|

市場調查報告書

商品編碼

1683939

歐洲LED照明:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Europe LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

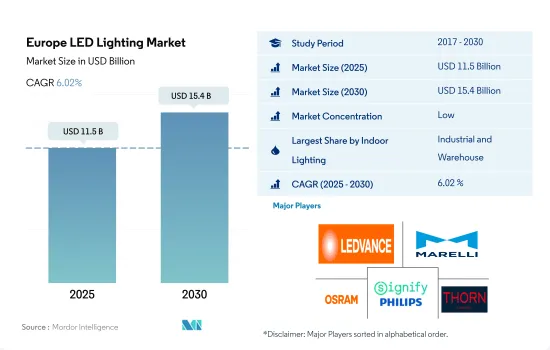

預計2025年歐洲LED照明市場規模為115億美元,到2030年將達到154億美元,預測期間(2025-2030年)的複合年成長率為6.02%。

工業和住宅領域的發展不斷加快,推動市場成長

- 以金額為準,截至2023年,工業和倉庫照明將佔較大佔有率,其次是商業、住宅和農業照明。法國、俄羅斯和波蘭佔據倉庫建設的大部分。新冠疫情危機加速了法國恢復工業能至疫情前水準的努力。 2022年12月,法國工業生產成長1.1%,11月成長2%。波蘭擁有近440萬平方公尺的空間。到 2022 年中期,波蘭將建造近 450 萬平方公尺的倉庫和工業空間。

- 在商業設施中,醫院、學校和機場佔據了大部分市場。在受訪的42個國家中,可支配所得差異很大。列支敦士登、瑞士和盧森堡的可支配收入最高,因此人們更容易負擔學校或大學的學費。

- 截至 2023 年,住宅領域將佔最大佔有率。在強勁需求的支撐下,義大利住宅市場保持穩定。 2021 年第四季住宅房地產交易量年增 14.1%,達到 263,795 套。所有地區的銷售額均強勁成長。自 2022 年 1 月上次封鎖結束以來,儘管許多企業正處於過渡期,但辦公室入住率仍呈上升趨勢。截至 2022 年第三季度,辦公大樓領域的平均折扣為 26%,低於 31% 的整體平均值。 年終整體空置率為7.2%,與2021年終相比大致穩定(+10bp)。整體而言,辦公室和住宅的吸收率正在上升,導致LED需求大幅增加。

倉庫和體育場建設的增加以及各國政府的資助正在推動市場

- 2023 年,其他歐洲國家將佔據大部分市場佔有率。歐盟各地的開發活動持續保持中等水平,2022 年將有超過 2,000 萬平方公尺的現代化倉庫和工業空間進入市場。波蘭在倉庫建設開發領域處於領先地位。在歐洲,波蘭以約 440 萬平方公尺的面積領先。捷克共和國的供應量也創歷史新高,超過 110 萬平方公尺。到 2022 年中期,波蘭將建造近 450 萬平方公尺的倉庫和工業空間。

- 體育場館的持續發展和維修正在推動 LED 照明的使用。例如,西班牙的瓦倫西亞是第二大投資者,斥資3億歐元,計劃於2022年建造諾梅斯塔利亞球場。塞爾維亞足球聯合會(FSS)在歐洲足球協會聯盟(UEFA)的支持下,已投資超過2000萬歐元,用於2023年對全國多個體育場館進行現代化改造。這些發展反映了該國對LED照明日益成長的需求。

- 2023年,法國將佔據較大的金額佔有率,而德國將佔據最高的銷售佔有率。巴黎市已與電力公司 EDF 和工程公司 Eiffage 的一家子公司簽訂了一份價值 7.04 億歐元的契約,用於對其街道照明和配電線路進行現代化改造。德國聯邦政府正在採取措施,實現2050年使國家實現氣候中和的目標。政府希望透過為新住宅和多用戶住宅提供額外資金來實現這一目標,津貼最高可達投資價值的20%。這些努力有望促進LED照明市場的成長。

