|

市場調查報告書

商品編碼

2066264

全球食品飲料先進包裝市場:依材料類型、包裝形式、類型、應用和地區分類-預測至2031年Advanced Packaging for Food & Beverage Market by Type (Modified Atmosphere Packaging, Active Packaging, Smart Packaging ), Material Type (Plastics, Paper & Paperboard, Glass, Metal), Packaging Format, Application, and Region - Global Forecast to 2031 |

||||||

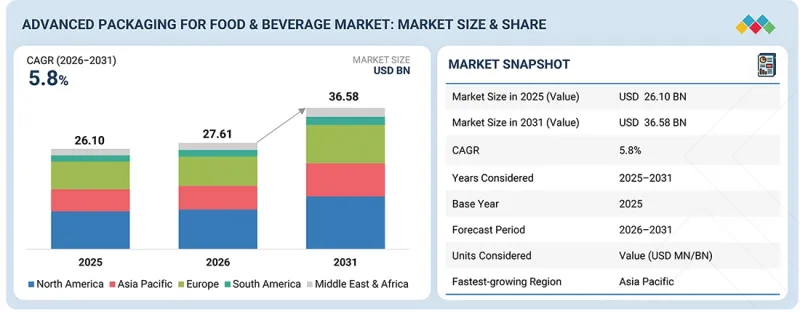

預計到 2031 年,食品和飲料先進包裝的市場規模將達到 365.8 億美元,高於 2026 年的 276.1 億美元,預測期內的複合年成長率為 5.8%。

| 調查範圍 | |

|---|---|

| 調查期 | 2025-2031 |

| 基準年 | 2025 |

| 預測期 | 2026-2031 |

| 計算單位 | 金額(100萬/10億美元) |

| 部分 | 按材料類型、包裝類型、類型、應用和地區分類 |

| 目標區域 | 北美洲、亞太地區、歐洲、中東和非洲、南美洲 |

全球先進食品飲料包裝市場正經歷顯著成長,主要驅動力是消費者對安全性、延長保存期限和提升產品品質日益成長的需求。這些包裝產品不僅在盛裝食品方面發揮至關重要的作用,而且在保護和維持食品新鮮度方面也發揮關鍵作用。調氣包裝、活性包裝和智慧包裝等技術因其有助於提高食品保護性能和增強消費者便利性而日益受到重視。市場成長的主要促進因素包括加速的都市化、加工食品和簡便食品食品消費量的成長以及有組織的零售和線上通路的興起。此外,人們對永續性關注和更嚴格的法規也促進了永續高性能材料的應用。

“在預測期內,軟包裝有望成為食品飲料市場中成長最快的先進包裝形式。”

由於其輕巧、經濟高效且便捷,軟包裝預計將在預測期內成為成長最快的先進食品飲料包裝形式。其卓越的阻隔性能,有效防止水分、氧氣和污染物的侵入,使其成為維持食品新鮮度和延長保存期限的理想選擇。即食食品飲料偏好的不斷成長,以及電子商務的興起,都顯著推動了軟包裝在先進食品飲料包裝市場中的應用。

“在預測期內,金屬有望成為先進食品飲料包裝市場中成長最快的材料類型。”

由於金屬具有高強度、耐久性和優異的阻隔性能,預計在預測期內,金屬將成為先進食品飲料包裝市場成長最快的材料類型。鋁和鋼等材料擴大用於罐頭、瓶子和瓶蓋,因為它們可以保護產品免受光照和氧氣等環境因素的影響,並防止污染。

“在預測期內,調氣包裝預計將成為先進食品飲料包裝市場中成長最快的類型。”

在預測期內,調氣包裝(MAP)預計將成為先進食品飲料包裝市場中成長最快的類型。由於該技術能夠延長保存期限並維持產品質量,預計其應用將日益廣泛。該技術透過控制包裝內的氣體成分(例如氧氣、二氧化碳和氮氣)來最大限度地減少微生物活性和氧化作用。消費者對生鮮食品和未經加工食品日益成長的需求預計將推動MAP技術在乳製品、肉類和烘焙產品中的應用。

“在預測期內,食品行業預計將在先進食品飲料包裝市場中呈現最高的成長率。”

在預測期內,受加工食品、新鮮食品和簡便食品需求不斷成長的推動,食品業預計將成為先進食品飲料包裝市場中成長最快的應用領域。都市化、飲食習慣的改變以及快節奏的生活方式正在推動即食食品和生鮮食品的需求。人們對食品安全、延長保存期限和減少廢棄物的日益關注,促使了調氣包裝(MAP)、活性包裝和阻隔性材料等先進技術的應用。此外,食品零售、食品加工和食品電子商務行業的顯著成長也增加了對先進解決方案的需求。

“在預測期內,亞太地區先進食品飲料包裝市場預計將呈現最高的成長率。”

在預測期內,亞太地區預計將成為先進食品飲料包裝市場成長最快的地區。這一成長將主要由快速的都市化、人口成長、工資上漲以及對安全便捷食品日益成長的需求所驅動。預計到2050年,該地區人口將超過48.4億,其中約64%居住在都市區,將顯著增加食品需求。已調理食品、飲料和新鮮水果消費量的成長正在推動對調氣包裝(MAP)、活性包裝和智慧包裝解決方案的需求。印度和中國等國家食品加工、有組織零售和線上食品配送的快速發展,進一步促進了該地區對先進包裝的需求。

本報告涵蓋的公司有:安姆科公司(瑞士)、希悅爾公司(美國)、蒙迪公司(英國)、利樂公司(瑞士)、胡塔瑪基公司(芬蘭)、東洋制菓集團控股有限公司(日本)、皇冠公司(美國)、康斯坦蒂亞軟性包裝公司(奧地利)、圖形包裝公司控股有限公司(美國)和溫帕克有限公司。

本研究對先進食品飲料包裝市場的主要參與者進行了詳細的競爭分析,包括公司簡介、近期發展和主要市場策略。

調查範圍

本研究報告根據材料類型(塑膠、紙/紙板、玻璃、金屬)、形狀(硬質、軟質、半硬質)、類型(調氣包裝、活性包裝、智慧包裝)和應用(食品和飲料)對先進食品飲料包裝市場進行了細分。報告詳細資訊了影響先進食品飲料包裝市場成長的促進因素、阻礙因素、挑戰和成長機會。該報告還對主要行業參與企業進行了深入分析,包括其業務概況、產品供應以及與先進食品飲料包裝市場相關的關鍵策略,例如併購、產品發布和擴張。此外,報告還涵蓋了先進食品飲料包裝市場生態系統中新興新創企業的競爭考察。

購買本報告的理由

本報告為市場領導和新參與企業提供先進食品飲料包裝市場及其細分市場的整體收入預測。它幫助相關人員了解競爭格局,獲得更深入的洞察以更好地定位自身業務,並制定合適的打入市場策略。報告還提供有關市場趨勢、關鍵市場促進因素、限制因素、挑戰和機會的資訊。

本報告深入分析了以下幾點:

- 本報告深入分析了關鍵促進因素(對加工食品、安全、保存期限長的食品和簡便食品的需求不斷成長;電子商務、食材自煮包和低溫運輸物流的擴張;以及新興市場食品消費的成長)和阻礙因素(嚴格且不斷變化的監管要求;回收基礎設施不足和使用後處理的限制;以及投入成本上升和原料價格波動),機會(可生物分解和可堆肥材料的下一代創新;智慧包裝、物聯網和工業4.0技術的融合;以及先進替代食品安全性和真實性的提高),以及挑戰(在高阻隔性能與永續性和減少廢棄物之間取得平衡;以及採用先進技術的高初始投資和成本障礙)。

- 產品開發/創新:深入洞察先進食品飲料包裝市場的未來技術趨勢、研發活動以及產品/服務發布。

- 市場發展:盈利市場的全面資訊-本報告分析了各個地區的先進食品和飲料包裝市場。

- 市場多元化:提供有關先進食品和飲料包裝市場的新產品和服務、未開發地區、最新趨勢和投資的全面資訊。

- 競爭評估:對主要公司(包括 Amcor plc(瑞士)、Sealed Air(美國)、Mondi(英國戰略和產品市場的市場發展。

目錄

第1章:引言

第2章執行摘要

第3章重要考察

第4章 市場概覽

- 市場動態

- 促進因素

- 抑制因子

- 機會

- 任務

- 未滿足的需求和未開發的領域

- 相互關聯的市場與跨產業機遇

- 一級/二級/三級公司的策略性舉措

第5章 產業趨勢

- 波特五力分析

- 宏觀經濟分析

- 價值鏈分析

- 生態系分析

- 價格分析

- 貿易分析

- 2026-2027 年主要會議和活動

- 影響客戶業務的趨勢/顛覆性因素

- 投資和資金籌措場景

- 案例研究分析

- 2025年美國關稅的影響:食品飲料產業先進包裝市場

第6章:透過採用技術、專利、數位技術和人工智慧實現策略顛覆

- 主要技術

- 互補技術

- 鄰近技術

- 技術/產品藍圖

- 專利分析

- 未來應用

- 人工智慧/通用人工智慧對食品飲料市場先進包裝的影響

- 成功案例和實際應用

第7章永續性和監管情勢

- 當地法規和合規性

- 對永續性的承諾

- 監理政策對永續性舉措的影響

第8章:顧客趨勢與購買行為

- 決策流程

- 買方相關人員和採購評估標準

- 實施障礙和內部挑戰

- 各種應用中尚未滿足的需求

- 市場盈利

第9章:食品飲料先進包裝市場(依材料類型分類)

- 塑膠

- 紙張和紙板

- 玻璃

- 金屬

- 其他

第10章 先進食品飲料包裝市場(依形式分類)

- 硬質包裝

- 軟質包裝

- 半剛性包裝

第11章:食品飲料先進包裝市場(按類型分類)

- 調氣包裝

- 活性包裝

- 智慧包裝

第12章 先進食品飲料包裝市場(依應用領域分類)

- 食物

- 飲料

第13章 先進食品飲料包裝市場(按地區分類)

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 義大利

- 英國

- 西班牙

- 俄羅斯

- 其他

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他

- 中東和非洲

- 海灣合作理事會國家

- 南非

- 其他

- 南美洲

- 巴西

- 阿根廷

- 其他

第14章 競爭格局

- 概述

- 主要公司的策略/優勢

- 市佔率分析

- 主要公司的收入分析

- 企業估值和財務指標

- 品牌對比

- 企業估值矩陣

- 新創企業/中小企業估值象限

- 競爭格局

第15章:公司簡介

- 大公司

- AMCOR PLC

- SEALED AIR

- MONDI

- TETRA LAVAL

- HUHTAMAKI

- TOYO SEIKAN GROUP HOLDINGS, LTD.

- CROWN

- CONSTANTIA FLEXIBLES

- GRAPHIC PACKAGING HOLDING COMPANY

- WINPAK LTD.

- 其他公司

- AVERY DENNISON CORPORATION

- CCL INDUSTRIES

- PROAMPAC

- KLOCKNER PENTAPLAST

- COVERIS

- PPC FLEX COMPANY INC.

- MASTERPACK

- GRUPPO FABBRI

- EVERTIS

- FPS FLEXIBLE PACKAGING SOLUTIONS

- VARCODE

- INSIGNIA TECHNOLOGIES LTD.

- TIMESTRIP UK LTD

- ARIS PACK

- MULTISORB

第16章調查方法

第17章附錄

The advanced packaging for food & beverage market is projected to reach USD 36.58 billion by 2031 from USD 27.61 billion in 2026, at a CAGR of 5.8% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2025-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million/Billion) |

| Segments | Material Type, Packaging Format, Type, Application, and Region |

| Regions covered | North America, Asia Pacific, Europe, Middle East & Africa, and South America |

There is significant growth in the global market for advanced packaging in food & beverage, fueled by increasing demand for safety, longer shelf life, and improved product quality. Such packaging plays an important role not only in containing food products but also in protecting and preserving their freshness. Modified atmosphere packaging, active packaging, and smart packaging technologies have been gaining importance owing to their ability to enhance packaging protection and consumer convenience. Some key drivers of market growth are accelerated urbanization, rising consumption of processed and convenience foods, and the rise of organized retail and online channels. Furthermore, the increasing focus on sustainability and stricter regulations is helping drive acceptance of sustainable, high-performing packaging materials.

"Flexible packaging is projected to be the fastest-growing packaging format in the advanced packaging for food & beverage market during the forecast period."

Flexible packaging is projected to be the fastest-growing packaging format in the advanced packaging for food & beverage market during the forecast period, propelled by its lightweight characteristics, cost efficiency, and enhanced convenience. Its capacity to offer superior barrier protection against moisture, oxygen, and pollutants renders it optimal for maintaining food freshness and prolonging shelf life. The growing preference for ready-to-eat foods and beverages, along with the advent of e-commerce, has also contributed significantly to the increasing adoption of flexible packaging in the advanced packaging for food and beverages market.

"Metal is projected to be the fastest-growing material type in the advanced packaging for food & beverage market during the forecast period."

Metal is anticipated to be the fastest-growing material type in the advanced packaging for food & beverage market during the forecast period, owing to its high strength and durability, along with good barrier qualities. The use of materials like aluminum and steel in cans, jars, and closures has been rising because they protect against environmental elements such as light and oxygen and prevent contamination.

"Modified atmosphere packaging is projected to be the fastest-growing type in the advanced packaging for food & beverage market during the forecast period."

Modified atmosphere packaging (MAP) is anticipated to be the fastest-growing type in the advanced packaging for food & beverage market over the forecast period. This technology will see increased application due to its ability to prolong shelf life and maintain product quality. It works by ensuring that the composition of gases such as oxygen, carbon dioxide, and nitrogen within the pack is controlled, thereby minimizing microbial activity and oxidation. Increasing demand for fresh products and minimal processing of food products is expected to drive their use in dairy, meat, and bakery products, among others.

