|

市場調查報告書

商品編碼

1773384

室內生物塑膠市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Bioplastic for Interior Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

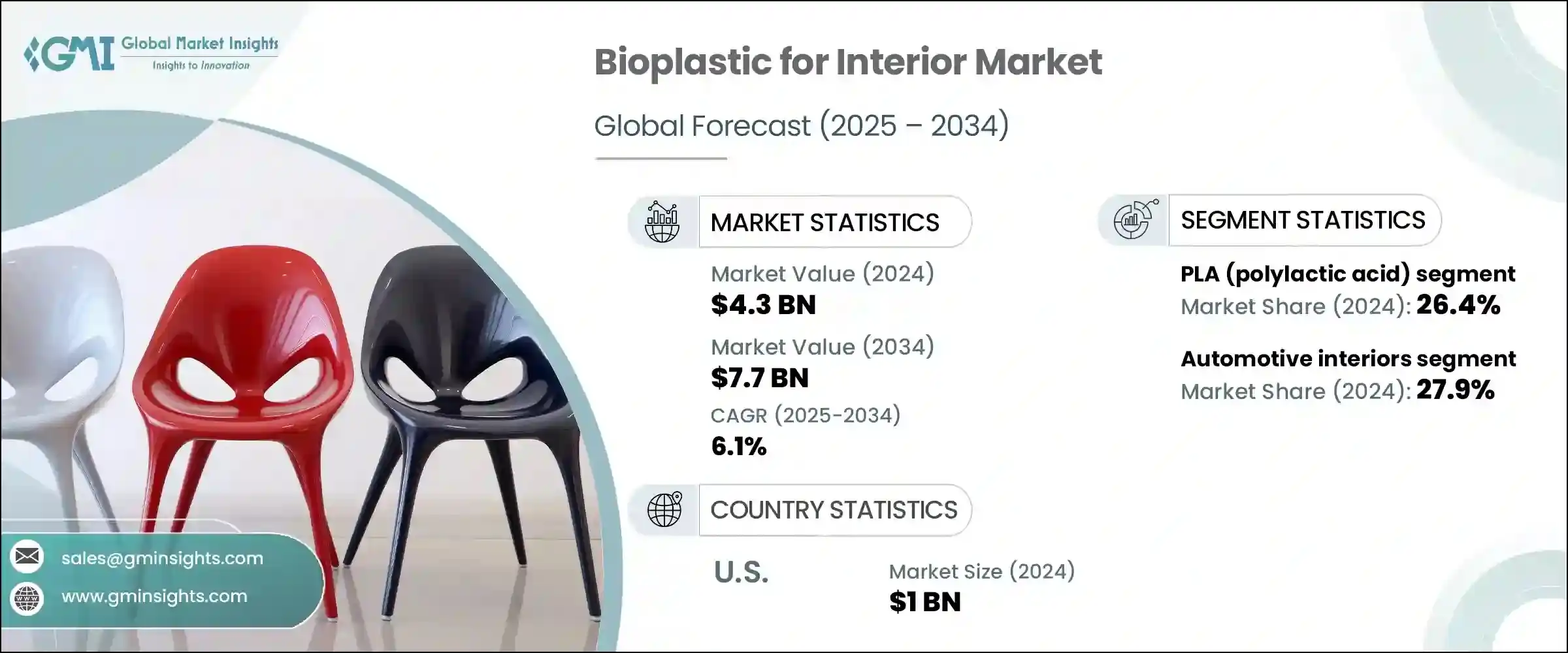

2024年,全球室內裝潢用生物塑膠市場規模達43億美元,預計2034年將以6.1%的複合年成長率成長,達到77億美元。消費者和企業日益增強的環保意識正在重塑室內裝潢材料格局,推動人們向再生、低影響的替代方案轉變。傳統塑膠正日益被生物塑膠所取代,生物塑膠源自於甘蔗、玉米和纖維素等天然資源。這些材料不僅支持環保目標,還具有生物分解性和減少碳排放等實際優勢,與永續生活和生產實踐的廣泛倡導相契合。

