|

市場調查報告書

商品編碼

2071222

城市空中交通市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測Urban Air Mobility (UAM) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

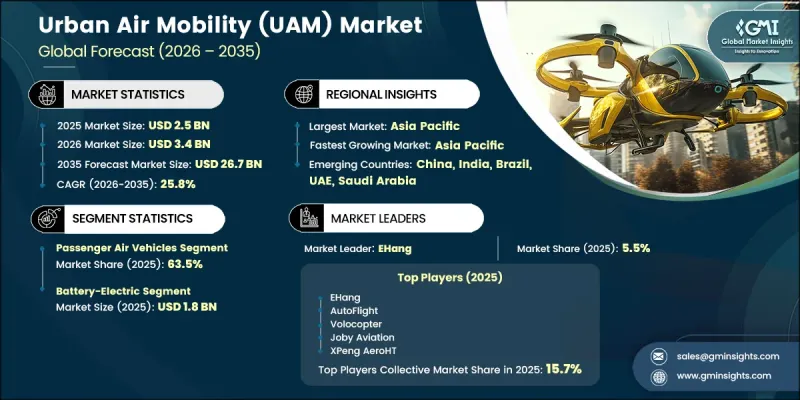

全球城市航空運輸市場預計到 2025 年將達到 25 億美元,並以 25.8% 的複合年成長率成長,到 2035 年將達到 267 億美元。

先進航空運輸解決方案的快速發展為城市航空運輸業創造了巨大的成長機會。在交通擁擠嚴重的大都會圈,人們對更快捷交通途徑的需求日益成長,推動了旨在提高出行效率和縮短出行時間的創新空中運輸平台的普及。下一代航空技術的進步,以及相應的法律規範,正在加速商業化進程。產業相關人員加大投資和建立策略合作夥伴關係,透過支持技術成熟和營運準備,進一步加強了市場發展。此外,業界也受益於對永續交通解決方案和減少環境影響的日益重視,從而促進了更清潔出行技術的應用。隨著城市交通系統的不斷發展,相關人員正增加對基礎設施、車輛研發和生態系統整合的投資,以支持長期的商業化。預計在整個預測期內,技術創新、有利的政策支援以及對高效出行服務日益成長的需求將推動全球城市航空運輸市場持續成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 25億美元 |

| 預計金額 | 267億美元 |

| 複合年成長率 | 25.8% |

隨著都市區交通擁擠日益嚴重,城市交通網路壓力不斷增大,人們對替代出行解決方案的需求也日益成長,城市空中運輸市場因此蓬勃發展。持續完善的基礎設施為大規模部署先進空中交通服務提供了有力支撐,也推動了市場擴張。對營運生態系統的持續投入正在加速從研發到商業化的進程。航太公司、技術供應商、基礎設施開發商和監管相關人員之間的合作,正在加速技術進步,提高部署效率,並增強人們對新興旅遊平台的信心。不斷增加的資本投資和行業範圍內的夥伴關係,在支持城市空中交通業務擴張和市場長期成長方面繼續發揮著至關重要的作用。基礎設施建設仍然是影響該行業發展的最重要趨勢之一,因為專用設施和支援網路對於將空中交通服務整合到更廣泛的交通系統中至關重要。預計未來幾年,這種運力擴張將提高營運效率,並促進空中交通服務的更廣泛應用。

到2025年,客運飛機市佔率將達到63.5%。在都市區,人們對更有效率的出行方式的需求日益成長,以應對日益嚴峻的交通挑戰,而對先進客運解決方案的強勁需求也持續推動著該領域的成長。客運飛機因其有望提高運輸效率、縮短旅行時間而備受營運商和公共機構的關注。隨著互聯互通交通網路的不斷完善以及對商業客運運營的日益重視,客運飛機在市場上的主導地位將進一步鞏固。

預計2026年至2035年間,氫燃料電池市場將以29%的複合年成長率成長。該市場成長的主要驅動力在於,與其他推進技術相比,氫燃料電池具有更高的能源效率和更長的續航里程。氫燃料電池系統適用於多種交通運輸應用,因為它們能夠延長運行時間並承載負載容量。人們對清潔能源技術和永續航空解決方案日益成長的興趣進一步加速了氫燃料電池技術的應用,而氫燃料電池正逐漸成為不斷發展的城市空中交通領域的關鍵技術之一。

