地區的美容和個人護理支出將達到470億美元,主要受高階家居護理套裝需求的推動。炎熱的氣候需要更強的阻隔性和抗紫外線顏料,這也影響了供應商的產品規格。沙烏地阿拉伯佔海灣合作理事會藥品銷售額的34.6%,凸顯了衛生初級包裝的巨大市場潛力。

北美和歐洲市場依然重要,但監管環境日趨嚴格。光是歐盟的PPWR(包裝材料回收條例)就迫使全球品牌所有者不得不增加重新設計預算。同時,奧勒岡州和科羅拉多將於2025年7月前實施EPR(生產者責任延伸)計劃,擴大生產者自籌資金的回收模式。拉丁美洲市場展現出新的潛力。根據fastmarkets.com網站預測,原物料成本上漲將推動紙盒價格在2025年上漲,這標誌著市場走向成熟。各地區的法規和消費行為正在潛移默化地改變整個家居護理包裝市場的成長軌跡。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 優質化和品牌主導SKU數量的增加

- 可回收單一材料包裝的循環經濟義務

- 電子商務的蓬勃發展推動了對耐損格式的需求。

- 亞洲都市區家庭喜歡方便的單份包裝。

- 物聯網賦能的智慧分配器與補充裝生態系統

- 市場限制

- 石化樹脂價格波動

- 歐洲的生產者延伸責任制(EPR)費用

- 品牌承諾所需的食品級PCR樹脂短缺

- 監管環境

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模及成長預測(數值)

- 材料

- 塑膠

- 紙張和紙板

- 金屬

- 玻璃

- 生質塑膠

- 按包裝類型

- 瓶子和硬質容器

- 小袋和袋子

- 紙箱和瓦楞紙箱

- 金屬罐和氣霧劑

- 填充用袋和分發系統

- 條狀包裝和小袋

- 按產品類型

- 衣物洗護

- 洗碗

- 表面清潔劑和廁所清潔劑

- 空氣清淨

- 殺蟲劑

- 研磨劑和特殊清潔劑

- 按外形規格

- 液體

- 粉末

- 膠囊/片劑

- 凝膠

- 噴霧/泡沫

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 亞太其他地區

- 中東

- 以色列

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Amcor plc

- Ball Corporation

- RPC Group(Berry Global)

- Winpak Ltd

- Aptar Group Inc.

- Sonoco Products Company

- Silgan Holdings

- Constantia Flexibles GmbH

- DS Smith plc

- Can-Pack SA

- ProAmpac LLC

- Berry Global Group

- Mondi plc

- Huhtamaki Oyj

- Smurfit Kappa Group

- Sealed Air Corp.

- WestRock Company

- Albea Group

- Gerresheimer AG

- Tetra Pak

第7章 市場機會與未來展望

The home care packaging market reached USD 37.3 billion in 2025 and is forecast to advance to USD 47.8 billion by 2030, translating into a 5.10% CAGR.

This expansion reflects steady demand for hygiene products, widening e-commerce penetration, and policy support for sustainable solutions. Momentum is reinforced by the European Union's Packaging and Packaging Waste Regulation, effective February 2025, which requires all packs to be recyclable by 2030. Material-price swings, especially in polyethylene and polypropylene, add cost volatility yet stimulate lightweighting and bio-based innovation. Asia-Pacific retains dominance thanks to urbanisation and rising disposable incomes, while the Middle East posts the quickest regional growth on the back of economic diversification. Corporate consolidation-illustrated by Amcor's USD 8.4 billion takeover of Berry Global-signals a push for scale as producers tackle raw-material inflation and looming Extended Producer Responsibility (EPR) fees.

Global Home Care Packaging Market Trends and Insights

Rising Premiumisation and Brand-Led SKU Proliferation

Demand for upscale cleaning products drives packaging innovation beyond functional containment. Brands deploy advanced barriers, smart closures, and distinctive aesthetics to justify higher price points. Tide evo fibre tiles, launched in 2024, replace plastic with a dissolvable six-layer fibre structure and target premium shoppers. Middle East beauty spending, set to hit USD 47 billion by 2027, fuels similar expectations for home-care packs. Manufacturers of dispensing and specialty closures benefit, as evidenced by Silgan's Q4 2024 sales jump to USD 639.4 million. Premiumisation simultaneously promotes smaller, design-rich formats and boosts margin resilience against resin cost swings. The trend cuts across developed and emerging markets, reshaping shelf competition within the home care packaging market.

Circular-Economy Mandates for Recyclable Mono-Material Packs

Regulators push producers toward designs that enable straightforward recycling. The EU's PPWR stipulates 100% recyclability by 2030 and 30% recycled content for single-use plastic beverage bottles, compelling shifts to mono-material structures. Unilever's paper-based detergent bottle underscores how corporate R&D aligns with looming quotas. Sixty-three countries now run formal EPR schemes, moving disposal costs from municipalities to producers and rewarding design-for-recycling approaches. Converters positioned in mono-material films gain pricing power, whereas multi-layer barrier suppliers must retool or face declining order books. Over the long term, compliance investments are expected to stabilise and support the broader home care packaging market trajectory.

