|

市場調查報告書

商品編碼

1693968

廣告科技-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Ad Tech - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

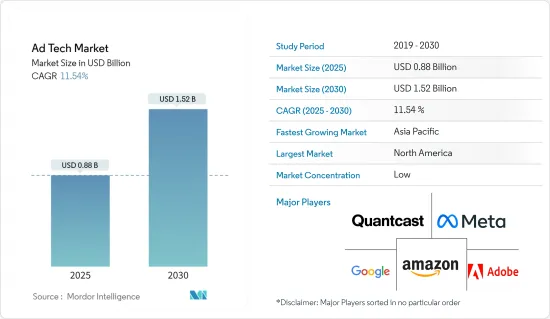

預計 2025 年廣告科技市場規模為 8.8 億美元,到 2030 年將達到 15.2 億美元,預測期內(2025-2030 年)的複合年成長率為 11.54%。

受數位設備和網路使用日益增多的推動,廣告科技市場在過去幾年中經歷了顯著成長。隨著智慧型手機和社群媒體平台的興起,數位廣告已成為全球企業行銷計畫的重要組成部分。

關鍵亮點

- 從傳統廣告到網路廣告的持續轉變是市場成長的主要動力。隨著網路的廣泛普及和網路用戶的增加,現在可以透過數位廣告覆蓋更廣泛的受眾。人們在網路上花費更多的時間在工作、娛樂和社交,廣告商有能力在網路上接觸到他們。

- 5G技術提供更低的延遲、更快的下載速度和更高的網路效率,預計將對廣告科技需求的成長產生重大影響。這些進步為廣告科技公司創造了新的機會,使其能夠提供創新、有針對性、數據主導的廣告解決方案,從而改善用戶體驗。

- 疫情期間,線上電子商務服務業也出現強勁成長。隨著越來越多的人轉向網路購物等數位服務,這些行業的公司增加了廣告支出以接觸潛在受眾。這導致對線上廣告的需求增加,尤其是在搜尋引擎和社交媒體平台上。

- 然而,大眾對廣告科技實踐缺乏認知,導致監管問題日益嚴重。消費者保護機構越來越擔心他們的資料被使用和收集用於廣告目的的方式,這導致了更嚴格的監管,威脅到廣告科技產業的發展。

- 新冠疫情為廣告業帶來了重大變化,其中一些變化預計將對該行業產生長期影響。由於消費者支出下降和經濟不確定性,許多品牌選擇削減廣告預算,導致廣告支出整體下降。這種下降趨勢在廣播、電視和印刷等傳統媒體平台上尤其明顯,這些平台的廣告收入大幅下降。同時,隨著人們在家中度過更多時間並轉向數位媒體,數位廣告支出大幅增加。隨著越來越多的人熟悉電子商務和數位管道,預計即使在疫情消退後,這種上升趨勢仍將持續下去。總體而言,這場疫情加速了該行業向數據主導方法和數位廣告管道的轉變,對該行業的未來產生了長期影響。

廣告科技市場趨勢

行動裝置和智慧型手機將經歷顯著成長

- 行動裝置上的廣告是企業與目標受眾建立聯繫和互動的重要工具。商業領域的小型企業可以利用該領域的視覺方面在行動裝置上創建引人注目的廣告,突出其產品和獨特的品牌身份驗證。

- 此外,行動裝置有多種形式的廣告,包括圖片文字廣告、橫幅廣告、點擊通話廣告、點擊訊息廣告和點擊下載廣告。此外,由於其移動性和便利性,人們最終會選擇智慧型手機設備而不是筆記型電腦和桌上型電腦。此外,由於行動平台能夠處理類似的任務,預計其獲利能力將越來越強。

- 賦予企業權力並使其能夠加入第四次工業革命的最新行銷策略包括數位廣告和行動行銷。鑑於我們將在不久的將來看到轉向線上銷售的小型企業數量大幅增加,智慧型手機使用率上升,以及缺乏現場活動和展覽,這可能會提供一個重要的廣告管道,並對線上廣告市場產生積極影響。

- 愛立信表示,近年來全球智慧型手機行動網路用戶總數已達到約64億,預計預測期內將超過77億人。行動網路智慧型手機用戶數量最多的國家是中國、印度和美國。因此,隨著全球智慧型手機行動網路用戶數量的不斷增加,預計該領域將迎來充足的成長機會。

