|

市場調查報告書

商品編碼

1848062

琥珀酸:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030)Succinic Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

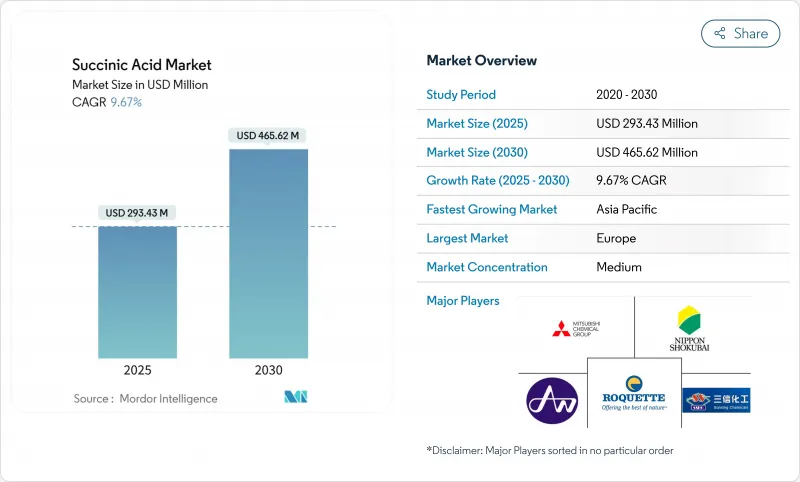

2025 年琥珀酸市場規模為 2.9343 億美元,預計到 2030 年將達到 4.6562 億美元,複合年成長率為 9.67%。

市場成長的促進因素包括:生產方式從石油基向生物基的轉變、發酵成本的降低以及企業以可再生中間體為重點的永續性舉措的不斷增多。市場擴張得益於對可生物分解聚合物(尤其是Polybutylene Succinate)日益成長的需求,以及其在食品和化妝品領域的廣泛應用。歐洲和北美的監管支持也促進了市場發展。企業正在投資先進的發酵技術,以減少生產過程中的二氧化碳排放,從而實現淨零排放目標。亞太地區也不斷建立製造中心,以確保原料多樣性並增強供應鏈穩定性。

全球琥珀酸市場趨勢與見解

對可生物分解聚合物的需求不斷增加

受汽車和包裝行業對傳統塑膠生物分解性塑膠替代品的需求推動,聚丁二酸丁二醇酯 (PBS) 的生產已成為琥珀酸需求的主要成長催化劑。慕尼黑工業大學的研究人員利用海洋細菌「鹽弧菌」(Vibrio natriegens) 實現了突破性的發酵效率,將生產時間從傳統的 24-48 小時週期縮短至 2-3 小時。這項技術進步解決了先前限制生物基琥珀酸競爭力的關鍵瓶頸——發酵可擴展性。為了符合循環經濟法規,尤其是在歐洲,聚合物製造商擴大指定使用生物基琥珀酸進行 PBS 生產,因為歐洲的延伸生產者責任框架對不可生物分解的包裝材料施加了處罰。

生物基化學品的監管支持

美國能源局2025年永續化學圓桌會議將琥珀酸確定為工業脫碳的優先平台化學品。在生物基化學品日益成長的需求的推動下,各國都在大力投資生物技術計畫。根據科技部2024年的數據,印度政府啟動了BioF3(生物技術促進經濟、環境和就業)政策,以促進該國的高性能生物技術製造業。 FDA對食品用琥珀酸的GRAS(一般認為是安全的)核準確定了其在調味品和肉品中的最大允許含量,消除了其在食品和飲料配方中擴大使用的監管障礙。此類監管核准為生物基琥珀酸製造商提供了優先的市場進入,同時建立了有利於具有成熟生產能力的現有製造商的品質標準。

商業規模生產基礎設施有限

包括BioAmber在內的幾家先驅企業的破產,導致現有產能下降,同時也抑制了對製造業基礎設施的新投資。開發中地區缺乏建造發酵設施所需的技術專長和資金,因此生產集中在現有的化學製造地。生物基生產的獨特特性要求與傳統化工廠不同的設備和工藝,這限制了現有設施的再利用,並增加了資本需求。原料供應鏈的發展落後於產能需求,尤其是非食品生質能原料,這些原料需要預處理基礎設施投資。

細分分析

預計2025年至2030年,生物基琥珀酸的複合年成長率將達到11.38%,而油基琥珀酸在2024年將維持59.42%的市佔率。生物基生產的高成長率反映了在監管要求和企業環保目標的推動下,永續生產方法的採用日益增加。向生物基生產的轉變符合全球永續性計劃以及各行各業日益增強的環保意識。石油基生產憑藉其完善的基礎設施和低成本,尤其是在價格敏感性高於環境問題的工業應用中,保持著市場主導。

