|

市場調查報告書

商品編碼

2061494

太陽能追蹤器市場機會、成長促進因素、產業趨勢分析及預測(2026-2035)Solar Tracker Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

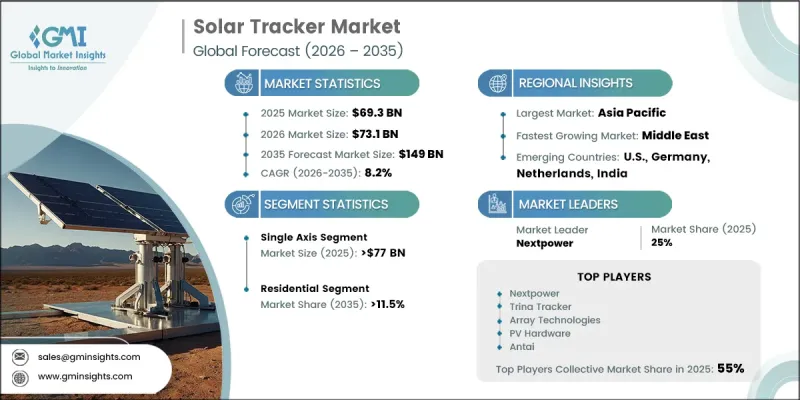

2025年全球太陽能追蹤器市場價值為693億美元,預計到2035年將以8.2%的複合年成長率成長至1,490億美元。

太陽能追蹤器是一種先進的系統,旨在全天調整太陽能電池板和反射器的方向,使其始終朝向太陽,從而最大限度地提高太陽能發電量。這些系統透過維持最佳的太陽輻射條件,在提高光電裝置的效率和生產力方面發揮著至關重要的作用。全球對可再生能源基礎設施投資的增加以及對提高可再生能源發電效率的日益重視,正顯著推動市場擴張。大型太陽能發電工程的日益普及和太陽能追蹤技術成本的下降,進一步促進了行業成長。與固定傾角光伏系統相比,太陽能追蹤器能夠顯著提高發電量,因此在大型商業可再生能源專案中越來越受歡迎。智慧電網整合、物聯網 (IoT) 技術和自動化監控系統的進步,也提高了現代太陽能追蹤器的運作性能和可靠性。此外,世界各國政府和組織不斷加強的永續性措施和排放碳目標,正在加速對高效能光電技術的需求,從而支持市場的長期成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 693億美元 |

| 預測金額 | 1490億美元 |

| 複合年成長率 | 8.2% |

太陽能追蹤器市場也受益於材料技術和控制系統的持續創新,這些創新旨在提高耐用性、運作效率和長期可靠性。降低維護成本和提升能源最佳化能力的日益重視,進一步推動了先進太陽能追蹤系統在住宅、商業和公用事業規模應用中的普及。可再生能源的日益普及和對智慧能源管理解決方案需求的成長,也進一步促進了全球市場的動態。

預計到2035年,單軸太陽能追蹤器市場規模將達到770億美元。單軸太陽能追蹤器之所以持續保持高普及率,是因為與固定式安裝相比,它們能夠顯著提高太陽能板的效率和發電量。設計和工程技術的進步使得這些系統能夠實現更高的運作可靠性、更強的耐用性和更低的維護需求。對經濟高效的光伏最佳化解決方案日益成長的需求,以及發電工程投資回報率(ROI)的提高,進一步推動了單軸追蹤技術在全球可再生能源領域的廣泛應用。

預計到2035年,住宅太陽能市場將以11.5%的複合年成長率成長。人們對住宅太陽能發電的興趣日益濃厚,加上創新的資金籌措模式和靈活的租賃方案,正推動住宅投資先進的太陽能追蹤技術。地方太陽能舉措和可再生能源共用計畫也促進了住宅太陽能追蹤系統的部署。此外,太陽能追蹤器與智慧家庭技術的整合,使住宅能夠更有效地改善能源管理、監控系統性能並最佳化電力消耗。

預計到2035年,美國太陽能追蹤器市場規模將達到75億美元。美國市場成長的驅動力包括有利的可再生能源政策、對太陽能發電投資的增加以及大型太陽能發電工程的擴張。豐富的太陽能資源和太陽能追蹤器系統的持續技術進步進一步推動了全部區域市場的擴張。此外,經濟高效且易於使用的住宅和商業應用追蹤技術的日益普及也增強了美國可再生能源產業的需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系統

