|

市場調查報告書

商品編碼

1690062

歐洲電動卡車:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)Europe Electric Truck - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

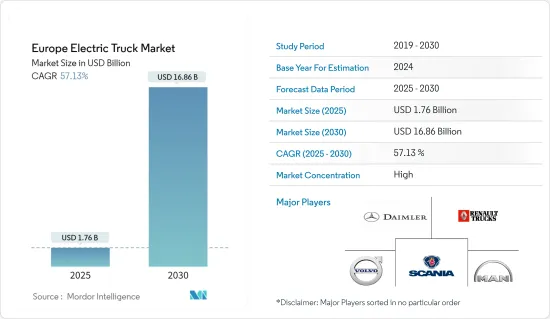

預計2025年歐洲電動卡車市場規模為17.6億美元,2030年將達到168.6億美元,預測期間(2025-2030年)的複合年成長率為57.13%。

由於全部區域政府實施的貿易和旅行限制,COVID-19 疫情阻礙了電動卡車市場的成長。不過,2020年上半年電動卡車銷售量大幅下滑,下半年強勁反彈。

從中期來看,電動卡車有望成為比柴油卡車更受歡迎的選擇,因為它具有扭矩大、噪音污染小、維護成本低等顯著優勢。

然而,隨著法規的放寬,電子商務和物流供應商對電動卡車的需求增加,收益也隨之成長。預計,在顯著的環境目標的推動下,全部區域替代燃料卡車(尤其是商用電池電動卡車)的發展將進一步推動當前的情況。例如,瑞士透過對柴油卡車徵收道路稅來鼓勵燃料電池電動卡車的發展,使替代燃料對瑞士大型零售商協會更具吸引力。

主要亮點

- 歐盟委員會於2021年10月推出了替代燃料基礎設施基金。該基金規模為15億美元,將支持興建零排放基礎設施,包括快速充電站和加氫站。該基金將協助歐洲國家實現2025年安裝100萬個充電站、2030年安裝350萬個充電站的目標。

- 德國政府也承諾額外投入 66 億美元,鼓勵商業車隊更換或升級柴油車輛。這筆資金將用於購買 N1(相當於美國2 級)、N2(相當於美國3-6 級)和 N3(相當於美國7-8 級)零排放汽車,以及將 N2 和 N3 汽車改裝為零排放汽車。該計劃還包括擴大為新車提供動力所需的零排放基礎設施的資金。預計未來比利時、丹麥、法國、西班牙等國家也將效法德國的做法。

預計在預測期內,制定針對內燃機汽車的嚴格排放法規以及增加政府獎勵和補貼以增加商用電動車(尤其是卡車)的普及率將推動市場發展。自動駕駛技術、輕量化零件和材料的發展將為市場企業提供新的機會。

除此之外,主要市場參與者對研發的投資增加以及自動駕駛卡車的顯著發展也是未來推動整個歐洲電動卡車市場向前發展的其他因素。

歐洲電動卡車市場趨勢

純電動卡車發展勢頭強勁

由於對環境問題的擔憂日益加劇,政府和環境機構正在製定嚴格的排放法規和立法,這可能會在預測期內增加電力傳動系統和節油柴油引擎的製造成本。

此外,預計在預測期內,旨在推動電動卡車廣泛應用的創新政府立法政策將推動市場需求。例如,2022年2月,歐盟成員國通過了新的立法,要求所有歐盟成員國在2023年實施新的道路收費制度,為零排放卡車提供重大獎勵。

- 到 2023 年 5 月,營運零排放卡車(即電池電動或氫動力汽車)的運輸商將享受至少 50% 的基於距離的道路通行費折扣。成員國可以選擇對石化燃料卡車徵收基於二氧化碳的附加費,或同時實施這兩項措施。每輛卡車每年的道路通行費為 25,000 歐元,改用零排放汽車可大幅降低運輸成本。

- 新法也要求各國從2026年起對卡車徵收空氣污染費。從2024年起,新的基於時間的卡車道路使用費可能僅限於有限情況,因為它們不如基於距離的收費公平。如果2024年4月之後要在主要高速公路上實施計時收費,則必須根據卡車的二氧化碳排放調整收費標準。擁有收費公路並簽訂了特許經營協議的國家可以免除二氧化碳排放和空氣污染收費,但僅限於合約續約或進行重大修改之前。

