|

市場調查報告書

商品編碼

1690173

日本第三方物流(3PL)-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Japan Third-Party Logistics (3PL) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

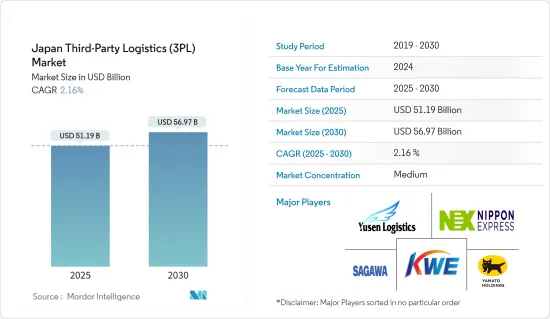

日本第三方物流市場規模預計在2025年為511.9億美元,預計到2030年將達到569.7億美元,預測期內(2025-2030年)的複合年成長率為2.16%。

主要亮點

- 新冠疫情對運輸、儲存和運輸貨物的物流公司產生了直接影響。物流公司幫助企業開展業務並將產品運送給客戶。物流公司幫助企業開展業務並將產品運送給客戶。物流公司是國內外價值鏈的重要組成部分。因此,疫情造成的供應鏈中斷可能會影響該產業的競爭力、經濟擴張和就業機會。

- 日本在供應鏈領域取得了巨大進展。例如,我們擁抱數位技術,改造傳統產業。近年來,影響物流的社會經濟因素發生了重大變化。這些因素包括人口減少和老化、某些領域的新想法、小件物品運送更頻繁以及不同的客戶需求。在日本,隨著大公司將注意力轉向自己的物流網路如何運作,並將更多的業務委託給第三方物流公司以降低成本並提高效率,對第三方物流服務的需求正在上升。

- 第三方物流公司營運供應鏈,向各行各業和消費者運送材料和貨物。日本是東亞最大的經濟體之一,其製造業嚴重依賴第三方物流。因此,像 Yamato Holdings 這樣的組織已經成為世界領先的物流供應商之一。群島的 1.2 億人口處理了 47.1 億噸國內貨物,而對外貿易增加了 9 億噸。

- 自2000年以來,日本對大型現代化物流設施的租賃需求大幅增加。物流業務外包、企業房地產不平衡以及騰空一些舊倉庫都導致了這種成長。日本的貨運及物流業佔該國GDP的比重很大,佔比超過5%。

- 物流業以激烈的成本競爭而聞名。為了擊敗競爭對手,需要高水準的合作和規模經濟。物流公司開始利用第三方物流(通常稱為 3PL)來簡化業務。自動化和人工智慧(AI)是成本控制的進一步工具。

透過採用更多此類技術解決方案,物流系統產業有望實現成長。雖然如今自動化倉庫正在使用,但我們可能還需要一段時間才能在道路上看到全自動卡車。對日本來說,自動化的進步還不夠快。物流業正面臨人手不足的問題,此外,司機老化速度加快,引發了人們對其能否以公平價格提供服務的擔憂。該計劃的兩個目標是提高卡車運輸行業的生產力並創造一個吸引和留住老年司機和女性司機的職場環境。在自動化變得更加普及之前,這種策略是否足以穩定市場還有待觀察。

日本第三方物流(3PL)市場的趨勢

汽車和製造業的成長正在推動市場

日本一直是世界機械製造和汽車工業的領導者之一。據經濟產業省稱,高科技製造業是日本最重要的成長領域之一。日本製造業的核心產業包括家電、汽車製造、半導體製造、光纖、光電子、光學媒體、鋼鐵和影印機。

日本長期以來一直是世界主要汽車出口國之一。它以高品質的製造和高效的物流服務而聞名。其出口強國地位得益於高度發展的基礎設施和港口網路以及高度集中的航運航線。

日本汽車業的一些主要公司都有自己的物流部門。 Vantec 是日本領先的汽車物流供應商,隸屬於 HTS 集團。 Vantec集團支援汽車零件的順序供應,完美滿足汽車製造商複雜的物流要求。

日野汽車對未來移動社會的願景可以用「SPACE」這個字來表達。 「共享(共用移動、空間和時間)」、「平台(自由回應各種服務)」、「自主(擺脫駕駛)」、「互聯(將移動與人、物和城市連接起來)」和「電動化(提高效率和靈活性)」。