- 因此,隨著越來越多的顧客使用行動裝置瀏覽和購買商品,行動廣告對於時尚企業來說變得越來越重要。為了接觸並吸引目標受眾,企業正在大幅增加對行動廣告的投資。

亞太地區:預計大幅成長

- 近年來,中國經濟的不斷成長和技術熟練的人口推動了網路消費和行動裝置普及率的上升。隨著社群媒體的普及,該國的廣告科技產業正在快速發展。中國是百度、騰訊和阿里巴巴等科技巨頭的所在地。基於影片的平台的日益成長的趨勢也推動了該地區對各種廣告形式的需求。

- 數位革命和網路普及率的提高正在推動印度廣告科技市場的發展。網路購物和其他數位服務的興起,以及對數位廣告(主要來自搜尋引擎和社交媒體平台)日益成長的需求,迫使印度廣告科技行業的公司增加廣告支出。

- 由於對數據、自動化、人工智慧和程式化廣告的投資增加,日本的廣告科技市場預計將成長。新市場參與企業和創新的出現在日本的廣告科技科技生態系統中發揮關鍵作用。隨著日本行動應用生態系統的不斷擴大,預計預測期內行動廣告支出將會增加,為廣告科技公司創造龐大的機會。此外,進入日本市場的影片廣告分發平台數量也在增加。

- 澳洲日益成長的數位和網路普及率正在幫助推動該地區廣告科技市場的成長。人工智慧 (AI)、機器學習 (ML)、虛擬實境 (VR) 和擴增實境(AR) 技術的日益普及預計將為廣告科技公司提供豐厚的成長機會。社群媒體應用程式的日益普及和遊戲產業的興起也為澳洲廣告科技市場的成長創造了許多選擇。

- 在韓國,不斷增加的投資、官民合作關係以及不斷成長的數位遊戲市場預計將為行銷人員提供在高度互動的戶外(OOH) 環境中吸引觀眾的絕佳機會。程序化數位戶外廣告為媒體所有者開闢了新的收益來源,帶來了額外的收益。

- 創新創新、技術採用和對道德廣告的奉獻精神的結合將決定紐西蘭在全球廣告科技市場中的地位。隨著市場預期擴張、重視在地化和法規合規,紐西蘭完全有能力影響數位廣告的變革。

廣告科技產業概覽

廣告科技市場分散,大公司和小公司之間的競爭非常激烈。參與企業包括 Adobe、Google LLC、Amazon.com Inc.、Meta Platform Inc. 和 Quantcast。該市場的參與企業正在採取合作和收購等策略來增強其產品供應並獲得永續的競爭優勢。

- 2023 年 10 月 - Meta 為廣告主推出首個生成式 AI 功能,讓他們可以使用 AI 創建背景、縮放圖像並根據原始副本生成多個版本的廣告文字。第一個新功能允許廣告商透過產生多個不同的背景來客製化他們的創新資產,以改變他們的產品圖像的外觀。另一個功能「圖像拉伸」允許廣告商縮放其資產以適應各種產品(如供稿和捲軸)所需的不同長寬比。

- 2023 年 7 月—宏盟集團與Google合作,將Google的生成式人工智慧模型整合到其廣告科技平台中。此次整合旨在增強宏盟廣告科技平台的功能,同時提供更個人化和有效的廣告機會。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 評估新冠疫情對各行業的影響

- 宏觀經濟趨勢的影響

第5章市場動態

- 市場促進因素

- 智慧型手機和社群媒體的普及率不斷提高

- 數位廣告:精準、有效、經濟

- 市場限制

- 在認知度較低的情況下,點擊機器人和安裝劫持現象增多

- 廣告數位化

- 出版商可以更多地存取客戶數據

- 創造新的收益源

- 透過建議引擎個人化改善觀看體驗

- 基於位置的廣告

- 顧客行為分析有助於形成消費模式

- 加強與科技公司的夥伴關係和合作

第6章市場區隔

- 按平台

- 供應端平台(SSP)

- 需求端平台(DSP)

- 廣告交易平臺

- 資料管理

- 按廣告格式

- 影片廣告

- 社群媒體

- 搜尋廣告

- 電子郵件

- 其他廣告格式

- 按設備平台

- 桌面

- 行動智慧型手機

- 其他設備平台

- 按最終用戶產業

- 零售與電子商務

- 醫療保健

- BFSI

- 服務業(旅館業、觀光業、法律服務)

- 通訊業

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 紐西蘭

- 其他亞太地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 奈及利亞

- 埃及

- 其他中東和非洲地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 其他拉丁美洲

- 北美洲

第7章競爭格局

- 公司簡介

- Google LLC

- Amazon.com, Inc.