- 原物料供應商

- 零件製造商

- 追蹤器組裝和整合

- 銷售代理和系統整合商

- EPC承包商和專案開發商

- 最終用戶

- 監理情勢

- 全球政策和獎勵計劃

- 淨計量及上網電價制度

- 排碳權和可再生能源認證標準

- 貿易政策與反傾銷法規

- 技術與創新展望

- 物聯網和數位整合在追蹤系統中的應用

- 先進材料提升耐用性

- 預測性維護技術

- 連排式建築的創新

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 波特的分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- PESTLE分析

- 太陽能發電工程資料庫

- 手術

- 估計

- 成本結構分析

- 材料清單細分

- 製造成本和學習曲線的趨勢

- 系統平衡(BOS)成本趨勢

- 價格趨勢分析

- 對過去價格趨勢的分析

- 定價策略:按業務類型分類

- 貿易數據分析

- 進出口額趨勢

- 主要貿易路線及關稅的影響

- 生產能力和運轉率

- 各國具體生產能力

- 運轉率和擴張計劃

- 人工智慧和生成式人工智慧對市場的影響

- 預測性維護和故障檢測

- 電網最佳化和負載預測

- 利用數位雙胞胎進行模擬和測試

- 風險、限制和監管考量

- 新機會與趨勢

- 數位化和物聯網整合

- 投資分析及未來展望

第4章 競爭情勢

- 介紹

- 企業市佔率分析:按地區分類

- 北美洲

- 歐洲

- 亞太地區

- 中東

- 非洲

- 拉丁美洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

- 按公司規模進行基準測試

- 排名分類標準與遴選標準

- 按銷售額、地區和創新能力分類的層級定位矩陣。

第5章 市場規模及預測:依產品分類,2022-2035年

- 單軸

- 水平的

- 垂直的

- 雙軸

第6章 市場規模及預測:依技術分類,2022-2035年

- PV

- CSP

第7章 市場規模及預測:依應用領域分類,2022-2035年

- 住宅

- 商業和工業用途

- 公用事業

第8章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 法國

- 荷蘭

- 德國

- 瑞典

- 西班牙

- 奧地利

- 亞太地區

- 中國

- 日本

- 韓國

- 澳洲

- 印度

- 中東

- 沙烏地阿拉伯

- UAE

- 約旦

- 以色列

- 非洲

- 南非

- 埃及

- 阿爾及利亞

- 奈及利亞

- 摩洛哥

- 拉丁美洲

- 巴西

- 智利

第9章:公司簡介

- Arcelormittal

- Array Technologies

- Arctech

- Antai

- All Earth Renewables

- Clenergy

- Convert Italia

- Degerenergie

- Flexrack

- FTC Solar

- GameChange Solar

- Gonvarri Solar Steel

- Haosolar

- Ideematec

- Mecasolar

- Nclave

- Nextpower

- Powerway Renewable Energy

- PVHardware

- Solar Steel

- Scorpius Trackers

- SmartTrak Solar Systems

- Soltec

- STI Norland

- Valmont Industries

- Versolsolar

- Trina Solar

The Global Solar Tracker Market was valued at USD 69.3 billion in 2025 and is estimated to grow at a CAGR of 8.2% to reach USD 149 billion by 2035.

Solar trackers are advanced systems designed to position solar panels or reflective surfaces toward the sun throughout the day to maximize solar energy generation. These systems play a crucial role in improving the efficiency and productivity of solar power installations by maintaining optimal solar exposure. Rising global investments in renewable energy infrastructure and increasing focus on improving solar power generation efficiency are significantly driving market expansion. The growing adoption of utility-scale solar projects and the declining cost of solar tracking technologies are further strengthening industry growth. Solar trackers can substantially improve electricity generation compared to fixed-tilt solar systems, making them increasingly attractive for large-scale and commercial renewable energy projects. Advancements in smart grid integration, Internet of Things technologies, and automated monitoring systems are also enhancing the operational performance and reliability of modern solar trackers. In addition, rising sustainability initiatives and carbon reduction targets established by governments and organizations worldwide are accelerating demand for high-efficiency solar energy technologies, supporting long-term market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $69.3 Billion |

| Forecast Value | $149 Billion |

| CAGR | 8.2% |

The solar tracker market is also benefiting from continuous innovation in material technologies and control systems designed to improve durability, operational efficiency, and long-term reliability. Increasing emphasis on reducing maintenance costs and improving energy optimization capabilities is encouraging broader adoption of advanced solar tracking systems across residential, commercial, and utility-scale applications. Expanding renewable energy deployment and growing demand for intelligent energy management solutions are further contributing to positive market dynamics worldwide.

