|

市場調查報告書

商品編碼

1693664

亞太燃料電池汽車:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)Asia-Pacific Fuel Cell Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

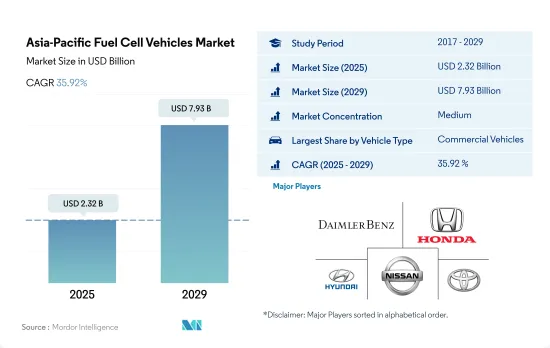

亞太地區燃料電池汽車市場規模預計在 2025 年為 23.2 億美元,預計到 2029 年將達到 79.3 億美元,預測期內(2025-2029 年)的複合年成長率為 35.92%。

展示該地區將燃料電池技術引入各類車輛的領先方法,並強調氫能作為交通運輸清潔能源來源的巨大潛力

- 亞太地區永續交通運輸正蓬勃發展,各領域的強勁成長就是明證。從乘用車到輕型商用車、貨車、中型和重型卡車以及公共汽車,該地區正在穩步擁抱綠色交通。尤其值得注意的是乘用車領域燃料電池電動車(FCEV)銷量的成長,凸顯了該地區在採用清潔交通方面的領導地位。預計 2017 年至 2023 年間銷售額將大幅成長,這一趨勢預計將持續到 2030 年。

- 在商用車領域,對氫燃料電池技術的戰略重點有望推動輕型和重型商用車領域的顯著成長。輕型商用車皮卡和貨車的銷量正在顯著成長,這表明物流和運輸行業正在向零排放汽車轉變。這項轉變是由氫能基礎設施投資和政府旨在抑制二氧化碳排放的獎勵所推動的。

- 除了燃料電池公車外,中型和重型商用卡車也呈現快速成長態勢,預計到 2030 年銷售量將大幅成長。亞太地區對燃料電池電動車的樂觀情緒凸顯了向氫能經濟邁出的重大一步,為全球採用清潔能源樹立了先例。政府措施、技術進步和綠氫生產成本下降是這項轉變的關鍵因素,使得 FCEV 對商業和客運的吸引力越來越大。

亞太地區的燃料電池汽車市場正在蓬勃發展,一些國家率先採用氫燃料技術。

- 世界各國政府為抑制和控制交通污染而採取的綠色能源旅行舉措是預計在不久的將來推動燃料電池商用車市場發展的關鍵因素之一。 2019 年 11 月,中國政府支持的卡車和巴士製造商北汽福田汽車表示,將投資 26 億美元用於替代能源汽車,包括燃料電池引擎。該公司計劃在2025年投放20萬輛新能源商用車。

- 幾家主要的OEM正在大力投資研發,並建立了戰略夥伴關係,以增強其商用車技術。 2020年1月,日本本田汽車工業與五十鈴汽車公司宣布將共同進行氫燃料電池動力來源重型卡車的研究,希望透過將零排放技術應用於重型車輛來擴大燃料電池的使用範圍。預計此類發展將促進亞太地區電動商用車市場的發展。

- 2020年,韓國將電動車購買補貼延長至2024年(乘用車)、2025年(公車和卡車)。獎金與價格上限掛鉤。售價低於6,000萬韓元的電動車可以獲得全額補貼,但售價在6,000萬韓元至9,000萬韓元之間的電動車只能獲得全額補貼的50%。此前,每輛車最高可獲得800萬韓元的補貼。

亞太燃料電池汽車市場趨勢

亞太地區的汽車貸款利率反映了每個國家的經濟策略,一些國家優先採取獎勵策略,而其他國家則採取更保守的立場。

- 過去幾年,這些數字發生了顯著變化。印尼和印度已大幅下調汽車貸款利率,顯示兩國在汽車銷售數據波動的情況下可能採取措施提振汽車產業。日本堅持傳統,維持名目利率,這是其超寬鬆貨幣政策延續的指標。馬來西亞在 2021 年經歷了急劇下滑,但在 2022 年重新站穩了腳跟,標誌著經濟實現了適應性再平衡。同時,紐西蘭和菲律賓則呈下降趨勢。泰國在 2020 年急劇下降,但在 2022 年開始再次上升。澳洲的歷程很有趣,每年都在穩步上升,這或許顯示了經濟韌性和策略超脫的結合。

