|

市場調查報告書

商品編碼

1640435

數位物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Digital Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

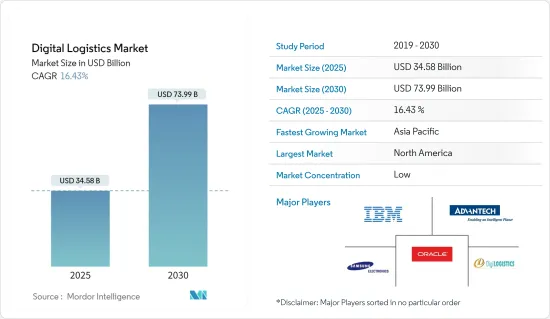

2025 年數位物流市場規模預估為 345.8 億美元,預計到 2030 年將達到 739.9 億美元,預測期內(2025-2030 年)的複合年成長率為 16.43%。

主要亮點

- 這一成長是由物流業日益採用先進技術所推動的。此外,這些數位解決方案正在幫助物流公司降低所產生的成本。物流和技術的整合、覆蓋整個供應鏈的雲端基礎的協作解決方案、倉儲、運輸和最終消費者資訊的緊密整合以及整個供應鏈的透明度正在推動所研究市場的成長。

- 數位市場的技術進步和雲端運算的不斷普及預計將推動對數位物流解決方案的需求。例如,去年四月,Locus 和 loconav 宣佈建立策略夥伴關係。 loconav 和 Locus 之間的合作將透過自動化供應鏈流程加速物流產業的數位轉型。

- 由於 COVID-19 疫情爆發,政府採取多項封鎖措施,導致許多產業的供應鏈和物流面臨嚴重中斷。為了滿足這些必要的交付,公司正在利用數位物流平台轉變其供應鏈能力。根據《物流新聞》報道,使用人工智慧並支援數位付款的數位供應鏈是解決新冠疫情等緊急情況的解決方案。

- 在過去的十幾年中,由於網路購物和網路用戶的發展,電子商務公司經歷了巨大的成長。電子商務的興起產生了對更快、更有效率的運輸供應商的需求。在網上購物時,客戶期望準確的訂購、快速的運送和快速的退貨流程。企業正在尋找降低訂單交付成本和縮短交貨時間的方法。電子商務正在推動可見性、成本、易用性、交付速度和無憂退貨等因素。必須開發新模型和新技術來滿足這一需求,包括物流路線自動化、物流規劃數位化和物料運輸自動化。因此,履約服務變得更快、更多樣化,特別是在最後一英里的交付和退款方面。

數位物流市場趨勢

倉庫管理系統 (WMS) 領域預計將佔據很大佔有率。

- 數位市場的技術進步和雲端運算的不斷普及預計將推動對數位物流解決方案的需求。例如,京東和中石化宣布計劃在數位供應鏈模式上建立廣泛的夥伴關係。 2022年3月,中國石化安徽分公司與京東簽署夥伴關係協議,以多項供應鏈服務合作,推動全通路營運。該協議涵蓋產品和數位供應鏈、共用倉儲設施和智慧物流。京東將發揮技術與供應鏈服務優勢,協助安徽中化集團提高生產效率、降低成本。

- 此外,物流領域產品創新的不斷增加也顯著提高了市場成長率。例如,2022 年 6 月,Semtech 宣布推出其 LoRa Cloud Locator 服務,該服務測試 LoRa Edge 的超低功耗資產追蹤功能。 Semtech 的 LoRa Edge 技術透過在雲端基礎的求解器中而不是在設備本身上解決資產位置,顯著降低了功耗。因此,設備的電池壽命可長達 10 年或更長。 LoRa Edge LR系列晶片使用GNSS和Wi-Fi在室內或室外的任何地方掃描設備的經緯度。結合 LoRa 無線傳輸到 Semtech 的雲端,無論您的資產位於何處,您都可以獲得持續覆蓋。

- 感測器和物聯網分析的市場吸引力有望吸引物流供應商投資數位解決方案。物流中的物聯網簡化了產品儲存並實現了高效率的倉庫管理。此外,現代技術使重新思考倉庫業務變得更加簡單。 RFID 標籤和感測器可以監控庫存的狀態和位置。實施倉庫自動化也有助於最大限度地減少人為錯誤,因為流程在需要時才會啟動和使用。

