|

市場調查報告書

商品編碼

1693700

印度軟體服務出口 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)India Software Services Export - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

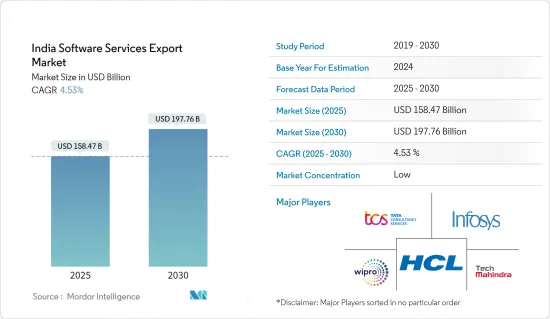

印度軟體服務出口市場規模預計在 2025 年為 1,584.7 億美元,預計到 2030 年將達到 1977.6 億美元,預測期內(2025-2030 年)的複合年成長率為 4.53%。

北美和歐洲國家的雲端轉型高成本,缺乏合適的資源,因此選擇印度,因為印度處於境外外包外包的前沿,並且正在更新新趨勢、新技術和新技巧。預計這些因素將有助於預測期內市場的擴張。

關鍵亮點

- 各行各業的快速數字轉型、物聯網、人工智慧和區塊鏈等新技術的採用,以及透過外包非核心業務越來越注重利用核心競爭力,是市場的主要驅動力。

- 數位轉型 (DX) 和 IT 現代化支出已成為印度企業的首要任務,因為他們傾向於使用雲端、人工智慧 (AI)、自動化、網路基礎設施、物聯網 (IoT) 和其他先進技術進行數位轉型。

- 向雲端服務的日益轉變是市場的主要驅動力,從而帶來了可觀的收益合作。雲端遷移允許大大小小的企業將其軟體應用程式、資料庫和其他 IT 資源遷移到雲端伺服器,從而創建一個無縫、安全和透明的系統。這使得企業軟體開發生命週期流程管理更有效率。企業通常會投資雲端遷移策略,以獲得更好的可擴展性、可用性和更快的軟體服務部署。

- 印度的國家軟體產品政策部分由下一代孵化計劃(NGIS)解決,該計劃已獲核准用於支援軟體產品生態系統。蓬勃發展的軟體產品生態系統旨在幫助持續擴大強大的 IT 產業、創造新的就業機會並提高競爭力。根據NASSCOM估計,印度軟體產品產業在23會計年度的營收將創下歷史新高,達到142億美元。

- 然而,管理法規和合規需求等因素可能會在預測期內抑制市場成長。這會給企業帶來成本,因為它會增加營運成本,由於嚴格的資料保護法而限制服務交付,並且由於需要不斷適應不斷變化和發展的法規而轉移創新和擴張努力的資源。

- 此外,在新冠疫情爆發後,許多公司都安排員工在家工作,這大大增加了對高效 IT 系統的需求。越來越多的組織正在將其應用程式和軟體遷移到雲端和雲端基礎的平台。這種情況大大增加了被調查市場的成長機會。

印度軟體服務出口市場趨勢

對基礎設施現代化、數位支援和雲端服務的需求不斷成長

- 基礎設施現代化涉及增強組織的 IT 設置,旨在提高效能、可擴展性和安全性。這包括將舊系統遷移到雲端基礎的平台、採用容器化以及整合自動化和 DevOps 方法。主要目標是提高靈活性、降低營運成本、加速數位轉型並使企業始終走在技術趨勢和客戶需求的前沿。

- 對網路安全、營運效率和成本效益的日益關注正在推動基礎設施現代化。這些改進將使印度軟體服務供應商不僅能夠滿足全球客戶不斷變化的需求,而且還能透過提供高品質、創新和安全的解決方案在國際市場上保持競爭力。

- 印度正在向已開發市場經濟轉型,先進技術的採用預計將在這一過程中發揮關鍵作用。此外,印度財政部長在該國臨時預算中強調了印度數位基礎設施在推動現代經濟正規化方面的作用。 Vi Business(沃達豐 Idea 的子公司)最近對近 1,000 家中小微型企業進行的一項調查顯示,各個垂直行業的企業中,只有不到 60% 實現了數位化。