歐洲 LED 照明市場趨勢

住宅和非住宅用途的增加可能推動 LED 照明的成長

- 2022年,歐洲人口為7.435億。歐盟成員國共有超過1.31億棟建築物。歐盟有1.19億棟住宅和1200萬棟非住宅。 2022年,住宅需求依然強勁,鼓勵該地區住宅建設,並使當地LED市場受益。

- 預計家庭數量將從 2020 年的 1.96 億增加到 2021 年的 1.974 億。在歐盟,2021 年 49.4% 的家庭有一個孩子,其次是 38.6% 有兩個孩子,12% 有三個或三個以上孩子。 2020年,約70%的歐盟公民擁有自己的住房。 2019年,歐洲平均每人擁有1.6個房間。隨著人口和家庭數量的增加,家庭和商業空間中 LED 的使用可能會增加。

- 截至2019年,歐盟道路上共有2.427億輛汽車,比與前一年同期比較成長1.8%,其中包括2800萬多輛貨車。目前,法國是持有數量最多的國家,共擁有 600 萬輛,其次是義大利(420 萬輛)、西班牙(380 萬輛)和德國(280 萬輛)。歐盟道路上有 620 萬輛中型和重型商用車。儘管近期註冊量增加,但歐盟所有車輛中只有 4.6% 採用替代能源。混合動力電動車佔歐盟道路上所有車輛的 0.8%,而電池電動車和插電式混合動力車僅佔 0.2%。汽車銷量的成長可能會對該地區的 LED 銷售產生積極影響。

可支配收入增加和政府獎勵有望推動 LED 的普及

- 2022年,歐盟共有1.98億個居住,平均每個家庭有2.2人。該地區人口在2020年為7.462億,到2023年將下降到7.422億。歐盟的房屋自有率從2021年的69.90%下降到2022年的69.10%。這些案例表明,儘管家庭數量略有下降,但住宅開發計劃的數量卻比平常少。因此,預計 LED 滲透率將呈正成長,但與以前相比,住宅領域的成長率較低。

- 在歐洲,大多數國家的可支配收入都很高,這又增加了個人的消費能力,尤其是在購買新住宅空間的消費能力。 2022年英國的人均所得達到3,3,138美元,法國達到2,5,337.7美元。

- 在歐洲,政府正在提供獎勵計劃來促進 LED 的普及。英國政府公佈了節能照明的新提案。根據該提案,LED 等耗能較低的照明設備將取代老式鹵素燈泡。此類努力可為家庭節省 2,000 英鎊(2,525.96 美元)至 3,000 英鎊(3,788.98 美元):歐洲戶外住宅 2021 年 1 月,德國啟動了「聯邦高效建築資助」計畫。任何在德國擁有或考慮購買房產的人都可以申請這筆資金。該能源效率計劃還包括照明節能建築。 2017年6月,法國政府宣布了一項能源效率證書計劃,允許家庭根據其收入獲得最高可達LED燈泡價格100%的補貼。預計預測期內此類案例將推動該地區對 LED 照明的需求。

歐洲LED照明產業概況

歐洲LED照明市場較為分散,前五大企業佔比為36.91%。該市場的主要企業有:LEDVANCE GmbH(MLS)、Marelli Holdings、OSRAM GmbH.、Signify(飛利浦)和Thorn Lighting Ltd.(Zumtobel Group)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第 3 章 簡介

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 汽車產量

- 人口

- 人均收入

- 汽車貸款利率

- 充電站數量

- 持有汽車數量

- LED進口總量

- 照明耗電量

- #家庭數量

- 道路網路

- LED滲透率

- #體育場數量

- 園藝區

- 法律規範

- 室內照明

- 法國

- 德國

- 英國

- 戶外照明

- 法國

- 德國

- 英國

- 汽車照明

- 法國

- 德國

- 西班牙

- 英國

- 室內照明

- 價值鏈與通路分析

第5章 市場區隔

- 室內照明

- 農業照明

- 商業照明

- 辦公室

- 零售

- 其他

- 工業/倉庫

- 住宅照明

- 戶外照明

- 公共設施

- 路

- 其他

- 汽車實用照明

- 日間行車燈 (DRL)

