|

市場調查報告書

商品編碼

1835658

汽車 3D 列印:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Automotive 3D Printing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

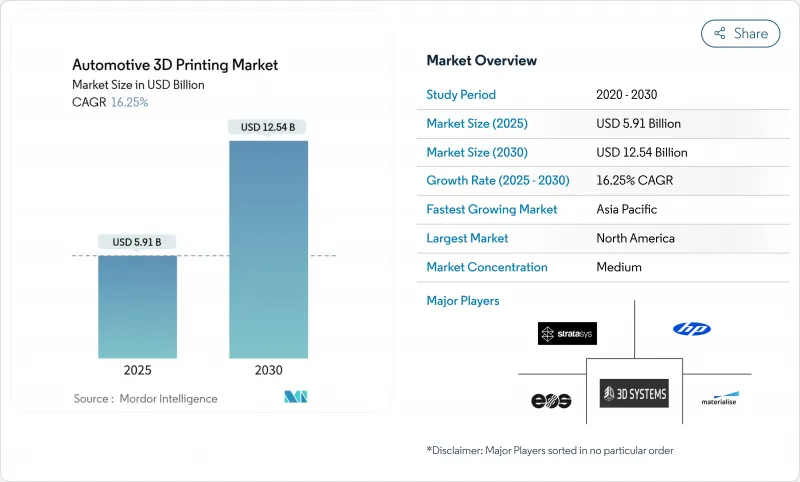

預計 2025 年汽車 3D 列印市場價值將達到 59.1 億美元,到 2030 年將達到 125.4 億美元,複合年成長率為 16.25%。

隨著多材料加工、數位供應鏈編配和人工智慧主導的品管方面的突破重新定義了製造業經濟學,從原型製作到全面生產的轉變正在加速。對符合嚴格排放法規的輕型零件的需求正在支撐成長,BMW透過電弧積層製造減少了 27% 的排放就證明了這一點。熔融沈積成型 (FDM) 和選擇性雷射燒結 (SLS) 硬體的進步正在提高產量,而具有成本效益的矽鐵粉末正在為電動車 (EV) 馬達零件的金屬應用開闢道路。監管壓力、在岸戰略以及永續原料的可用性正在推動汽車 3D 列印市場在現有和新興經濟體中的擴張。

全球汽車 3D 列印市場趨勢與洞察

對輕量化電動車零件的需求

電動車製造商正在追求重量最佳化,以增加續航里程並符合排放法規。通用汽車已在凱迪拉克 Celestiq 車型中採用了 130 多個列印零件,其中包括汽車生產中最大的積層製造鋁製零件。歐洲的歐盟 7 法規正在加速煞車盤盤塗層和結構件的採用。砂基 3D 列印縮短了模具開發週期,並使得鑄造設計能夠在保持公差目標的同時減輕重量。為了減輕電池重量,各大廠商競相將整個汽車平臺的重量降到最低。

降低快速原型製作成本

多家公司報告稱,積層製造可以取代早期設計迭代中的機械加工,將原型前置作業時間縮短高達 90%,並顯著降低單一零件成本。光固化成形法的高尺寸精度支援低成本的熔模鑄造替代方案,而基於人工智慧的建造參數最佳化則提高了首次成功率。低於 3,000 美元的桌上型 SLS 印表機擴大了中小型供應商的可及性,並縮短了亞太製造群的創新週期。

金屬印表機高成本

雖然工業級SLS印表機的成本在12,000美元到33,000美元之間,但特種金屬粉末的平均價格為每公斤300美元到600美元,這限制了成本敏感型供應商的採用。氦霧化粉末製造是最永續的途徑,但資本支出仍然很高。生命週期分析表明,粉末層熔融對於高複雜度零件而言經濟實惠,但巨大的初始投資使其難以廣泛採用。低成本的金屬絲製程降低了進入門檻,但增加了後處理的複雜性,導致汽車3D列印市場的複合年成長率下降了2.4個百分點。

