|

市場調查報告書

商品編碼

1693636

歐洲輕型商用車電氣化:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)Europe Electric Light Commercial Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

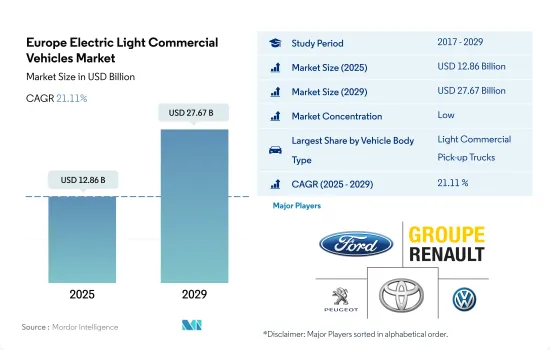

預計 2025 年歐洲輕型商用車市場規模將達到 128.6 億美元,預計到 2029 年將達到 276.7 億美元,預測期內(2025-2029 年)的複合年成長率為 21.11%。

歐洲在推動輕型商用車電氣化方面發揮先鋒作用,其配置可滿足各種業務需求。

- 以貨車和廂型車為特徵的歐洲輕型商用車 (ELCV) 市場正在經歷重大變革時期,這得益於向永續性和電氣化的轉變。特別是在貨車領域,各大汽車製造商正在推出電動車,以滿足日益成長的零排放汽車需求。例如,日產推出新款 Townstar 貨車,這是取代 e-NV200 的戰略舉措,提供全電動選擇,旨在加速向零排放汽車的過渡。

- 歐洲市場動態受到多種因素的影響,包括技術進步、法律規範以及電子商務的成長,這些都推動了對高效最後一哩交付解決方案的需求。然而,市場面臨的挑戰包括商用車註冊量整體下降和貨車銷售下降,部分原因是疫情對經濟的影響以及旨在減少排放的監管環境的變化。

- 隨著人們越來越關注減少溫室氣體排放和改善都市區空氣質量,歐洲 ELCV 市場提供了多種機會。大眾汽車計劃在 2030 年之前在歐洲建立六家電池工廠等措施凸顯了該行業對擴大電動車生態系統的承諾。此外,該領域的合作與創新,例如邦奇動力傳動系統與 Gruau 達成的開發永續ELCV 的協議,預示著未來電動貨車和卡車將在商業運輸中發揮核心作用。

歐洲輕型商用車市場新興國家的發展反映了歐洲大陸在電氣化進程中的領導地位。

- 全球整體商用車銷量達1770萬輛。歐洲新註冊的廂型車、卡車和巴士超過 290 萬輛,佔全球總量的 16.4%。由於人們對環境問題的日益關注、政府計劃在 2030 年前禁止使用內燃機以及人們普遍認知到燃油效率和零排放等環保汽車的好處,消費者的購買習慣正在轉向電動車。

- 新冠疫情對文化和經濟產生了前所未有的影響。汽車產業也受到較大影響,復甦可能仍需時日;未來還面臨許多挑戰。儘管如此,義大利政府仍預測自 2025 年起電動車的普及率將大幅增加。此外,2019年12月,歐盟委員會核准七個成員國提供32億歐元公共資金,用於泛歐研究和創新計劃。它將促進鋰離子電池高度創新和永續的技術發展,包括整個電池價值鏈直至首次工業部署的研發活動。

- 政府優先發展電池、汽車、充電站、數位行動應用程式、資訊通訊技術、智慧運輸和能源服務,以加速未來幾年電動車的普及。由於電子商務和物流活動的成長,對電動商用車的需求預計會增加。

歐洲輕型商用車市場趨勢

環境問題、政府支持和脫碳目標刺激了歐洲電動車的需求和銷售

- 過去幾年,歐洲國家對電動車的需求和銷售量大幅成長。德國 2022 年電動車銷量與 2021 年相比成長了 22%,其次是英國,2022 年電動車銷量與 2021 年相比成長了 18.40%。日益成長的環境問題、嚴格的政府規範、電動車的優勢(例如更好的燃油經濟性、更低的服務成本、更少的碳排放)以及政府補貼是推動歐洲國家電動車成長的一些因素。

- 歐洲國家對電動商用車,特別是輕型卡車的需求逐漸增加。此外,世界各國政府也支持電動車的普及。 2021年11月,英國政府宣布承諾在2040年實現所有重型車輛零排放。這些因素將使2022年英國電動商用車銷量較2021年成長23.17%,各國類似做法將提振整個歐洲對電動商用車的需求。

- 預計未來幾年歐洲國家的汽車電氣化將呈指數級成長。預計政府在脫碳方面的努力將推動歐洲電動商用車市場的發展。例如,2022年1月,德國交通部長宣布了2030年道路上電動車保有量達到1,500萬輛的目標。受這些因素影響,預計2024年至2030年間歐洲國家的電動車銷量將會成長。