Petro-chemical Resin Price Volatility

Fluctuating polyethylene and polypropylene prices compress converter margins and complicate pricing strategy. PE registered several 5 ¢/lb hikes in 2024 - 2025 due to outages and feedstock spikes. PET saw a 1.1% jump after Tropical Storm Alberto disrupted supply. Smaller converters lack hedging tools, forcing cost-pass through or margin erosion in the home care packaging market. Volatility accelerates interest in lightweighting and alternative substrates. Converters able to shift to bio-based or recycled inputs faster can cushion against fossil-fuel price swings.

Other drivers and restraints analyzed in the detailed report include:

- E-commerce Boom Accelerating Demand for Shatter-Proof Formats

- Urban Asian Households Favouring Single-Dose Convenience Packs

- Extended-Producer-Responsibility Fees in Europe

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastics captured 63.00% of the home care packaging market share in 2024, underlining their entrenched role in cost-effective, barrier-rich applications. The segment continues to leverage mature supply chains and versatile processing techniques. However, bioplastics, propelled by a 12.10% CAGR, increasingly command design conversations as regulators and brands prioritise renewable feedstocks.

Paper and paperboard regain relevance through high recycling rates and lower carbon footprints, yet weight and moisture sensitivity keep them from mainstream liquid detergents. Metal retains niche importance in pressurised aerosols, and glass sees marginal use due to breakage risks in e-commerce. Bioplastics' momentum spurs investment in PLA and PHA resins, with converters trialling mono-material films that still meet oxygen-barrier demands. As recycled-content mandates tighten, compatibilised blends of PCR and bio-based inputs can bolster supply stability and cost competitiveness for the home care packaging market.

Bottles and rigid containers accounted for 47.00% of the home care packaging market size in 2024, reflecting legacy production lines and consumer familiarity with traditional formats. Lightweight HDPE and PET bottles remain prevalent thanks to excellent drop-impact resistance and brand-billboard capability. Yet refill pouches and dispensing systems, expanding at a 9.90% CAGR, are redefining value propositions through material savings and circular-loop convenience. Aptar's recyclable airless bottle for dermocosmetics and B-CAP's eco dosing cap demonstrate how innovation modernises even established formats.

Pouches deliver logistics efficiencies, shaving freight weight and cubic volume, crucial for e-commerce profitability. Reusable dispensers coupled with lightweight refill sachets reduce life-cycle emissions, resonating with EPR fee structures. Meanwhile, metal cans and stick packs maintain roles in specialty cleaners requiring specific delivery modes. Across all types, converters integrate QR codes for recycling instructions, aiming to ease consumer participation in circular schemes and boost compliance metrics that underpin the future growth of the home care packaging market.

Home Care Packaging Market Report Segments the Industry Into Material (Plastic, Paper and More), Packaging Type (Bottles and Rigid Containers, Pouches and Bags and More), Product Category (Dishwashing, Insecticides and More), Form Factor(Liquids, Powders and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated with 38.70% home care packaging market share in 2024, reflecting rapid urbanisation, e-commerce growth, and middle-class expansion in China, India, and Southeast Asia. China's forthcoming rules for recycled food-contact plastics will set new compliance benchmarks regionally. Japan's ageing society drives demand for easy-open packs and single-dose detergents suited to smaller households. Investment in regional packaging machinery is forecast to surpass USD 18 billion by 2024, underpinning scale-up for converters.

The Middle East is the fastest-growing territory, with a 7.80% CAGR through 2030, supported by premiumisation in Gulf Cooperation Council markets. Regional beauty and personal-care outlays-from which spillover demand for upscale home-care packs emerges-will hit USD 47 billion by 2027. Hot climates necessitate barrier enhancements and UV-stable pigments, shaping supplier specifications. Saudi Arabia's 34.6% share of GCC pharmaceutical sales highlights parallel opportunities for hygienic primary packs.

North America and Europe remain pivotal yet face tightening regulatory nets. The EU PPWR alone drives redesign budgets for global brand owners. Meanwhile, Oregon and Colorado introduce EPR schemes by July 2025, broadening producer-funded recycling models. Latin America shows emerging promise: higher raw-material costs push paper-pack prices up in 2025, signalling market maturation fastmarkets.com. Collectively, region-specific rules and consumer behaviours maintain nuanced growth paths across the home care packaging market.

- Amcor plc

- Ball Corporation

- RPC Group (Berry Global)

- Winpak Ltd

- Aptar Group Inc.