亞太地區可望創下最快成長

- 由於中國和印度等國家採用了數位技術,亞太地區在預測期間的成長速度最高。物聯網、人工智慧和雲端運算等技術進步進一步促進了市場成長。

- 儘管面臨包括新冠疫情在內的諸多障礙,中國物流業仍在採用數位技術來提高效率。 2022年4月,中共中央、國務院聯合發布加速形成國內統一市場的指示。 《意見》指出,中國將最佳化商貿流通基礎設施設計,鼓勵線上線下融合發展。

- 此舉措符合國家政府鼓勵發展第三方物流配送數位平台和培育一系列具有全球影響力的供應鏈業務的承諾。例如,中國卡車叫車公司滿幫物流正在加強利用數位技術提高疫情地區的物流效率。

- 此外,印度的國家物流政策可望透過降低物流成本和提高國產商品在全球市場的競爭力,為該國的經濟發展創造無縫銜接的進程。如此高的物流成本已經使印度製造的產品在國際市場上銷售處於不利地位。印度製造商急需的轉變可能伴隨著全面的政策審查,這將使他們能夠在國際市場上具有競爭力的價格。統一物流介面平台、數位化系統整合、物流簡化和系統改進群是新物流計劃的四大主要部分。 「印度製造」、「數位印度」和「Atma-nirbhara 驅動」等政策的成功實施將從國家物流政策中獲得另一個組成部分。

數位物流行業概覽

數位物流市場較為分散,因為有許多參與者為從中小企業到大型企業等各種類型的組織提供服務。市場的主要企業包括 IBM 公司、研華公司和三星電子。主要市場發展包括:

- 2023 年 11 月,Suttons International 與 LogChain 建立數位化夥伴關係。這項合作是在 LogChain 最近成功促成全球首筆全數位化跨境貨運之後達成的,這提高了物流業的數位透明度和擴充性。薩頓國際 (Sutton International) 已將該平台作為其數位轉型歷程中的重要組成部分。該平台的採用彰顯了薩頓致力於引領業界數位創新的重要一步。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 競爭對手之間的競爭

- 替代品的威脅

第5章 市場動態

- 市場促進因素

- 數位科技的出現

- 電子商務產業的成長與多通路分銷網路的出現

- 雲端基礎應用程式的採用率不斷提高

- 市場限制

- 缺乏資訊通訊技術基礎設施和資料安全問題

- COVID-19 產業影響評估

第6章 市場細分

- 按類型

- 庫存管理

- 倉庫管理系統 (WMS)

- 車隊管理

- 其他類型

- 按最終用戶產業

- 車

- 製藥/生命科學

- 零售

- 飲食

- 石油和天然氣

- 其他最終用戶產業

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

第7章 競爭格局

- 公司簡介

- IBM Corporation

- Advantech Corporation

- Oracle Corporation

- Samsung Electronics Co. Ltd

- DigiLogistics Technology Ltd

- Hexaware Technologies Limited

- Tech Mahindra Limited

- JDA Software Pvt Ltd

- UTI Worldwide Inc.(DSV Group)

- SAP SE

- Manhattan Associates Inc.

- HighJump Software Inc.

- Vinculum Group

第8章投資分析

第9章:市場的未來

簡介目錄

Product Code: 52939

The Digital Logistics Market size is estimated at USD 34.58 billion in 2025, and is expected to reach USD 73.99 billion by 2030, at a CAGR of 16.43% during the forecast period (2025-2030).

Key Highlights

- Growth is driven owing to the increasing adoption of advanced technologies in the logistics sector. Moreover, these digital solutions are helping logistic companies in reducing incurred costs. Convergence of logistics and technology, along with cloud-based collaborative solutions that extend through the entire supply chain, tight integration of warehouse, transport, and end consumer information, and transparency through the supply chain are driving the growth of the market studied.

- The technological advancement in the digital market and rising cloud adoption are expected to fuel the demand for digital logistic solutions. For instance, in April last year, Locus and loconav announced a strategic cooperation. This partnership between loconav and Locus will promote digital transformation in the logistics sector by automating supply chain processes.

- With the outbreak of COVID-19, many industries have faced significant supply chain and logistic disruption owing to the lockdown imposed by various governments. Companies are transforming their supply chain capabilities with digital logistics platforms to meet those essential deliveries. According to Logistics News, digital supply chains using artificial intelligence and enabling digital payments are the solution to emergencies such as the Covid-19 pandemic.