歐洲輕型商用車產業概況

歐洲輕型商用車市場較為分散,前五大企業佔32.16%。市場的主要企業是:福特汽車公司、雷諾集團、標緻汽車公司、豐田汽車公司和大眾汽車公司(按字母順序排列)

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 人口

- 人均GDP

- 消費者汽車支出(cvp)

- 通貨膨脹率

- 汽車貸款利率

- 電氣化的影響

- 電動車充電站

- 電池組價格

- 新款 Xev 車型發布

- 物流績效指數

- 燃油價格

- OEM生產統計

- 法律規範

- 價值鍊和通路分析

第5章市場區隔

- 車輛配置

- 輕型商用車

- 燃料類別

- BEV

- FCEV

- HEV

- PHEV

- 國家

- 奧地利

- 比利時

- 捷克共和國

- 丹麥

- 愛沙尼亞

- 法國

- 德國

- 愛爾蘭

- 義大利

- 拉脫維亞

- 立陶宛

- 挪威

- 波蘭

- 俄羅斯

- 西班牙

- 瑞典

- 英國

- 其他歐洲國家

第6章 競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- ADDAX MOTORS NV.

- ARRIVAL LTD.

- Daimler AG(Mercedes-Benz AG)

- Fiat Chrysler Automobiles NV

- Ford Motor Company

- Groupe Renault

- Maxus

- Nissan Motor Co. Ltd.

- Peugeot SA

- Toyota Motor Corporation

- Volkswagen AG

- Volvo Group

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 數據包

- 詞彙表

簡介目錄

Product Code: 93024

The Europe Electric Light Commercial Vehicles Market size is estimated at 12.86 billion USD in 2025, and is expected to reach 27.67 billion USD by 2029, growing at a CAGR of 21.11% during the forecast period (2025-2029).

Europe has a pioneering role in driving the adoption of electric light commercial vehicles with configurations suited to various business needs

- The European electric light commercial vehicles (ELCVs) market, characterized by cargo trucks and vans, is undergoing significant transformations driven by a shift toward sustainability and electrification. The van segment, in particular, has seen notable activity, with major automotive players introducing electric variants to cater to the rising demand for zero-emission vehicles. For example, Nissan's introduction of the all-new Townstar van represents a strategic move to replace the e-NV200, offering a fully electric option designed to accelerate the transition to zero-emission motoring.

- The European market's dynamics are influenced by various factors, including technological advancements, regulatory frameworks, and the growth of e-commerce, which has increased the demand for efficient last-mile delivery solutions. However, the market has faced challenges, such as the overall decline in commercial vehicle registrations and the specific downturn in van sales, attributed partly to the economic impact of the pandemic and the changing regulatory landscape aimed at reducing emissions.

- The ELCV market in Europe presents several opportunities, underpinned by the growing emphasis on reducing greenhouse gas emissions and improving urban air quality. Initiatives like Volkswagen's plan to set up six battery factories across Europe by 2030 underscore the industry's commitment to expanding the electric vehicle ecosystem. Additionally, collaborations and innovations in the sector, such as Punch Powertrain's agreement with Gruau to develop sustainable ELCVs, signal a future where electric vans and trucks play a central role in commercial transportation.

Country-specific developments in the European electric light commercial vehicles market are showcasing the continent's leadership in electrification efforts

- Globally, sales of commercial vehicles reached a total of 17.7 million each year. With more than 2.9 million new vans, trucks, and buses, Europe accounts for 16.4% of global registrations. Consumer purchasing habits have shifted in favor of electric vehicles due to increasing environmental concerns, the government's plan to ban internal combustion engines by 2030, and a general understanding of the benefits of eco-friendly vehicles, such as fuel efficiency and zero emissions.

- The COVID-19 pandemic has had unparalleled repercussions on culture and the economy. The automobile industry has experienced significant effects, and the recovery process is still expected to be drawn out and challenging. Despite this, the Italian government continues to predict that starting in 2025, the use of electric vehicles will significantly expand. Additionally, the European Commission approved public financing of EUR 3.2 billion in December 2019 from seven Member States for pan-European research and innovation projects. This promotes the development of highly innovative and sustainable technologies for lithium-ion batteries, involving R&I activities up to the first industrial deployment along the entire battery value chain.

- The government has prioritized the development of batteries, vehicles, charging stations, digital mobility apps, ICT, smart mobility, and energy services to accelerate the adoption of electric vehicles in the coming years. The demand for electric commercial vehicles is anticipated to increase due to the growth of e-commerce and logistical activities.