- 據印度電子和資訊技術部稱,印度的 IT/ITeS 產業具有全球重要性,是出口和創造就業機會的重要推動力。國內 IT-BPM 產業(不包括電子商務)價值 2,540 億美元,預計 2023-24 會計年度出口額將達到 2,000 億美元左右(估計)。此外,IT-ITeS 行業預計將大幅增加就業,僱用約 543 萬名專業人員。這比上年度年(2022-2023 年)增加了 6 萬人。值得注意的是,女性佔該行業勞動力的36%。

- 市場相關人員正在幫助企業建立數位轉型 IT 策略。例如,2024 年 3 月,塔塔諮詢服務公司宣布與總部位於丹麥的夥伴關係、工程和顧問公司 Ramboll 建立價值數百萬美元的策略合作夥伴關係,以協助其實現端到端 IT 轉型。該公司的目標是在未來七年內實現 Ramboll 的 IT 營運模式現代化和簡化,並推動 IT 業務成長。

IT服務可望佔據主要市場佔有率

- 許多國家一直將 IT業務出口到印度等新興經濟體,以節省人事費用。許多大型 IT 服務出口公司已在印度開展業務,預計未來幾年 IT 服務出口需求將獲得顯著成長。隨著世界經歷數位轉型,企業正在迅速升級其傳統IT基礎設施,從而產生了對印度 IT 諮詢和實施服務的需求。數位轉型在確定IT服務及其重要性、進一步將IT服務組織到計劃-建構-運行的活動框架中以及定義組織的IT服務策略方面為企業提供了策略和競爭優勢。

- 印度的 IT 服務格局正在快速改變。巨量資料和機器學習等先進技術在各個終端用戶行業的廣泛應用正在推動IT基礎設施更新的需求。採用這些新技術也使企業能夠更換過時的基礎設施和硬體,從而推動印度 IT 服務領域的成長。此外,隨著IT營運在雲端基礎平台上的推進,IT服務越來越數據主導、即時化,為企業創造了巨大的價值,特別是在提高業務效率、發掘機會、最佳化遠端存取等方面。根據NASSCOM的數據,對先進、現代化數位基礎設施的投資幫助印度科技產業成長了2,450億美元。

- 此外,雲端運算被視為企業、政府和消費者的變革技術。雲端運算不僅支援數位轉型,還促進了IT生態系統參與企業之間的創新和協作。根據印度國際貿易部的數據,ICT產業和數位經濟合計佔印度GDP的13%以上,是印度經濟的重要支柱。印度有一個雄心勃勃的目標:到2025年將其ICT產業的估值提高到1兆美元。

- IT服務供應商也與各種最終用戶公司夥伴關係,幫助他們採用先進技術。 2024年2月,Wipro宣布將成為Agne的大股東。此舉使 Wipro 能夠獲得 Agne 的先進技術和專業知識,從而鞏固其在產物保險行業的地位。 Wipro 和 Agne 的全面能力將有助於利用科技為產物保險業的客戶提供更快的上市時間和有競爭力的服務。

- 此外,用戶數量的增加也推動了對 CRM、收費和網路管理系統等電訊專用軟體解決方案的需求,這大大推動了市場成長。增強的連接和通訊能力將增加遠端協作和外包的機會,使軟體服務供應商能夠在全球範圍內提供服務。此外,通訊的進步將促進創新應用和數位服務的發展,擴大軟體出口商的市場機會。電訊擴張和軟體需求之間的這種協同效應正在極大地推動市場成長。根據TRAI統計,截至2023年12月,印度德里都市區電訊用戶超過5,800萬,測量期間印度全國都市區電訊用戶總數超過6.62億。

印度軟體服務出口產業概況

印度軟體服務出口產業市場呈現細分化。塔塔諮詢服務有限公司、印孚瑟斯有限公司、威普羅有限公司、HCL 科技、Tech Mahindra 有限公司等是主要企業。公司不斷創新並形成策略聯盟以保持市場佔有率。

- 2024 年 4 月:HCL Tech 宣布與 Google Cloud 合作建立產業解決方案並部署多模態大規模語言 AI 模型 Gemini。 HCL 計劃利用 Gemini 先進的程式碼完成和摘要功能來增強其 HCL Tech AI Force 平台,使工程師能夠有效率地編寫程式碼、解決問題、縮短交付時間並提高客戶軟體計劃的品質。