- Meta Platform, Inc.

- Quantcast

- Adobe

- Adform A/S

- MediaMath

- Microsoft Corporation

- Zeta Global Holdings Corp.

- Mediaocean

第8章投資分析

The Ad Tech Market size is estimated at USD 0.88 billion in 2025, and is expected to reach USD 1.52 billion by 2030, at a CAGR of 11.54% during the forecast period (2025-2030).

The ad tech market has witnessed considerable growth over the past few years, driven by the growing use of digital devices and the Internet. With the increasing adoption of smartphones and social media platforms, digital advertising has become essential to marketing plans for businesses worldwide.

Key Highlights

- The continuous shift from traditional to online advertising is the main driving force behind the market's growth. The proliferation of the Internet and the increase in the number of Internet users has made it possible to reach a larger audience through digital ads. People spend more time online for work, entertainment, and socializing, and advertisers can now reach them online.

- 5G technology is expected to significantly impact ad tech demand growth, offering lower latency, faster download speeds, and improved network efficiency. These advances introduce new opportunities for ad tech companies to provide targeted, innovative, data-driven advertising solutions to enhance user experience.

- The online and e-commerce services sector also significantly boosted during the pandemic. As more people turn to digital services such as online shopping, companies in these industries have increased their advertising spending to reach potential audiences. This has increased the demand for online advertising, especially on search engines and social media platforms.

- However, a lack of public awareness of ad tech practices has led to augmented regulatory concerns. Consumer protection agencies are becoming increasingly concerned about data being used and collected for advertising efforts, leading to strict regulations that threaten the growth of the ad tech industry.

- The COVID-19 pandemic has brought about significant transformations in the advertising industry, and several of these changes are expected to have a long-lasting impact on the sector. With reduced consumer spending and economic uncertainty, many brands have opted to decrease their advertising budgets, leading to an overall decrease in ad spending. This decline has been particularly noticeable in traditional media platforms such as radio, television, and print media, which have experienced a sharp decrease in advertising revenues. On the other hand, as people spend more time at home and engage with digital media, there has been a substantial increase in digital ad spending. This upward trend is predicted to persist even after the pandemic subsides as more individuals become acquainted with e-commerce and digital channels. Overall, the pandemic has augmented the industry's shift to a more data-driven approach and digital advertising channels, with long-term effects for the sector's future.

Ad Tech Market Trends

Mobile Devices and Smartphones to Witness Significant Growth

- Advertising on mobile devices acts as a significant tool for firms to connect with and interact with their target audience. Small firms in the business sector may make use of the visual aspect of the sector to create engaging advertising on mobile devices that highlights their offerings and distinctive brand identities.

- Furthermore, there are several forms of advertising for mobile devices, such as image text and banner ads, click-to-call ads, click-to-message ads, and click-to-download ads. Additionally, due to their mobility and ease, people ultimately choose smartphone devices over laptops or desktops. Also, due to the former's ability to undertake similar tasks, mobile platforms are predicted to become increasingly profitable.

- Modern marketing strategies that would empower firms and bring them into the fourth industrial revolution include digital advertising and mobile marketing. In due course, it would supply the essential advertising channels and prove to produce a good influence on the online advertising market, given the significant number of SMEs transitioning to online sales, rising smartphone usage, and the lack of on-ground events or exhibits in the near future.

- According to Ericsson, the total number of smartphone mobile network subscriptions worldwide reached around 6.4 billion in the recent years and is forecasted to surpass 7.7 billion during the forecast period. China, India, and the United States are the countries with the most significant number of smartphone mobile network subscriptions. Hence, with the rise in the overall number of smartphone mobile network subscriptions worldwide, the market is expected to witness ample opportunities to grow within the market sector.

- Therefore, as more customers use their mobile devices to explore and buy things, mobile advertising is becoming more crucial for the fashion business. In order to reach and interact with their target audience, firms are increasing their investment in mobile advertising significantly.

