|

市場調查報告書

商品編碼

1690135

合約包裝和履約服務:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)Contract Packaging and Fulfillment Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

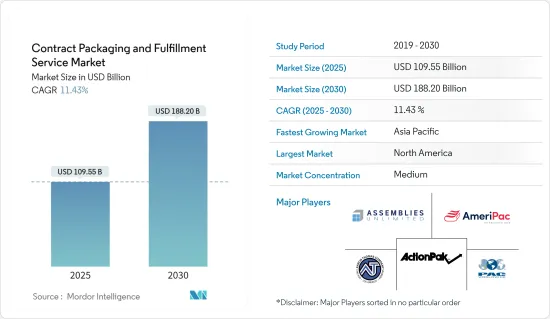

合約包裝和履約服務市場規模預計在 2025 年達到 1,095.5 億美元,預計到 2030 年將達到 1,882 億美元,預測期內(2025-2030 年)的複合年成長率為 11.43%。

新冠疫情進一步刺激了食品飲料和製藥業的需求成長。此外,全球電子商務產業的成長是預測期內推動研究市場成長的關鍵因素之一。

關鍵亮點

- 近年來,合約包裝和履約服務市場經歷了顯著成長。這是因為製造商更加重視成本最佳化以增強其核心競爭力,從而改變了合約包裝商的偏好。許多行業專家聲稱,由於機器維護和人事費用成本的減少,此類服務可以將營運成本降低 7-10%。

- 此外,許多政府都制定了有關藥品和食品標籤檢視和包裝的嚴格法律法規,這進一步擴大了包裝承包的範圍。例如,在有類似法律的美國,由於資金和其他監管障礙,企業更願意將製造和包裝外包。

- 即使在歐洲和北美等市場,提高品質的需求也迫使企業投資研究市場。在這些地區,合約包裝和履約服務供應商的角色正在從外部包裝的臨時設施轉變為能夠縮短交貨時間和減少批量生產的策略創新合作夥伴。

- 市場也觀察到協會和組織的出現,以提高所研究市場的知名度。歐洲聯合包裝協會和合約包裝協會就是例子。歐洲約有 1,000 家合約包裝供應商,其中 40-50% 是小型企業。

- 新冠疫情爆發後,由於封鎖和保持社交距離的規範,電子商務市場蓬勃發展,大多數消費者更喜歡透過線上管道購物,企業紛紛將端到端或獨立履約服務外包,以滿足日益成長的需求,因此合約包裝和履行服務市場呈現出巨大的成長。

合約包裝與履約服務市場趨勢

合約包裝預計將大幅成長

- 合約包裝服務在研究市場中佔有最大的市場佔有率,因為它包含裝瓶/填充、包裝、貼標籤、包裝等合約包裝服務所必需的各種操作。此外,合約包裝分為三類:初級包裝、二次包裝和三級包裝。

- 初級包裝是與產品直接接觸或包裹產品的第一層包裝,用於保存和保護產品免受外部污染、損壞或變質。

- 初級包裝列出了製造商可能無法獲得的「關鍵任務」功能,特別是當涉及到需要小批量生產或頻繁轉換的計劃時,這些項目通常超出了初級製造的經濟範圍,例如新產品或利基產品或季節性需求。

- 初級包裝通常包括泡殼包裝、泡殼包裝、紙板包裝、單位劑量包裝和收縮包裝。 Wasdell Packaging Group 等公司提供泡殼包裝、容器填充、帶狀包裝和小袋填充包裝等初級包裝服務。

- 食品飲料和個人護理等其他終端用戶行業對初級包裝的需求不斷增加,迫使公司增加最終產品的產量,因此必須透過外包包裝活動來縮短產品上市時間。預計這將在預測期內推動初級包裝合約市場的發展。

亞太地區將經歷最高成長

- 疫情刺激了電子商務的成長,包括中國賣家和歐洲買家之間的跨境線上銷售。根據CNBC報道,2020年中國跨境電商銷售額成長31.1%,倉儲成長80%。阿里巴巴等中國市場的主要參與者正在透過其速賣通平台和菜鳥物流部門擴大其跨境電子商務業務。預計這將促進該地區的履約和倉儲服務。

- 阿里巴巴的數據顯示,2020年最後三個月,跨境電商為菜鳥貢獻了17.4億美元的收益,與前一年同期比較增51%。期內,該公司國際貿易批發收益成長53%,達5.77億美元。這為市場供應商在亞洲市場擴展倉儲服務創造了更多機會。