- 2024 年 2 月:技術服務和顧問公司 Wipro Limited推出了Wipro 企業人工智慧 (AI) 就緒平台,使客戶能夠建立企業級、完全整合和客製化的 AI 環境。該平台包括投資人工智慧所需的基礎設施和核心軟體,用於自動化和產生人工智慧工作負載的消耗,動態資源管理,使用預測分析動態調整以適應不斷變化的工作負載,以及投資減少事故並提高企業業務效率。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 宏觀經濟趨勢如何影響市場

第5章市場動態

- 市場促進因素

- 疫情挑戰推動基礎設施現代化、數位支援和雲端服務需求

- 政府改革以支持IT產業,減少合規性,提高生產力並增強國際競爭力

- 市場限制

- 管理全球監管和合規需求

- 軟體服務趨勢和技術發展

- 區域分析

- 卡納塔克邦

- 泰米爾納德邦

- 特倫甘納邦

- 馬哈拉斯特拉邦

- 北方邦

- 哈里亞納邦

第6章市場區隔

- 按活動

- IT服務

- 軟體產品開發

- BPO服務

- 工程服務

- 按服務類型

- 現場

- 異地

- 按出口目的地

- 北美洲

- 歐洲

- 亞太地區

- 其他

第7章競爭格局

- 公司簡介

- Tata Consultancy Services Limited

- Infosys Limited

- Wipro Limited

- HCL Technologies

- Tech Mahindra Ltd

- Mphasis Limited

- Oracle Corporation

- LTIMindtree Limited

- Microsoft Corporation

- Capgemini Technology Services India Ltd

- IBM Corporation

- Accenture PLC

- Deloitte Touche Tohmatsu Limited

- PWC LLP

第8章 取得公司列表

第9章 諮詢機構名錄

第10章投資分析

第11章 市場的未來

The India Software Services Export Market size is estimated at USD 158.47 billion in 2025, and is expected to reach USD 197.76 billion by 2030, at a CAGR of 4.53% during the forecast period (2025-2030).

As the cloud transformation in the North American and European nations involves high costs and lacks proper resources, India is preferred as it is at the forefront of offshoring and outsourcing and is updated with emerging trends, techniques, and technology. This factor is expected to contribute to the market's expansion during the forecast period.

Key Highlights

- Rapidly increasing digital transformation across industries, adoption of new technologies such as IoT, AI, and blockchain, and a growing emphasis on leveraging the core competencies by outsourcing non-core operations are the major driving factors of the market.

- As Indian organizations gravitate toward the cloud, artificial intelligence (AI), automation, network infrastructure, Internet of Things (IoT), and other developed technologies to transform them digitally, spending on digital transformation (DX) and IT modernization are the top priorities of Indian companies.

- The growing migration to cloud services is a crucial driving factor in the market studied, resulting in significant collaborations generating revenue from it. Cloud migration facilitates both large and small businesses to move their software applications, databases, and other IT resources to cloud servers for seamless, secure, and transparent systems. This allows the company's software development lifecycle process management to be more efficient. Businesses generally invest in cloud migration strategies for better scalability, availability, and quicker deployment of software services.

- The Indian National Policy on Software Products has been addressed partly by the Next Generation Incubation Scheme (NGIS), which has been approved to support the software product ecosystem. It is planned to build a thriving software product ecosystem to support the strong IT sector's sustained expansion, new job creation, and competitiveness improvement. As per NASSCOM estimate, the Indian Software Product industry has made historic achievements in revenue in FY 2023, reaching USD 14.2 billion.

- However, factors like managing regulatory and compliance needs can restrain the market's growth during the forecast period. It is because this involves increasing operational costs, limiting service offerings due to stringent data protection laws, and diverting resources from innovation and expansion efforts due to the constant need to adapt to varying and evolving regulations.

- Furthermore, after the COVID-19 pandemic, several businesses have employees working from home, and the need to adopt efficient IT systems has increased substantially. Organizations have increasingly migrated to the cloud or cloud-based platforms for their applications and software. This situation has significantly augmented the growth opportunities for the market studied.

India Software Services Export Market Trends

Increasing Demand for Infrastructure Modernization, Digital Support, and Cloud Services

- Infrastructure modernization involves enhancing an organization's IT setup for better performance, scalability, and security. This encompasses transitioning from older systems to cloud-based platforms, embracing containerization, and integrating automation and DevOps methodologies. The primary goal is to boost agility, cut operational expenses, and facilitate digital transformation, empowering businesses to stay ahead of tech trends and customer needs.