Europe Electric Light Commercial Vehicles Market Trends

Environmental concerns, government support, and decarbonization goals fuel European electric vehicle demand and sales

- The demand and sales of electric vehicles in European countries have grown significantly over the past few years. Germany witnessed a growth in the sales of electric cars by 22% in 2022 over 2021, followed by the United Kingdom with an 18.40% increase in 2022 over 2021. Growing environmental concerns, stringent governmental norms, advantages of electric vehicles such as fuel efficiency, low service cost, no carbon emissions, and subsidies by the government are some of the factors contributing to the growth of electric vehicles in European countries.

- The demand for electric commercial vehicles, especially light trucks, is growing gradually in European countries. Moreover, the governments of various countries are also supporting the adoption of electric vehicles. In November 2021, the government of the United Kingdom announced a pledge that all heavy-duty vehicles would be zero-emission by the year 2040. Such factors have increased the sales of electric commercial vehicles in the United Kingdom by 23.17% in 2022 over 2021, and similar practices in various countries are enhancing the demand for electric commercial vehicles across Europe.

- It is projected that the electrification of vehicles in European countries is expected to grow tremendously in the next few years. The efforts of the governments in the regions for decarbonization are expected to drive the electric commercial vehicle market in Europe. For instance, in January 2022, the transport minister of Germany announced a goal to put 15 million electric vehicles on the road by 2030. Such factors are expected to increase the sales of electric vehicles during the 2024-2030 period in European countries.

Europe Electric Light Commercial Vehicles Industry Overview

The Europe Electric Light Commercial Vehicles Market is fragmented, with the top five companies occupying 32.16%. The major players in this market are Ford Motor Company, Groupe Renault, Peugeot S.A., Toyota Motor Corporation and Volkswagen AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.2 GDP Per Capita

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.4 Inflation

- 4.5 Interest Rate For Auto Loans

- 4.6 Impact Of Electrification

- 4.7 EV Charging Station

- 4.8 Battery Pack Price

- 4.9 New Xev Models Announced

- 4.10 Logistics Performance Index

- 4.11 Fuel Price

- 4.12 Oem-wise Production Statistics

- 4.13 Regulatory Framework

- 4.14 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Configuration

- 5.1.1 Light Commercial Vehicles

- 5.2 Fuel Category

- 5.2.1 BEV

- 5.2.2 FCEV

- 5.2.3 HEV

- 5.2.4 PHEV

- 5.3 Country

- 5.3.1 Austria

- 5.3.2 Belgium

- 5.3.3 Czech Republic

- 5.3.4 Denmark

- 5.3.5 Estonia

- 5.3.6 France

- 5.3.7 Germany

- 5.3.8 Ireland

- 5.3.9 Italy

- 5.3.10 Latvia

- 5.3.11 Lithuania

- 5.3.12 Norway

- 5.3.13 Poland

- 5.3.14 Russia

- 5.3.15 Spain

- 5.3.16 Sweden

- 5.3.17 UK

- 5.3.18 Rest-of-Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 ADDAX MOTORS NV.

- 6.4.2 ARRIVAL LTD.

- 6.4.3 Daimler AG (Mercedes-Benz AG)

- 6.4.4 Fiat Chrysler Automobiles N.V

- 6.4.5 Ford Motor Company

- 6.4.6 Groupe Renault

- 6.4.7 Maxus

- 6.4.8 Nissan Motor Co. Ltd.

- 6.4.9 Peugeot S.A.

- 6.4.10 Toyota Motor Corporation

- 6.4.11 Volkswagen AG

- 6.4.12 Volvo Group

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

2026-2030年全球電動商用車(ECV)市場

2026-2030年全球電動商用車(ECV)市場 2026年全球中重型商用電動車市場報告2026年全球商用電動車市場報告

2026年全球中重型商用電動車市場報告2026年全球商用電動車市場報告 電動商用車市場:2026-2032年全球市場預測(按車輛類型、充電基礎設施、推進系統、驅動系統、車速、應用和最終用途產業分類)

電動商用車市場:2026-2032年全球市場預測(按車輛類型、充電基礎設施、推進系統、驅動系統、車速、應用和最終用途產業分類) 全球電動商用車MRO市場規模、佔有率、趨勢與成長分析報告(2026-2034年)

全球電動商用車MRO市場規模、佔有率、趨勢與成長分析報告(2026-2034年) 2026 年至 2035 年電動商用車的市場機會、成長要素、產業趨勢分析與預測。電動商用車市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年全球工業電動車市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球電動商用車市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

2026 年至 2035 年電動商用車的市場機會、成長要素、產業趨勢分析與預測。電動商用車市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年全球工業電動車市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球電動商用車市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 電動商用車市場-全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、動力系統、續航里程、地區及競爭格局分類,2021-2031年)

電動商用車市場-全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、動力系統、續航里程、地區及競爭格局分類,2021-2031年)

▼