- 在中國,代包裝服務也呈現成長趨勢,越來越多的供應商進入該行業。例如,總部位於中國的 Sofeast 為中國買家提供與當地供應商共同包裝的服務,使客戶能夠外包標籤和包裝服務,而無需知識產權、定價和分銷管道資訊。

- 此外,來自亞馬遜、eBay、flipkart 和 snapdeal 等各種線上市場的當日送達和餐飲訂單等趨勢正在幫助組織獲得專業知識。此外,亞馬遜和 Flipkart 正在透過開設履約中心擴大其在新興經濟體的影響力。例如,2020 年 7 月,亞馬遜印度宣布將透過開設 10 個新的履約中心 (FC) 和擴建 7 座現有建築來擴大其在印度的履約網路。由此,亞馬遜將把其營運網路擴展到印度 15 個州的 60 個履約中心,並將其儲存容量提高 20%,達到總合超過 3,200 萬立方英尺。這使得包裝、物流和運輸能夠更快地交付和成長。

合約包裝與履約服務業概覽

合約包裝和履約服務市場競爭激烈,國內和國際市場上都有多家參與企業。市場集中度適中,主要企業正在採取業務擴張等策略來保持競爭力並擴大影響力。市場的主要企業包括 Aaron Thomas Company、ActionPak Inc. 和 Assemblies Unlimited。

- 2021 年 3 月——ActionPak Inc. 宣布已在其位於新澤西州卡姆登的 175,000 平方英尺的新包裝工廠完成了 196kW 屋頂太陽能安裝。 491塊太陽能板將抵消新建築20%的電力消耗。

- 2020 年 5 月-夏普 (UDG Healthcare PLC) 宣布已從 Quality Packaging Specialists International LLC (QPSI) 收購了一家醫藥包裝工廠。該設施佔地 160,000 平方英尺,並已獲得全面監管部門的批准。該工廠擁有 12 個初級生產套件和多條二級包裝線,並將提供初級和二級藥品包裝,包括裝瓶、泡殼、管瓶貼標和醫療設備配套,以及序列化服務。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業價值鏈分析

- 產業吸引力——波特分析

- 供應商的議價能力

- 新進入者的威脅

- 購買者和消費者的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

- COVID-19 市場影響評估

第5章市場動態

- 市場促進因素

- 尋求透過外包非核心活動獲得競爭優勢的公司

- 食品飲料等主要產業需求穩定

- 主要倉儲供應商進入合約包裝領域,推動創新

- 市場限制

- 嚴格的政府法規

- 與內部包裝衝突

- 行業法規和標準

- 合約包裝的演變

第6章市場區隔

- 服務類型

- 包裝設計與原型製作

- 合約包裝(裝瓶/灌裝、包裝、貼標籤、包裹等)

- 包裝測試

- 倉儲和履約

- 其他

- 最終使用者類型

- 食物

- 飲料

- 製藥

- 家庭和個人護理

- 其他最終用戶細分市場

- 地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

第7章競爭格局

- 公司簡介

- Aaron Thomas Company, Inc.

- ActionPak Inc.

- Assemblies Unlimited, Inc.

- PAC Worldwide, Inc.

- AmeriPac Inc

- Kane Logistics

- FW Logistics

- Warren Industries, Inc.

- Swan Packaging Fulfillment, Inc.

- Multi-Pac Solutions LLC

- Sharp(UDG Healthcare plc)

- Boughey Distribution Ltd

- Budelpack Poortvliet BV

- Wasdell Packaging Group

- Sonoco Products Company

第8章投資分析

第9章 市場機會與未來趨勢

The Contract Packaging and Fulfillment Service Market size is estimated at USD 109.55 billion in 2025, and is expected to reach USD 188.20 billion by 2030, at a CAGR of 11.43% during the forecast period (2025-2030).

The increased demand from food and beverage and pharmaceutical industries was further fuelled by the COVID-19 pandemic. Furthermore, growth of the e-commerce industry globally are among some of the major factors driving growth of the market studied over the forecast period.

Key Highlights

- In recent years, the contract packaging and fulfilment services market has witnessed significant growth, owing to the changing preference of manufacturing firms toward contract packagers, as they are increasingly focusing on cost optimization, to enhance their core competency. Many industry experts claim that these services can reduce operational costs by 7-10%, due to the reduced maintenance costs of machines and labor costs.

- Many governments are also mandating stringent laws and regulations on the labeling and packaging of drugs and food products, which is further expanding the scope of contract packaging. For instance, in the United States, due to similar laws, the companies have preferred to outsource their manufacturing and packaging due to capital and other regulatory barriers.