- 方向指示器

- 頭燈

- 倒車燈

- 紅綠燈

- 尾燈

- 其他

- 汽車照明

- 二輪車

- 商用車

- 搭乘用車

- 國家

- 法國

- 德國

- 英國

- 歐洲其他地區

第6章競爭格局

- 主要策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介(包括全球概況、市場層級概況、主要業務部門、財務狀況、員工人數、關鍵資訊、市場排名、市場佔有率、產品和服務、最新發展分析)

- Dialight PLC

- HELLA GmbH & Co. KGaA

- KOITO MANUFACTURING CO., LTD.

- LEDVANCE GmbH(MLS Co Ltd)

- Marelli Holdings Co., Ltd.

- OSRAM GmbH.

- Panasonic Holdings Corporation

- Signify(Philips)

- Thorn Lighting Ltd.(Zumtobel Group)

- Valeo

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 50001637

The Europe LED Lighting Market size is estimated at 11.5 billion USD in 2025, and is expected to reach 15.4 billion USD by 2030, growing at a CAGR of 6.02% during the forecast period (2025-2030).

Increasing development in the industrial and residential sectors drives market growth

- In terms of value, as of 2023, industrial and warehouse had a major share, followed by commercial, residential, and agricultural lighting. France, Russia, and Poland had the majority of warehouse constructions. The COVID-19 crisis accelerated France's efforts to return industrial production capacities to the pre-pandemic levels. French industrial production increased by 1.1% over one month in December 2022, after +2% in November 2022. Poland has close to 4.4 million sq. m of space. By the middle of 2022, almost 4.5 million sq. m of warehouse and industrial space was under construction in Poland.

- In commercial, hospitals, schools, and airports comprise the majority of the share. The disposable net income among the 42 countries surveyed varies significantly. Liechtenstein, Switzerland, and Luxembourg have the highest disposable net income by a wide margin, which means more affordability for schools and college studies.

- In terms of volume, as of 2023, the residential sector had a major share. Italy's housing market remains stable, supported by strong demand. In Q4 2021, residential property transactions increased by 14.1% to 263,795 units compared to a year earlier. All regions saw a strong sales increase during the period. Despite many businesses remaining in transition, office usage rates continued on an upward trend from the end of the last lockdown in January 2022. As of Q3 2022, the office sector traded at an average discount of 26%, which was below the 31% overall average. The overall vacancy rate stood at 7.2% at the end of 2022, almost stable compared to the end of 2021 (+10bp). Overall, there is a positive trend toward a higher office and residential absorption rate, leading to a major increase in the demand for LEDs.

Increasing warehouse and stadium construction along with government funds in their countries drives the market

- The Rest of Europe comprised the majority of the market share in 2023. Development activities across the European Union continued at a par level, with more than 20 million sq m of modern warehouse and industrial space entering the market in 2022. Poland leads in the construction segment with its warehouse construction development. In Europe, Poland was at the top, with nearly 4.4 million sq m of space. The Czech Republic also reported high supply levels with over 1.1 million sq m. By the middle of 2022, almost 4.5 million sq m of warehouse and industrial space was under construction in Poland.

- Continued development and renovation of stadiums are encouraging the use of LED lighting. For example, Spain's Valencia was the second-largest investor, with EUR 300 million, to build the Nou Mestalla stadium in 2022. The Serbian Football Federation (FSS) invested over EUR 20 million in modernizing several stadiums in the country in 2023 with the support of the Union of European Football Associations (UEFA). These developments reflect the growing demand for LED lighting in the country.

- France occupied the major value share, and Germany had the highest volume share in 2023. The City of Paris awarded a EUR 704 million contract to subsidiaries of the utility EDF and engineering firm Eiffage to modernize streetlights and energy distribution lines. The German federal government is taking steps to meet its goal of becoming climate-neutral by 2050. The government hopes to achieve this by providing extra funding for newly built houses and apartment buildings and granting up to 20% of the investment. Such initiatives are expected to promote the growth of the LED lighting market.