"Food is projected to be the fastest-growing application in the advanced packaging for food & beverage market during the forecast period."

Food is expected to be the fastest-growing application in the advanced packaging for food and beverage market over the forecast period, driven by rising demand for processed, packaged, and convenience food products. Increased urbanization, shifting eating patterns, and hectic lives are driving up demand for ready-to-eat meals and fresh packaged food. Growing concerns about food safety, shelf-life extension, and waste reduction are driving the adoption of advanced packaging technologies such as modified atmosphere packaging (MAP), active packaging, and high-barrier materials. Additionally, the retail food business, the food processing industry, and e-commerce websites for food products are witnessing tremendous growth, thereby increasing the demand for advanced packaging solutions.

"Asia Pacific is projected to be the fastest-growing region in the advanced packaging for food & beverage market during the forecast period."

Asia Pacific is estimated to be the fastest-growing region in the advanced packaging for food & beverage market over the forecast period. The growth will be aided by rapid urbanization, population growth, rising wages, and increasing demand for easy-to-consume, safe packaged foods. The region is projected to attain over 4.84 billion inhabitants by 2050, with nearly 64% living in urban areas, thereby greatly increasing the demand for packaged foods. The growing consumption of pre-cooked foods, beverages, and fresh fruits is driving demand for MAP, active packaging, and smart packaging solutions. Countries such as India and China, owing to rapid growth in food processing, organized retailing, and e-delivery of food products, are further propelling demand for advanced packaging in the region.

By Company Type: Tier 1: 40%, Tier 2: 30%, and Tier 3: 30%

By Designation: Directors: 30%, Managers: 20%, and Others: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and Middle East & Africa 20%

Notes: Others include sales, marketing, and product managers.

Tier 1: >USD 1 Billion; Tier 2: USD 500 million-1 Billion; and Tier 3: <USD 500 million

Companies Covered: Amcor plc (Switzerland), Sealed Air (US), Mondi (UK), Tetra Laval (Switzerland), Huhtamaki (Finland), Toyo Seikan Group Holdings, Ltd. (Japan), Crown (US), Constantia Flexibles (Austria), Graphic Packaging Holding Company (US), and Winpak LTD. (Canada) are covered in the report.

The study includes an in-depth competitive analysis of these key players in the advanced packaging for food & beverage market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the advanced packaging for food & beverage market based on Material Type (Plastics, Paper & Paperboard, Glass, Metal), Packaging Format (Rigid Packaging, Flexible Packaging, Semi-Rigid Packaging), Type (Modified Atmosphere Packaging, Active Packaging, and Smart Packaging), and Application (Food and Beverages). The report's scope covers detailed information regarding the drivers, restraints, challenges, and opportunities influencing the growth of the advanced packaging for food & beverage market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products offered, and key strategies, such as mergers, acquisitions, product launches, and expansions, associated with the advanced packaging for food & beverage market. This report covers a competitive analysis of upcoming startups in the advanced packaging for food & beverage market ecosystem.

Reasons to Buy the Report

The report will provide market leaders/new entrants with estimates of revenue for the overall advanced packaging for food & beverage market and its subsegments. This report will help stakeholders understand the competitive landscape, gain more insights into positioning their businesses better, and plan suitable go-to-market strategies. The report will help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

- Analysis of key drivers (Rising demand for processed, safe, shelf-stable, and convenient food, Expansion of e-commerce, meal kits, and cold-chain logistics, and Expansion of packaged food consumption in emerging markets ), restraints (Stringent and evolving regulatory requirements, Inadequate recycling infrastructure and end-of-life constraints, and Rising input costs and material price volatility), opportunities (Next-generation innovations in biodegradable and compostable packaging materials, Convergence of smart packaging, IoT, and Industry 4.0 technologies, and Enhancing food safety and authenticity through advanced packaging), and challenges (Balancing high-barrier performance with sustainability and waste reduction and High initial investment and cost barriers in advanced packaging adoptions).

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the advanced packaging for food & beverage market.

- Market Development: Comprehensive information about profitable markets - the report analyzes the advanced packaging for food & beverage market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the advanced packaging for food & beverage market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as Amcor plc (Switzerland), Sealed Air (US), Mondi (UK), Tetra Laval (Switzerland), Huhtamaki (Finland), Toyo Seikan Group Holdings, Ltd. (Japan), Crown (US), Constantia Flexibles (Austria), Graphic Packaging Holding Company (US), and Winpak LTD. (Canada), among others.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET

- 3.2 NORTH AMERICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION AND COUNTRY

- 3.3 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY MATERIAL TYPE

- 3.4 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT

- 3.5 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY TYPE

- 3.6 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION

- 3.7 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising demand for safe, shelf-life-extended, and convenience foods

- 4.2.1.2 Expansion of e-commerce, meal kits, and cold-chain logistics

- 4.2.1.3 Expansion of packaged food consumption in emerging markets

- 4.2.2 RESTRAINTS

- 4.2.2.1 Stringent and evolving regulatory requirements

- 4.2.2.2 Inadequate recycling infrastructure and end-of-life constraints

- 4.2.2.3 Rising input costs and material price volatility

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Next-generation innovations in biodegradable and compostable packaging materials

- 4.2.3.2 Convergence of smart packaging, IoT, and Industry 4.0 technologies

- 4.2.3.3 Enhancing food safety and authenticity through advanced packaging

- 4.2.4 CHALLENGES

- 4.2.4.1 Balancing high-barrier performance with sustainability and waste reduction

- 4.2.4.2 High initial investment and cost barriers in advanced packaging adoption

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.4.2.1 Dairy industry -> Ready-to-eat (RTE) food industry

- 4.4.2.2 Meat & seafood industry -> Fresh produce industry

- 4.4.2.3 Beverage industry -> Functional & nutraceutical food industry

- 4.4.2.4 Bakery & confectionery industry -> Snack food industry

- 4.4.2.5 Frozen food industry -> Online food delivery industry

- 4.4.2.6 Alcoholic beverage industry -> Premium food industry

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 TIER 1 PLAYERS: GLOBAL LEADERS DRIVING SCALE AND CIRCULAR INNOVATION

- 4.5.1.1 Amcor: participation in crisp circular recycling initiative

- 4.5.1.2 Sealed air: launch of CRYOVAC compostable overwrap tray

- 4.5.2 TIER 2 PLAYERS: REGIONAL EXPANSION AND REGULATORY-LED INNOVATION

- 4.5.2.1 PROAMPAC: acquisition of belle-pak inc.