報告中分析的其他促進因素和限制因素

- 客製化生產

- 模具數位化備件庫存

- 材料品質差距

細分分析

2024年,FDM佔據了汽車3D列印市場佔有率的38.32%,這得益於低廉的系統成本和豐富的材料選擇。隨著售價低於3,000美元的桌上型粉末床系統推動高性能尼龍和複合材料列印的普及,預計到2030年,SLS的複合年成長率將達到18.53%。光固化成形法至100奈米,列印速度達100微米/秒,使其應用領域拓展至微流體和光學領域。數位光處理(DLP)技術擴大支援珠寶飾品和牙科模型,而電子束熔化技術在航太鈦合金零件的製造中發揮著重要作用。隨著電動車製造商採用耐用的尼龍齒輪和引擎蓋下零件,基於SLS技術的汽車3D列印零件市場預計將迅速擴張。

混合製造技術(即融合積層製造和減材製造技術)正在興起。 FDM 刀具路徑整合了連續纖維增強材料,無需二次加工即可提高拉伸強度。全像像體積列印透過同時固化整個列印層,已證明可將速度提升高達 20 倍,這在汽車內裝零件的量產中展現出巨大的潛力。製程模擬軟體的持續改進減少了試驗,確保 FDM 在 SLS裝置量不斷成長的情況下仍然保持競爭力。

到2024年,硬體將佔總收入的57.32%,其中包括印表機、後處理站和掃描器。然而,隨著機器學習演算法降低缺陷率並促進多工廠車隊組織,軟體將以18.78%的複合年成長率成長。貝克休斯實施的製造營運平台將監控時間縮短了98%,廢品率降低了18%。當汽車製造商外包特殊材料或小批量生產而無法證明資本支出合理性時,服務機構就會發揮作用。

人工智慧驅動的建置參數引擎將工程工作量減少了80%,幫助該軟體擴大了其在汽車3D列印領域的市場佔有率。基於瀏覽器的協作套件支援跨洲設計迭代,從而實現同步工程和快速投產。隨著雲端連接的擴展,訂閱收入為供應商提供了豐厚的年金,將競爭重點從機器轉向數位生態系統。

汽車產業3D列印市場報告按技術類型(選擇性雷射燒結 (SLS)、立體光刻技術(SLA)、其他)、組件類型(硬體、軟體、服務)、材料類型(金屬、聚合物、其他)、應用類型(生產、原型製作、其他)和地區細分。市場預測以金額(美元)和數量(單位)提供。

區域分析

北美在2024年將以38.63%的市佔率領先汽車3D列印市場,這得益於美國主導的航太和電動車供應鏈。通用電氣航空航太公司對積層製造設施的10億美元投資,顯示了對國內生產的長期信心。 「縮短製造週期舉措」與《通膨削減法案》相結合,獎勵了本地製造業,並加速了印表機在汽車產業的部署。加拿大和墨西哥利用跨境貿易框架,透過輕型卡車零件和航太鑄模做出了貢獻。

受中國製造業數位化和印度新興生物列印公司推動,亞太地區將成為成長最快的地區,到2030年複合年成長率將達到19.47%。中國的五年規劃將積層製造確定為戰略支柱,推動其在汽車輪轂和電池工廠的廣泛應用。在印度,EOS和Godrej的合作將加速其在航太的應用,而公私合作研發中心將促進技能發展。日本和韓國將推動材料創新,開發用於混合動力電動動力傳動系統的耐熱聚合物。東南亞的電子產業叢集正在採用3D列印技術進行模具製造,部分原因是受到政府稅收優惠政策的推動。

歐洲佔了很大佔有率,其中以德國為首,大多數製造商都採用了積層製造流程。該地區積層製造公司30.6%的銷售額用於研發,並鞏固了其在金屬印表機出口方面的領先地位。法國和義大利正在擴大超級跑車的複合材料列印,而斯堪地那維亞則正在探索用於汽車內飾的生物基聚合物。透過ISO/ASTM標準的監管協調,支援列印零件的跨境認證並簡化了供應鏈。南美和中東的新興地區正在追求多元化,沙烏地阿拉伯向中小企業提供入門級印表機,以降低金屬加工的能源消耗。巴西正在試驗建立一個農業機械增材維修中心,顯示該技術正在向高所得經濟體以外的地區擴展。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 對輕量化電動車零件的需求