The single-axis segment is expected to reach USD 77 billion by 2035. Single-axis solar trackers continue to witness strong adoption due to their ability to significantly improve solar panel efficiency and energy output compared to fixed-tilt installations. These systems offer enhanced operational reliability, improved durability, and lower maintenance requirements because of advancements in design and engineering technologies. Increasing demand for cost-effective solar optimization solutions and stronger return on investment for solar energy projects are further supporting the widespread deployment of single-axis tracking technologies across the global renewable energy sector.

The residential segment is projected to grow at a CAGR of 11.5% through 2035. Growing interest in residential solar energy adoption, combined with innovative financing models and flexible leasing options, is encouraging homeowners to invest in advanced solar tracking technologies. Community-based solar initiatives and shared renewable energy programs are also contributing to increased deployment of residential solar tracker systems. In addition, integration of solar trackers with smart home technologies is enabling homeowners to improve energy management, monitor system performance, and optimize electricity consumption more effectively.

U.S. Solar Tracker Market is anticipated to reach USD 7.5 billion by 2035. Market growth across the United States is being supported by favorable renewable energy policies, increasing solar energy investments, and expanding deployment of utility-scale solar projects. Strong solar generation potential and continuous technological advancements in solar tracking systems are further contributing to market expansion throughout the region. The growing availability of cost-efficient and user-friendly tracking technologies for residential and commercial applications is also strengthening demand across the U.S. renewable energy industry.

Major companies operating in the Solar Tracker Market include ArcelorMittal, Array Technologies, Arctech, All Earth Renewables, Convert Italia, Degerenergie GmbH, GameChange Solar, Gonvarri Solar Steel, Haosolar, Ideematec, Mecasolar, Nclave, Nextpower, Powerway Renewable Energy, PVHardware, Scorpius Trackers, SmartTrak Solar Systems, Soltec, STI Norland, SunPower Corporation, and Trina Solar. Companies operating in the solar tracker market are implementing multiple strategic initiatives to strengthen their market presence and improve competitive positioning globally. Leading industry participants are investing heavily in research and development activities to introduce advanced tracking systems with enhanced efficiency, durability, and intelligent automation capabilities. Strategic partnerships, acquisitions, and collaborations with renewable energy developers are helping companies expand their global footprint and strengthen project portfolios. Organizations are also focusing on integrating smart monitoring technologies, artificial intelligence, and IoT-enabled control systems to improve energy optimization and operational performance. Increasing investments in lightweight materials and cost-efficient manufacturing processes are further supporting product innovation and scalability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360-degree synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Technology trends

- 2.4 Product trends

- 2.5 Application trends

- 2.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Raw Material Suppliers

- 3.1.2 Component Manufacturers

- 3.1.3 Tracker assembly & integration

- 3.1.4 Distributors & system integrators

- 3.1.5 EPC contractors & project developers

- 3.1.6 End users

- 3.2 Regulatory landscape

- 3.2.1 Global policy & incentive programs

- 3.2.2 Net metering & feed-in tariff mechanisms

- 3.2.3 Carbon credit & renewable energy certification standards

- 3.2.4 Trade policies & anti-dumping regulations

- 3.3 Technology & innovation landscape

- 3.3.1 IoT & digital integration in tracking systems

- 3.3.2 Advanced materials for durability enhancement

- 3.3.3 Predictive maintenance technologies

- 3.3.4 Linked-row architecture innovations

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

- 3.7.1 Political factors

- 3.7.2 Economic factors

- 3.7.3 Social factors

- 3.7.4 Technological factors

- 3.7.5 Legal factors

- 3.7.6 Environmental factors

- 3.8 Solar PV project database

- 3.8.1 Operational

- 3.8.2 Estimated

- 3.9 Cost structure analysis

- 3.9.1 Bill of Materials Breakdown

- 3.9.2 Manufacturing Cost Evolution & Learning Curve

- 3.9.3 Balance of System Cost Trends

- 3.10 Price trend analysis (Driven by Primary Research)

- 3.10.1 Historical price trend analysis

- 3.10.2 Pricing strategy by player type

- 3.11 Trade data analysis (Driven by Primary Research)

- 3.11.1 Import/export value trends

- 3.11.2 Key trade corridors & tariff impact

- 3.12 Production capacity & utilization (Driven by Primary Research)

- 3.12.1 Production capacity by country

- 3.12.2 Utilization rates and expansion pipeline

- 3.13 Impact of AI & generative AI on the market [SOLUTION CORE]