- 4.5.2.2 Coveris: PFAS-free design strategy and portfolio transformation

- 4.5.3 TIER 3 PLAYERS: NICHE INNOVATORS AND TECHNOLOGY-DRIVEN EXPANSION

- 4.5.3.1 PPC Flexible Packaging: Acquisition Of STEPAC, Mapfresh Holdings

- 4.5.1 TIER 1 PLAYERS: GLOBAL LEADERS DRIVING SCALE AND CIRCULAR INNOVATION

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC ANALYSIS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECASTS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND ANALYSIS

- 5.6 TRADE ANALYSIS

- 5.6.1 EXPORT SCENARIO (HS CODE 3923)

- 5.6.2 IMPORT SCENARIO (HS CODE 3923)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 SUSTAINABLE SHELF-LIFE EXTENSION & BRAND ENHANCEMENT THROUGH MAP-BASED FIBER PACKAGING

- 5.10.2 ENHANCING CONSUMER ENGAGEMENT THROUGH SMART & CONNECTED PACKAGING IN CONFECTIONERY

- 5.10.3 OPERATIONAL EFFICIENCY & BUSINESS GROWTH THROUGH DIGITAL PACKAGING MANAGEMENT SYSTEMS

- 5.11 IMPACT OF 2025 US TARIFF: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRY/REGION

- 5.11.4.1 US

- 5.11.4.2 Canada

- 5.11.4.3 China

- 5.11.4.4 Europe

- 5.11.5 END-USE INDUSTRY IMPACT

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 ADVANCED MATERIALS AND NANOTECHNOLOGY IN SUSTAINABLE SMART PACKAGING

- 6.1.2 ADVANCED BARRIER COATINGS AND MONO-MATERIAL PACKAGING IN FOOD & BEVERAGE MARKET

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 AI AND IOT INTEGRATION IN NEXT-GENERATION SMART PACKAGING

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 FOOD IRRADIATION TECHNOLOGY IN ADVANCED FOOD PRESERVATION

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM (2025-2027) | SUSTAINABILITY OPTIMIZATION AND EARLY SMART INTEGRATION

- 6.4.2 MID-TERM (2027-2030) | BIO-MATERIAL INNOVATION AND SMART ECOSYSTEM INTEGRATION

- 6.4.3 LONG-TERM (2030-2035+) | AUTONOMOUS AND NET-ZERO PACKAGING SYSTEMS

- 6.5 PATENT ANALYSIS

- 6.5.1 INTRODUCTION

- 6.5.2 METHODOLOGY

- 6.5.3 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, PATENT ANALYSIS, 2016-2025

- 6.6 FUTURE APPLICATIONS

- 6.6.1 INTELLIGENT PACKAGING WITH REAL-TIME FRESHNESS SENSORS & IOT CONNECTIVITY

- 6.6.2 SUSTAINABLE & BIO-BASED PACKAGING

- 6.6.3 ACTIVE & INTELLIGENT PACKAGING SYSTEMS

- 6.6.4 HIGH-BARRIER & MODIFIED ATMOSPHERE PACKAGING (MAP)

- 6.7 IMPACT OF AI/GEN AI ON ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES IN ADVANCED PACKAGING FOR FOOD & BEVERAGE PROCESSING

- 6.7.3 CASE STUDIES OF AI IMPLEMENTATION IN ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET

- 6.7.3.1 Interconnected adjacent ecosystem and impact on market players

- 6.7.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET

- 6.8 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.8.1 NON-THERMAL TECHNOLOGIES AND SMART PACKAGING ENHANCING SHELF LIFE IN EUROPE

- 6.8.2 MAP-BASED PACKAGING IMPROVING FRESHNESS AND EFFICIENCY IN JAPAN

- 6.8.3 SMART QR-BASED PACKAGING ENHANCING TRANSPARENCY IN US

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 LOW-CARBON MATERIALS AND ECO-FRIENDLY SOURCING

- 7.2.2 LIGHTWEIGHTING AND MATERIAL OPTIMIZATION

- 7.2.3 RECYCLABILITY AND CIRCULAR PACKAGING DESIGN

- 7.2.4 WASTE REDUCTION AND CLOSED-LOOP SYSTEMS

- 7.2.5 SUSTAINABLE BARRIER TECHNOLOGIES AND ACTIVE PACKAGING

- 7.2.6 SMART PACKAGING FOR SUPPLY CHAIN EFFICIENCY

- 7.2.7 END-OF-LIFE MANAGEMENT AND COMPOSTABILITY

- 7.3 IMPACT OF REGULATORY POLICY ON SUSTAINABILITY INITIATIVES

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS APPLICATIONS

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES BY APPLICATION

9 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY MATERIAL TYPE

- 9.1 INTRODUCTION

- 9.2 PLASTIC

- 9.2.1 COST-EFFICIENT, SCALABLE, AND TECHNOLOGY-ENABLING MATERIAL

- 9.3 PAPER & PAPERBOARD

- 9.3.1 RENEWABLE AND SUSTAINABLE MATERIALS FOR ADVANCED FOOD & BEVERAGE PACKAGING

- 9.4 GLASS

- 9.4.1 PREMIUM, INERT, AND CIRCULAR MATERIAL

- 9.5 METAL

- 9.5.1 DURABLE, HIGH-BARRIER, AND CIRCULAR PACKAGING MATERIAL

- 9.6 OTHER MATERIAL TYPES

10 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT

- 10.1 INTRODUCTION

- 10.2 RIGID PACKAGING

- 10.2.1 ENSURING PRODUCT PROTECTION, SHELF STABILITY, AND CIRCULARITY

- 10.3 FLEXIBLE PACKAGING

- 10.3.1 DRIVING LIGHTWEIGHT EFFICIENCY AND SHELF-LIFE EXTENSION

- 10.4 SEMI-RIGID PACKAGING

- 10.4.1 BALANCING PROTECTION, CONVENIENCE, AND SUSTAINABILITY

11 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY TYPE

- 11.1 INTRODUCTION

- 11.2 MODIFIED ATMOSPHERE PACKAGING

- 11.2.1 RISING DEMAND FOR FRESH, MINIMALLY PROCESSED, AND LONGER-LASTING PRODUCTS

- 11.3 ACTIVE PACKAGING

- 11.3.1 RISING DEMAND FOR SHELF-LIFE EXTENSION AND SUSTAINABLE FOOD PRESERVATION TECHNOLOGIES

- 11.4 SMART PACKAGING

- 11.4.1 RISING DEMAND FOR INTELLIGENT MONITORING TO REDUCE FOOD WASTE AND ENHANCE FRESHNESS ASSURANCE

12 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION

- 12.1 INTRODUCTION

- 12.2 FOOD

- 12.2.1 FROZEN

- 12.2.1.1 Advanced packaging enabling cold chain integrity and global trade expansion

- 12.2.2 DRIED PRODUCTS

- 12.2.2.1 Advanced packaging enhancing shelf life, freshness, and consumer convenience

- 12.2.3 OTHER FOOD

- 12.2.1 FROZEN

- 12.3 BEVERAGES

- 12.3.1 HOT BEVERAGES

- 12.3.1.1 Advanced packaging for aroma preservation and premium positioning

- 12.3.2 COLD BEVERAGES

- 12.3.2.1 Supporting shelf life, safety, and regulatory compliance

- 12.3.1 HOT BEVERAGES

13 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 E-commerce expansion, export demand, and circular packaging transformation