隨著人們追求更環保的設計元素,對綠色室內設計的需求日益成長,這也進一步強化了生物塑膠在這項轉型中所扮演的角色。擺脫石油基塑膠的趨勢已不再局限於利基應用領域;它在家具、牆面處理、室內裝飾元素、地板等眾多領域都越來越受到青睞。全球廢棄物管理法規的日益嚴格以及人們對塑膠污染日益成長的擔憂,迫使製造商採用永續的替代品,這進一步推動了生物塑膠在室內裝飾中的成長。企業也意識到迎合環保偏好的商業價值,從而廣泛採用兼具高性能和永續性的生物塑膠材料。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 43億美元 |

| 預測值 | 77億美元 |

| 複合年成長率 | 6.1% |

2024年,聚乳酸 (PLA) 佔據按聚合物類型分類的市場佔有率的26.4%。 PLA憑藉其良好的環保特性、可再生性和廣泛的應用前景,繼續引領該領域。 PLA源自植物糖,是傳統塑膠零件的永續替代品。其卓越的視覺清晰度和強大的機械性能使其成為各種內裝應用的首選,尤其是在注重透明度或拋光效果的領域。隨著對環保解決方案的需求日益成長,PLA已成為製造商兼顧功能性和生態效益的首選聚合物。

從應用角度來看,汽車內裝在2024年佔據最大佔有率,佔整體市場的27.9%。汽車製造商正積極用生物塑膠取代傳統塑膠零件,以滿足環保法規和消費者期望。生物塑膠的減重能力在提高燃油效率方面發揮著重要作用,同時也支持車輛的可回收性。這些材料用於各種內裝部件,包括座椅底座、儀表板結構、裝飾件和麵板。它們具有精密成型能力,並與更清潔的生產技術相容,使其成為性能和設計靈活性同等重要的汽車應用的理想選擇。

從終端用戶來看,建築業在2024年引領市場,佔據主導地位。然而,汽車原始設備製造商(OEM)已成為內裝領域最積極採用生物塑膠的產業。作為更廣泛的環境策略的一部分,這些公司積極參與將生物基材料融入汽車內裝。在結構和外觀部件中使用生物塑膠不僅可以減輕車輛重量,還可以降低生命週期排放。許多公司正在與材料供應商建立長期合作關係,以增強其生物塑膠採購能力並確保穩定的供應鏈。

家具製造商在生物塑膠使用量方面排名第二。他們正在將生物基材料融入模組化系統和永續家居裝飾,以滿足環保意識強的買家不斷變化的需求。室內設計工作室正在使用生物塑膠客製化項目,尤其是在遵守綠色認證計劃的高階住宅和商業環境中。這些材料在零售和展廳設施的使用也日益增多,在這些領域,永續的美學設計有助於提升品牌定位。此外,建築商和商業室內承包商也開始使用生物塑膠來製造符合現代綠建築規範的覆層、面板和隔間等產品。

2024年,美國內裝用生物塑膠市場規模達10億美元。美國市場的成長主要得益於消費者意識的提升以及旨在減少環境影響的監管力度,尤其是在汽車和建築行業。為了滿足消費者對清潔技術和永續產品的需求,領先的製造商正在優先考慮生物基材料。生物聚合物的創新推動了材料性能的提升,使得生物塑膠能夠更順暢地融入大規模生產線。因此,美國生產商不僅在拓展產能,還在為永續製造樹立新的標竿。

在全球範圍內,內裝生物塑膠市場受到競爭環境的影響,企業專注於專有材料、先進的加工技術和永續的生產模式。領先的企業正在不斷鞏固上游原料來源,以穩定成本並確保供應。同時,企業也努力提高產品耐用性、獲得綠色認證和提供設計彈性,從而脫穎而出。這些策略使關鍵利益相關者能夠在快速發展的市場中保持領先地位,以滿足監管要求和消費者對環保內飾的期望。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 市場機會

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 價格趨勢

- 按地區

- 按聚合物類型

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 專利態勢

- 貿易統計(HS編碼)

(註:僅提供重點國家的貿易統計數據

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考慮

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按聚合物類型,2021 - 2034 年

- 主要趨勢

- PLA(聚乳酸)

- 澱粉基生物塑膠

- 聚羥基脂肪酸酯(PHA)