綠色交通正在全球迅速擴張,因此貨運公司也將現有車隊轉換為電力驅動車輛。隨著電動卡車需求的成長,汽車製造商正計劃推出更多的電動卡車。例如

- 2022 年 6 月,瑞典斯堪尼亞推出了所謂的「下一代電池電動卡車 (BEV)」。配備 R 或 S 臥舖駕駛室的新型電動卡車的充電容量高達 375kW,這意味著充電一小時可增加約 270-300 公里的續航里程,而 Scania 45 R 或 S 的功率水平為 410kW(相當於約 560 馬力)。

此外,隨著電子商務和物流活動的擴展,這些領域的多家公司廣泛依賴卡車運輸業在全國範圍內運輸貨物。亞馬遜等大型線上競爭對手以及使用卡車和司機作為其電子商務供應鏈一部分的零售商正在推動對更快送貨速度的需求。例如,

- 2021年,歐洲電子商務規模成長13%,達7,180億歐元。增速較2020年略有上升,但維持穩定。根據2022年歐洲電子商務和歐元商務報告,西歐是迄今為止B2C電子商務領域最強勁的地區,佔2021年總銷售額的63%。排名第二的是南歐,僅佔總銷售額的16%,第三和第四是中歐和北歐(分別為10%和9%),最後是東歐(2%)。

基於上述因素,新型電動卡車的持續推出、電動卡車製造投資的增加以及世界各國政府的電動車支援政策可能會在預測期內推動電池電動卡車市場的發展。

英國在預測期內將實現顯著成長

預計預測期內英國將佔據電動卡車總銷量的很大佔有率。英國正在大力投資開發電動車基礎設施。該國已開通一條新的電動高速公路,供架空線路驅動的混合動力電動卡車使用。該國堅持不懈地致力於鼓勵電動車的發展,並推出政策推動電動卡車進入該國,預計將刺激市場需求。

該國的污染法規不斷變化,未來柴油卡車可能會被徹底淘汰。柴油卡車將被電動車取代,從而推動電動工程車輛產業的發展。

此外,英國政府將電動貨車和卡車補貼計畫延長兩年,至2025年。新的重量級別將從4月起有資格獲得補助。政府表示,這項補貼旨在幫助企業轉型其車輛,並使其在 2030 年逐步淘汰內燃機之前「領先一步」。自 2012 年推出以來,插電式貨車和卡車補貼已幫助英國購買了超過 26,000 輛電動貨車和卡車。

- 截至2021年底,政府已降低電動車補貼率。自 2022 年 4 月 1 日起,大型貨車和小型電動卡車也屬於此變更範圍。電動卡車的最低重量要求將從 3.5 噸增加到 4.25 噸,但上限仍為 12 噸。這些汽車將獲得購買價格 20% 的補貼,每輛車最高補貼額為 16,000 英鎊。此外,重量不超過16,000磅的輕型電動卡車的補貼門檻將從3.5噸提高到4.25噸。重量不超過 4.25 噸的電動卡車將獲得 5,000 英鎊的補助。

隨著電子商務領域的擴張,日本對物流和配送公司的需求日益成長。為了實現市場佔有率的商業化,這些公司已經開始製定計劃,在未來幾年在其車隊中部署更多的電動商用車。例如

- 2022年5月,沃爾沃卡車與德國郵政敦豪集團同意合作,加速零排放汽車轉型。 DHL 計劃在其歐洲航線上部署 44 輛新型沃爾沃電動卡車,加速向重型電動車的轉變。計劃中的訂單包括 40 輛沃爾沃 FE 和沃爾沃 FL 電動卡車,用於都市區的包裹遞送。 DHL 已選擇使用沃爾沃卡車進行區域運輸,首先在英國使用四輛沃爾沃 FM 電動卡車。