石油基生產的成本優勢源自於數十年的製程最佳化和現有設施的規模經濟效益。生物基替代品在食品、藥品和化妝品等高階領域日益受到青睞,這些領域對永續性的要求決定了更高的價格,消費者的偏好也影響購買決策。在這些高階領域,終端使用者對環保產品的需求促使他們願意承擔與生物基生產方法相關的額外成本。

區域分析

歐洲憑藉其完善的法規結構和成熟的製造基礎設施,支持生物基化學品的發展,到2024年將佔據32.09%的市場佔有率。德國和法國在產能方面領先該地區,其一體化的化工園區促進了下游加工和分銷。該地區包裝材料生產者責任框架的不斷擴大,正在推動對由生物基琥珀酸製成的可生物分解聚合物的需求。

亞太地區是成長最快的地區,受中國、印度和東南亞快速工業化和製造能力擴張的推動,2025 年至 2030 年的複合年成長率為 10.58%。曉星在越南投資 10 億美元用於生產生物基 1,4-丁二醇,體現了該地區在生物基化學品製造中的戰略地位;該工廠的目標是到 2026 年年產能達到 50,000 公噸。中國在化學品製造業的主導地位為擴大琥珀酸生產提供了完善的基礎設施,而印度日益成長的製藥和個人護理行業正在創造對高等級產品日益成長的需求。該地區受益於豐富的農業廢棄物原料,如稻草和玉米秸稈,為生物基生產提供了具有成本效益的原料。政府支持工業脫碳和循環經濟發展的政策為全部區域採用生物基化學創造了有利條件。

儘管面臨來自低成本亞洲生產的競爭壓力,北美仍保持著重要的市場佔有率。美國農業部《2024年生質能供應鏈報告》指出,充足的原料供應是關鍵的競爭優勢,這得益於完善的農業基礎設施支撐可再生原料供應。美國美國能源局永續化學圓桌會議已將琥珀酸列為工業脫碳的平台化學品,並為國內生產發展提供政策支援。加拿大BioAmber商業化的失敗為風險管理和市場發展策略提供了經驗教訓,凸顯了切合實際的成本預測和市場價格假設的重要性。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 對可生物分解聚合物的需求不斷增加

- 生物基化學品的監管支持

- 擴大在食品和飲料中作為酸度調節劑和增味劑的用途

- 個人護理和化妝品需求不斷成長

- 生物基生產技術的進步

- 對綠色溶劑和工業化學品的需求不斷增加

- 市場限制

- 生產成本高

- 商業規模生產基礎設施有限

- 能源密集型煉油損害了環境效益

- 來自替代生物基酸的競爭

- 供應鏈分析

- 監理展望

- 五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章市場規模及成長預測

- 依產品類型

- 石油基

- 生物基

- 按年級

- 工業/技術級

- 食品級

- 醫藥級

- 化妝品級

- 按用途

- 工業化學品

- 飲食

- 製藥

- 個人護理和化妝品

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭態勢

- 市場集中度

- 策略舉措

- 市場排名分析

- 公司簡介

- Roquette Freres

- Mitsubishi Chemical Group

- Nippon Shokubai Co., Ltd.

- Air Water Performance Chemical Inc.

- Jinan Finer Chemical Co., Ltd

- Anhui Sunsing Chemicals

- Haihang Group

- Henan GP Chemicals Co.,Ltd

- Kunshan Odowell Co. Ltd

- Royal DSM(Reverdia)

- Wenzhou Blue Dolphin New Material Co., Ltd

- Ensince Industry Co., Ltd

- Carl Roth GmbH+Co. KG

- Axiom Chemicals Pvt. Ltd.

- LCY Biosciences Inc.

- Fengchen Group Co.,Ltd

- Shandong Biotech

- Shandong Feiyang Chemical

- Spectrum Chemical Mfg.

- Thermo Fisher Scientific

第7章 市場機會與未來展望

The succinic acid market size, valued at USD 293.43 million in 2025, is projected to reach USD 465.62 million by 2030, growing at a CAGR of 9.67%.

The market growth is driven by the shift from petroleum-based to bio-based production methods, reduced fermentation costs, and increased corporate sustainability initiatives focusing on renewable intermediates. The market expansion is supported by increasing demand for biodegradable polymers, specifically polybutylene succinate, along with broader adoption in food and cosmetic applications. Regulatory support in Europe and North America contributes to market development. Companies are investing in advanced fermentation technologies that reduce CO2 emissions during production, aligning with net-zero objectives. The Asia-Pacific region is establishing manufacturing centers to ensure feedstock diversity and strengthen supply chain stability.

