|

市場調查報告書

商品編碼

2071361

人體膠帶市場商機、成長要素、產業趨勢分析及2026-2035年預測Body Tape Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

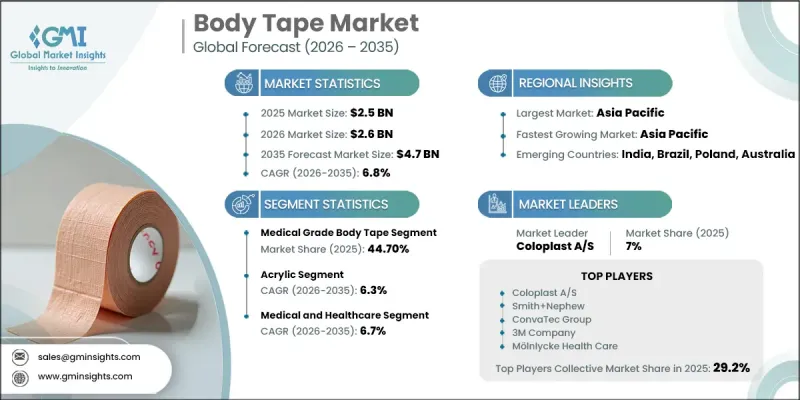

全球塑身膠帶市場預計到 2025 年將達到 25 億美元,年複合成長率為 6.8%,到 2035 年將達到 47 億美元。

市場擴張的驅動力在於對功能性黏合劑解決方案日益成長的需求,這些解決方案能夠在臨床和消費領域提供支撐、固定和提升美觀度的功能。醫療產業仍然是需求的主要驅動力,這得益於北美和亞太地區對醫療基礎設施的持續投資,以及醫院、復健機構和居家照護服務機構強勁的採購模式。同時,黏合劑化學的進步正在重新定義產品性能標準,並逐漸轉向矽基配方,與傳統的丙烯酸產品相比,矽基配方具有更好的皮膚親和性,刺激性更小。消費者對人體膠帶在美容和時尚領域的接受度不斷提高,也推動了市場成長,人體膠帶擴大用於服裝加固和造型。數位商務的快速發展和社交媒體主導的美容潮流顯著縮短了產品的接受週期,使人體膠帶從小眾應用走向主流產品。材料創新的進步、新興經濟體地理滲透率的提高以及與線上零售生態系統的日益融合,都為全球各地市場的長期成長潛力做出了貢獻。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 25億美元 |

| 預測金額 | 47億美元 |

| 複合年成長率 | 6.8% |

預計到2035年,醫用膠帶市佔率將達到44.70%,複合年成長率(CAGR)為7%。此細分市場的主導地位得益於與臨床採購系統的緊密合作,醫院、長期護理機構、復健中心和居家醫療提供者優先選擇經過認證和皮膚病學測試的黏合劑解決方案。監理合規要求和標準化採購架構也持續推動該品類的穩定需求。

預計到2035年,丙烯酸黏合劑市場佔有率將達到32.90%,複合年成長率(CAGR)為6.3%。其市場主導地位主要歸功於其成本效益、廣泛的生產管道和成熟的供應鏈網路,而非其作為高階性能產品的定位。丙烯酸配方廣泛應用於中階和成本績效導向產品,尤其在價格敏感型市場中備受歡迎,因為在這些市場中,價格因素在購買決策中起著至關重要的作用。這些材料具有可調節的黏合強度和柔軟性,使其適用於從通用時尚應用到基礎醫療固定應用等各種用途。

預計到2025年,北美醫用膠帶市佔率將達到31%。這得益於北美完善的醫療採購體係以及時尚和個人護理領域的強勁消費需求。美國仍然是該地區需求的主要驅動力,這得益於其系統化的法規核准體系,該體系規範了醫用黏合劑產品並製定了影響全球產品開發和創新趨勢的性能標準。

目錄

第1章:調查方法

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 前景

- 製造商

- 中斷

- 供應商情況

- 主要新聞和舉措

- 技術與創新展望

- 監理情勢

- 影響因素

- 促進因素

- 產業潛在風險與挑戰

- 機會

- 2025年價格分析

- 2022-2025年歷史價格趨勢分析

- 依球員類型分類的定價策略(高級球員、超值球員、成本加成球員)