- The increasing emphasis on cybersecurity, operational efficiency, and cost-effectiveness is driving the push for infrastructure modernization. These enhancements empower Indian software service providers to not only meet the evolving demands of global clients but also to stay competitive in the international market by delivering high-quality, innovative, and secure solutions.

- India is on a journey to transition into a developed market economy and advanced technology deployment, which is expected to play a significant part in this process. Moreover, India's Finance Minister has emphasized India's digital infrastructure in driving economic formalization in the modern era in the country's interim budget. According to a recent survey by Vi Business (the Arm of Vodafone Idea), nearly one lakh MSMEs said that less than 60% of businesses had embraced digitalization across various verticals.

- As per the Ministry of Electronics and Information Technology, India's IT/ITeS industry holds a significant global position, significantly bolstering exports and job creation. The nation's IT-BPM sector (excluding e-commerce) is poised to hit a valuation of USD 254 billion, with exports making up approximately USD 200 billion in the fiscal year 2023-24 (estimated). The IT-ITeS industry has also significantly bolstered employment and is anticipated to employ a total workforce of around 5.43 million professionals. This marks an increase of 60,000 individuals from the previous fiscal year (FY 2022-2023). Notably, women constitute 36% of the industry's workforce.

- The market players are helping companies build their digital transformation IT strategies. For instance, in March 2024, Tata Consultancy Services declared the multimillion-dollar strategic partnership to support the end-to-end IT transformation of Ramboll, an architecture, engineering, and consultancy company headquartered in Denmark. The company would modernize and streamline Ramboll's IT operating model to strive for business growth in IT over the next seven years.

IT Services Expected to Capture Significant Market Share

- Many countries have long exported IT work to developing economies like India to save on labor costs. With the country housing many major IT service export players, the demand for IT services export is expected to gain significant momentum in India in the coming years. In the wake of digital transformation worldwide, companies are rapidly upgrading their legacy IT infrastructure, thus creating demand for IT consulting and implementation services in India. Digital transformation provides companies with a strategic and competitive advantage in terms of determining IT services and their importance, further organizes the IT services as an activity of a plan-build-run framework, and defines the IT service strategy for the organization.

- The landscape of IT services in India is changing rapidly. The proliferation of advanced technologies, like big data and machine learning in various end-user industries, fuels the need for updated IT infrastructure. In addition, this adoption of emerging technologies enables businesses to replace outdated infrastructure and hardware, driving the IT services segment's growth in India. Moreover, due to advancements in IT operation across the cloud-based platform, IT services have become more data-driven and real-time, creating greater value for the business, especially in operational efficiency, business opportunity discovery, and remote access optimization. As per data by NASSCOM, the technology sector grew by USD 245 billion in India due to investments in advanced and modern digital infrastructure.

- Furthermore, cloud computing is envisioned as a transformative technology for enterprises, governments, and consumers. It not only supports digital transformation but also enables innovation and collaboration among the IT ecosystem players. According to the International Trade Administration, the ICT sector and the digital economy collectively account for over 13% of India's GDP, making them pivotal economic pillars. India has set an ambitious target, aiming to elevate the ICT sector to a USD 1 trillion valuation by 2025, representing a significant 20% of the projected GDP.

- In addition, IT service providers are indulging in partnerships with various end-user companies to assist them with advanced technology implementation. In February 2024, Wipro announced becoming a majority shareholder in Aggne. This move strengthens Wipro's position in the property and casualty (P&C) insurance industry by giving them access to Aggne's advanced technology and expertise. The integrated capabilities of Wipro and Aggne will help leverage technologies to deliver faster speed-to-market and more competitive services to clients in the P&C sector.

- Furthermore, the rising number of telecom subscribers is driving the market's growth significantly, as it increases the demand for telecom-specific software solutions, such as CRM, billing, and network management systems. Enhanced connectivity and communication capabilities boost remote collaboration and outsourcing opportunities, enabling software service providers to deliver their services globally. In addition, telecom advancements promote the development of innovative applications and digital services, expanding market opportunities for software exporters. This synergy between telecom expansion and software demand fuels the growth of the market significantly. According to TRAI, as of December 2023, there were over 58 million urban telecom subscribers in Delhi, India, and the total number of urban telecom subscribers across India during the measured time period was more than 662 million.