Global Succinic Acid Market Trends and Insights

Rising demand for biodegradable polymers

Polybutylene succinate (PBS) production has emerged as the primary growth catalyst for succinic acid demand, with automotive and packaging industries mandating biodegradable alternatives to conventional plastics. Technical University of Munich researchers achieved breakthrough fermentation efficiency using the marine bacterium Vibrio natriegens, reducing production time to 2-3 hours compared to traditional 24-48 hour cycles. This technological advancement addresses the critical bottleneck of fermentation scalability that previously limited bio-based succinic acid competitiveness. Polymer manufacturers increasingly specify bio-based succinic acid for PBS production to meet circular economy regulations, particularly in Europe, where extended producer responsibility frameworks penalize non-biodegradable packaging materials.

Regulatory support for bio-based chemicals

Government policy frameworks have crystallized around bio-based chemical incentives, with the U.S. Department of Energy's 2025 sustainable chemistry roundtable identifying succinic acid as a priority platform chemical for industrial decarbonization . Owing to the rising demand for bio-based chemicals, various countries are investing heavily in biotechnology initiatives. According to the Ministry of Science and Technology data from 2024, the Government of India launched the BioF3 (Biotechnology for Economy, Environment and Employment) policy to foster high-performance biotechnology manufacturing in the country . FDA recognition of succinic acid as Generally Recognized as Safe (GRAS) for food applications removes regulatory barriers for expanded usage in food and beverage formulations, with maximum allowable levels established for condiments and meat products. These regulatory endorsements create preferential market access for bio-based succinic acid producers while establishing quality standards that favor established manufacturers with proven production capabilities.

Limited commercial-scale production infrastructure

The collapse of several pioneering companies, including BioAmber, has reduced available production capacity while deterring new investment in manufacturing infrastructure. Developing regions lack the technical expertise and capital access required for fermentation facility construction, concentrating production in established chemical manufacturing hubs. The specialized nature of bio-based production requires different equipment and processes compared to traditional chemical plants, limiting the ability to repurpose existing facilities and increasing capital requirements. Feedstock supply chain development lags behind production capacity needs, particularly for non-food biomass sources that require preprocessing infrastructure investment.

Other drivers and restraints analyzed in the detailed report include:

- Expanding food and beverage usage as acidity regulator and flavor enhancer

- Growing demand in personal care and cosmetics

- Competition from alternative bio-based acids

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bio-based succinic acid is projected to grow at a CAGR of 11.38% during 2025-2030, while petro-based succinic acid maintains a 59.42% market share in 2024. The higher growth rate of bio-based production reflects increasing adoption of sustainable manufacturing methods, driven by regulatory requirements and corporate environmental goals. The shift toward bio-based production aligns with global sustainability initiatives and growing environmental consciousness across industries. Petro-based production retains its market leadership due to established infrastructure and lower costs, particularly in industrial applications where price sensitivity outweighs environmental concerns.

The cost advantage of petro-based production stems from decades of process optimization and economies of scale in existing facilities. Bio-based alternatives are gaining traction in premium segments such as food, pharmaceuticals, and cosmetics, where sustainability requirements justify higher prices and consumer preferences influence purchasing decisions. These premium segments demonstrate increasing willingness to absorb the additional costs associated with bio-based production methods, driven by end-user demand for environmentally responsible products.

The Succinic Acid Market is Segmented Into Product Type (Petro and Bio-Based), Grade (Industrial/Technical, Food, Pharmaceuticals, and Cosmetic), Application (Industrial Chemicals, Food and Beverages, Pharmaceuticals, Personal Care and Cosmetics, and Others), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe commands 32.09% market share in 2024, leveraging established regulatory frameworks supporting bio-based chemicals and mature manufacturing infrastructure. Germany and France lead regional production capacity with integrated chemical complexes that facilitate downstream processing and distribution. The region's extended producer responsibility frameworks for packaging materials create preferential demand for biodegradable polymers derived from bio-based succinic acid.

Asia-Pacific emerges as the fastest-growing region with 10.58% CAGR for 2025-2030, driven by rapid industrialization and expanding manufacturing capacity across China, India, and Southeast Asia. Hyosung's USD 1 billion investment in Vietnam for bio-based 1,4-butanediol production exemplifies the region's strategic positioning in bio-based chemical manufacturing, with the facility targeting 50,000 metric tons of annual capacity by 2026. China's dominance in chemical manufacturing provides established infrastructure for succinic acid production scale-up, while India's growing pharmaceutical and personal care industries create expanding demand for higher-grade products. The region benefits from abundant agricultural waste feedstocks, including rice straw and corn stalks that provide cost-effective raw materials for bio-based production. Government policies supporting industrial decarbonization and circular economy development create favorable conditions for bio-based chemical adoption across the region.