- 降低快速原型製作成本

- 客製化生產工具

- 數位備件庫存

- 多材料AM整合

- 促進供應鏈回流

- 市場限制

- 金屬印表機高成本

- 材料品質的差異

- 能量密集型雷射系統

- IP安全問題

- 價值/供應鏈分析

- 監管狀況

- 技術展望

- 五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章市場規模與成長預測:價值(美元)與數量(單位)

- 依技術類型

- 選擇性雷射燒結(SLS)

- 光固化成形法(SLA)

- 數位光處理 (DLP)

- 電子束熔煉(EBM)

- 選擇性雷射熔融(SLM)

- 熔融沉積建模(FDM)

- 依組件類型

- 硬體

- 軟體

- 服務

- 依材料類型

- 金屬

- 聚合物

- 陶瓷製品

- 複合材料

- 按用途

- 製造業

- 原型製作

- 模具和夾具

- 備件/維護、修理和運行

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 埃及

- 其他中東和非洲地區

- 北美洲

第6章 競爭態勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Stratasys Ltd

- 3D Systems Corporation

- EOS GmbH

- HP Inc.

- Materialise NV

- GE Additive(Arcam AB)

- Desktop Metal(ExOne)

- Ultimaker BV

- Voxeljet AG

- Carbon Inc.

- Hoganos AB

- EnvisionTEC GmbH

- SLM Solutions Group AG

- Renishaw plc

- BASF Forward AM

- Markforged Inc.

- Sindoh Co. Ltd

- XYZprinting Inc.

- Moog Inc.

第7章 市場機會與未來展望

The Automotive 3D printing market is valued at USD 5.91 billion in 2025 and is forecast to reach USD 12.54 billion by 2030, reflecting a 16.25% CAGR.

The shift from prototyping toward full-scale production is accelerating as breakthroughs in multi-material processing, digital supply-chain orchestration, and artificial-intelligence-driven quality control redefine manufacturing economics. Demand for lightweight components that meet stringent emissions rules, illustrated by BMW's 27% emissions reduction using wire-arc additive manufacturing, underpins growth. Hardware advances in fused deposition modeling (FDM) and selective laser sintering (SLS) improve throughput, while cost-effective iron-silicon powders open metal applications for electric-vehicle (EV) motor parts. Regulatory pressure, on-shoring strategies, and the availability of sustainable feedstocks align to expand the Automotive 3D printing market across established and emerging economies.

Global Automotive 3D Printing Market Trends and Insights

EV Lightweight-Parts Demand

Electric vehicle makers pursue weight optimization to extend their range and comply with emissions standards. General Motors integrates more than 130 printed parts in the Cadillac Celestiq, including the largest additively manufactured aluminum component in automotive production. Europe's Euro 7 norms accelerate adoption for brake-disc coatings and structural elements. Sand-based 3D printing shortens mold-development cycles, enabling casting designs that reduce mass while preserving tolerance targets. The need to offset battery weight intensifies competitive incentives to remove every gram across vehicle platforms.

Rapid Prototyping Cost-Cuts

Enterprises report up to 90% reductions in prototype lead times and sharp declines in single-part costs as additive manufacturing replaces machining for early-stage design iterations. Stereolithography's high dimensional accuracy supports low-cost investment casting alternatives, while AI-based build-parameter optimization elevates first-time-right success rates. Desktop SLS printers priced below USD 3,000 broaden access for small and midsize suppliers, compressing innovation cycles across Asia-Pacific manufacturing clusters.

High Cost of Metal Printers

Industrial SLS printers list between USD 12,000 and USD 33,000, while specialty metal powders average USD 300-600 per kg, limiting adoption among cost-sensitive suppliers. Helium-atomized powder production offers the most sustainable route, yet capital outlays remain steep. Lifecycle analyses show powder-bed fusion is economical for high-complexity components, but up-front capital still deters wide deployment. Lower-cost metal-filament processes mitigate entry barriers but add post-processing complexity, reducing the Automotive 3D printing market CAGR by 2.4 percentage points

Other drivers and restraints analyzed in the detailed report include:

- Custom Production Tooling

- Digital Spare-Parts Inventory

- Material-Qualification Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

FDM accounted for 38.32% of the Automotive 3D printing market share in 2024, owing to low system costs and broad material selection. SLS is projected to grow at an 18.53% CAGR through 2030 as desktop powder-bed systems below USD 3,000 democratize high-performance nylon and composite printing. Advances in nanoscale photopolymerization have pushed stereolithography resolution to 100 nm at 100 µm per second, extending its use into microfluidic and optics applications. Digital Light Processing (DLP) increasingly supports jewelry and dental models, while electron-beam melting serves aerospace titanium parts. The Automotive 3D printing market size for SLS-based parts is forecast to expand sharply as EV manufacturers adopt durable nylon gears and under-hood components.

Hybrid manufacturing that blends additive and subtractive techniques is gaining ground. FDM toolpaths integrate continuous-fiber reinforcement, improving tensile strength without secondary operations. Holographic volumetric printing demonstrates up-to-20-fold speed gains by curing entire layers simultaneously, holding promise for high-volume automotive interiors. Continual improvements in process simulation software reduce trial iterations, ensuring FDM retains relevance even as the SLS installed base rises.

Hardware captured 57.32% of 2024 revenue, encompassing printers, post-processing stations, and scanners. However, software is expanding at 18.78% CAGR as machine-learning algorithms cut defect rates and orchestrate multi-factory fleets. Manufacturing operations platforms deployed at Baker Hughes trimmed monitoring time by 98% and scrap by 18%. Service bureaus flourish when automakers outsource specialty materials or small production runs that do not justify capital spending.

AI-driven build-parameter engines reduce engineering labor by 80%, contributing to a rising software share within the Automotive 3D printing market. Browser-based collaboration suites allow design iterations across continents, enabling simultaneous engineering and rapid release to production. As cloud connectivity scales, subscription revenue offers vendors a high-margin annuity, shifting the competitive balance from machines to digital ecosystems

The 3D Printing in Automotive Industry Market Report is Segmented by Technology Type (Selective Laser Sintering (SLS), Stereo Lithography (SLA), and More ), Component Type (Hardware, Software, and Service), Material Type (Metal, Polymer, and More), Application Type (Production, Prototyping, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

North America leads the Automotive 3D printing market with a 38.63% share in 2024, supported by the United States' dominant aerospace and EV supply chains. GE Aerospace's USD 1 billion investment in additive facilities signals long-term confidence in domestic productio. Reshoring initiatives combined with the Inflation Reduction Act incentivize localized manufacturing, accelerating printer installations across automotive tiers. Canada and Mexico contribute through lightweight truck components and aerospace casting molds, leveraging cross-border trade frameworks.

Asia-Pacific is the fastest-growing region at a 19.47% CAGR through 2030, propelled by China's manufacturing digitalization and India's emerging bioprinting startups. Chinese five-year plans earmark additive manufacturing as a strategic pillar, spurring installation growth across automotive hubs and battery factories. India's collaboration between EOS and Godrej accelerates aerospace applications, while public-private R&D centers foster skill development. Japan and South Korea push materials innovation, developing heat-resistant polymers tailored to hybrid-electric powertrains. Southeast Asian electronics clusters adopt 3D printing for tooling, aided by government tax incentives.

Europe holds a significant share, anchored by Germany where majority of manufacturers deploy additive processes. The region invests 30.6% of AM company turnover back into R&D, reinforcing leadership in metal-printer exports. France and Italy expand composite printing for supercars, while Scandinavia explores bio-based polymers for vehicle interiors. Regulatory alignment through ISO/ASTM standards supports cross-border qualification of printed parts, smoothing supply-chain flows. Emerging regions in South America and the Middle East pursue diversification; Saudi Arabia outfits SMEs with entry-level printers to decrease energy consumption in metal fabrication. Brazil pilots additive repair hubs for agricultural machinery, demonstrating the technology's reach beyond high-income economies.

- Stratasys Ltd

- 3D Systems Corporation

- EOS GmbH

- HP Inc.

- Materialise NV

- GE Additive (Arcam AB)

- Desktop Metal (ExOne)

- Ultimaker BV

- Voxeljet AG

- Carbon Inc.