Asia-Pacific Expected to Witness Major Growth

- China's economic growth and a rising tech-savvy population have resulted in higher penetration of internet consumption and mobile device penetration in recent years. Due to the increased proliferation of social media, the ad tech industry is growing rapidly in the country. China hosts several tech giants such as Baidu, Tencent, and Alibaba. The rising inclination toward video-based platforms has also increased the demand for various advertising formats in the region.

- The digital revolution and growing internet penetration are driving the ad tech market in India. The rise of online shopping and other digital services, as well as increasing demand for digital advertising, especially on search engines and social media platforms, have compelled businesses in the Indian ad tech industry to increase their advertisement spending.

- The ad tech market in Japan is anticipated to grow due to increasing investment in data, automation, artificial intelligence, and programmatic advertising. The emergence of new market players and innovation plays a critical role in the ad tech ecosystem in Japan. Mobile ad spending is projected to increase in Japan during the forecast period, attributed to the country's expanding mobile app ecosystem, representing a massive opportunity for ad tech companies. Japan also has an increased influx of video advertising serving platforms entering the Japanese market.

- The rising digital and internet penetration in Australia is bolstering the growth of the regional ad tech market. The rising adoption of artificial intelligence (AI), machine learning (ML), Virtual reality (VR), and augmented reality (AR) technologies is expected to provide lucrative growth opportunities for advertising technology players. The growing use of social media apps and the rising gaming industry also create numerous options for the ad tech market growth in Australia.

- Increased investments, public-private partnerships, and the ever-growing digital gaming market are projected to provide tremendous opportunities for marketers to attract audiences in highly interactive out-of-home (OOH) environments in South Korea. Programmatic Digital out-of-home advertising is opening up new revenue streams for media owners to drive additional revenues.

- A combination of creative innovation, technical adoption, and a dedication to ethical advertising define New Zealand's position in the global ad tech market. Because of the market's projected expansion and emphasis on regional specifics and legal compliance, New Zealand is positioned to have a significant impact on the changing face of digital advertising.

Ad Tech Industry Overview

The Ad tech market is fragmented, with high competition among large and small companies. Some of the players include Adobe, Google LLC, Amazon.com Inc., Meta Platform Inc., and Quantcast. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- October 2023 - Meta launched its first generative AI features for advertisers, allowing them to use AI to create backgrounds, expand images, and generate multiple versions of ad text based on their original copy. The first among the trio of new features allows an advertiser to customize their creative assets by generating multiple different backgrounds to change the look of their product images. Another feature, image expansion, allows advertisers to adjust their assets to fit different aspect ratios required across various products, like Feed or Reels.

- July 2023 - Omnicom has partnered with Google to integrate the latter's generative AI models into its Adtech platform. The integration aims to improve the capabilities of Omnicom's Adtech platform while providing personalized and effective advertising opportunities.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 An Assessment of the Impact of COVID-19 on the Industry

- 4.3 Impact of Macroeconomic Trends

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rise in the Adoption of Smartphones and Social Media

- 5.1.2 High Precision, Effectiveness, and Cost Efficiency of Digital Advertising

- 5.2 Market Restraint

- 5.2.1 Rise of Click Bots and Install Hijacks Amid Low Public Awareness

- 5.3 Digital Transformation in Advertising

- 5.3.1 Increased Access of Customer Data for Publishers

- 5.3.2 Generation of New Revenue Streams

- 5.3.3 Better Viewer Experience Through Personalization Through Recommendation Engines

- 5.3.4 Location-Based Advertising

- 5.3.5 Customer Behavior Analytics Helping with Spending Pattern

- 5.3.6 Increasing Partnerships and Collaboration with Technology Companies

6 MARKET SEGMENTATION

- 6.1 By Platform

- 6.1.1 Supply Side Platform (SSP)

- 6.1.2 Demand Side Platform (DSP)

- 6.1.3 Ad Exchange

- 6.1.4 Data Management

- 6.2 By Ad Format

- 6.2.1 Video Advertising

- 6.2.2 Social Media

- 6.2.3 Search Advertising

- 6.2.4 Email

- 6.2.5 Other Ad Formats

- 6.3 By Device Platforms

- 6.3.1 Desktop

- 6.3.2 Mobile Devices and Smartphones

- 6.3.3 Other Device Platforms

- 6.4 By End-user Industry

- 6.4.1 Retail and E-Commerce

- 6.4.2 Healthcare

- 6.4.3 BFSI

- 6.4.4 Services (Hospitality, Tourism, Legal Services)