Europe LED Lighting Market Trends

Increasing residential housing and non-residential buildings may drive the growth of LED lights

- In 2022, Europe had 743.5 million people. The Member States of the European Union contain over 131 million structures. The European Union has 119 million residential buildings and 12 million non-residential buildings. In 2022, the demand for housing remained high, encouraging the building of new homes in the region, thus benefitting the local LED market.

- There were 197.4 million households in 2021 as opposed to 196.0 million in 2020. In the EU, 49.4% of households had a single child in 2021, followed by 38.6% with two children and 12% with three or more. About 70% of EU citizens were homeowners in 2020. In 2019, European homes had 1.6 rooms per person on average. The use of LEDs in homes and business spaces may increase as the population and the number of households rise.

- As of 2019, there were 242.7 million cars on the road in the European Union, an increase of 1.8% from the previous year, and more than 28 million vans on the road. France has by far the largest fleet of vans, with six million vehicles, followed by Italy (4.2 million), Spain (3.8 million), and Germany (2.8 million). EU roadways have 6.2 million medium and heavy commercial vehicles. Even though registrations have gone up recently, only 4.6% of all EU vehicles are alternatively powered. Hybrid electric vehicles make up 0.8% of all vehicles on EU roads, while battery-electric and plug-in hybrid vehicles each account for only 0.2% of the total. The increase in automotive vehicle sales may positively impact LED sales in the region.

Increasing disposable income and government incentives may lead to more LED penetration

- In 2022, 198 million households resided in the EU, with 2.2 members per household on average. The region's population was 746.2 million in 2020, which reduced to 742.2 million by 2023. Homeownership rates in the EU declined by 69.10% in 2022 from 69.90% in 2021. Such instances suggest that housing development projects are less than in previous years despite a slight decline in the number of households. Thus, LED penetration is expected to grow positively but less in the residential segment compared to previous years.

- In Europe, disposable income is high for most countries, resulting in rising spending power of individuals, especially on new residential spaces. The United Kingdom's per capita income reached USD 33,138 in 2022, while that of France reached USD 25,337.7.

- In Europe, the governments provide incentive programs to create more LED penetration. The UK government announced the launch of a new energy-efficient lighting proposal. Under this, lighting, such as low energy-use LEDs, would replace old halogen bulbs. Such initiatives could save households between GBP 2,000 (USD 2,525.96) and GBP 3,000 ( USD 3,788.98) over: Europe outdoor households. The "Federal Funding for Efficient Buildings" program was launched in January 2021 in Germany. Anyone who owns a property in Germany or who is looking to buy property in the country can apply for the funding. The energy efficiency program also includes lighting energy efficiency buildings. In June 2017, the French government announced the Energy Savings Certificate scheme, which allows people to get subsidies that can cover up to 100% of the price of LED bulbs based on the householder's income. Such instances are expected to boost the demand for LED lighting in the region during the forecast period.

Europe LED Lighting Industry Overview

The Europe LED Lighting Market is fragmented, with the top five companies occupying 36.91%. The major players in this market are LEDVANCE GmbH (MLS Co Ltd), Marelli Holdings Co., Ltd., OSRAM GmbH., Signify (Philips) and Thorn Lighting Ltd. (Zumtobel Group) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Automotive Production