- 2021 年 12 月,樂購宣布計劃將英國首輛全電動式重型貨車投入其位於威爾斯的配送中心商業使用。這些車輛一次充電可行駛約 100 英里,兩輛 37 噸重的卡車將把貨物從卡迪夫的鐵路貨運站運送到該公司位於馬戈爾的樞紐。

因此,隨著上述案例以及該國與電動卡車相關的發展,英國電動卡車市場有望佔據整體市場的巨大佔有率。

歐洲電動卡車產業概況

歐洲電動卡車市場以戴姆勒、斯堪尼亞、曼恩、雷諾卡車和沃爾沃卡車等主要企業為特徵。市場競爭非常激烈,大型企業和本地企業都在爭奪更大的市場佔有率。公司正在進行合併、收購、合資和合作協議以加強其市場地位。例如

2022 年 5 月,沃爾沃卡車與 Bücher Municipal 合作,將下水道清潔卡車電動化。 Bücher Municipal 的目標是到 2023 年底向歐洲社區提供多達 80 輛全電動下水道清潔車。到 2023 年底,Bücher Municipal 預計多達 80 輛下水道清潔車將是零排放沃爾沃卡車,佔其產量的 50%。

2022 年 3 月,雷諾卡車宣布與 Geodis推出新計劃:Oxygen 16 噸電動卡車。雷諾卡車推出了其 E-Tech 產品組合,這是一系列重要服務,旨在支持客戶轉型為電動車。用於區域運輸的雷諾卡車 T E-Tech 和用於建設業的雷諾卡車 C E-Tech 將於 2023 年推出。

2021 年 6 月,Volta Trucks 推出了 Volta Zero 的首個運行原型底盤。 Volta Zero 將成為歐洲第一款採用創新 e-Axle 的商用車,可提高效率和續航里程。客戶客製化車輛的全面生產預計將於 2022 年底開始。

2021 年 6 月,Proton 馬達 Fuel Cell GmbH 與英國公司 Electra Commercial Vehicles 簽署了一份合作備忘錄 (MoU),以開發英國和愛爾蘭的零排放燃料電池卡車市場。根據合作備忘錄,Electra 將作為系統整合,將 Proton 馬達 Fuel Cell 的燃料電池系統整合到其現有的電動卡車產品組合中。

因此,基於上述案例和該地區的發展,市場公司正在探索新的機會,以佔領歐洲電動卡車市場的大部分市場佔有率。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場促進因素

- 市場限制

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章市場區隔

- 依推進類型

- 插電式混合動力

- 燃料電池電動

- 電池電動

- 按卡車類型

- 小型貨車

- 中型卡車

- 大型卡車

- 按應用

- 後勤

- 地方政府

- 其他用途

- 按國家

- 德國

- 英國

- 法國

- 義大利

- 荷蘭

- 西班牙

- 其他歐洲國家

第6章競爭格局

- 供應商市場佔有率

- 公司簡介

- AB Volvo

- Volta Trucks

- Daimler Trucks(Mercedes Benz Group AG)

- DAF Trucks NV(PACCAR Inc.)

- E-Trucks Europe BE

- Renault Trucks

- Tesla Motors Inc.

- Einride AB

- Tevva Motors Limited

- BYD Co. Ltd

- Scania AG

- MAN SE(Volkaswagen AG)

- IVECO SpA

- E-Force One AG

第7章 市場機會與未來趨勢

The Europe Electric Truck Market size is estimated at USD 1.76 billion in 2025, and is expected to reach USD 16.86 billion by 2030, at a CAGR of 57.13% during the forecast period (2025-2030).

The COVID-19 pandemic hindered the growth of the electric truck market due to trade and travel restrictions imposed by governments across the region. However, the sales of electric trucks decreased notably in the first half of 2020 and recovered significantly in the latter half.

Over the medium-term, electric trucks are expected to become the preferred choice over diesel trucks owing to their remarkable advantages such as gobs of torque, noise pollution, lower maintenance cost, and others.

However, as restrictions eased, e-commerce and logistic providers witnessed revenue growth, increasing demand for electric trucks. The current situation is further expected to be driven by the development of alternative-fueled trucks, specifically commercial battery-electric trucks, across the European region, in the wake of its notable environmental targets. For instance, Switzerland is encouraging fuel cell electric truck growth through its road tax on diesel truck operations, making alternative fuels more attractive for large Swiss retail associations.