- 2017年至2023年,亞太地區汽車貸款利率波動全景圖。印尼的利率最高,在 10% 至 11% 之間波動,這清楚地表明了其經濟狀況。相較之下,日本的利率一直維持在1%以下,反映了多年來為刺激經濟活動而實施的低利率。預計澳洲和紐西蘭將呈現更穩定的趨勢,到2019年將略有成長。同時,菲律賓在2017年以適度基數起步後,呈現大幅成長,在2019年達到7%以上的高峰。印度保持了穩定的節奏,保持在9-10%的範圍內,而馬來西亞則略有成長。相反,泰國卻呈現逐漸下滑的趨勢。

亞洲對電動車(EV)的需求激增,促使全球汽車製造商推出新產品,擴大了電動車和電池組的市場。

- 隨著亞太地區對電動車 (EV) 的需求不斷成長,許多汽車製造商正在採取策略推出適合這個快速成長的市場的創新產品。斯柯達於 2023 年 1 月宣布計劃將一款尖端電動 SUV 引入印度就是一個重要的例子。該車配備強大的82kWh電池,一次充電續航里程超過500公里。斯柯達計劃於 2023 年下半年推出這項舉措,象徵著席捲該地區的更廣泛趨勢。這些措施的推出不僅將刺激電動車的需求,還將推動亞太國家廣泛採用電池組。

- 隨著公共運輸成為亞太地區城市生活中越來越不可或缺的一部分,它激勵新一代製造商推出創新、環保的車型。 2022 年 4 月,印度先鋒新創新興企業Greencell Mobility 推出了其電動行動巴士服務品牌 NueGo。 GreenCell 計劃在印度南部、北部和西部三大地區部署 750 輛優質電動公車,以徹底改變城際通勤方式。最初的計劃是在 24 個城市推出 250 輛公車,但長期願景強調了該公司對加強環保公共交通的承諾。這些舉措預示著電動大眾運輸解決方案的蓬勃發展,未來幾年電動大眾運輸解決方案很可能在亞太地區得到更廣泛的應用。

亞太地區燃料電池汽車產業概況

亞太地區燃料電池汽車市場適度整合,前五大企業佔60%的市場。該市場的主要企業包括戴姆勒股份公司(梅賽德斯-奔馳股份公司)、本田汽車公司、現代汽車公司、日產汽車公司、豐田汽車公司等。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 人口

- 人均GDP

- 消費者汽車支出(cvp)

- 通貨膨脹率

- 汽車貸款利率

- 共乘

- 電氣化的影響

- 電動車充電站

- 電池組價格

- 新款 Xev 車型發布

- 物流績效指數

- 二手車銷售

- 燃油價格

- OEM生產統計

- 法規結構

- 價值鍊和通路分析

第5章市場區隔

- 汽車模型

- 商用車

- 公車

- 大型商用卡車

- 輕型商用皮卡車

- 輕型商用廂型車

- 中型商用卡車

- 商用車

- 國家

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 馬來西亞

- 韓國

- 泰國

- 其他亞太地區

第6章 競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- Ballard Power Systems

- Daihatsu Motor Co. Ltd.

- Daimler AG(Mercedes-Benz AG)

- Dongfeng Motor Corporation

- Honda Motor Co. Ltd.

- Hyundai Motor Company

- Mazda Motor Corporation

- Nissan Motor Co. Ltd.

- Toyota Motor Corporation

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 數據包

- 詞彙表

簡介目錄

Product Code: 93064

The Asia-Pacific Fuel Cell Vehicles Market size is estimated at 2.32 billion USD in 2025, and is expected to reach 7.93 billion USD by 2029, growing at a CAGR of 35.92% during the forecast period (2025-2029).

Demonstrates the region's advanced approach to implementing fuel cell technology in various vehicle types, indicating strong potential for hydrogen as a clean energy source in transportation

- The Asia-Pacific region is witnessing a surge in sustainable transportation, evident in its robust growth across diverse segments. From passenger cars to commercial vehicles, spanning light commercial pick-up trucks, vans, medium to heavy-duty trucks, and buses, the region is steadfastly embracing green mobility. Notably, the rising sales of fuel cell electric vehicles (FCEVs) in the passenger car segment highlight the region's leadership in adopting clean transportation. These sales saw a significant increase from 2017 to 2023, and the trend is projected to persist till 2030.

- In the commercial vehicle arena, both light and heavy-duty segments are poised for substantial growth, driven by a strategic emphasis on hydrogen fuel cell technology. Sales of light commercial pick-up trucks and vans have witnessed a remarkable surge, signaling a shift toward zero-emission vehicles tailored for the logistics and transportation sectors. This transition is bolstered by investments in hydrogen infrastructure and government incentives aimed at curbing carbon emissions.