- 4.2 Population

- 4.3 Per Capita Income

- 4.4 Interest Rate For Auto Loans

- 4.5 Number Of Charging Stations

- 4.6 Number Of Automobile On-road

- 4.7 Total Import Of Leds

- 4.8 Lighting Electricity Consumption

- 4.9 # Of Households

- 4.10 Road Networks

- 4.11 Led Penetration

- 4.12 # Of Stadiums

- 4.13 Horticulture Area

- 4.14 Regulatory Framework

- 4.14.1 Indoor Lighting

- 4.14.1.1 France

- 4.14.1.2 Germany

- 4.14.1.3 United Kingdom

- 4.14.2 Outdoor Lighting

- 4.14.2.1 France

- 4.14.2.2 Germany

- 4.14.2.3 United Kingdom

- 4.14.3 Automotive Lighting

- 4.14.3.1 France

- 4.14.3.2 Germany

- 4.14.3.3 Spain

- 4.14.3.4 United Kingdom

- 4.14.1 Indoor Lighting

- 4.15 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Indoor Lighting

- 5.1.1 Agricultural Lighting

- 5.1.2 Commercial

- 5.1.2.1 Office

- 5.1.2.2 Retail

- 5.1.2.3 Others

- 5.1.3 Industrial and Warehouse

- 5.1.4 Residential

- 5.2 Outdoor Lighting

- 5.2.1 Public Places

- 5.2.2 Streets and Roadways

- 5.2.3 Others

- 5.3 Automotive Utility Lighting

- 5.3.1 Daytime Running Lights (DRL)

- 5.3.2 Directional Signal Lights

- 5.3.3 Headlights

- 5.3.4 Reverse Light

- 5.3.5 Stop Light

- 5.3.6 Tail Light

- 5.3.7 Others

- 5.4 Automotive Vehicle Lighting

- 5.4.1 2 Wheelers

- 5.4.2 Commercial Vehicles

- 5.4.3 Passenger Cars

- 5.5 Country

- 5.5.1 France

- 5.5.2 Germany

- 5.5.3 United Kingdom

- 5.5.4 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 Dialight PLC

- 6.4.2 HELLA GmbH & Co. KGaA

- 6.4.3 KOITO MANUFACTURING CO., LTD.

- 6.4.4 LEDVANCE GmbH (MLS Co Ltd)

- 6.4.5 Marelli Holdings Co., Ltd.

- 6.4.6 OSRAM GmbH.

- 6.4.7 Panasonic Holdings Corporation

- 6.4.8 Signify (Philips)

- 6.4.9 Thorn Lighting Ltd. (Zumtobel Group)

- 6.4.10 Valeo

7 KEY STRATEGIC QUESTIONS FOR LED CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

全球LED照明市場(至2035年):依產品、安裝類型、銷售通路、顯色指數、控制系統、技術、通路、應用、最終用戶及地區劃分

全球LED照明市場(至2035年):依產品、安裝類型、銷售通路、顯色指數、控制系統、技術、通路、應用、最終用戶及地區劃分 LED 照明和 OLED 照明:市場分析和製造趨勢

LED 照明和 OLED 照明:市場分析和製造趨勢 LED照明供應:全球市佔率及排名、總收入及需求預測(2025-2031年)LED舞檯燈光:全球市佔率及排名、總收入及需求預測(2025-2031年)

LED照明供應:全球市佔率及排名、總收入及需求預測(2025-2031年)LED舞檯燈光:全球市佔率及排名、總收入及需求預測(2025-2031年) LED攝影機照明市場按產品類型、應用、最終用戶、分銷管道和照明類型分類-2025-2032年全球預測LED照明市場按產品類型、應用、最終用戶、分銷管道、安裝方式和技術分類-2025-2032年全球預測智慧 LED 照明市場(按產品類型、安裝類型、連接通訊協定、應用和最終用戶分類)—2025 年至 2032 年全球預測

LED攝影機照明市場按產品類型、應用、最終用戶、分銷管道和照明類型分類-2025-2032年全球預測LED照明市場按產品類型、應用、最終用戶、分銷管道、安裝方式和技術分類-2025-2032年全球預測智慧 LED 照明市場(按產品類型、安裝類型、連接通訊協定、應用和最終用戶分類)—2025 年至 2032 年全球預測 2025年LED(發光二極體)霓虹燈全球市場報告2025年雙色發光二極體(LED)環形燈全球市場報告

2025年LED(發光二極體)霓虹燈全球市場報告2025年雙色發光二極體(LED)環形燈全球市場報告 全球LEDBrick燈市場

全球LEDBrick燈市場

▼