Key Highlights

- The European Commission launched the 'Alternative Fuels Infrastructure Facility' in October 2021. The USD 1.5 billion funds support building zero-emission infrastructure such as fast charging and hydrogen refueling stations. The fund brings European countries closer to reaching their goal of 1 million recharging stations by 2025 and 3.5 million by 2030.

- The German government also pledged an additional USD 6.6 billion to incentivize commercial fleets to replace or upfit their diesel vehicles. The funding covers the purchase of N1 (similar to US class 2), N2 (similar to US class 3-6), and N3 (similar to US class 7-8) zero-emissions vehicles, as well as the conversion to zero-emission drives in N2 and N3 vehicles. The program also includes funding for expanding the zero-emission infrastructure required to power the new vehicles. Countries such as Belgium, Denmark, France, and Spain are expected to follow Germany's example in the future.

Enactment of stringent emission norms on the use of IC engine-powered vehicles and rising government incentives and subsidies focusing on improving the penetration rate of commercial electric vehicles, especially trucks, are expected to drive the market during the forecast period. Development of self-driving technology, lightweight components, and materials to offer new opportunities for players in the market.

Besides these, increasing investments in research and development efforts by key market players and notable developments across autonomous trucks/self-driving trucks are other factors expected to drive the overall Europe electric truck market forward in the future.

Electric Trucks Europe Market Trends

Battery Electric Truck Gaining Momentum

With the growing environmental concerns, governments and environmental agencies are enacting stringent emission norms and laws that may increase the manufacturing cost of electric drivetrains and fuel-efficient diesel engines during the forecast period.

Further, innovative government legislative policies focusing on spurring the penetration of electric trucks are expected to propel demand in the market during the forecast period. For instance, in February 2022, EU member states adopted new legislation which states that all EU member states have until 2023 to implement a new road toll system that gives big incentives for zero-emissions trucks.

- By May 2023, haulers operating zero-emissions trucks, i.e., battery electric or hydrogen, must be given at least 50% discounts on distance-based road tolls. Member states could opt to levy extra CO2-based charges on fossil fuel lorries instead or implement both measures. With road tolls costing haulers up to EUR 25,000 per truck annually, switching to zero-emissions vehicles may cut their overheads considerably.

- The new law also requires countries to apply truck air pollution charges from 2026. From 2024, new time-based road charges for trucks, less fair than distance-based tolling, may be restricted to limited circumstances. If time-based charges remain on major highways after April 2024, they must be varied according to the truck's CO2 emissions. Countries with toll roads under concession contracts may exempt these tolls from both CO2- and air pollution-based charging, but only until these contracts are renewed or substantially amended.

Green transportation is swiftly growing around the world, owing to which the goods transportation companies are also converting their existing fleet into electric propulsion-based vehicles. As the demand for electric trucks is growing, vehicle manufacturers are planning to launch more electric trucks. For instance,

- In June 2022, Swedish Company Scania introduced the "next level of battery-electric trucks (BEV)." With R or S sleeper cabs, the charging capability of the new e-trucks could be up to 375 kW, which means that an hour of charging will add some 270 to 300 km of range, and the power output level for a Scania 45 R or S is 410 kW (equivalent to some 560 hp).

Furthermore, in the wake of growing e-commerce and logistic activities, several companies operating across these sectors are widely depending on the trucking industry to transport goods across the nation. The demand for increases in shipping speed is fueled by huge online competitors, such as Amazon and other retailers that use their trucks and drivers as part of their e-commerce supply chain. For instance,

- In 2021, European e-commerce increased by 13 % to EUR 718 billion. The growth rate has remained stable, though it has risen slightly compared to 2020. According to the e-commerce Europe and euro commerce report 2022, Western Europe is, by far, the strongest region in B2C e-commerce turnover, holding 63% of the total turnover for 2021. Southern Europe follows in second place with just 16% of total turnover, Central Europe and Northern Europe come in third and fourth (10% and 9% respectively), and Eastern Europe (2%) in last place.