North America maintains a significant market presence despite facing competitive pressure from lower-cost Asian production. The U.S. Department of Agriculture's 2024 biomass supply chain report identifies abundant feedstock availability as a key competitive advantage, with established agricultural infrastructure supporting renewable raw material supply . The U.S. Department of Energy's sustainable chemistry roundtable prioritizes succinic acid as a platform chemical for industrial decarbonization, providing policy support for domestic production development. Canada's experience with BioAmber's failed commercialization provides lessons for risk management and market development strategies, highlighting the importance of realistic cost projections and market pricing assumptions.

- Roquette Freres

- Mitsubishi Chemical Group

- Nippon Shokubai Co., Ltd.

- Air Water Performance Chemical Inc.

- Jinan Finer Chemical Co., Ltd

- Anhui Sunsing Chemicals

- Haihang Group

- Henan GP Chemicals Co.,Ltd

- Kunshan Odowell Co. Ltd

- Royal DSM (Reverdia)

- Wenzhou Blue Dolphin New Material Co., Ltd

- Ensince Industry Co., Ltd

- Carl Roth GmbH + Co. KG

- Axiom Chemicals Pvt. Ltd.

- LCY Biosciences Inc.

- Fengchen Group Co.,Ltd

- Shandong Biotech

- Shandong Feiyang Chemical

- Spectrum Chemical Mfg.

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for biodegradable polymers

- 4.2.2 Regulatory support for bio-based chemicals

- 4.2.3 Expanding food and beverage usage as acidity regulator and flavor enhancer

- 4.2.4 Growing demand in personal care and cosmetics

- 4.2.5 Advancements in bio-based production technologies

- 4.2.6 Rising demand for green solvents and industrial chemicals

- 4.3 Market Restraints

- 4.3.1 High production costs

- 4.3.2 Limited commercial-scale production infrastructure

- 4.3.3 Energy-intensive purification undermining eco-benefits

- 4.3.4 Competition from alternative bio-based acids

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Petro-based

- 5.1.2 Bio-based

- 5.2 By Grade

- 5.2.1 Industrial/Technical Grade

- 5.2.2 Food Grade

- 5.2.3 Pharmaceutical Grade

- 5.2.4 Cosmetic Grade

- 5.3 By Application

- 5.3.1 Industrial Chemicals

- 5.3.2 Food and Beverage

- 5.3.3 Pharmaceuticals

- 5.3.4 Personal Care and Cosmetics

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Roquette Freres

- 6.4.2 Mitsubishi Chemical Group

- 6.4.3 Nippon Shokubai Co., Ltd.

- 6.4.4 Air Water Performance Chemical Inc.

- 6.4.5 Jinan Finer Chemical Co., Ltd

- 6.4.6 Anhui Sunsing Chemicals

- 6.4.7 Haihang Group

- 6.4.8 Henan GP Chemicals Co.,Ltd

- 6.4.9 Kunshan Odowell Co. Ltd

- 6.4.10 Royal DSM (Reverdia)

- 6.4.11 Wenzhou Blue Dolphin New Material Co., Ltd

- 6.4.12 Ensince Industry Co., Ltd

- 6.4.13 Carl Roth GmbH + Co. KG

- 6.4.14 Axiom Chemicals Pvt. Ltd.

- 6.4.15 LCY Biosciences Inc.

- 6.4.16 Fengchen Group Co.,Ltd

- 6.4.17 Shandong Biotech

- 6.4.18 Shandong Feiyang Chemical

- 6.4.19 Spectrum Chemical Mfg.

- 6.4.20 Thermo Fisher Scientific

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

磺基琥珀酸酯市場:2026-2032年全球市場按產品類型、劑型、銷售管道和應用分類的預測

磺基琥珀酸酯市場:2026-2032年全球市場按產品類型、劑型、銷售管道和應用分類的預測 全球聚丁二酸丁二醇酯市場規模、佔有率、趨勢和成長分析報告(2026-2034年)琥珀酸全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球聚丁二酸丁二醇酯市場規模、佔有率、趨勢和成長分析報告(2026-2034年)琥珀酸全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026-2030年全球琥珀酸市場

2026-2030年全球琥珀酸市場 磺基琥珀酸酯市場機會、成長要素、產業趨勢分析及2026年至2035年預測

磺基琥珀酸酯市場機會、成長要素、產業趨勢分析及2026年至2035年預測 琥珀酸市場規模、佔有率及成長分析(按類型、應用、終端用戶產業和地區分類)-產業預測(2026-2033)

琥珀酸市場規模、佔有率及成長分析(按類型、應用、終端用戶產業和地區分類)-產業預測(2026-2033) 生物琥珀酸衍生聚酯多元醇市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2025-2033 年)

生物琥珀酸衍生聚酯多元醇市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2025-2033 年) Polybutylene Succinate的全球市場

Polybutylene Succinate的全球市場 生物基琥珀酸:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)琥珀酸市場規模(按類型、最終用途行業、地區和預測)

生物基琥珀酸:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)琥珀酸市場規模(按類型、最終用途行業、地區和預測)