低溫運輸物流發展

日本是繼美國之後全球成長第二快的成熟醫藥市場。國際社會對日本醫藥市場的興趣可能會為低溫運輸物流服務提供者創造機會。國內公司正在透過與競爭對手以及為第三方物流公司提供平台服務的公司達成交易、建立合作夥伴關係和簽訂合約來積極改進和更新其服務。

低溫運輸市場也因其所需的大量能源和在運輸過程中產生的巨大排放而聞名。這些公司正在建立物流中心,並將其車輛改裝成環保車輛,以最大程度地排放氣體並使用永續能源來源。

2022年2月20日,日本政府和聯合國兒童基金會(UNICEF)向衛生署和SAMES捐贈了三輛冷藏車。在帝力的 SAMES 設施,日本駐東帝汶大使 Masami Kinefti 和聯合國兒童基金會副代表 Ainhoa 層級將車輛交給衛生部副部長 Bonifacio Maucori dos Reis。

此外,目前,艾納羅、包考、博博納羅和奧庫西特別行政區的所有區域倉庫均已配備並正在安裝步入式冷藏室。擁有配備所有部件的冷藏車、步入式冷藏室和冷凍非常重要,這樣才能安全、快速地將疫苗運送到城鎮和醫療機構。

日本第三方物流(3PL)產業概況

市場相當小,最大的參與者是 Yusen 物流、Expeditors、DHL、Hitachi Transport System 和 Kuhne Nagel。自行處理物流的零售商和製造商也在市場中發揮重要作用。

日本的電子商務市場正以前所未有的速度成長。這體現在日本附加價值服務的快速成長。因此,日本物流業的包裝、標籤和分類工作量激增。

為解決國內需求旺盛和勞動力短缺的問題,可以採取聯合配送或共用配送等措施,即將多家公司的貨物運送到一個通用的配送點;使用平台應用程式幫助快遞公司找到有空位的司機和托運人;利用都市區的小型倉庫作為中間配送中心;以及收集物流。

物流行業變革的目標,例如使用自動化機器和車輛,是為了消除該行業對整體經濟的碳排放。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查結果

- 調查前提

- 研究範圍

第2章調查方法

- 分析方法

- 研究階段

第3章執行摘要

第4章 市場動態與洞察

- 當前市場狀況

- 市場動態

- 驅動程式

- 限制因素

- 機會

- 價值鏈/供應鏈分析

- 行業法規與政策

- 倉儲市場的整體趨勢

- CEP、最後一哩配送和低溫運輸物流等其他領域的需求

- 電子商務業務洞察

- 技術趨勢和自動化

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

- COVID-19對市場的影響

第5章市場區隔

- 按服務

- 國內運輸管理

- 國際運輸管理

- 加值倉儲物流

- 按最終用戶

- 製造/汽車

- 石油、天然氣和化工

- 分銷業(批發和零售,包括電子商務)

- 製藥和醫療保健

- 建造

- 其他最終用戶

第6章 競爭格局

- 公司簡介

- Nippon Express

- Yamato Holdings

- Kintetsu World Express

- Sagawa Express

- Hitachi Transport System

- Nichirei Logistics

- Sankyu

- Kokusai Express

- Fukuyama

- Mitsui-Soko

- Alps Logistics

- Yusen Logistics

- DHL*

第7章:市場的未來

第 8 章 附錄

- 宏觀經濟指標(GDP分佈、按活動分類、運輸和倉儲業對經濟的貢獻)

- 對外貿易統計 - 出口和進口(按產品)

- 深入了解主要出口和進口國家/地區目的地

The Japan Third-Party Logistics Market size is estimated at USD 51.19 billion in 2025, and is expected to reach USD 56.97 billion by 2030, at a CAGR of 2.16% during the forecast period (2025-2030).

Key Highlights

- The COVID-19 epidemic had a direct effect on logistics companies, which move, store, and move goods.Logistics companies help businesses do business and get their products to customers. They became an important part of value chains both inside and outside of national borders. Hence, supply chain interruptions brought on by the pandemic could affect the sector's competitiveness, economic expansion, and job creation.

- Japan has made a lot of progress in the supply chain space over time. For example, it has embraced digital technologies to change a traditional industry. In the last few years, the social and economic factors that affect logistics have changed a lot. These factors include a shrinking or aging population, new ideas in some areas, more frequent deliveries of smaller goods, and different customer needs. In Japan, there is more demand for 3PL as large companies look at how their logistics networks work and outsource more tasks to 3PL providers to cut costs and improve efficiency.