- 纖維素基生物塑膠

- Bio-PE(生物聚乙烯)

- 生物PET(生物聚對苯二甲酸乙二酯)

- 其他

第6章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 汽車內裝

- 家具和家居內飾

- 商業和辦公室室內設計

- 零售和酒店室內設計

- 其他

第7章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 汽車OEM

- 家具製造商

- 室內設計公司

- 零售商和展廳

- 承包商和建築商

- 其他

第8章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- Arkema SA

- BASF SE

- Biome Bioplastics

- Braskem SA

- Cardia Bioplastics

- Celanese Corporation

- Covestro AG

- DuPont de Nemours, Inc

- Evonik Industries AG

- FKuR Kunststoff GmbH

- Mitsubishi Chemical Group

- NatureWorks LLC

- Novamont

- TotalEnergies Corbion

The Global Bioplastic for Interior Market was valued at USD 4.3 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 7.7 billion by 2034. Growing environmental consciousness among consumers and organizations is reshaping the interior materials landscape, encouraging the shift toward renewable, low-impact alternatives. Traditional plastics are increasingly being replaced by bioplastics, which are derived from natural sources such as sugarcane, corn, and cellulose. These materials not only support environmental goals but also deliver practical advantages like biodegradability and reduced carbon emissions, aligning with the broader push for sustainable living and production practices.

As people seek more eco-conscious design elements, the demand for green interiors is accelerating, reinforcing the role of bioplastics in this transition. The move away from petroleum-based plastics is no longer limited to niche applications; it is gaining traction across furniture, wall treatments, interior decorative elements, and flooring, among other uses. Stricter global waste management regulations and mounting concerns over plastic pollution are pressuring manufacturers to adopt sustainable alternatives, further fueling the growth of bioplastics in interior applications. Businesses are also realizing the commercial value of catering to environmentally driven preferences, leading to widespread adoption of bioplastic materials that offer performance without compromising sustainability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.3 Billion |

| Forecast Value | $7.7 Billion |

| CAGR | 6.1% |

In 2024, polylactic acid (PLA) accounted for 26.4% of the total market share by polymer type. PLA continues to lead the segment due to its favorable environmental profile, renewability, and wide usability. Sourced from plant-based sugars, PLA offers a sustainable substitute for conventional plastic components. Its visual clarity and strong mechanical performance make it a preferred choice for a variety of interior applications, especially where transparency or a polished finish is important. As demand for environmentally responsible solutions grows, PLA stands out as a go-to polymer for manufacturers aiming to blend functionality with ecological benefits.

From an application standpoint, automotive interiors held the largest share in 2024, contributing 27.9% to the overall market. Automakers are actively replacing traditional plastic parts with bioplastics to meet both environmental regulations and consumer expectations. The ability of bioplastics to deliver weight savings plays a significant role in enhancing fuel efficiency while also supporting vehicle recyclability. These materials are used in numerous interior parts, including seat bases, dashboard structures, trim pieces, and panels. Their capacity for precise molding and compatibility with cleaner production techniques make them ideal for automotive applications, where performance and design flexibility are equally important.

On the basis of end users, the building construction segment led the market in 2024, capturing a dominant position. However, automotive OEMs emerged as the most active adopters of bioplastics in the interiors domain. These companies are heavily involved in integrating bio-based materials into vehicle interiors as part of broader environmental strategies. Incorporating bioplastics in structural and aesthetic parts not only reduces vehicle mass but also lowers lifecycle emissions. Many companies are forming long-term collaborations with material suppliers to enhance their bioplastic sourcing capabilities and ensure stable supply chains.

Furniture manufacturers ranked second in terms of bioplastic usage. They are incorporating bio-based materials into modular systems and sustainable home decor, meeting the evolving needs of environmentally conscious buyers. Interior design studios are customizing projects with bioplastics, particularly in high-end residential and commercial settings that adhere to green certification programs. The use of these materials is also rising in retail and showroom installations, where sustainable aesthetics contribute to brand positioning. Additionally, builders and commercial interior contractors are turning to bioplastics for items like cladding, panels, and partitions that comply with modern green building codes.