- Medium and heavy-duty commercial trucks, alongside FCEV-powered buses, are also on a rapid growth trajectory, with sales volumes set to soar by 2030. The optimism surrounding FCEVs in the Asia-Pacific region underscores a significant move toward a hydrogen-based economy, setting a global precedent for clean energy adoption. Government initiatives, technological advancements, and the declining cost of green hydrogen production are pivotal factors in this transition, rendering FCEVs increasingly attractive for both commercial and passenger transportation.

The Asia-Pacific fuel cell vehicles market is gaining momentum, with specific countries leading the charge toward hydrogen fuel technology adoption

- These initiatives taken by governments across the world to adopt green energy mobility in order to curtail and curb transportation pollution are among the key factors that are projected to drive the fuel cell commercial vehicle market in the near future. In November 2019, the government-backed Chinese business, Beiqi Foton Motor, a truck and bus manufacturer, announced that it would invest USD 2.6 billion in alternative energy vehicles, including fuel cell engines. The company plans to deploy 200,000 new energy commercial vehicles by 2025.

- Several major OEM players are investing heavily in research and development, and they are entering strategic partnerships to enhance their technologies for commercial vehicles. In January 2020, Japan's Honda Motor and Isuzu Motors announced that they would jointly conduct research on the use of hydrogen fuel cells to power heavy-duty trucks, looking forward to expanding fuel-cell usage by applying zero-emission technology to larger vehicles. Such developments are expected to enhance the electric commercial vehicles market across Asia-Pacific.

- In 2020, South Korea extended the purchase subsidy for electric vehicles for passenger cars until 2024, and for buses and trucks, it was extended until 2025. The bonus is tied to a price cap. EVs priced below KRW 60 million are eligible for full subsidies, but vehicles priced between KRW 60 million and 90 million may receive only 50% of the full amount. Previously, up to KRW 8 million in subsidies were available per vehicle.

Asia-Pacific Fuel Cell Vehicles Market Trends

Asia-Pacific's auto loan interest rates reflected varying national economic strategies, with some countries emphasizing stimulation while others took a more conservative stance

- Over the past few years, there have been noticeable changes in these figures. Indonesia and India notably reduced their auto loan rates, signaling potential efforts to bolster the automotive sector in the face of fluctuating sales. Japan, adhering to its legacy, sustained its nominal rates, an indicator of its persistent ultra-loose monetary policy. Malaysia, after a sharp dip in 2021, seemed to regain its footing in 2022, hinting at an adaptive economic recalibration. New Zealand and the Philippines, meanwhile, navigated a descending path. Thailand, with a plunge in 2020, retraced some steps upward by 2022. Australia's journey was intriguing, with a steady climb each year, possibly indicating a blend of economic resilience and strategic divergence from its regional peers.

- During 2017-2023 period, Asia-Pacific showcased a panorama of fluctuating interest rates for auto loans. Indonesia stood out with the steepest rates oscillating between 10% and11%, clearly underlining its economic landscape. In stark contrast, Japan's rates remained consistently below 1%, reflecting its long-standing policy of low-interest rates to boost economic activity. Australia and New Zealand moved along a more stable trend with a slight increase by 2019. Meanwhile, the Philippines, though starting from a moderate base in 2017, marked a dramatic ascent, peaking over 7% in 2019. India maintained a steady rhythm, keeping within the 9-10% bracket, while Malaysia's course was slightly upward. Conversely, Thailand embraced a gentle downward slope.

The surging demand for electric vehicles (EVs) in Asia is prompting global automakers to introduce new offerings, thereby expanding the EV and battery pack market

- In response to the escalating demand for electric vehicles (EVs) in the Asia-Pacific region, numerous automakers are aligning their strategies to unveil innovative products tailored to this burgeoning market. One important instance is the announcement made by Skoda in January 2023, where it shared plans to introduce a cutting-edge electric SUV in India. This vehicle stands out due to its formidable 82-kWh battery, boasting an impressive range exceeding 500 kilometers on a singular charge. With its launch slated for late 2023, Skoda's move is emblematic of the broader trend sweeping across the region. Such introductions are poised to not only fuel the EV demand but also drive the proliferation of battery packs in various Asia-Pacific countries.