- 3PL logistics firms are the ones who run supply chains and get materials and goods to all industries and consumers. Japan, one of the biggest economies in East Asia, relies on 3PL logistics a lot because of its manufacturing industry. As a result, organizations like Yamato Holdings are among the top logistics providers globally. 120 million people in the archipelago handled 4.71 billion tons of domestic freight, and foreign trade added 900 million tons more.

- Since 2000, there has been a big rise in the need for large, modern logistics leasing facilities in Japan. Outsourcing logistics operations, imbalances in corporate real estate, and moving out of multiple old warehouses all contributed to the rise. The freight and logistics industry in Japan is a big part of the economy, making up more than 5% of the GDP.

- The logistics business is known for its fierce cost competitiveness. To outbid rivals, sophisticated coordination and economies of scale are required. Through the use of "third-party logistics," sometimes known as "3PL," logistics firms have begun to streamline their operations. Automation and artificial intelligence (AI) are further tools for cost control.

It's likely that the logistics systems industry will grow to include more of these technical solutions. Although automated warehouses are now in use, it will be some time before fully autonomous trucks are allowed on the roads. Automation advancements cannot arrive soon enough for Japan. Its logistics sector is experiencing a manpower deficit, and on top of that, drivers are aging quickly, endangering the availability of services at fair prices. Two goals of this effort are to increase productivity in the trucking sector and to foster work environments that attract and retain older and female drivers. It has to be seen whether this tactic stabilizes the market effectively enough until automation advances further.

Japan Third-Party Logistics (3PL) Market Trends

Growth in automotive and manufacturing sector driving the market

Japan has always been and is one of the global leaders in the manufacturing machinery and automobile industries. The Ministry of Economy, Trade, and Industry (METI) says that high-tech manufacturing is one of Japan's most important growth sectors. The core areas in Japan's manufacturing sector are consumer electronics, automobile manufacturing, semiconductor manufacturing, optical fibers, optoelectronics, optical media, steel and iron, and copy machines.

Since a long time ago, Japan has been one of the top exporters of cars in the world. It is known for its high-quality manufacturing and efficient logistics services. Its highly developed infrastructure and port network support its status as an exporting giant, as do its dense concentration of shipping lines.

Some of the major players in the automotive industry in Japan also have in-house logistics arms. Vantec, a leading automotive logistics provider in Japan, operates under the HTS Group. The Vantec Group supports the sequential supply of auto parts in full alignment with the complex logistics requirements of automotive manufacturers.

As per Hino Motors, the future mobility society to be considered is represented by the word "SPACE". "Shared (sharing of movement, space, and time)" "Platform (corresponding to various services freely) and "Autonomous (free from driving)" "Connected (connecting mobility with people, things, and cities)" "Electricity" (increase efficiency and flexibility).

Development in cold chain logistics

Japan is the second-fastest-growing mature pharmaceutical market in the world, following the United States. The international interest in the Japanese pharmaceutical market will create opportunities for cold chain logistics service providers. The companies in the country are heavily improving and updating their services through deals, partnerships, and agreements with competitors and companies that provide platform services to the 3PL companies.

The cold chain market is also known for the amount of energy required in the process and the huge amount of emissions that occur. The companies are setting up logistics centers and transforming vehicles into ones that are environment-friendly, produce minimum emissions, and run on sustainable sources of energy.

The Government of Japan and the United Nations Children's Fund (UNICEF) gave three refrigerated vans to the Ministry of Health and SAMES on February 20, 2022. These vans will be used to move vaccines.At the SAMES compound in Dili, Masami Kinefuchi, the Japanese ambassador to Timor-Leste, and Ainhoa Jaureguibeitia, the deputy UNICEF representative, gave the vehicles to Sr. Bonifacio Maucoli dos Reis, the vice minister of health.

Moreover, walk-in cool rooms have been provided and are currently being installed at all regional warehouses in the municipalities of Ainaro, Baucau, Bobonaro, and the Special Administrative Area of Oecusse. It is important to have refrigerated vans, walk-in coolers, and freezer rooms with all of their parts so that vaccines can be kept safely and quickly sent to towns and medical facilities.

Japan Third-Party Logistics (3PL) Industry Overview

The market is pretty small, and its biggest players are Yusen Logistics, Expeditors, DHL, Hitachi Transport System, and Kuehne Nagel. Retail and manufacturing companies that handle their own logistics also play a big role in the market.