- 3.13.1 Predictive maintenance & fault detection

- 3.13.2 Grid optimization & load forecasting

- 3.13.3 Digital twin simulation & testing

- 3.13.4 Risks, limitations & regulatory considerations

- 3.14 Emerging opportunities & trends

- 3.15 Digitalization & IoT integration

- 3.16 Investment analysis and future outlook

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East

- 4.2.5 Africa

- 4.2.6 Latin America

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Product, 2022 - 2035 (USD Billion & MW)

- 5.1 Key trends

- 5.2 Single axis

- 5.2.1 Horizontal

- 5.2.2 Vertical

- 5.3 Dual axis

Chapter 6 Market Size and Forecast, By Technology, 2022 - 2035 (USD Billion & MW)

- 6.1 Key trends

- 6.2 PV

- 6.3 CSP

Chapter 7 Market Size and Forecast, By Application, 2022 - 2035 (USD Billion & MW)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial & industrial

- 7.4 Utility

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Billion & MW)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Netherlands

- 8.3.4 Germany

- 8.3.5 Sweden

- 8.3.6 Spain

- 8.3.7 Austria

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 South Korea

- 8.4.4 Australia

- 8.4.5 India

- 8.5 Middle East

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Jordan

- 8.5.4 Israel

- 8.6 Africa

- 8.6.1 South Africa

- 8.6.2 Egypt

- 8.6.3 Algeria

- 8.6.4 Nigeria

- 8.6.5 Morocco

- 8.7 Latin America

- 8.7.1 Brazil

- 8.7.2 Chile

Chapter 9 Company Profiles

- 9.1 Arcelormittal

- 9.2 Array Technologies

- 9.3 Arctech

- 9.4 Antai

- 9.5 All Earth Renewables

- 9.6 Clenergy

- 9.7 Convert Italia

- 9.8 Degerenergie

- 9.9 Flexrack

- 9.10 FTC Solar

- 9.11 GameChange Solar

- 9.12 Gonvarri Solar Steel

- 9.13 Haosolar

- 9.14 Ideematec

- 9.15 Mecasolar

- 9.16 Nclave

- 9.17 Nextpower

- 9.18 Powerway Renewable Energy

- 9.19 PVHardware

- 9.20 Solar Steel

- 9.21 Scorpius Trackers

- 9.22 SmartTrak Solar Systems

- 9.23 Soltec

- 9.24 STI Norland

- 9.25 Valmont Industries

- 9.26 Versolsolar

- 9.27 Trina Solar

太陽能追蹤器市場-2026-2032年全球市場預測雙軸太陽能追蹤器市場—2026-2032年全球市場預測

太陽能追蹤器市場-2026-2032年全球市場預測雙軸太陽能追蹤器市場—2026-2032年全球市場預測 雙軸太陽能追蹤器市場規模、佔有率和趨勢分析報告:按類型、應用、地區和細分市場分類(2026-2033 年)太陽能追蹤器市場規模、佔有率和趨勢分析報告:按技術、類型、應用、地區和細分市場分類(2026-2033 年)

雙軸太陽能追蹤器市場規模、佔有率和趨勢分析報告:按類型、應用、地區和細分市場分類(2026-2033 年)太陽能追蹤器市場規模、佔有率和趨勢分析報告:按技術、類型、應用、地區和細分市場分類(2026-2033 年) 單軸太陽能追蹤器市場預測至2034年—按產品類型、旋轉軸、應用和區域分類的全球分析

單軸太陽能追蹤器市場預測至2034年—按產品類型、旋轉軸、應用和區域分類的全球分析 太陽能追蹤器市場規模、佔有率和成長分析:按類型、軸類型、應用和地區分類-2026-2033年產業預測

太陽能追蹤器市場規模、佔有率和成長分析:按類型、軸類型、應用和地區分類-2026-2033年產業預測 太陽能追蹤器市場規模、佔有率、趨勢和預測:按類型、追蹤方法、技術、應用和地區分類(2026-2034 年)

太陽能追蹤器市場規模、佔有率、趨勢和預測:按類型、追蹤方法、技術、應用和地區分類(2026-2034 年) 公用事業太陽能追蹤器市場機會、成長要素、產業趨勢分析及2026-2035年預測商業和工業太陽能追蹤器的市場機會、成長要素、產業趨勢分析和預測(2026-2035 年)住宅太陽能追蹤器市場機會、成長要素、產業趨勢分析及2026-2035年預測

公用事業太陽能追蹤器市場機會、成長要素、產業趨勢分析及2026-2035年預測商業和工業太陽能追蹤器的市場機會、成長要素、產業趨勢分析和預測(2026-2035 年)住宅太陽能追蹤器市場機會、成長要素、產業趨勢分析及2026-2035年預測