India Software Services Export Industry Overview

The Indian software services export industry market is fragmented. Tata Consultancy Services Limited, Infosys Limited, Wipro Limited, HCL Technologies, and Tech Mahindra Ltd are among the major companies. The corporations continue to innovate and form strategic partnerships to maintain their market share.

- April 2024: HCL Tech announced an alliance with Google Cloud to establish industry solutions and deploy Gemini for its multimodal large-language AI model. HCL planned to boost the HCL Tech AI Force platform with Gemini's advanced code completion and summarization capabilities, which allow engineers to code efficiently, solve issues, reduce delivery time, and enhance the quality of software projects for clients.

- February 2024: Wipro Limited, a technology services and consulting company, launched the Wipro Enterprise Artificial Intelligence (AI)-Ready Platform to help clients create enterprise-level, fully integrated, and customized AI environments. This platform provides the necessary infrastructure and core software for the consumption of AI and generative AI workloads for automation, dynamic resource management to adjust to varying workloads using predictive analytics dynamically, and investment in improvements in incident reduction and operational efficiency in the enterprise.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Infrastructure Modernization, Digital Support, and Cloud Services Owing to Pandemic Challenges

- 5.1.2 Government Reforms Aiding IT Industry that has Reduced Compliance, Increased Productivity, and Increased Global Competitiveness

- 5.2 Market Restraints

- 5.2.1 Managing Regulatory and Compliance Needs Across the World

- 5.3 Trends and Technology Developments in Software Services

- 5.4 Regional Analysis

- 5.4.1 Karnataka

- 5.4.2 Tamil Nadu

- 5.4.3 Telangana

- 5.4.4 Maharashtra

- 5.4.5 Uttar Pradesh

- 5.4.6 Haryana

6 MARKET SEGMENTATION

- 6.1 By Activity

- 6.1.1 IT Services

- 6.1.2 Software Product Development

- 6.1.3 BPO Services

- 6.1.4 Engineering Services

- 6.2 By Services Type

- 6.2.1 On-site

- 6.2.2 Off-site

- 6.3 By Export Destination

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Tata Consultancy Services Limited

- 7.1.2 Infosys Limited

- 7.1.3 Wipro Limited

- 7.1.4 HCL Technologies

- 7.1.5 Tech Mahindra Ltd

- 7.1.6 Mphasis Limited

- 7.1.7 Oracle Corporation

- 7.1.8 LTIMindtree Limited

- 7.1.9 Microsoft Corporation

- 7.1.10 Capgemini Technology Services India Ltd

- 7.1.11 IBM Corporation

- 7.1.12 Accenture PLC

- 7.1.13 Deloitte Touche Tohmatsu Limited

- 7.1.14 PWC LLP

8 LIST OF CAPTIVES

9 LIST OF PURE-PLAY ADVISORY COMPANIES

10 INVESTMENT ANALYSIS

11 FUTURE OF THE MARKET

2026年全球教育科技數位轉型市場報告2026年全球數位轉型市場報告

2026年全球教育科技數位轉型市場報告2026年全球數位轉型市場報告 2026-2030年全球數位轉型服務市場

2026-2030年全球數位轉型服務市場 數位轉型市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、部署、最終用戶、流程和解決方案分類

數位轉型市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、部署、最終用戶、流程和解決方案分類 2026-2034年全球數位轉型市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球數位轉型市場規模、佔有率、趨勢和成長分析報告 日本數位轉型市場:規模、佔有率、趨勢和預測:按類型、部署形式、企業規模、最終用戶產業和地區分類(2026-2034 年)

日本數位轉型市場:規模、佔有率、趨勢和預測:按類型、部署形式、企業規模、最終用戶產業和地區分類(2026-2034 年) 全球 AI RAN 市場(2026 年 1 月)區塊鏈數位轉型數位轉型市場-2026-2031年預測

全球 AI RAN 市場(2026 年 1 月)區塊鏈數位轉型數位轉型市場-2026-2031年預測 數位轉型市場-全球產業規模、佔有率、趨勢、機會及預測(依技術、最終用途、部署方式、地區及競爭格局分類,2021-2031年)

數位轉型市場-全球產業規模、佔有率、趨勢、機會及預測(依技術、最終用途、部署方式、地區及競爭格局分類,2021-2031年)