- 13.2.2 CANADA

- 13.2.2.1 Food processing strength, retail consolidation, and cross-border trade integration

- 13.2.3 MEXICO

- 13.2.3.1 Export expansion, food processing strength, and modern retail transformation

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 GERMANY

- 13.3.1.1 Strong retail structure, premium food demand, and supply chain efficiency

- 13.3.2 FRANCE

- 13.3.2.1 Strong SME-based food processing and dominance of modern retail formats

- 13.3.3 ITALY

- 13.3.3.1 Strong export-oriented agri-food system and high-value product portfolio

- 13.3.4 UK

- 13.3.4.1 Large-scale food manufacturing, export growth, and health-focused innovation

- 13.3.5 SPAIN

- 13.3.5.1 Expanding retail networks, FoodTech innovation, and export growth

- 13.3.6 RUSSIA

- 13.3.6.1 Shift toward value-added food exports and expanding meat production

- 13.3.7 REST OF EUROPE

- 13.3.1 GERMANY

- 13.4 ASIA PACIFIC

- 13.4.1 CHINA

- 13.4.1.1 Rapid expansion of food consumption, processing industry, and premium beverage

- 13.4.2 INDIA

- 13.4.2.1 Strong growth of food processing sector, agricultural abundance, and policy support

- 13.4.3 JAPAN

- 13.4.3.1 Rising global demand for Japanese food exports and expanding beverage consumption

- 13.4.4 SOUTH KOREA

- 13.4.4.1 Expanding K-food exports, strong retail demand, and global popularity of Korean cuisine

- 13.4.5 REST OF ASIA PACIFIC

- 13.4.1 CHINA

- 13.5 MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.5.1.1 Saudi Arabia

- 13.5.1.1.1 Rapid expansion of organized retail and rising demand for convenient packaged foods

- 13.5.1.2 UAE

- 13.5.1.2.1 Rapid growth of E-commerce and high dependence on processed food supply

- 13.5.1.3 Rest of GCC countries

- 13.5.1.1 Saudi Arabia

- 13.5.2 SOUTH AFRICA

- 13.5.2.1 Strong retail consolidation and rising demand for convenient, health-focused packaged foods

- 13.5.3 REST OF MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.6 SOUTH AMERICA

- 13.6.1 BRAZIL

- 13.6.1.1 Strong meat export growth, expanding food processing industry, and large retail base

- 13.6.2 ARGENTINA

- 13.6.2.1 Strong beef export growth and rising demand for premium meat

- 13.6.3 REST OF SOUTH AMERICA

- 13.6.1 BRAZIL

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 14.3 MARKET SHARE ANALYSIS

- 14.4 REVENUE ANALYSIS OF KEY PLAYERS

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.6 BRAND COMPARISON

- 14.7 COMPANY EVALUATION MATRIX

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Material type footprint

- 14.7.5.4 Packaging format footprint

- 14.7.5.5 Type footprint

- 14.7.5.6 Application footprint

- 14.8 STARTUP/SME EVALUATION QUADRANT

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 14.8.5.1 Detailed list of key startups/SMEs

- 14.8.5.1.1 Competitive benchmarking of key startups/SMEs

- 14.8.5.1 Detailed list of key startups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 AMCOR PLC

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product Launches

- 15.1.1.3.2 Deals

- 15.1.1.3.3 Expansions

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 SEALED AIR

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product Launches

- 15.1.2.3.2 Deals

- 15.1.2.3.3 Expansions

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 MONDI

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product Launches

- 15.1.3.3.2 Deals

- 15.1.3.3.3 Expansions

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 TETRA LAVAL

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product Launches

- 15.1.4.3.2 Deals

- 15.1.4.3.3 Expansions

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 HUHTAMAKI

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product Launches

- 15.1.5.3.2 Deals

- 15.1.5.3.3 Expansions

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 TOYO SEIKAN GROUP HOLDINGS, LTD.

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 MnM view

- 15.1.7 CROWN

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Deals

- 15.1.7.3.2 Expansions

- 15.1.7.4 MnM view

- 15.1.8 CONSTANTIA FLEXIBLES

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Deals

- 15.1.8.4 MnM view

- 15.1.9 GRAPHIC PACKAGING HOLDING COMPANY

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Product Launches

- 15.1.9.3.2 Deals

- 15.1.9.3.3 Expansions

- 15.1.9.4 MnM view

- 15.1.10 WINPAK LTD.

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.2.1 Expansions

- 15.1.10.3 MnM view

- 15.1.1 AMCOR PLC

- 15.2 OTHER PLAYERS

- 15.2.1 AVERY DENNISON CORPORATION

- 15.2.2 CCL INDUSTRIES

- 15.2.3 PROAMPAC

- 15.2.4 KLOCKNER PENTAPLAST

- 15.2.5 COVERIS

- 15.2.6 PPC FLEX COMPANY INC.

- 15.2.7 MASTERPACK

- 15.2.8 GRUPPO FABBRI

- 15.2.9 EVERTIS

- 15.2.10 FPS FLEXIBLE PACKAGING SOLUTIONS

- 15.2.11 VARCODE

- 15.2.12 INSIGNIA TECHNOLOGIES LTD.

- 15.2.13 TIMESTRIP UK LTD

- 15.2.14 ARIS PACK

- 15.2.15 MULTISORB

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.2.2 Key industry insights

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.3 BASE NUMBER CALCULATION

- 16.3.1 DEMAND-SIDE APPROACH

- 16.3.2 SUPPLY-SIDE APPROACH

- 16.4 MARKET FORECAST APPROACH

- 16.4.1 SUPPLY SIDE

- 16.4.2 DEMAND SIDE

- 16.5 DATA TRIANGULATION

- 16.6 FACTOR ANALYSIS

- 16.7 RESEARCH ASSUMPTIONS

- 16.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS

List of Tables

- TABLE 1 PORTER'S FIVE FORCES ANALYSIS

- TABLE 2 GLOBAL GDP GROWTH PROJECTION, BY REGION, 2021-2028 (USD TRILLION)

- TABLE 3 ROLES OF COMPANIES IN ADVANCED PACKAGING FOR FOOD & BEVERAGE ECOSYSTEM

- TABLE 4 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET: INDICATIVE SELLING PRICE, BY TYPE

- TABLE 5 EXPORT DATA RELATED TO HS CODE 3923-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 6 IMPORT DATA RELATED TO HS CODE 3923-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 7 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET: DETAILED LIST OF CONFERENCES AND EVENTS, 2026-2027

- TABLE 8 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET: LIST OF KEY PATENTS, 2023-2025

- TABLE 9 TOP USE CASES AND MARKET POTENTIAL

- TABLE 10 BEST PRACTICES: COMPANIES IMPLEMENTING USE CASES

- TABLE 11 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET: CASE STUDIES RELATED TO GEN AI IMPLEMENTATION

- TABLE 12 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, INDUSTRY ASSOCIATIONS, AND OTHER ORGANIZATIONS

- TABLE 13 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, INDUSTRY ASSOCIATIONS, AND OTHER ORGANIZATIONS

- TABLE 14 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, INDUSTRY ASSOCIATIONS, AND OTHER ORGANIZATIONS

- TABLE 15 MIDDLE EAST & AFRICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, INDUSTRY ASSOCIATIONS, AND OTHER ORGANIZATIONS