In 2024, the bioplastic for interior market in the United States was valued at USD 1 billion. Growth in the U.S. is being driven by a combination of consumer awareness and regulatory efforts to reduce environmental impact, especially in the automotive and construction sectors. Leading manufacturers are prioritizing bio-based materials in response to consumer demands for cleaner technologies and sustainable products. Enhanced material performance, driven by innovation in bio-polymers, is allowing smoother integration of bioplastics into large-scale production lines. As a result, U.S.-based producers are not only expanding their capabilities but also setting new benchmarks for sustainable manufacturing.

Globally, the bioplastic for interior market are shaped by a competitive environment where companies are focusing on proprietary materials, advanced processing technologies, and sustainable production models. Leading players are increasingly securing upstream raw material sources to stabilize costs and ensure availability. At the same time, efforts to improve product durability, achieve green certifications, and offer design flexibility are helping companies differentiate themselves. These strategies are enabling key stakeholders to stay ahead in a market that is quickly evolving to meet both regulatory demands and consumer expectations for environmentally friendly interiors.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Polymer type

- 2.2.2 Application

- 2.2.3 End use

- 2.2.4 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By polymer type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Polymer Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 PLA (polylactic acid)

- 5.3 Starch-based bioplastics

- 5.4 Polyhydroxyalkanoates (PHA)

- 5.5 Cellulose-based bioplastics

- 5.6 Bio-PE (bio-polyethylene)

- 5.7 Bio-PET (bio-polyethylene terephthalate)

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Automotive interiors

- 6.3 Furniture & home interiors

- 6.4 Commercial & office interiors

- 6.5 Retail & hospitality interiors

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive OEM

- 7.3 Furniture manufacturers

- 7.4 Interior design firms

- 7.5 Retailers & showrooms

- 7.6 Contractors & Builders

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Arkema S.A.

- 9.2 BASF SE

- 9.3 Biome Bioplastics

- 9.4 Braskem S.A.

- 9.5 Cardia Bioplastics

- 9.6 Celanese Corporation

- 9.7 Covestro AG

- 9.8 DuPont de Nemours, Inc

- 9.9 Evonik Industries AG

- 9.10 FKuR Kunststoff GmbH

- 9.11 Mitsubishi Chemical Group

- 9.12 NatureWorks LLC

- 9.13 Novamont

- 9.14 TotalEnergies Corbion

汽車3D列印市場:依材料類型、製程、組件、設備、應用及最終用途分類-2026-2032年全球市場預測

汽車3D列印市場:依材料類型、製程、組件、設備、應用及最終用途分類-2026-2032年全球市場預測 2026年全球汽車3D列印市場報告

2026年全球汽車3D列印市場報告 3D列印汽車市場-全球產業規模、佔有率、趨勢、競爭格局、機會及預測(按材料、技術、應用、地區和競爭情況分類,2021-2031年)汽車3D列印市場-全球產業規模、佔有率、趨勢、機會及預測(依技術、應用、區域及競爭格局分類,2021-2031年)

3D列印汽車市場-全球產業規模、佔有率、趨勢、競爭格局、機會及預測(按材料、技術、應用、地區和競爭情況分類,2021-2031年)汽車3D列印市場-全球產業規模、佔有率、趨勢、機會及預測(依技術、應用、區域及競爭格局分類,2021-2031年) 汽車3D列印市場規模、佔有率和成長分析(按產品、組件、車輛類型、材料和地區分類)-產業預測(2026-2033年)

汽車3D列印市場規模、佔有率和成長分析(按產品、組件、車輛類型、材料和地區分類)-產業預測(2026-2033年) 汽車3D列印市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)

汽車3D列印市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年) 汽車3D列印市場:2025-2030年預測

汽車3D列印市場:2025-2030年預測 全球汽車3D列印市場

全球汽車3D列印市場 2025-2029 年全球 AI 影像轉 3D 生成器市場

2025-2029 年全球 AI 影像轉 3D 生成器市場 2032 年高性能生質塑膠市場預測:按產品類型、原料、製造流程、最終用戶和地區進行的全球分析

2032 年高性能生質塑膠市場預測:按產品類型、原料、製造流程、最終用戶和地區進行的全球分析