|

市場調查報告書

商品編碼

2071213

從 2026 年到 2035 年,採用玻璃基板的先進封裝市場的商業機會、成長要素、產業趨勢分析和預測。Glass Substrate Advanced Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

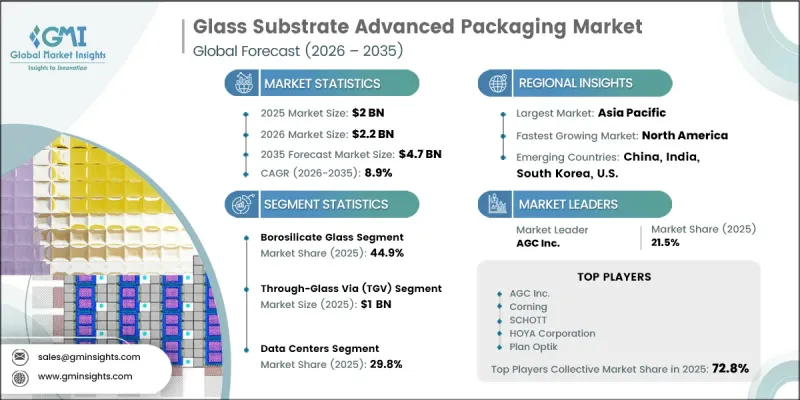

全球採用玻璃基板的先進封裝市場預計到 2025 年將達到 20 億美元,並以 8.9% 的複合年成長率成長,到 2035 年將達到 47 億美元。

先進封裝產業採用玻璃基板的成長主要得益於人工智慧 (AI) 和高效能運算領域對半導體解決方案日益成長的需求,以及晶片級架構和麵板級封裝技術的快速發展。下一代半導體裝置對高密度互連的需求不斷成長,進一步推動了市場擴張。人工智慧加速器和先進資料中心處理器的日益普及,為傳統基板技術帶來了巨大壓力,加速了向玻璃基板解決方案的轉型。玻璃基板之所以備受關注,是因為它能夠支援超細重線路重布,從而在緊湊型晶片設計中實現更高的電氣性能和佈線密度。對更高輸入/輸出密度、更優訊號完整性和可擴展封裝格式的需求不斷成長,也進一步推動了玻璃基板的應用。此外,生態系統的持續發展、中試規模生產的推進以及對克服有機基板材料局限性的日益重視,也為該行業帶來了積極影響。所有這些因素共同支撐了玻璃基板在先進封裝應用中的長期應用。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 20億美元 |

| 預計金額 | 47億美元 |

| 複合年成長率 | 8.9% |

到2025年,硼矽酸玻璃市佔率將達到44.9%。其優點在於兼具優異的熱穩定性、機械強度和成本效益。此外,它與現有半導體製造流程的兼容性也推動了其在大批量生產環境中的廣泛應用。這些特性使得硼矽酸玻璃成為尋求可靠且擴充性的先進封裝應用基板解決方案的製造商的理想選擇。

混合封裝(TGV 和 RDL 組合)市場預計將在 2026 年至 2035 年間以 12.6% 的複合年成長率成長。這一成長主要得益於市場對整合垂直互連結構和高解析度線路重布(RDL) 組合的需求不斷成長,這種組合能夠提升設計柔軟性並增強系統效能。混合封裝技術能夠實現更有效率的訊號佈線、更高的整合密度以及擴充性。在需要高互連性能和最佳化封裝效率的先進晶片設計中,混合封裝技術的應用正在迅速擴展。

到2025年,北美採用玻璃基板的先進封裝市場將佔據24.3%的市場。該地區正經歷強勁成長,這得益於半導體封裝基礎設施、研發設施和先進製造能力投資的增加。對國內半導體生產的日益重視以及人工智慧驅動晶片技術的創新,進一步增強了該地區的需求。先進封裝生態系的持續發展,在提升供應鏈韌性的同時,也加速了北美地區下一代基板技術的商業化進程。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 人工智慧和高效能運算需求的不斷成長,催生了對更高互連密度的需求。

- 玻璃基板能夠形成用於超細線條的線路重布。

- 與有機基板相比,具有更優異的熱穩定性

- 晶片組異質整合的日益普及

- 面板級封裝提高了大規模生產的成本效益。

- 產業潛在風險與挑戰

- 生態系發育不足及與有機基質的比較

- 搬運和生產過程中存在損壞風險

- 市場機遇

- 應用於下一代人工智慧加速器和資料中心晶片。

- 部署到汽車高效能運算系統

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特的分析

- PESTLE分析

- 技術與創新展望

- 最新科技趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 市場集中度分析

- 主要公司的競爭標竿分析

- 財務績效比較

- 收入

- 利潤率

- R&D

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係和聯盟

- 技術進步

- 擴張和投資策略

- 數位轉型計劃

- 新興企業競爭公司和新創企業的發展趨勢

第5章 市場估算與預測:依材料類型分類,2022-2035年

- 硼矽酸玻璃

- 鋁矽酸鹽玻璃

- 熔融石英/石英

- 特種工程玻璃

第6章 市場估算與預測:依封裝架構類型分類,2022-2035年

- 2.5D中介層封裝

- 3D-IC/晶片封裝

- 扇出型晶圓級封裝(FOWLP)