- TABLE 16 SOUTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, INDUSTRY ASSOCIATIONS, AND OTHER ORGANIZATIONS

- TABLE 17 GLOBAL INDUSTRY STANDARDS IN ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET

- TABLE 18 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY APPLICATION (%)

- TABLE 19 KEY BUYING CRITERIA, BY END-USE INDUSTRY

- TABLE 20 UNMET NEEDS IN ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET BY APPLICATION

- TABLE 21 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY MATERIAL TYPE, 2025-2031 (USD MILLION)

- TABLE 22 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 23 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY TYPE, 2025-2031 (USD MILLION)

- TABLE 24 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 25 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 26 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 27 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 28 NORTH AMERICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY COUNTRY, 2025-2031 (USD MILLION)

- TABLE 29 NORTH AMERICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY MATERIAL TYPE, 2025-2031 (USD MILLION)

- TABLE 30 NORTH AMERICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 31 NORTH AMERICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 32 NORTH AMERICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 33 NORTH AMERICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 34 US: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 35 US: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 36 US: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 37 US: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 38 CANADA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 39 CANADA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 40 CANADA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 41 CANADA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 42 MEXICO: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 43 MEXICO: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 44 MEXICO: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 45 MEXICO: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 46 EUROPE: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY COUNTRY, 2025-2031 (USD MILLION)

- TABLE 47 EUROPE: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY MATERIAL TYPE, 2025-2031 (USD MILLION)

- TABLE 48 EUROPE: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 49 EUROPE: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 50 EUROPE: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 51 EUROPE: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 52 GERMANY: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 53 GERMANY: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 54 GERMANY: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 55 GERMANY: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 56 FRANCE: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 57 FRANCE: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 58 FRANCE: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 59 FRANCE: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 60 ITALY: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 61 ITALY: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 62 ITALY: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 63 ITALY: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 64 UK: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 65 UK: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 66 UK: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 67 UK: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 68 SPAIN: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 69 SPAIN: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 70 SPAIN: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 71 SPAIN: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 72 RUSSIA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 73 RUSSIA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 74 RUSSIA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 75 RUSSIA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 76 REST OF EUROPE: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 77 REST OF EUROPE: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 78 REST OF EUROPE: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 79 REST OF EUROPE: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 80 ASIA PACIFIC: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY COUNTRY, 2025-2031 (USD MILLION)

- TABLE 81 ASIA PACIFIC: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY MATERIAL TYPE, 2025-2031 (USD MILLION)

- TABLE 82 ASIA PACIFIC: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 83 ASIA PACIFIC: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 84 ASIA PACIFIC: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 85 ASIA PACIFIC: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 86 CHINA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 87 CHINA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 88 CHINA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 89 CHINA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 90 INDIA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 91 INDIA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 92 INDIA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 93 INDIA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 94 JAPAN: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 95 JAPAN: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 96 JAPAN: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 97 JAPAN: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 98 SOUTH KOREA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 99 SOUTH KOREA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 100 SOUTH KOREA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 101 SOUTH KOREA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 102 REST OF ASIA PACIFIC: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 103 REST OF ASIA PACIFIC: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 104 REST OF ASIA PACIFIC: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 105 REST OF ASIA PACIFIC: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 106 MIDDLE EAST & AFRICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY COUNTRY, 2025-2031 (USD MILLION)

- TABLE 107 MIDDLE EAST & AFRICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY MATERIAL TYPE, 2025-2031 (USD MILLION)

- TABLE 108 MIDDLE EAST & AFRICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 109 MIDDLE EAST & AFRICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 110 MIDDLE EAST & AFRICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 111 MIDDLE EAST & AFRICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 112 GCC COUNTRIES: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 113 GCC COUNTRIES: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 114 GCC COUNTRIES: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 115 GCC COUNTRIES: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 116 SAUDI ARABIA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 117 SAUDI ARABIA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 118 SAUDI ARABIA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 119 SAUDI ARABIA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 120 UAE: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 121 UAE: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 122 UAE: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 123 UAE: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 124 REST OF GCC COUNTRIES: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 125 REST OF GCC COUNTRIES: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 126 REST OF GCC COUNTRIES: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 127 REST OF GCC COUNTRIES: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 128 SOUTH AFRICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 129 SOUTH AFRICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 130 SOUTH AFRICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 131 SOUTH AFRICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 132 REST OF MIDDLE EAST & AFRICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 133 REST OF MIDDLE EAST & AFRICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 134 REST OF MIDDLE EAST & AFRICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 135 REST OF MIDDLE EAST & AFRICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 136 SOUTH AMERICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY COUNTRY, 2025-2031 (USD MILLION)

- TABLE 137 SOUTH AMERICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY MATERIAL TYPE, 2025-2031 (USD MILLION)

- TABLE 138 SOUTH AMERICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 139 SOUTH AMERICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 140 SOUTH AMERICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 141 SOUTH AMERICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 142 BRAZIL: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 143 BRAZIL: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 144 BRAZIL: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 145 BRAZIL: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 146 ARGENTINA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 147 ARGENTINA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 148 ARGENTINA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 149 ARGENTINA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 150 REST OF SOUTH AMERICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY PACKAGING FORMAT, 2025-2031 (USD MILLION)

- TABLE 151 REST OF SOUTH AMERICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY APPLICATION, 2025-2031 (USD MILLION)

- TABLE 152 REST OF SOUTH AMERICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY FOOD APPLICATION, 2025-2031 (USD MILLION)

- TABLE 153 REST OF SOUTH AMERICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, BY BEVERAGE APPLICATION, 2025-2031 (USD MILLION)

- TABLE 154 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET: OVERVIEW OF MAJOR STRATEGIES ADOPTED BY KEY PLAYERS, JANUARY 2021-MARCH 2026

- TABLE 155 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET: DEGREE OF COMPETITION, 2025

- TABLE 156 ADVANCED PACKAGING MARKET FOR FOOD & BEVERAGE MARKET: REGIONAL FOOTPRINT, 2025

- TABLE 157 ADVANCED PACKAGING MARKET FOR FOOD & BEVERAGE MARKET: MATERIAL TYPE FOOTPRINT, 2025

- TABLE 158 ADVANCED PACKAGING MARKET FOR FOOD & BEVERAGE MARKET: PACKAGING FORMAT FOOTPRINT, 2025

- TABLE 159 ADVANCED PACKAGING MARKET FOR FOOD & BEVERAGE MARKET: TYPE FOOTPRINT, 2025

- TABLE 160 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET: APPLICATION FOOTPRINT, 2025