- 區域價格波動分析

- 成長潛力分析

- 波特的分析

- PESTLE分析

- 消費者購買行為分析

- 人口趨勢

- 影響購買決策的因素

- 消費者產品採納

- 首選分銷管道

- 貿易數據分析

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 出口目的地分析

- 原物料進口來源分析

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 按細分市場分類的生成式人工智慧用例和部署藍圖

- 風險、限制和監管考量

- 生產能力和生產情況

- 設備產能:按地區和主要生產商分類

- 運轉率和擴張計劃

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

- 主要市場公司的競爭分析

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 主要趨勢

- 醫用膠帶

- 雙面膠帶

- 單面人體膠帶

第6章 市場估計與預測:依材料分類,2022-2035年

- 主要趨勢

- 丙烯酸纖維

- 矽酮

- 棉布

- 合成

- 其他

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 主要趨勢

- 醫療保健

- 時尚與服裝

- 化妝品和美容

- 其他

第8章 市場估計與預測:依價格分類,2022-2035年

- 主要趨勢

- 低的

- 中等的

- 高的

第9章 市場估價與預測:依最終用戶分類,2022-2035年

- 主要趨勢

- 個人

- 商業

第10章 市場估價與預測:依通路分類,2022-2035年

- 主要趨勢

- 線上

- 電子商務網站

- 企業網站

- 離線

- 專賣店

- 其他

第11章及預測:區域細分,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- UAE

- 沙烏地阿拉伯

- 南非

第12章:公司簡介

- 世界公司

- 3M

- Avery Dennison

- Nitto Denko

- Berry Global

- Coloplast A/S

- Smith+Nephew

- Molnlycke Health Care

- ConvaTec Group

- Scapa Group

- 當地公司

- Adhex Technologies

- DermaMed Coatings

- Kinesio

- Fashion Forms

- Hollywood Fashion Secrets

- 新興企業

- Booby Tape

- Brazabra Corp

- Fearless Tape

- EasyTape

- Maidenform

The Global Body Tape Market was valued at USD 2.5 billion in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 4.7 billion by 2035.

Market expansion is driven by increasing demand for functional adhesive solutions that provide support, fixation, and aesthetic enhancement across both clinical and consumer environments. The medical segment remains the core demand driver due to strong institutional purchasing patterns across hospitals, rehabilitation facilities, and home-based care services, supported by ongoing investments in healthcare infrastructure across North America and Asia Pacific. At the same time, advancements in adhesive chemistry are reshaping product performance standards, with a gradual shift toward silicone-based formulations that offer improved skin compatibility and reduced irritation compared to traditional acrylic-based options. The market is also benefiting from growing consumer acceptance of body tape in beauty and fashion applications, where it is increasingly used for garment support and styling purposes. The rapid rise of digital commerce and social media-driven beauty trends has significantly shortened product adoption cycles, enabling body tape to transition from niche usage to mainstream acceptance. Increasing material innovation, expanding geographic penetration in emerging economies, and rising integration into online retail ecosystems collectively support long-term market growth potential across global regions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.5 Billion |

| Forecast Value | $4.7 Billion |

| CAGR | 6.8% |

The medical-grade body tape segment is projected to hold a 44.70% share by 2035 and is expected to grow at a CAGR of 7%. This segment's leadership is driven by its strong alignment with clinical procurement systems, where hospitals, long-term care institutions, rehabilitation centers, and home healthcare providers prioritize certified and dermatologically tested adhesive solutions. Regulatory compliance requirements and standardized purchasing frameworks continue to reinforce demand stability within this category.

The acrylic-based adhesives segment is expected to hold 32.90% share by 2035, growing at a CAGR of 6.3%. This dominance is primarily attributed to cost efficiency, widespread manufacturing availability, and established supply chain networks rather than premium performance positioning. Acrylic formulations are widely used across mid-range and value-oriented products, particularly in cost-sensitive markets where affordability plays a critical role in purchasing decisions. These materials provide adaptable adhesion strength and flexibility characteristics suitable for a wide range of applications, including general-purpose fashion and basic medical fixation uses.

North America Body Tape Market accounted for a 31% share in 2025, supported by a well-developed healthcare procurement ecosystem and strong consumer demand across fashion and personal care segments. The United States remains the primary contributor to regional demand, backed by structured regulatory approval systems that govern medical-grade adhesive products and establish performance standards influencing global product development and innovation trends.

Key companies operating in the Global Body Tape Market include Smith+Nephew, 3M Company, Coloplast A/S, ConvaTec Group plc, and Smith+Nephew. Companies in the body tape market are actively focusing on product innovation, material advancement, and expansion of application-specific portfolios to strengthen their competitive position. Leading players are investing in silicone-based adhesive technologies to enhance skin compatibility, reduce irritation risks, and improve product performance across medical and cosmetic uses. Strategic collaborations with healthcare providers, beauty brands, and retail distributors are enabling wider market penetration and improved product accessibility. Manufacturers are also expanding into emerging economies where rising healthcare infrastructure and increasing consumer awareness are driving new demand opportunities. Digital marketing strategies and influencer-led promotional campaigns are accelerating adoption in the fashion and beauty segment by improving product visibility and consumer engagement. Additionally, companies are strengthening supply chain integration and manufacturing scalability to maintain cost efficiency while supporting rising global demand.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Material

- 2.2.4 Application

- 2.2.5 Price

- 2.2.6 End User

- 2.2.7 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Key news & initiatives

- 3.4 Technology & Innovation Landscape

- 3.5 Regulatory landscape

- 3.6 Impact on forces

- 3.6.1 Growth drivers

- 3.6.2 Industry pitfalls & challenges

- 3.6.3 Opportunities

- 3.7 Pricing analysis, 2025 (driven by primary research)

- 3.7.1 Historical price trend analysis (2022-2025)

- 3.7.2 Pricing strategy by player type (premium/value/cost-plus)

- 3.7.3 Regional price variation analysis

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Consumer buying behavior analysis