- 共封裝光學/光電裝置

第7章 市場估計與預測:依互連技術分類,2022-2035年

- 玻璃直通式(TGV)

- 重新分配層 (RDL)

- 混合型(TGV + RDL)

第8章 市場估算與預測:依最終用戶產業分類,2022-2035年

- 資料中心

- 電訊

- 家用電子產品

- 車

- 航太/國防

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第10章:公司簡介

- 全球主要公司

- AGC Inc.

- Corning

- SCHOTT

- HOYA Corporation

- Intel Corporation

- 該地區的主要公司

- 北美洲

- Mosaic Microsystems

- 亞太地區

- Absolics

- NEG(Nippon Electric Glass Co., Ltd.)

- Nippon Sheet Glass Co., Ltd.

- Ohara Inc.

- Shyawei Optronics(Taiwan)

- TOPPAN

- 歐洲

- AT&S(Austria Technologie & Systemtechnik)

- Plan Optik

- 北美洲

- 小眾玩家/顛覆者

- Avanstrate Inc.

The Global Glass Substrate Advanced Packaging Market was valued at USD 2 billion in 2025 and is estimated to grow at a CAGR of 8.9% to reach USD 4.7 billion by 2035.

Growth in the glass substrate advanced packaging industry is driven by accelerating demand for artificial intelligence and high-performance computing semiconductor solutions, alongside rapid advancements in chiplet-based architectures and panel-level packaging technologies. Increasing requirements for high-density interconnects in next-generation semiconductor devices are further strengthening market expansion. Rising deployment of AI accelerators and advanced data center processors is placing significant pressure on traditional substrate technologies, driving the transition toward glass-based solutions. Glass substrates are gaining traction due to their ability to support ultra-fine redistribution layers, enabling improved electrical performance and higher interconnect density in compact chip designs. The growing need for enhanced input/output density, superior signal integrity, and scalable packaging formats is further reinforcing adoption. Additionally, the industry is benefiting from ongoing ecosystem development, pilot-scale production efforts, and increasing focus on overcoming the limitations of organic substrate materials. These factors collectively support the long-term adoption of glass substrates in advanced semiconductor packaging applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2 Billion |

| Forecast Value | $4.7 Billion |

| CAGR | 8.9% |

The borosilicate glass segment held a 44.9% share in 2025. Its dominance is attributed to its strong balance of thermal stability, mechanical strength, and cost efficiency. The material's compatibility with established semiconductor manufacturing processes has further strengthened its adoption in high-volume production environments. These properties make borosilicate glass a preferred option for manufacturers seeking reliable and scalable substrate solutions for advanced electronic packaging applications.

The hybrid (TGV combined with RDL) segment is projected to grow at a CAGR of 12.6% during 2026-2035. This growth is driven by increasing demand for integrated vertical interconnect structures combined with high-resolution redistribution layers, enabling improved design flexibility and enhanced system performance. Hybrid packaging approaches support more efficient signal routing, improved integration density, and greater scalability for complex semiconductor architectures. Their adoption is expanding rapidly in advanced chip designs that require high interconnect performance and optimized packaging efficiency.

North America Glass Substrate Advanced Packaging Market accounted for 24.3% share in 2025. The region is witnessing strong growth supported by rising investments in semiconductor packaging infrastructure, research facilities, and advanced manufacturing capabilities. Expanding focus on domestic semiconductor production and innovation in AI-driven chip technologies is further strengthening regional demand. Continued development of advanced packaging ecosystems is enhancing supply chain resilience while accelerating the commercialization of next-generation substrate technologies across North America.

Key companies operating in the global glass substrate advanced packaging market include Corning, Intel Corporation, SCHOTT, AGC Inc., HOYA Corporation, AT&S (Austria Technologie & Systemtechnik), Nippon Sheet Glass Co., Ltd., Avanstrate Inc., NEG (Nippon Electric Glass Co., Ltd.), Absolics, Plan Optik, Ohara Inc., Mosaic Microsystems, TOPPAN, and Shyawei Optronics (Taiwan). Companies participating in the glass substrate advanced packaging industry are focusing on strategic initiatives aimed at strengthening technological capabilities and expanding market presence. A major emphasis is placed on research and development to improve substrate performance, enhance thermal and electrical properties, and enable finer interconnect scaling for next-generation semiconductor devices. Market participants are also investing in pilot production lines and scaling up manufacturing capacity to support the commercialization of advanced packaging solutions. Strategic collaborations with semiconductor manufacturers, foundries, and technology developers are helping accelerate innovation and ecosystem development. In addition, companies are working on improving process integration, cost efficiency, and material optimization to enhance competitiveness.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Material type trends