到2025年,北美城市空中交通市場將佔據36.5%的市場。這一成長得益於成熟的航太創新企業以及先進空中交通平台商業部署的持續進展。持續的測試、認證進度以及對航空安全要求的遵守,正在加速從研發到營運的過渡。此外,政府的大力支持和致力於推動空中運輸舉措的合作努力也為市場帶來了益處。監管指南、基礎設施規劃和空域管理項目正在為商業化鋪平道路,進一步鞏固北美作為城市空中交通技術領先市場的地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 都市區擁塞日益嚴重,對更快捷的交通途徑。

- eVTOL和自主輕型飛行器技術的進步

- 擴大政府支持並改善監管

- 增加投資和策略夥伴關係

- 人們對永續和低排放的交通途徑越來越感興趣。

- 產業潛在風險與挑戰

- 高昂的基礎設施建設和營運成本

- 監管的不確定性和空域一體化的複雜性

- 市場機遇

- 在物流和緊急服務領域的實施

- 擴大城際和區域間空中運輸服務

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特的分析

- PESTLE分析

- 技術與創新展望

- 最新科技趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 市場集中度分析

- 主要公司的競爭標竿分析

- 財務績效比較

- 收入

- 利潤率

- R&D

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係和聯盟

- 技術進步

- 擴張和投資策略

- 數位轉型計劃

- 新興企業競爭公司和新創企業的趨勢

第5章 市場估算與預測:依平台類型分類,2022-2035年

- 客機

- 空中計程車

- 空中接駁

- 個人飛機

- 貨運飛機

- 最後一公里配送車輛

- 大型貨運無人機

- 特種車輛

- 空中救護

- 緊急/災難支援

第6章 市場估計與預測:依驅動類型分類,2022-2035年

- 電池供電

- 油電混合

- 氫燃料電池

第7章 市場估計與預測:依營運模式分類,2022-2035年

- 載人操作

- 半自動/遠端監控操作

- 完全自動駕駛

第8章 市場估計與預測:依投資範圍分類,2022-2035年

- 短程(0-50公里)

- 中等距離(50-150公里)

- 長途(150-300公里)

第9章 市場估價與預測:依最終用戶分類,2022-2035年

- 商業出行業者

- 物流運營商

- 醫療機構及急救服務

- 私人/企業營運商

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第11章:公司簡介

- 全球主要公司

- EHang

- AutoFlight

- Volocopter

- Joby Aviation

- XPeng AeroHT

- 該地區的主要公司

- 北美洲

- Wisk Aero

- Archer Aviation

- Beta Technologies

- Electra.aero

- Overair

- Elroy Air

- Doroni Aerospace

- Jump Aero

- Natilus

- 亞太地區

- SkyDrive

- TCab Tech

- Volant Aerotech

- 歐洲

- Vertical Aerospace

- Pipistrel

- Dronamics

- Middle East & Africa

- Apeleon

- Aergility

- 北美洲

The Global Urban Air Mobility Market was valued at USD 2.5 billion in 2025 and is estimated to grow at a CAGR of 25.8% to reach USD 26.7 billion by 2035.

The rapid evolution of advanced aerial transportation solutions is creating significant growth opportunities across the urban air mobility industry. Increasing demand for faster transportation alternatives in congested metropolitan areas is encouraging the adoption of innovative air mobility platforms designed to improve travel efficiency and reduce transit times. Advancements in next-generation aviation technologies, coupled with supportive regulatory frameworks, are accelerating the path toward commercial deployment. Growing financial investments and strategic collaborations among industry participants are further strengthening market development by supporting technology maturation and operational readiness. The industry is also benefiting from rising emphasis on sustainable transportation solutions and reduced environmental impact, encouraging the adoption of cleaner mobility technologies. As urban transportation systems continue to evolve, stakeholders are increasingly investing in infrastructure, vehicle development, and ecosystem integration initiatives that support long-term commercialization. The convergence of technological innovation, favorable policy support, and increasing demand for efficient mobility services is expected to drive sustained growth across the global urban air mobility market throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.5 Billion |