Based on the aforementioned factors, consistent launches of new electric trucks, growing investment in electric truck manufacturing, and the government's EV-supporting policies around the world are likely to drive the battery-electric truck market over the forecast period.

United Kingdom to Exhibit a Significant Growth Rate During the Forecast Period

The United Kingdom is expected to account for a significant share of the total sales of electric trucks during the forecast period. The United Kingdom is investing heavily in infrastructure development for electric mobility. It opened a new electric highway for hybrid electric trucks that overhead electric lines will power. It is constantly focusing on encouraging electric mobility and its policies are intended to push electric trucks into the country, expected to drive demand in the market.

Country's pollution laws are constantly changing, and diesel-powered trucks may be phased out entirely in the future. They would be replaced by electric counterparts, taking advantage of the electric construction vehicle industry.

Additionally, the British government has extended its electric van and truck subsidy scheme for another two years until 2025. New weight classes will be eligible for the subsidy beginning in April. According to the government, the subsidy is designed to help businesses convert their fleets in time and be "one step ahead" of the combustion engine's demise in 2030. Since the scheme's inception in 2012, plug-in van and truck grants have aided in the purchase of over 26,000 electric vans and trucks in the United Kingdom.

- By the end of 2021, the government had already cut the subsidy rates for electric vehicles. The large vans and small electric trucks were also subject to changes from April 1, 2022. The lower weight requirement for electric trucks rises from 3.5 to 4.25 tones, while the highest limit remains at 12 tones. These automobiles will be subsidized by 20% of the purchase price, up to a maximum of £16,000 per vehicle. Furthermore, the grant threshold for small electric trucks up to 16,000 pounds would be lifted from 3.5 tons to 4.25 tons. Electric trucks weighing up to 4.25 tons will be eligible for a £5,000 subsidy.

With the growing e-commerce sector, the demand from Logistics and delivery companies in the country has increased. To commercialize the market share, these companies started designing plans to deploy more electric commercial vehicles in their fleet in the coming years. For instance,

- In May 2022, Volvo Trucks and Deutsche Post DHL Group have agreed to collaborate to expedite the transition to zero-emission vehicles. DHL plans to accelerate its shift to big electric vehicles by deploying 44 new electric Volvo trucks on European routes. The planned order includes 40 Volvo FE and Volvo FL electric trucks, which will be utilized for package deliveries in urban areas. Electric trucks for longer routes are also included in the scope, and DHL has opted to start employing Volvo trucks for regional haulage, beginning with four Volvo FM Electric trucks in the United Kingdom.

- In December 2021, Tesco announced its plans to launch the first fully-electric HGVs used commercially in Britain to serve its distribution center in Wales. The vehicles can travel about 100 miles on a single charge, and these two 37-tonne trucks will transport goods from a rail freight terminal in Cardiff to the company's hub in Magor.

Therefore, in line with the abovementioned instances and developments associated with electric trucks in the country, the UK electric truck market is expected to capture a significant share in the overall market.

Electric Trucks Europe Industry Overview

The European electric truck market is characterized by major players, such as Daimler, Scania, MAN, Renault Trucks, Volvo Trucks, etc. The market is highly competitive, as major and local players compete to gain a larger market share. Companies are entering into mergers, acquisitions, joint ventures, and collaboration agreements to strengthen their position in the market. For instance,

In May 2022, Volvo Trucks and Bucher Municipal joined in electrifying sewer cleaner trucks. Bucher Municipal aims to provide up to 80 fully electric sewer cleaner vehicles to European communities by the end of 2023. By the end of 2023, Bucher Municipal anticipates that up to 80 sewer trucks, or 50% of their cleaning vehicle production, maybe Volvo zero-emission trucks.

In March 2022, Renault Trucks announced the launch of a new project with Geodis, the Oxygen 16-ton e-truck. Renault Trucks announced its E-Tech portfolio, which includes some critical services that may assist customers in their transition to electric vehicles. The Renault Trucks T E-Tech for regional transport and the Renault Trucks C E-Tech for the construction industry will be available in 2023.