- Over the past ten years, the e-commerce company has experienced tremendous growth due to the development of online shopping and Internet users. More rapid and efficient transportation providers are required due to the growth of e-commerce. When shopping online, customers expect accurate orders, prompt shipment, and return procedures. Businesses are looking for ways to reduce order shipping costs and timeframes. E-commerce is the driving force behind visibility, cost, ease of use, delivery speed, and hassle-free returns. New models and technologies must be created to accommodate this need by automating distribution routes, digitalizing logistics planning, and material movement. As a result, fulfillment services have become quicker and more varied, especially for last-mile delivery and refunds.

Digital Logistics Market Trends

Warehouse Management System (WMS) segment is expected to acquire major share.

- The technological advancement in the digital market and rising cloud adoption are expected to fuel the demand for digital logistic solutions. For instance, JD and Sinopec announced a plan to build a broad partnership with their digital supply chain model. In March 2022, Sinopec's Anhui province branch and JD.com signed a partnership agreement under which they will collaborate on a number of supply chain services and advance omnichannel operations. The agreement encompasses product and digital supply chains, sharing warehouse facilities, and smart logistics. JD will use its technology and supply chain services advantages to assist Sinopec Anhui in boosting productivity and cutting costs.

- Further, the growing product innovations in the logistics sector are significantly boosting the market growth rate. For instance, in June 2022, Semtech introduced the LoRa Cloud Locator Service to test the LoRa Edge's ultra-low power asset tracking capabilities. By solving the asset's position in a Cloud-based solver rather than on the device itself, Semtech'sLoRa Edge technology considerably lowers power usage. As a result, the device's battery life can last up to or even longer than ten years. The LoRa Edge LR-series chips use GNSS and Wi-Fi to scan for a device's latitude and longitude in any interior or outdoor location. Regardless of where assets are located, continuous coverage is obtained when combined with Semtech'sLoRa radio transmission to the Cloud.

- Advancements in the sensors and IoT analytics market are expected to attract logistics vendors, to invest in digital solutions. IoT in logistics can simplify storing products and ensure efficient warehouse management. Additionally, modern technology has made it much simpler to overhaul warehouse operations. RFID tags and sensors can monitor the status and location of the inventory items. Executing warehouse automation can also minimize human errors because the processes are enabled and used as needed.

Asia Pacific is Expected to Register the Fastest Growth Rate

- Asia-pacific is analyzed to grow at the highest growth rate during the forecast period owing to the adoption of digital technologies in countries such as China, India, and so on. Technological advancements such as IoT, AI, and Cloud further contribute to market growth.

- China's logistics sector is embracing digital technologies to increase efficiency in the face of numerous obstacles, including the COVID-19 pandemic. A directive on accelerating the creation of a unified domestic market was jointly published in April 2022 by the Communist Party of China Central Committee and the State Council. It stated that China would optimize the design of the infrastructure for commerce and trade circulation and encourage the fusion of online and offline development.

- The initiatives are in accordance with the central government's commitment to encourage the development of digital platforms for third-party logistics delivery and to foster a number of supply chain businesses with a global reach. For instance, Full Truck Alliance Co Ltd, a Chinese truck-hailing business, is boosting efforts to use digital technology to improve logistical effectiveness in pandemic-affected areas.

- Further, India's national logistics policy is anticipated to create a seamless course for economic development in the country by lowering logistic costs and enhancing the competitiveness of domestic goods on the global market. Due to these high logistical expenses, domestic commodities produced in India that are sold on the international market are already at a disadvantage. The shift that Indian manufacturers have been yearning for will be brought about by a comprehensive policy overhaul, allowing them to set competitive prices for their goods on the international market. Unified Logistics Interface Platform, Integration of Digital System, Ease of Logistics, and System Improvement Group are the four main parts of this new logistical project. The successful policy execution of Make in India, Digital India, and the "Atma-nirbhara drive" throughout the nation gains another component from the national logistics policy.