| Forecast Value | $26.7 Billion |

| CAGR | 25.8% |

The urban air mobility market is gaining momentum as rising traffic congestion and growing pressure on urban transportation networks increase demand for alternative mobility solutions. Market expansion is being supported by the ongoing development of the infrastructure required to enable large-scale deployment of advanced air transportation services. Continued investments in operational ecosystems are facilitating the transition from development stages to commercial implementation. Collaboration among aerospace companies, technology providers, infrastructure developers, and regulatory stakeholders is accelerating technology advancement, improving deployment efficiency, and strengthening confidence in emerging mobility platforms. Increasing capital investment and industry-wide partnerships continue to play a critical role in scaling urban air mobility operations and supporting long-term market growth. Infrastructure development remains one of the most influential trends shaping the industry, as dedicated facilities and supporting networks become essential for integrating air mobility services into broader transportation systems. The expansion of these capabilities is expected to enhance operational efficiency and support wider adoption over the coming years.

The passenger air vehicles segment held a 63.5% share in 2025. Strong demand for advanced passenger transportation solutions continues to drive growth within this segment as cities seek more efficient ways to address increasing mobility challenges. Passenger-focused air vehicles are receiving significant attention from operators and public authorities due to their potential to improve transportation efficiency and reduce travel times. Their growing incorporation into interconnected transportation networks and increasing focus on commercial passenger operations continue to strengthen the segment's leading market position.

The hydrogen fuel cell segment is projected to grow at a CAGR of 29% during 2026-2035. The segment's growth is being driven by its capability to deliver greater energy efficiency and extended operational range compared to alternative propulsion technologies. Hydrogen-based systems support longer-duration operations while accommodating increased payload requirements, making them well suited for a broader range of mobility applications. Growing interest in clean energy technologies and sustainable aviation solutions is further accelerating adoption, positioning hydrogen fuel cells as an important technology segment within the evolving urban air mobility landscape.

North America Urban Air Mobility Market accounted for 36.5% share in 2025. Regional growth is being supported by the presence of established aerospace innovators and ongoing progress toward the commercial deployment of advanced aerial transportation platforms. Continued testing activities, certification advancements, and alignment with aviation safety requirements are helping accelerate the transition from development to operational implementation. The market is also benefiting from strong governmental support and coordinated efforts focused on advancing air mobility initiatives. Regulatory guidance, infrastructure planning efforts, and airspace management programs are contributing to a more streamlined commercialization pathway, strengthening North America's position as a leading market for urban air mobility technologies.

Key companies operating in the Global Urban Air Mobility Market include Archer Aviation, Joby Aviation, Vertical Aerospace, EHang, Beta Technologies, Volocopter, Wisk Aero, AutoFlight, XPeng AeroHT, SkyDrive, and Electra.aero, Overair, Elroy Air, Dronamics, Pipistrel, TCab Tech, Volant Aerotech, Doroni Aerospace, Apeleon, Aergility, Natilus, and Jump Aero. Companies participating in the urban air mobility industry are pursuing a variety of strategic initiatives to strengthen their market position and expand their competitive advantage. Research and development investments remain a primary focus as manufacturers work to enhance aircraft performance, operational safety, energy efficiency, and commercial viability. Strategic collaborations with aerospace organizations, infrastructure developers, technology providers, and regulatory stakeholders are helping accelerate product development and market entry. Companies are also prioritizing certification milestones and operational readiness programs to support commercialization efforts. Expanding production capabilities, strengthening supply chain networks, and developing integrated mobility ecosystems are further supporting growth strategies. In addition, organizations are investing in advanced propulsion technologies, digital flight systems, and infrastructure partnerships to improve service scalability.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Platform type trends

- 2.2.2 Propulsion type trends

- 2.2.3 Operation mode trends

- 2.2.4 Operational range trends

- 2.2.5 End User trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing urban congestion and demand for faster transportation

- 3.2.1.2 Advancements in eVTOL and autonomous light technologies

- 3.2.1.3 Growing government support and regulatory development

- 3.2.1.4 Rising investments and strategic partnerships

- 3.2.1.5 Increasing focus on sustainable and low-emission transportation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High infrastructure development and operational costs