Japan's e-commerce market is growing at a rate that has never been seen before. This is reflected in the rapid growth of value-added services in Japan.As a result, packaging, labeling, and sorting activities have seen a large spike in the Japanese logistics industry.

To deal with the high demand and lack of workers in the country, steps can be taken like joint or shared delivery, which sends goods from multiple companies to common delivery points, platform apps, which help delivery companies find drivers with empty truck space and shippers, the use of small warehouses in cities as intermediate distribution centers, and collection logistics.

The goal of the changes in the logistics industry, like the use of self-driving machines and vehicles, is to get rid of the sector's carbon footprint on the economy as a whole.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.2 Restraints

- 4.2.3 Opportunities

- 4.3 Value Chain / Supply Chain Analysis

- 4.4 Industry Policies and Regulations

- 4.5 General Trends in Warehousing Market

- 4.6 Demand From Other Segments, such as CEP, Last Mile Delivery, Cold Chain Logistics Etc.

- 4.7 Insights on Ecommerce Business

- 4.8 Technological Trends and Automation

- 4.9 Industry Attractiveness - Porter's Five Forces Analysis

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Buyers/Consumers

- 4.9.3 Bargaining Power of Suppliers

- 4.9.4 Threat of Substitute Products

- 4.9.5 Intensity of Competitive Rivalry

- 4.10 Impact of COVID--19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Service

- 5.1.1 Domestic Transportation Management

- 5.1.2 International Transportation Management

- 5.1.3 Value-added Warehousing and Distribution

- 5.2 By End-User

- 5.2.1 Manufacturing & Automotive

- 5.2.2 Oil & Gas and Chemicals

- 5.2.3 Distributive Trade (Wholesale and Retail trade including e-commerce)

- 5.2.4 Pharma & Healthcare

- 5.2.5 Construction

- 5.2.6 Other End-Users

6 COMPETITIVE LANDSCAPE

- 6.1 Overview (market concentration and major players)

- 6.2 Company Profiles

- 6.2.1 Nippon Express

- 6.2.2 Yamato Holdings

- 6.2.3 Kintetsu World Express

- 6.2.4 Sagawa Express

- 6.2.5 Hitachi Transport System

- 6.2.6 Nichirei Logistics

- 6.2.7 Sankyu

- 6.2.8 Kokusai Express

- 6.2.9 Fukuyama

- 6.2.10 Mitsui-Soko

- 6.2.11 Alps Logistics

- 6.2.12 Yusen Logistics

- 6.2.13 DHL*

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 Macroeconomic Indicators (GDP Distribution, by Activity, Contribution of Transport and Storage Sector to economy)

- 8.2 External Trade Statistics - Exports and Imports, by Product

- 8.3 Insights into Key Export Destinations and Import Origin Countries

第三方化學品分銷市場(按產品類型、最終用途產業、分銷通路、實體形態和服務類型分類)-2025-2032年全球預測第三方物流市場:2025-2032 年全球預測(按服務類型、運輸方式、物流模型和產業)第三方物流市場:按運輸方式、類型、服務類型、技術解決方案、整合程度、客戶類型、經營模式和最終用戶產業 - 全球預測,2025-2032第三方物流軟體市場按應用類型、部署類型、組織規模、最終用戶產業和服務類型分類-2025-2032年全球預測

第三方化學品分銷市場(按產品類型、最終用途產業、分銷通路、實體形態和服務類型分類)-2025-2032年全球預測第三方物流市場:2025-2032 年全球預測(按服務類型、運輸方式、物流模型和產業)第三方物流市場:按運輸方式、類型、服務類型、技術解決方案、整合程度、客戶類型、經營模式和最終用戶產業 - 全球預測,2025-2032第三方物流軟體市場按應用類型、部署類型、組織規模、最終用戶產業和服務類型分類-2025-2032年全球預測 2025年第三方物流(3PL)全球市場報告

2025年第三方物流(3PL)全球市場報告 第三方物流(3PL) 市場 - 2025 年至 2030 年預測

第三方物流(3PL) 市場 - 2025 年至 2030 年預測 全球汽車第三者物流市場第三方物流(3PL)全球市場機會與策略(至2034年)

全球汽車第三者物流市場第三方物流(3PL)全球市場機會與策略(至2034年) 第三方物流:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)全球第三方物流市場研究報告-產業分析、規模、佔有率、成長、趨勢及2025年至2033年預測

第三方物流:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)全球第三方物流市場研究報告-產業分析、規模、佔有率、成長、趨勢及2025年至2033年預測