- Hoganos AB

- EnvisionTEC GmbH

- SLM Solutions Group AG

- Renishaw plc

- BASF Forward AM

- Markforged Inc.

- Sindoh Co. Ltd

- XYZprinting Inc.

- Moog Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV lightweight-parts demand

- 4.2.2 Rapid prototyping cost-cuts

- 4.2.3 Custom production tooling

- 4.2.4 Digital spare-parts inventory

- 4.2.5 Multi-material AM integration

- 4.2.6 Supply-chain on-shoring push

- 4.3 Market Restraints

- 4.3.1 High cost of metal printers

- 4.3.2 Material-qualification gaps

- 4.3.3 Energy-intensive laser systems

- 4.3.4 IP-security concerns

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Technology Type

- 5.1.1 Selective Laser Sintering (SLS)

- 5.1.2 Stereolithography (SLA)

- 5.1.3 Digital Light Processing (DLP)

- 5.1.4 Electron Beam Melting (EBM)

- 5.1.5 Selective Laser Melting (SLM)

- 5.1.6 Fused Deposition Modeling (FDM)

- 5.2 By Component Type

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Service

- 5.3 By Material Type

- 5.3.1 Metal

- 5.3.2 Polymer

- 5.3.3 Ceramic

- 5.3.4 Composite

- 5.4 By Application Type

- 5.4.1 Production

- 5.4.2 Prototyping

- 5.4.3 Tooling and Fixtures

- 5.4.4 Spare-Parts / MRO

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Stratasys Ltd

- 6.4.2 3D Systems Corporation

- 6.4.3 EOS GmbH

- 6.4.4 HP Inc.

- 6.4.5 Materialise NV

- 6.4.6 GE Additive (Arcam AB)

- 6.4.7 Desktop Metal (ExOne)

- 6.4.8 Ultimaker BV

- 6.4.9 Voxeljet AG

- 6.4.10 Carbon Inc.

- 6.4.11 Hoganos AB

- 6.4.12 EnvisionTEC GmbH

- 6.4.13 SLM Solutions Group AG

- 6.4.14 Renishaw plc

- 6.4.15 BASF Forward AM

- 6.4.16 Markforged Inc.

- 6.4.17 Sindoh Co. Ltd

- 6.4.18 XYZprinting Inc.

- 6.4.19 Moog Inc.

7 Market Opportunities & Future Outlook

汽車3D列印市場:依材料類型、製程、組件、設備、應用及最終用途分類-2026-2032年全球市場預測

汽車3D列印市場:依材料類型、製程、組件、設備、應用及最終用途分類-2026-2032年全球市場預測 2026年全球汽車3D列印市場報告

2026年全球汽車3D列印市場報告 3D列印汽車市場-全球產業規模、佔有率、趨勢、競爭格局、機會及預測(按材料、技術、應用、地區和競爭情況分類,2021-2031年)汽車3D列印市場-全球產業規模、佔有率、趨勢、機會及預測(依技術、應用、區域及競爭格局分類,2021-2031年)

3D列印汽車市場-全球產業規模、佔有率、趨勢、競爭格局、機會及預測(按材料、技術、應用、地區和競爭情況分類,2021-2031年)汽車3D列印市場-全球產業規模、佔有率、趨勢、機會及預測(依技術、應用、區域及競爭格局分類,2021-2031年) 汽車3D列印市場規模、佔有率和成長分析(按產品、組件、車輛類型、材料和地區分類)-產業預測(2026-2033年)

汽車3D列印市場規模、佔有率和成長分析(按產品、組件、車輛類型、材料和地區分類)-產業預測(2026-2033年) 汽車3D列印市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)

汽車3D列印市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年) 汽車3D列印市場:2025-2030年預測

汽車3D列印市場:2025-2030年預測 全球汽車3D列印市場

全球汽車3D列印市場 2025-2029 年全球 AI 影像轉 3D 生成器市場

2025-2029 年全球 AI 影像轉 3D 生成器市場 2032 年高性能生質塑膠市場預測:按產品類型、原料、製造流程、最終用戶和地區進行的全球分析

2032 年高性能生質塑膠市場預測:按產品類型、原料、製造流程、最終用戶和地區進行的全球分析