- In developed markets, such as Europe and North America, the need to enhance quality is also forcing companies to invest in the studied market. In these regions, the role of contract packaging and fulfilment service providers shifted from temporary facility for external packaging to a strategic innovation partner, which ensures even shorter delivery times and can produce even smaller production batches.

- The market is also witnessing the emergence of associations and organizations to create more awareness in the studied market. European Co-Packers Association and Contract Packaging Association are a few examples. There are around 1,000 contract packaging vendors active in Europe, out of which 40-50% are small companies.

- With the outbreak of COVID-19, the contract packaging and fulfillment services market has witnessed tremendous growth as the e-commerce market has taken a boom owing to lockdown and social distancing norms where the majority of the consumer are preferring online channel for shopping and companies are outsourcing their packaging end to end or standalone services to meet the growing demand.

Contract Packaging and Fulfillment Service Market Trends

Contract Packing is Expected to Witness Significant Growth

- Contract packing service holds one of the largest market shares in the studied market as it comprises of various operation ranging from Bottling/Filling, Packaging, Labeling, Wrapping, among other that are an essential part of contract packaging services. Also, the contract packing are divided into three parts- primary packaging, secondary packaging, and tertiary packaging.

- Primary packaging involves direct contact with the product or is the first packaging layer in which the product is enclosed, which enables the user to protect and preserve the product from external contamination, damage, and spoiling.

- Primary contract packaging provides 'mission-critical' capabilities that may be inaccessible to manufacturers, especially when it comes to projects that require short runs or frequent changeovers, such as new or niche products, or seasonal demand, that are usually outside of primary manufacturing economies.

- The primary packaging typically includes blister packs, clamshell packaging, paperboard packaging, unit dose packs, and shrink-wrapping. Players, such as the Wasdell Packaging Group, provide primary contract packaging services that include blister packing, container filling, strip packs, and sachet filling and packing.

- The rising demand from other end-user industries, such as food and beverages and personal care, for the primary packaging, has left the players to increase the production of their end products, thereby making it essential for them to reduce the time to markets by outsourcing the packaging activities. This is expected to boost the primary contract packaging market over the forecast period.

Asia-Pacific to Witness Highest Growth

- The pandemic has fueled E-commerce growth, including the cross-border online sales between Chinese sellers and European buyers. According to CNBC, China's cross-border e-commerce sales rose to 31.1% in 2020, while warehouses grew by 80%. Some of the Chinese market's big giants, such as Alibaba, have been expanding their cross-border e-commerce business through the AliExpress platform and Cainiao logistics arm. This is expected to drive the Fulfillment and warehousing services in the region.

- According to Alibaba, cross-border e-commerce has contributed a 51% year-on-year surge in Cainiao's revenue to USD 1.74 billion in the last three months of 2020. Revenue from the company's international commerce wholesale rose 53%, accounting for USD 577 million during that time. This increases opportunities for the vendors in the market to expand the warehousing services in the Asian market.

- Also, co-packing services are increasing in China, with more and more vendors venturing into the business. For instance, Sofeast, a chines-based company, offers Co-packaging for Chinese buyers with local suppliers and enable the customers to outsource the labeling and packaging services by eliminating the need for IP, pricing, or distribution channel information,

- Furthermore, trends like same-day deliveries and catering orders from various online marketplaces, like Amazon, eBay, flipkart, and snapdeal, have helped organizations gain expertise. Also, Amazon, Flipkart, is expanding its foothold in the developing economy by opening its fulfillment center. For instance, in July 2020, Amazon India announced to expand its fulfillment network in India, with ten new Fulfillment Centers (FC) and an expansion of 7 existing buildings. With this, Amazon expands its operations network to sixty fulfillment centers across 15 states in India to increase the storage capacity by 20% to total more than 32 million cubic feet. This helps in faster delivery and growth of packaging, logistics, and transportation.

Contract Packaging and Fulfillment Service Industry Overview

The Contract Packaging and Fulfillment Service Market is highly competitive owing to the presence of multiple players in the market operating their business in domestic and international markets. The market appears to be moderately concentrated with the major players adopting strategies like expansion among others in order to stay competitive and expand their reach. Some of the major players in the market are Aaron Thomas Company, ActionPak Inc., Assemblies Unlimited among others.

- March 2021 - ActionPak Inc. announced that it completed the 196-kW rooftop solar installation on its new 175,000 sq ft, packaging facility located in Camden, New Jersey, to do both primary and secondary packaging of food and OTC products under strict SQF and FDA guidelines. The 491 solar panels are said to offset 20% of the electric usage at the newly constructed building.