- 6.4.5 Telecommunications

- 6.4.6 Other End-user Industries

- 6.5 By Geography

- 6.5.1 North America

- 6.5.1.1 United States

- 6.5.1.2 Canada

- 6.5.2 Europe

- 6.5.2.1 United Kingdom

- 6.5.2.2 Germany

- 6.5.2.3 France

- 6.5.2.4 Spain

- 6.5.2.5 Italy

- 6.5.2.6 Rest of Europe

- 6.5.3 Asia-Pacific

- 6.5.3.1 China

- 6.5.3.2 India

- 6.5.3.3 Japan

- 6.5.3.4 Australia

- 6.5.3.5 South Korea

- 6.5.3.6 New Zealand

- 6.5.3.7 Rest of Asia-Pacific

- 6.5.4 Middle-East and Africa

- 6.5.4.1 Saudi Arabia

- 6.5.4.2 United Arab Emirates

- 6.5.4.3 South Africa

- 6.5.4.4 Nigeria

- 6.5.4.5 Egypt

- 6.5.4.6 Rest of Middle East and Africa

- 6.5.5 Latin America

- 6.5.5.1 Brazil

- 6.5.5.2 Mexico

- 6.5.5.3 Argentina

- 6.5.5.4 Colombia

- 6.5.5.5 Rest of Latin America

- 6.5.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Google LLC

- 7.1.2 Amazon.com, Inc.

- 7.1.3 Meta Platform, Inc.

- 7.1.4 Quantcast

- 7.1.5 Adobe

- 7.1.6 Adform A/S

- 7.1.7 MediaMath

- 7.1.8 Microsoft Corporation

- 7.1.9 Zeta Global Holdings Corp.

- 7.1.10 Mediaocean

8 INVESTMENT ANALYSIS

廣告科技市場規模、佔有率和成長分析:按技術、廣告格式、部署類型、組織規模、最終用戶和地區分類-2026-2033年產業預測

廣告科技市場規模、佔有率和成長分析:按技術、廣告格式、部署類型、組織規模、最終用戶和地區分類-2026-2033年產業預測 廣告科技市場:2026-2032年全球市場預測(按組件、廣告管道、部署模式和最終用戶分類)

廣告科技市場:2026-2032年全球市場預測(按組件、廣告管道、部署模式和最終用戶分類) 廣告科技市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、部署、最終用戶及解決方案分類

廣告科技市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、部署、最終用戶及解決方案分類 2026 年 AdTech 全球市場報告

2026 年 AdTech 全球市場報告 廣告技術市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034)

廣告技術市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034) 廣告科技市場-全球產業規模、佔有率、趨勢、機會與預測:按類型、組織規模、定價類型、最終用戶、通路類型、地區和競爭格局分類,2021-2031年

廣告科技市場-全球產業規模、佔有率、趨勢、機會與預測:按類型、組織規模、定價類型、最終用戶、通路類型、地區和競爭格局分類,2021-2031年 廣告科技市場規模、佔有率和成長分析(按產品、廣告類型、廣告管道、廣告格式、平台、公司規模、垂直產業和地區分類)—產業預測(2026-2033 年)

廣告科技市場規模、佔有率和成長分析(按產品、廣告類型、廣告管道、廣告格式、平台、公司規模、垂直產業和地區分類)—產業預測(2026-2033 年) 廣告科技的全球市場:提供區分·部署模型·組織規模·廣告類型·終端用戶產業·各地區的機會及預測 (2018-2032年)

廣告科技的全球市場:提供區分·部署模型·組織規模·廣告類型·終端用戶產業·各地區的機會及預測 (2018-2032年) 廣告科技市場規模、佔有率和趨勢分析報告:按平台、解決方案、廣告類型、公司規模、行業、地區和細分市場預測,2025-2030 年

廣告科技市場規模、佔有率和趨勢分析報告:按平台、解決方案、廣告類型、公司規模、行業、地區和細分市場預測,2025-2030 年 2025-2029 年全球廣告科技市場

2025-2029 年全球廣告科技市場