- As public transportation becomes increasingly integral to urban life in the Asia-Pacific, it is inspiring a new generation of manufacturers to debut novel, eco-friendly models. In a significant move in April 2022, the pioneering India-based startup, GreenCell Mobility, unveiled its electric mobility bus service brand, NueGo. GreenCell has plans to revolutionize intercity commutes by deploying 750 premium electric buses across three key regions in India, encompassing the South, North, and West. While the initial phase will witness the rollout of 250 buses across 24 cities, the long-term vision underscores the company's commitment to enhancing green public transportation. Such initiatives signal a promising surge in electric public transit solutions, setting the pace for broader adoption across Asia-Pacific in the coming years.

Asia-Pacific Fuel Cell Vehicles Industry Overview

The Asia-Pacific Fuel Cell Vehicles Market is moderately consolidated, with the top five companies occupying 60%. The major players in this market are Daimler AG (Mercedes-Benz AG), Honda Motor Co. Ltd., Hyundai Motor Company, Nissan Motor Co. Ltd. and Toyota Motor Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.2 GDP Per Capita

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.4 Inflation

- 4.5 Interest Rate For Auto Loans

- 4.6 Shared Rides

- 4.7 Impact Of Electrification

- 4.8 EV Charging Station

- 4.9 Battery Pack Price

- 4.10 New Xev Models Announced

- 4.11 Logistics Performance Index

- 4.12 Used Car Sales

- 4.13 Fuel Price

- 4.14 Oem-wise Production Statistics

- 4.15 Regulatory Framework

- 4.16 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Type

- 5.1.1 Commercial Vehicles

- 5.1.1.1 Buses

- 5.1.1.2 Heavy-duty Commercial Trucks

- 5.1.1.3 Light Commercial Pick-up Trucks

- 5.1.1.4 Light Commercial Vans

- 5.1.1.5 Medium-duty Commercial Trucks

- 5.1.1 Commercial Vehicles

- 5.2 Country

- 5.2.1 Australia

- 5.2.2 China

- 5.2.3 India

- 5.2.4 Indonesia

- 5.2.5 Japan

- 5.2.6 Malaysia

- 5.2.7 South Korea

- 5.2.8 Thailand

- 5.2.9 Rest-of-APAC

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Ballard Power Systems

- 6.4.2 Daihatsu Motor Co. Ltd.

- 6.4.3 Daimler AG (Mercedes-Benz AG)

- 6.4.4 Dongfeng Motor Corporation

- 6.4.5 Honda Motor Co. Ltd.

- 6.4.6 Hyundai Motor Company

- 6.4.7 Mazda Motor Corporation

- 6.4.8 Nissan Motor Co. Ltd.

- 6.4.9 Toyota Motor Corporation

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

燃料電池商用車市場:按技術、功率輸出、組件類型、車輛類型和應用分類,全球預測(2026-2032)

燃料電池商用車市場:按技術、功率輸出、組件類型、車輛類型和應用分類,全球預測(2026-2032) 全球燃料電池電動車市場:機會與策略展望(至2034年)

全球燃料電池電動車市場:機會與策略展望(至2034年) 燃料電池汽車全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

燃料電池汽車全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 燃料電池電動車市場機會、成長要素、產業趨勢分析及2026年至2035年預測

燃料電池電動車市場機會、成長要素、產業趨勢分析及2026年至2035年預測 燃料電池商用車市場-全球產業規模、佔有率、趨勢、機會及預測,依車輛類型(卡車、巴士)、功率範圍(低於100千瓦、100千瓦至200千瓦、高於200千瓦)、地區及競爭格局分類,2021-2031年預測

燃料電池商用車市場-全球產業規模、佔有率、趨勢、機會及預測,依車輛類型(卡車、巴士)、功率範圍(低於100千瓦、100千瓦至200千瓦、高於200千瓦)、地區及競爭格局分類,2021-2031年預測 燃料電池電動車市場:依車輛類型、燃料電池類型、功率輸出、續航里程和地區劃分 - 全球市場分析(2025-2035)

燃料電池電動車市場:依車輛類型、燃料電池類型、功率輸出、續航里程和地區劃分 - 全球市場分析(2025-2035) 燃料電池電動車市場預測至2032年:全球分析(按組件、燃料電池類型、功率輸出、車輛類型、續航里程、應用和地區分類)燃料電池電動車(FCEV)動力系統市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)汽車氫燃料電池堆市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

燃料電池電動車市場預測至2032年:全球分析(按組件、燃料電池類型、功率輸出、車輛類型、續航里程、應用和地區分類)燃料電池電動車(FCEV)動力系統市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)汽車氫燃料電池堆市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年) 商用車氫燃料電池引擎:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)

商用車氫燃料電池引擎:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)

▼