- Sonoco Products Company

- Silgan Holdings

- Constantia Flexibles GmbH

- DS Smith plc

- Can-Pack SA

- ProAmpac LLC

- Berry Global Group

- Mondi plc

- Huhtamaki Oyj

- Smurfit Kappa Group

- Sealed Air Corp.

- WestRock Company

- Albea Group

- Gerresheimer AG

- Tetra Pak

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising premiumisation and brand-led SKU proliferation

- 4.2.2 Circular-economy mandates for recyclable mono-material packs

- 4.2.3 E-commerce boom accelerating demand for shatter-proof formats

- 4.2.4 Urban Asian households favouring single-dose convenience packs

- 4.2.5 IoT-enabled smart dispensers and refill ecosystems

- 4.3 Market Restraints

- 4.3.1 Petro-chemical resin price volatility

- 4.3.2 Extended-producer-responsibility (EPR) fees in Europe

- 4.3.3 Scarcity of food-grade PCR resin for brand pledges

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Material

- 5.1.1 Plastics

- 5.1.2 Paper and Paperboard

- 5.1.3 Metal

- 5.1.4 Glass

- 5.1.5 Bioplastics

- 5.2 By Packaging Type

- 5.2.1 Bottles and Rigid Containers

- 5.2.2 Pouches and Bags

- 5.2.3 Cartons and Corrugated Boxes

- 5.2.4 Metal Cans and Aerosols

- 5.2.5 Refill Pouches and Dispensing Systems

- 5.2.6 Stick Packs and Sachets

- 5.3 By Product Category

- 5.3.1 Laundry Care

- 5.3.2 Dishwashing

- 5.3.3 Surface and Toilet Cleaners

- 5.3.4 Air Care

- 5.3.5 Insecticides

- 5.3.6 Polishes and Specialty Cleaners

- 5.4 By Form Factor

- 5.4.1 Liquids

- 5.4.2 Powders

- 5.4.3 Capsules/Tabs

- 5.4.4 Gels

- 5.4.5 Sprays/Foams

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Israel

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Turkey

- 5.5.5.5 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Ball Corporation

- 6.4.3 RPC Group (Berry Global)

- 6.4.4 Winpak Ltd

- 6.4.5 Aptar Group Inc.

- 6.4.6 Sonoco Products Company

- 6.4.7 Silgan Holdings

- 6.4.8 Constantia Flexibles GmbH

- 6.4.9 DS Smith plc

- 6.4.10 Can-Pack SA

- 6.4.11 ProAmpac LLC

- 6.4.12 Berry Global Group

- 6.4.13 Mondi plc

- 6.4.14 Huhtamaki Oyj

- 6.4.15 Smurfit Kappa Group

- 6.4.16 Sealed Air Corp.

- 6.4.17 WestRock Company

- 6.4.18 Albea Group

- 6.4.19 Gerresheimer AG

- 6.4.20 Tetra Pak

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

居家照護包裝市場:按產品類型、材料類型、分銷管道和最終用戶分類-2026-2032年全球市場預測

居家照護包裝市場:按產品類型、材料類型、分銷管道和最終用戶分類-2026-2032年全球市場預測 居家照護包裝市場規模、佔有率、趨勢和預測:按產品類型、材料、包裝形式和地區分類,2026-2034年

居家照護包裝市場規模、佔有率、趨勢和預測:按產品類型、材料、包裝形式和地區分類,2026-2034年 快速消費品包裝市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年日常消費品包裝市場規模、佔有率、趨勢及預測(按包裝類型、材料、最終用途行業和地區分類,2026-2034年)

快速消費品包裝市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年日常消費品包裝市場規模、佔有率、趨勢及預測(按包裝類型、材料、最終用途行業和地區分類,2026-2034年) 2026年全球居家護理產品包裝市場報告月餅包裝市場:2026-2032年全球預測(按包裝類型、材料、包裝形式、印刷技術、最終用戶和分銷管道分類)

2026年全球居家護理產品包裝市場報告月餅包裝市場:2026-2032年全球預測(按包裝類型、材料、包裝形式、印刷技術、最終用戶和分銷管道分類) 歐洲消費品包裝市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)居家護理包裝市場-2026-2031年預測

歐洲消費品包裝市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)居家護理包裝市場-2026-2031年預測 家居護理包裝市場規模、佔有率及成長分析(按材料、產品類型、包裝類型、最終用途和地區分類)-產業預測(2026-2033)

家居護理包裝市場規模、佔有率及成長分析(按材料、產品類型、包裝類型、最終用途和地區分類)-產業預測(2026-2033) 快速消費品包裝市場規模、佔有率、成長分析(按類型、材料、最終用途和地區)- 2025-2032 年產業預測

快速消費品包裝市場規模、佔有率、成長分析(按類型、材料、最終用途和地區)- 2025-2032 年產業預測