- 3.11.1 Demographic trends

- 3.11.2 Factors affecting buying decisions

- 3.11.3 Consumer product adoption

- 3.11.4 Preferred distribution channel

- 3.12 Trade data analysis (driven by paid database)

- 3.12.1 Import/export volume & value trends (Driven by Primary Research)

- 3.12.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.12.3 Export destination analysis

- 3.12.4 Import source analysis for raw materials

- 3.13 Impact of AI & generative AI on the market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Capacity & Production Landscape (Driven by Primary Research)

- 3.14.1 Installed Capacity by Region & Key Producer (Driven by Primary Research)

- 3.14.2 Capacity Utilization Rates & Expansion Pipelines (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022-2035 (USD Million) (Million Units)

- 5.1 Key Trends

- 5.2 Medical-grade Body Tape

- 5.3 Double-sided Body Tape

- 5.4 Single-sided Body Tape

Chapter 6 Market Estimates & Forecast, By Material, 2022-2035 (USD Million) (Million Units)

- 6.1 Key Trends

- 6.2 Acrylic

- 6.3 Silicone

- 6.4 Cotton

- 6.5 Synthetic

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Application, 2022-2035 (USD Million) (Million Units)

- 7.1 Key Trends

- 7.2 Medical & Healthcare

- 7.3 Fashion & Apparel

- 7.4 Cosmetics & Beauty

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Price, 2022 - 2035, (USD Million) (Million Units)

- 8.1 Key Trends

- 8.2 Low

- 8.3 Medium

- 8.4 High

Chapter 9 Market Estimates & Forecast, By End User, 2022 - 2035, (USD Million) (Million Units)

- 9.1 Key Trends

- 9.2 Individual

- 9.3 Commercial

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Million) (Million Units)

- 10.1 Key Trends

- 10.2 Online

- 10.2.1 E-commerce site

- 10.2.2 Company website

- 10.3 Offline

- 10.3.1 Specialty stores

- 10.3.2 Others

Chapter 11 & Forecast, By Region, 2022 - 2035, (USD Million) (Million Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 U.K.

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 Saudi Arabia

- 11.6.3 South Africa

Chapter 12 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 12.1 Global players

- 12.1.1 3M

- 12.1.2 Avery Dennison

- 12.1.3 Nitto Denko

- 12.1.4 Berry Global

- 12.1.5 Coloplast A/S

- 12.1.6 Smith+Nephew

- 12.1.7 Molnlycke Health Care

- 12.1.8 ConvaTec Group

- 12.1.9 Scapa Group

- 12.2 Regional players

- 12.2.1 Adhex Technologies

- 12.2.2 DermaMed Coatings

- 12.2.3 Kinesio

- 12.2.4 Fashion Forms

- 12.2.5 Hollywood Fashion Secrets

- 12.3 Emerging players

- 12.3.1 Booby Tape

- 12.3.2 Brazabra Corp

- 12.3.3 Fearless Tape

- 12.3.4 EasyTape

- 12.3.5 Maidenform

全球膠帶市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球膠帶市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 膠帶市場:2026-2032年全球市場預測(依樹脂類型、功能、基材、厚度、黏合方式、形狀、應用和通路分類)

膠帶市場:2026-2032年全球市場預測(依樹脂類型、功能、基材、厚度、黏合方式、形狀、應用和通路分類) 膠帶市場規模、佔有率、趨勢和預測:按材料、樹脂、技術、應用和地區分類,2026-2034年

膠帶市場規模、佔有率、趨勢和預測:按材料、樹脂、技術、應用和地區分類,2026-2034年 膠帶市場分析及預測(至2035年):類型、產品類型、應用、材料類型、技術、最終用戶、形態、組件、功能、工藝日本膠帶市場規模、佔有率、趨勢及預測(依材料、樹脂、技術、應用及地區分類),2026-2034年

膠帶市場分析及預測(至2035年):類型、產品類型、應用、材料類型、技術、最終用戶、形態、組件、功能、工藝日本膠帶市場規模、佔有率、趨勢及預測(依材料、樹脂、技術、應用及地區分類),2026-2034年 2026年全球膠帶市場報告

2026年全球膠帶市場報告 膠帶市場規模、佔有率和趨勢分析報告:按樹脂類型、最終用途、地區和細分市場預測(2026-2033 年)電動汽車電池膠帶市場按膠帶類型、黏合劑類型、電池化學成分、基材、應用和最終用途分類-2026-2032年全球預測

膠帶市場規模、佔有率和趨勢分析報告:按樹脂類型、最終用途、地區和細分市場預測(2026-2033 年)電動汽車電池膠帶市場按膠帶類型、黏合劑類型、電池化學成分、基材、應用和最終用途分類-2026-2032年全球預測 膠帶市場規模、佔有率和成長分析(按類型、黏合技術、樹脂、材料、終端用途產業和地區分類)—產業預測(2026-2033 年)

膠帶市場規模、佔有率和成長分析(按類型、黏合技術、樹脂、材料、終端用途產業和地區分類)—產業預測(2026-2033 年) 膠帶:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)

膠帶:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)