- 2.2.2 Packaging architecture type trends

- 2.2.3 Interconnect technology trends

- 2.2.4 End-user industry trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising AI, HPC demand requiring higher interconnect density

- 3.2.1.2 Glass substrates enable ultra-fine line redistribution layers

- 3.2.1.3 Superior thermal stability vs organic substrates

- 3.2.1.4 Increasing chiplet-based heterogeneous integration adoption

- 3.2.1.5 Panel-level packaging improves cost efficiency at scale

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited ecosystem readiness vs organic substrates

- 3.2.2.2 Fragility concerns during handling and manufacturing

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption in next-gen AI accelerators and data center chips

- 3.2.3.2 Expansion into automotive high-performance computing systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Borosilicate glass

- 5.3 Aluminosilicate glass

- 5.4 Fused silica / quartz

- 5.5 Specialty engineered glasses

Chapter 6 Market Estimates and Forecast, By Packaging Architecture Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 2.5D interposer packages

- 6.3 3D-IC / chiplet packages

- 6.4 Fan-out wafer-level packages (FOWLP)

- 6.5 Co-packaged optics / photonics packages

Chapter 7 Market Estimates and Forecast, By Interconnect Technology, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Through-glass via (TGV)

- 7.3 Redistribution layer (RDL)

- 7.4 Hybrid (TGV + RDL)

Chapter 8 Market Estimates and Forecast, By End-User Industry, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Data centers

- 8.3 Telecommunications

- 8.4 Consumer electronics

- 8.5 Automotive

- 8.6 Aerospace & defense

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 AGC Inc.

- 10.1.2 Corning

- 10.1.3 SCHOTT

- 10.1.4 HOYA Corporation

- 10.1.5 Intel Corporation

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Mosaic Microsystems

- 10.2.2 Asia Pacific

- 10.2.2.1 Absolics

- 10.2.2.2 NEG (Nippon Electric Glass Co., Ltd.)

- 10.2.2.3 Nippon Sheet Glass Co., Ltd.

- 10.2.2.4 Ohara Inc.

- 10.2.2.5 Shyawei Optronics (Taiwan)

- 10.2.2.6 TOPPAN

- 10.2.3 Europe

- 10.2.3.1 AT&S (Austria Technologie & Systemtechnik)

- 10.2.3.2 Plan Optik

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Avanstrate Inc.

全球先進半導體封裝市場(2027-2037 年)

全球先進半導體封裝市場(2027-2037 年) 半導體先進封裝市場預測至2034年-按封裝類型、材料、應用、最終用戶和地區分類的全球分析

半導體先進封裝市場預測至2034年-按封裝類型、材料、應用、最終用戶和地區分類的全球分析 2026-2030年全球先進半導體封裝市場先進封裝市場:規模、佔有率和成長率;全球產業分析;按類型、應用和地區分類;未來預測(2026-2034 年)

2026-2030年全球先進半導體封裝市場先進封裝市場:規模、佔有率和成長率;全球產業分析;按類型、應用和地區分類;未來預測(2026-2034 年) 晶片封裝及測試技術市場:依封裝技術、測試類型、最終用戶、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

晶片封裝及測試技術市場:依封裝技術、測試類型、最終用戶、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 全球食品飲料先進包裝市場:依材料類型、包裝形式、類型、應用和地區分類-預測至2031年先進封裝和晶片設計市場預測至2034年-按封裝技術、晶片整合方法、應用、最終用戶和地區分類的全球分析

全球食品飲料先進包裝市場:依材料類型、包裝形式、類型、應用和地區分類-預測至2031年先進封裝和晶片設計市場預測至2034年-按封裝技術、晶片整合方法、應用、最終用戶和地區分類的全球分析 先進封裝市場規模、佔有率和趨勢分析報告:按封裝類型、應用、地區和細分市場預測(2026-2033 年)晶片封裝市場預測至2034年-全球分析(依封裝技術、互連技術、晶片類型、材料類型、應用、最終使用者和地區分類)

先進封裝市場規模、佔有率和趨勢分析報告:按封裝類型、應用、地區和細分市場預測(2026-2033 年)晶片封裝市場預測至2034年-全球分析(依封裝技術、互連技術、晶片類型、材料類型、應用、最終使用者和地區分類) 先進封裝市場:依封裝類型、應用、終端用戶產業及地區分類

先進封裝市場:依封裝類型、應用、終端用戶產業及地區分類