- 3.2.2.2 Regulatory uncertainty and airspace integration complexity

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption in logistics and emergency services

- 3.2.3.2 Expansion of inter-city and regional air mobility services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Platform Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Passenger air vehicles

- 5.2.1 Air taxis

- 5.2.2 Air shuttles

- 5.2.3 Personal air vehicles

- 5.3 Cargo air vehicles

- 5.3.1 Last-mile delivery vehicles

- 5.3.2 Heavy cargo UAVs

- 5.4 Specialized service vehicles

- 5.4.1 Air ambulance

- 5.4.2 Emergency/disaster support

Chapter 6 Market Estimates and Forecast, By Propulsion Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Battery-electric

- 6.3 Hybrid-electric

- 6.4 Hydrogen fuel cell

Chapter 7 Market Estimates and Forecast, By Operation Mode, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Piloted operations

- 7.3 Semi-autonomous / remotely supervised operations

- 7.4 Fully autonomous operations

Chapter 8 Market Estimates and Forecast, By Operational Range, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Short range (0-50km)

- 8.3 Medium range (50-150km)

- 8.4 Long range (150-300km)

Chapter 9 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Commercial mobility operators

- 9.3 Logistics operators

- 9.4 Medical & emergency agencies

- 9.5 Private/corporate operators

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 EHang

- 11.1.2 AutoFlight

- 11.1.3 Volocopter

- 11.1.4 Joby Aviation

- 11.1.5 XPeng AeroHT

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 Wisk Aero

- 11.2.1.2 Archer Aviation

- 11.2.1.3 Beta Technologies

- 11.2.1.4 Electra.aero

- 11.2.1.5 Overair

- 11.2.1.6 Elroy Air

- 11.2.1.7 Doroni Aerospace

- 11.2.1.8 Jump Aero

- 11.2.1.9 Natilus

- 11.2.2 Asia Pacific

- 11.2.2.1 SkyDrive

- 11.2.2.2 TCab Tech

- 11.2.2.3 Volant Aerotech

- 11.2.3 Europe

- 11.2.3.1 Vertical Aerospace

- 11.2.3.2 Pipistrel

- 11.2.3.3 Dronamics

- 11.2.4 Middle East & Africa

- 11.2.4.1 Apeleon

- 11.2.4.2 Aergility

- 11.2.1 North America

先進空中交通市場規模、佔有率和成長分析:按飛機類型、推進技術、應用、基礎設施配置和地區分類-2026-2033年產業預測

先進空中交通市場規模、佔有率和成長分析:按飛機類型、推進技術、應用、基礎設施配置和地區分類-2026-2033年產業預測 垂直起降場市場規模、佔有率和成長分析:按基礎設施類型、組件、應用、最終用戶、部署模式、電源和地區分類-2026-2033年產業預測

垂直起降場市場規模、佔有率和成長分析:按基礎設施類型、組件、應用、最終用戶、部署模式、電源和地區分類-2026-2033年產業預測 垂直起降場市場商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。

垂直起降場市場商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。 全球城市空中交通(UAM)市場(至2040年):產業趨勢與預測

全球城市空中交通(UAM)市場(至2040年):產業趨勢與預測 城市空中運輸市場:按車輛類型、推進系統、自主程度、基礎設施、應用和最終用戶分類-2026-2032年全球市場預測

城市空中運輸市場:按車輛類型、推進系統、自主程度、基礎設施、應用和最終用戶分類-2026-2032年全球市場預測 2026年全球城市航空運輸市場報告2026年全球垂直起降機場市場報告垂直起降場市場:按類型、基礎設施、位置、技術整合和應用分類-2026-2032年全球市場預測

2026年全球城市航空運輸市場報告2026年全球垂直起降機場市場報告垂直起降場市場:按類型、基礎設施、位置、技術整合和應用分類-2026-2032年全球市場預測 城市空中運輸市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

城市空中運輸市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 城市空中交通市場-全球產業規模、佔有率、趨勢、機會與預測:按車輛類型、應用、地區和競爭格局分類,2021-2031年

城市空中交通市場-全球產業規模、佔有率、趨勢、機會與預測:按車輛類型、應用、地區和競爭格局分類,2021-2031年