In June 2021, Volta Trucks revealed the first running prototype chassis of the Volta Zero - the world's first purpose-built full electric 16-tonne commercial vehicle designed specifically for inner-city logistics. The Volta Zero will be Europe's first commercial vehicle to use an innovative e-Axle for increased efficiency and vehicle range. Full-scale production of customer-specification vehicles will then follow at the end of 2022.

In June 2021, Proton Motor Fuel Cell GmbH signed a "Memorandum of Understanding" (MoU) with UK company "Electra Commercial Vehicles Limited" to develop the zero-emission fuel cell truck market in the UK and Ireland. Under the MoU, Electra will act as a system integrator to integrate Proton Motor Fuel Cell's fuel cell systems into their existing electric truck portfolio.

Thus, based on the abovementioned instances and developments in the region, market players anticipated exploring new opportunities to capture the majority market share in the Europe electric truck market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value USD Million)

- 5.1 By Propulsion Type

- 5.1.1 Plug-In Hybrid

- 5.1.2 Fuel Cell Electric

- 5.1.3 Battery-Electric

- 5.2 By Truck Type

- 5.2.1 Light Truck

- 5.2.2 Medium-Duty Truck

- 5.2.3 Heavy-Duty Truck

- 5.3 By Application

- 5.3.1 Logistics

- 5.3.2 Municipal

- 5.3.3 Other Applications

- 5.4 By Country

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Netherland

- 5.4.6 Spain

- 5.4.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 AB Volvo

- 6.2.2 Volta Trucks

- 6.2.3 Daimler Trucks (Mercedes Benz Group AG )

- 6.2.4 DAF Trucks NV (PACCAR Inc.)

- 6.2.5 E-Trucks Europe BE

- 6.2.6 Renault Trucks

- 6.2.7 Tesla Motors Inc.

- 6.2.8 Einride AB

- 6.2.9 Tevva Motors Limited

- 6.2.10 BYD Co. Ltd

- 6.2.11 Scania AG

- 6.2.12 MAN SE (Volkaswagen AG)

- 6.2.13 IVECO SpA

- 6.2.14 E-Force One AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

日本電動卡車市場報告(按車輛類型、動力方式、續航里程、應用領域和地區分類,2026-2034年)

日本電動卡車市場報告(按車輛類型、動力方式、續航里程、應用領域和地區分類,2026-2034年) 重型電動卡車市場規模、佔有率和趨勢分析報告:按車輛類型、動力類型、應用、地區和細分市場預測(2026-2033 年)

重型電動卡車市場規模、佔有率和趨勢分析報告:按車輛類型、動力類型、應用、地區和細分市場預測(2026-2033 年) 電動卡車市場按動力系統、車輛類型、續航里程和區域分類

電動卡車市場按動力系統、車輛類型、續航里程和區域分類 電動卡車市場預測至2032年:全球分析(按組件、車輛類型、動力系統、續航里程、電池容量、電池類型、應用和地區分類)

電動卡車市場預測至2032年:全球分析(按組件、車輛類型、動力系統、續航里程、電池容量、電池類型、應用和地區分類) 全電動卡車:全球市場佔有率和排名、總銷量和需求預測(2025-2031年)電池電動卡車市場預測至2032年:按車輛類型、電池類型、充電方式、車身類型、最終用戶和地區分類的全球分析

全電動卡車:全球市場佔有率和排名、總銷量和需求預測(2025-2031年)電池電動卡車市場預測至2032年:按車輛類型、電池類型、充電方式、車身類型、最終用戶和地區分類的全球分析 自動中型及大型卡車市場2025 年至 2033 年電動卡車市場規模、佔有率、趨勢及預測(按車輛類型、推進系統、續航里程、應用和地區)

自動中型及大型卡車市場2025 年至 2033 年電動卡車市場規模、佔有率、趨勢及預測(按車輛類型、推進系統、續航里程、應用和地區) 全球電動卡車市場(負載容量、卡車類型、推進類型、電池容量、應用和銷售管道)預測 2025-2030 年

全球電動卡車市場(負載容量、卡車類型、推進類型、電池容量、應用和銷售管道)預測 2025-2030 年 全球外送車市場

全球外送車市場