- TABLE 161 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET: DETAILED LIST OF KEY STARTUPS/SMES, 2025

- TABLE 162 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES, 2025

- TABLE 163 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET: PRODUCT LAUNCHES, JANUARY 2021-MARCH 2026

- TABLE 164 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET: DEALS, JANUARY 2021-MARCH 2026

- TABLE 165 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET: EXPANSIONS, JANUARY 2021-MARCH 2026

- TABLE 166 AMCOR PLC: BUSINESS OVERVIEW

- TABLE 167 AMCOR PLC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 168 AMCOR PLC: PRODUCT LAUNCHES, JANUARY 2021-MARCH 2026

- TABLE 169 AMCOR PLC: DEALS, JANUARY 2021-MARCH 2026

- TABLE 170 AMCOR PLC: EXPANSIONS, JANUARY 2021-MARCH 2026

- TABLE 171 SEALED AIR: BUSINESS OVERVIEW

- TABLE 172 SEALED AIR: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 173 SEALED AIR: PRODUCT LAUNCHES, JANUARY 2021-MARCH 2026

- TABLE 174 SEALED AIR: DEALS, JANUARY 2021-MARCH 2026

- TABLE 175 SEALED AIR: EXPANSIONS, JANUARY 2021-MARCH 2026

- TABLE 176 MONDI: BUSINESS OVERVIEW

- TABLE 177 MONDI: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 178 MONDI: PRODUCT LAUNCHES, JANUARY 2021-MARCH 2026

- TABLE 179 MONDI: DEALS, JANUARY 2021-MARCH 2026

- TABLE 180 MONDI: EXPANSIONS, JANUARY 2021-MARCH 2026

- TABLE 181 TETRA LAVAL: COMPANY OVERVIEW

- TABLE 182 TETRA LAVAL: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 183 TETRA LAVAL: PRODUCT LAUNCHES, JANUARY 2021-MARCH 2026

- TABLE 184 TETRA LAVAL: DEALS, JANUARY 2021-MARCH 2026

- TABLE 185 TETRA LAVAL: EXPANSIONS, JANUARY 2021-MARCH 2026

- TABLE 186 HUHTAMAKI: COMPANY OVERVIEW

- TABLE 187 HUHTAMAKI: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 188 HUHTAMAKI: PRODUCT LAUNCHES, JANUARY 2021-MARCH 2026

- TABLE 189 HUHTAMAKI: DEALS, JANUARY 2021-MARCH 2026

- TABLE 190 HUHTAMAKI: EXPANSIONS, JANUARY 2021-MARCH 2026

- TABLE 191 TOYO SEIKAN GROUP HOLDINGS, LTD.: COMPANY OVERVIEW

- TABLE 192 TOYO SEIKAN GROUP HOLDINGS, LTD.: PRODUCTS/SOLUTIONS/ SERVICES OFFERED

- TABLE 193 CROWN: COMPANY OVERVIEW

- TABLE 194 CROWN: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 195 CROWN: DEALS, JANUARY 2021-MARCH 2026

- TABLE 196 CROWN: EXPANSIONS, JANUARY 2021-MARCH 2026

- TABLE 197 CONSTANTIA FLEXIBLES: COMPANY OVERVIEW

- TABLE 198 CONSTANTIA FLEXIBLES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 199 CONSTANTIA FLEXIBLES: DEALS, JANUARY 2021-MARCH 2026

- TABLE 200 GRAPHIC PACKAGING HOLDING COMPANY: COMPANY OVERVIEW

- TABLE 201 GRAPHIC PACKAGING HOLDING COMPANY: PRODUCTS/SOLUTIONS/ SERVICES OFFERED

- TABLE 202 GRAPHIC PACKAGING HOLDING COMPANY: PRODUCT LAUNCHES, JANUARY 2021-MARCH 2026

- TABLE 203 GRAPHIC PACKAGING HOLDING COMPANY: DEALS, JANUARY 2021-MARCH 2026

- TABLE 204 GRAPHIC PACKAGING HOLDING COMPANY: EXPANSIONS, JANUARY 2021-MARCH 2026

- TABLE 205 WINPAK LTD.: COMPANY OVERVIEW

- TABLE 206 WINPAK LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 207 WINPAK LTD.: EXPANSIONS, JANUARY 2021-MARCH 2026

- TABLE 208 AVERY DENNISON CORPORATION: COMPANY OVERVIEW

- TABLE 209 CCL INDUSTRIES: COMPANY OVERVIEW

- TABLE 210 PROAMPAC: COMPANY OVERVIEW

- TABLE 211 KLOCKNER PENTAPLAST: COMPANY OVERVIEW

- TABLE 212 COVERIS: COMPANY OVERVIEW

- TABLE 213 PPC FLEX COMPANY INC.: COMPANY OVERVIEW

- TABLE 214 MASTERPACK: COMPANY OVERVIEW

- TABLE 215 GRUPPO FABBRI: COMPANY OVERVIEW

- TABLE 216 EVERTIS: COMPANY OVERVIEW

- TABLE 217 FPS FLEXIBLE PACKAGING SOLUTIONS: COMPANY OVERVIEW

- TABLE 218 VARCODE: COMPANY OVERVIEW

- TABLE 219 INSIGNIA TECHNOLOGIES LTD.: COMPANY OVERVIEW

- TABLE 220 TIMESTRIP UK LTD: COMPANY OVERVIEW

- TABLE 221 ARIS PACK: COMPANY OVERVIEW

- TABLE 222 MULTISORB: COMPANY OVERVIEW

List of Figures

- FIGURE 1 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 KEY INSIGHTS AND MARKET HIGHLIGHTS

- FIGURE 3 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, 2025-2031

- FIGURE 4 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET (2020-2025)

- FIGURE 5 DISRUPTIVE TRENDS IMPACTING GROWTH OF ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET DURING FORECAST PERIOD

- FIGURE 6 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS IN ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, 2026-2031

- FIGURE 7 ASIA PACIFIC TO REGISTER HIGHEST GROWTH DURING FORECAST PERIOD

- FIGURE 8 HIGH DEMAND FOR ADVANCED PACKAGING IN FOOD SECTOR TO CREATE LUCRATIVE OPPORTUNITIES FOR MARKET PLAYERS

- FIGURE 9 FOOD AND US ACCOUNTED FOR LARGEST MARKET SHARES IN 2025

- FIGURE 10 PLASTICS DOMINATED ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET IN 2025

- FIGURE 11 FLEXIBLE PACKAGING SEGMENT DOMINATED ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET IN 2025

- FIGURE 12 MODIFIED ATMOSPHERE PACKAGING SEGMENT DOMINATED ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET IN 2025

- FIGURE 13 FOOD DOMINATED ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET IN 2025

- FIGURE 14 INDIA TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 15 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 16 INDIA'S PROCESSED FOOD EXPORTS, 2024-2025, %

- FIGURE 17 GLOBAL ECOMMERCE REVENUE FORECAST, F&B INDUSTRY, (USD BILLION), (2022-2027)