Digital Logistics Industry Overview

The Digital Logistics Market is fragmented due to the presence of a large number of players which cater to various types of organizations, such as SMEs to Large Enterprises. Some key players in the market are IBM Corporation, Advantech Corporation, and Samsung Electronics Co. Ltd., among others. Some key developments in the market are:

- November 2023, Suttons International and LogChain have started a digitalization partnership. This collaboration, coming from LogChain's recent success in facilitating the world's first fully digitalized cross-border shipment, symbolizes a mutual commitment to bolstering digital transparency and scalability in the logistics sector. Suttons International is integrating its platform as a pivotal component in its digital transformation journey. The platform's adoption underscores a significant step in Suttons' commitment to spearheading digital innovation within the industry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Emergence Of Digital Technology

- 5.1.2 Growth In E-Commerce Industry And Emergence Of Multichannel Distribution Networks

- 5.1.3 Growing Adoption Of Cloud Based Applications

- 5.2 Market Restraints

- 5.2.1 Lack of ICT Infrastructure and Data Security Concerns

- 5.3 Assessment of Impact of COVID-19 on the Industry

6 MARKET SEGMENTATION

- 6.1 Type

- 6.1.1 Inventory Management

- 6.1.2 Warehouse Management System (WMS)

- 6.1.3 Fleet Management

- 6.1.4 Other Types

- 6.2 End-user Vertical

- 6.2.1 Automotive

- 6.2.2 Pharmaceutical / Life Sciences

- 6.2.3 Retail

- 6.2.4 Food and Beverage

- 6.2.5 Oil and Gas

- 6.2.6 Other End-user Verticals

- 6.3 Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle-East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Advantech Corporation

- 7.1.3 Oracle Corporation

- 7.1.4 Samsung Electronics Co. Ltd

- 7.1.5 DigiLogistics Technology Ltd

- 7.1.6 Hexaware Technologies Limited

- 7.1.7 Tech Mahindra Limited

- 7.1.8 JDA Software Pvt Ltd

- 7.1.9 UTI Worldwide Inc.(DSV Group)

- 7.1.10 SAP SE

- 7.1.11 Manhattan Associates Inc.

- 7.1.12 HighJump Software Inc.

- 7.1.13 Vinculum Group

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

02-2729-4219

+886-2-2729-4219

數位物流市場按組件、解決方案類型、部署模式、公司規模和最終用戶產業分類-2025-2032 年全球預測

數位物流市場按組件、解決方案類型、部署模式、公司規模和最終用戶產業分類-2025-2032 年全球預測 按行業和地區分類的數位物流市場2032 年數位物流市場預測:按組件、部署類型、組織規模、技術、應用、最終用戶和地區進行的全球分析

按行業和地區分類的數位物流市場2032 年數位物流市場預測:按組件、部署類型、組織規模、技術、應用、最終用戶和地區進行的全球分析 2025 年數位物流全球市場報告

2025 年數位物流全球市場報告 數位物流的全球市場的評估:各解決方案,各用途,各部署方式,各終端用戶,各地區,機會,預測(2018年~2032年)

數位物流的全球市場的評估:各解決方案,各用途,各部署方式,各終端用戶,各地區,機會,預測(2018年~2032年) 全球數位物流市場規模、佔有率和趨勢分析報告(按部署模式、解決方案、應用、最終用戶、區域展望和預測,2024-2031)

全球數位物流市場規模、佔有率和趨勢分析報告(按部署模式、解決方案、應用、最終用戶、區域展望和預測,2024-2031) 數位物流市場規模、佔有率、趨勢分析報告:按組件、按部署、按應用、按最終用途、按地區、細分市場預測,2024-2030 年物流市場網路安全、機會、成長動力、產業趨勢分析與預測,2024-2032數位物流市場規模 - 按組成部分、按功能、按組織規模、按部署模式、按垂直行業和預測,2024 年至 2032 年

數位物流市場規模、佔有率、趨勢分析報告:按組件、按部署、按應用、按最終用途、按地區、細分市場預測,2024-2030 年物流市場網路安全、機會、成長動力、產業趨勢分析與預測,2024-2032數位物流市場規模 - 按組成部分、按功能、按組織規模、按部署模式、按垂直行業和預測,2024 年至 2032 年 2023-2030 年全球數位物流市場規模研究與預測(依解決方案、應用、部署模式、最終用戶和區域分析)

2023-2030 年全球數位物流市場規模研究與預測(依解決方案、應用、部署模式、最終用戶和區域分析)

▼