- May 2020 - Sharp (UDG Healthcare PLC) announced the acquisition of a pharmaceutical packaging facility from Quality Packaging Specialists International LLC (QPSI). The facility is 160,000 sq. ft and has full regulatory approval. It encompasses 12 primary production suites, space for multiple secondary packaging lines for offering both primary and secondary pharmaceutical packaging including bottling, blistering, vial labeling and medical device kitting as well as serialization services.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Threat of New Entrants

- 4.3.3 Bargaining Power of Buyers/Consumers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of COVID-19 Impact on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Companies Looking to Gain Competitive Advantage by Outsourcing Non-core Operations

- 5.1.2 Steady Demand from Key Verticals, such as the Food and Beverage Sector

- 5.1.3 Entry of Key Warehousing Vendors in the Field of Contract Packaging Expected to Drive Innovation

- 5.2 Market Restraints

- 5.2.1 Stringent Government Regulations

- 5.2.2 Competition from In-house Packaging

- 5.3 Industry Regulations and Standards

- 5.4 Evolution of Contract Packaging

6 MARKET SEGMENTATION

- 6.1 Service Type

- 6.1.1 Packaging Design & Prototyping

- 6.1.2 Contract Packing (Bottling/Filling, Packaging, Labeling, Wrapping, etc.)

- 6.1.3 Package Testing

- 6.1.4 Warehousing and Fulfilment

- 6.1.5 Other Service Types

- 6.2 End-user Type

- 6.2.1 Food

- 6.2.2 Beverage

- 6.2.3 Pharmaceutical

- 6.2.4 Household & Personal Care

- 6.2.5 Other End-user Segments

- 6.3 Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Aaron Thomas Company, Inc.

- 7.1.2 ActionPak Inc.

- 7.1.3 Assemblies Unlimited, Inc.

- 7.1.4 PAC Worldwide, Inc.

- 7.1.5 AmeriPac Inc

- 7.1.6 Kane Logistics

- 7.1.7 FW Logistics

- 7.1.8 Warren Industries, Inc.

- 7.1.9 Swan Packaging Fulfillment, Inc.

- 7.1.10 Multi-Pac Solutions LLC

- 7.1.11 Sharp (UDG Healthcare plc)

- 7.1.12 Boughey Distribution Ltd

- 7.1.13 Budelpack Poortvliet B.V

- 7.1.14 Wasdell Packaging Group

- 7.1.15 Sonoco Products Company

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

合約包裝市場:2026-2032年全球市場預測(按包裝類型、服務類型、包裝材料、合約類型和最終用途行業分類)

合約包裝市場:2026-2032年全球市場預測(按包裝類型、服務類型、包裝材料、合約類型和最終用途行業分類) 合約包裝市場規模、佔有率、成長及全球產業分析:按類型、應用和地區洞察,2026-2034年預測全球合約包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)家具拆卸和包裝服務市場按服務類型、應用和最終用戶分類-2026年至2032年全球預測

合約包裝市場規模、佔有率、成長及全球產業分析:按類型、應用和地區洞察,2026-2034年預測全球合約包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)家具拆卸和包裝服務市場按服務類型、應用和最終用戶分類-2026年至2032年全球預測 合約包裝市場規模、佔有率和成長分析(按包裝類型、材料、服務、最終用戶產業和地區分類)-產業預測,2026-2033年

合約包裝市場規模、佔有率和成長分析(按包裝類型、材料、服務、最終用戶產業和地區分類)-產業預測,2026-2033年 2025-2029年全球合約包裝市場

2025-2029年全球合約包裝市場 合約包裝和履約服務市場預測至 2032 年:按包裝類型、服務類型、最終用戶和地區進行的全球分析

合約包裝和履約服務市場預測至 2032 年:按包裝類型、服務類型、最終用戶和地區進行的全球分析 2025 年至 2033 年合約包裝市場規模、佔有率、趨勢及預測(按包裝類型、材料、服務、最終用途行業和地區)

2025 年至 2033 年合約包裝市場規模、佔有率、趨勢及預測(按包裝類型、材料、服務、最終用途行業和地區) 合約包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

合約包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 合約包裝和履行服務市場 - 全球行業規模、佔有率、趨勢、機會和預測,按服務類型、最終用戶、地區和競爭細分,2020-2030 年預測

合約包裝和履行服務市場 - 全球行業規模、佔有率、趨勢、機會和預測,按服務類型、最終用戶、地區和競爭細分,2020-2030 年預測