- FIGURE 18 INCREASING URBAN POPULATION TREND, 2020-2024, MILLION PERSONS

- FIGURE 19 GLOBAL BIOPLASTICS PRODUCTION EVOLUTION, 2024 VS. 2029

- FIGURE 20 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 21 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET: VALUE CHAIN ANALYSIS

- FIGURE 22 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET: ECOSYSTEM ANALYSIS

- FIGURE 23 EXPORT DATA FOR HS CODE 3923-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD MILLION)

- FIGURE 24 IMPORT DATA FOR HS CODE 3923-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD MILLION)

- FIGURE 25 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 26 INVESTMENT AND FUNDING SCENARIO, 2018-2025

- FIGURE 27 LIST OF MAJOR PATENTS FOR ADVANCED PACKAGING FOR FOOD & BEVERAGE, 2016-2025

- FIGURE 28 MAJOR PATENTS APPLIED AND GRANTED RELATED TO ADVANCED PACKAGING FOR FOOD & BEVERAGE, BY COUNTRY/REGION, 2016-2025

- FIGURE 29 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET DECISION-MAKING FACTORS

- FIGURE 30 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY APPLICATION

- FIGURE 31 KEY BUYING CRITERIA, BY APPLICATION

- FIGURE 32 ADOPTION BARRIERS & INTERNAL CHALLENGES

- FIGURE 33 METAL SEGMENT TO REGISTER HIGHEST GROWTH DURING FORECAST PERIOD

- FIGURE 34 FLEXIBLE PACKAGING SEGMENT TO REGISTER HIGHEST GROWTH DURING FORECAST PERIOD

- FIGURE 35 MODIFIED ATMOSPHERE PACKAGING SEGMENT TO REGISTER HIGHEST GROWTH DURING FORECAST PERIOD

- FIGURE 36 FOOD SEGMENT TO REGISTER HIGHEST GROWTH DURING FORECAST PERIOD

- FIGURE 37 INDIA TO BE FASTEST-GROWING MARKET DURING FORECAST PERIOD

- FIGURE 38 NORTH AMERICA LED ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET IN 2025

- FIGURE 39 NORTH AMERICA: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET SNAPSHOT

- FIGURE 40 EUROPE: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET SNAPSHOT

- FIGURE 41 ADVANCED PACKAGING FOR FOOD & BEVERAGE: MARKET SHARE ANALYSIS, 2025

- FIGURE 42 REVENUE ANALYSIS OF KEY COMPANIES IN ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET

- FIGURE 43 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET: COMPANY VALUATION, 2025

- FIGURE 44 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET: FINANCIAL MATRIX - EV/EBITDA RATIO, 2025

- FIGURE 45 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET: YEAR-TO-DATE PRICE AND FIVE-YEAR STOCK BETA, 2025

- FIGURE 46 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET: BRAND COMPARISON

- FIGURE 47 COMPANY EVALUATION MATRIX: ADVANCED PACKAGING MARKET FOR FOOD & BEVERAGE MARKET, 2025

- FIGURE 48 ADVANCED PACKAGING MARKET FOR FOOD & BEVERAGE MARKET: COMPANY FOOTPRINT, 2025

- FIGURE 49 SME MATRIX: ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET, 2025

- FIGURE 50 AMCOR PLC: COMPANY SNAPSHOT (2024)

- FIGURE 51 SEALED AIR: COMPANY SNAPSHOT

- FIGURE 52 MONDI: COMPANY SNAPSHOT

- FIGURE 53 TETRA LAVAL: COMPANY SNAPSHOT (2024)

- FIGURE 54 HUHTAMAKI: COMPANY SNAPSHOT

- FIGURE 55 TOYO SEIKAN GROUP HOLDINGS, LTD.: COMPANY SNAPSHOT (2024)

- FIGURE 56 CROWN: COMPANY SNAPSHOT

- FIGURE 57 GRAPHIC PACKAGING HOLDING COMPANY: COMPANY SNAPSHOT

- FIGURE 58 WINPAK LTD.: COMPANY SNAPSHOT

- FIGURE 59 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET: RESEARCH DESIGN

- FIGURE 60 BREAKDOWN OF INTERVIEWS WITH EXPERTS

- FIGURE 61 MARKET SIZE ESTIMATION: BOTTOM-UP APPROACH

- FIGURE 62 MARKET SIZE ESTIMATION: TOP-DOWN APPROACH

- FIGURE 63 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET: APPROACH 1

- FIGURE 64 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET: APPROACH 2

- FIGURE 65 ADVANCED PACKAGING FOR FOOD & BEVERAGE MARKET: DATA TRIANGULATION

半導體先進封裝市場預測至2034年-按封裝類型、材料、應用、最終用戶和地區分類的全球分析

半導體先進封裝市場預測至2034年-按封裝類型、材料、應用、最終用戶和地區分類的全球分析 2026-2030年全球先進半導體封裝市場

2026-2030年全球先進半導體封裝市場 晶片封裝及測試技術市場:依封裝技術、測試類型、最終用戶、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測先進封裝和晶片設計市場預測至2034年-按封裝技術、晶片整合方法、應用、最終用戶和地區分類的全球分析晶片封裝市場預測至2034年-全球分析(依封裝技術、互連技術、晶片類型、材料類型、應用、最終使用者和地區分類)

晶片封裝及測試技術市場:依封裝技術、測試類型、最終用戶、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測先進封裝和晶片設計市場預測至2034年-按封裝技術、晶片整合方法、應用、最終用戶和地區分類的全球分析晶片封裝市場預測至2034年-全球分析(依封裝技術、互連技術、晶片類型、材料類型、應用、最終使用者和地區分類) 先進半導體封裝市場:2026-2032年全球市場預測(依封裝技術、組件、佈線方式、材料類型、間距、最終用途產業及客戶類型分類)

先進半導體封裝市場:2026-2032年全球市場預測(依封裝技術、組件、佈線方式、材料類型、間距、最終用途產業及客戶類型分類) 先進半導體封裝市場機會、成長要素、產業趨勢分析及2026年至2035年預測

先進半導體封裝市場機會、成長要素、產業趨勢分析及2026年至2035年預測 先進半導體封裝市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、材料類型、裝置、製程分類先進半導體封裝市場預測至2034年:按封裝類型、材料、製程、互連技術、最終用戶和地區分類的全球分析先進半導體封裝市場,按封裝類型、封裝材料、製造方法、最終用戶、國家和地區分類 - 2025 年至 2032 年全球產業分析、市場規模、市場佔有率及預測

先進半導體封裝市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、材料類型、裝置、製程分類先進半導體封裝市場預測至2034年:按封裝類型、材料、製程、互連技術、最終用戶和地區分類的全球分析先進半導體封裝市場,按封裝類型、封裝材料、製造方法、最終用戶、國家和地區分類 - 2025 年至 2032 年全球產業分析、市場規模、市場佔有率及預測