|

市場調查報告書

商品編碼

2061484

太陽能發電組件市場機會、成長要素、產業趨勢分析及2026-2035年預測Solar PV Module Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

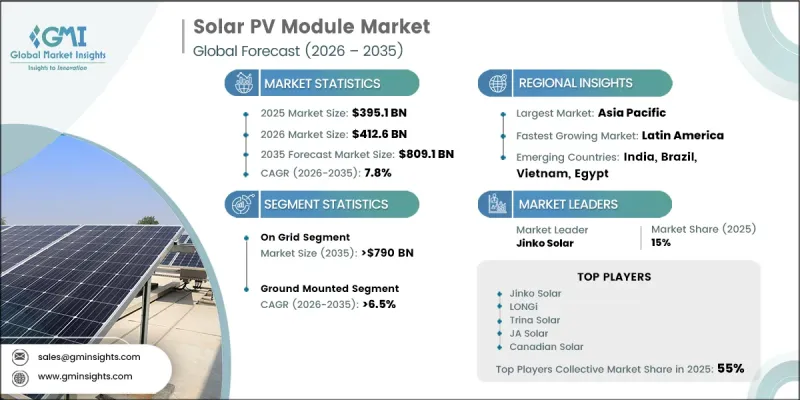

預計到 2025 年,全球太陽能模組市場規模將達到 3,951 億美元,並預計以 7.8% 的複合年成長率成長,到 2035 年達到 8,091 億美元。

太陽能發電組件旨在將太陽光直接轉化為電能,主要採用嵌入矽等半導體材料中的太陽能電池。這些組件的工作原理是捕獲太陽輻射並將其轉化為直流電,並透過互連陣列擴展為大規模的系統,從而滿足各種能源需求。市場成長的主要驅動力是技術成本的下降,而技術成本的下降又得益於製造效率的提升、技術創新和安裝方法的最佳化。政府透過獎勵、政策框架和財政支持計畫加強對併網太陽能發電工程的支持力度,進一步提升了投資吸引力。全球對氣候變遷日益成長的認知以及對減少溫室氣體排放緊迫性的日益理解,也在加速向可再生能源的轉型。此外,越來越多的企業、政府和家庭將太陽能解決方案納入永續性策略,這進一步刺激了需求,並支持了市場的長期擴張。預計向清潔能源系統的持續轉型以及有利的法規環境將使全球太陽能發電的普及保持強勁的成長勢頭。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 3951億美元 |

| 預測金額 | 8091億美元 |

| 複合年成長率 | 7.8% |

預計到2035年,併網太陽能市場規模將達到7,900億美元,主要得益於光學模組效率的持續提升,包括單晶和雙面技術的進步,這些進步提高了能源輸出和系統性能。補貼、稅收優惠和退稅計畫等扶持性政策框架正在加速許多地區併網太陽能發電系統的普及。主要經濟體系統性獎勵機制的擴展進一步推動了併網太陽能發電基礎設施的部署。

預計到2035年,地面光伏發電(TSP)市場將以6.5%的複合年成長率成長。高效能光電技術的進步,包括單晶矽和雙面光電模組,提高了面積的發電量,推動了這項成長。薄膜光伏技術的改進也促進了這一成長,其輕巧的結構和柔軟性使其適用於大規模安裝。

預計到2035年,美國太陽能模組市場規模將達570億美元。到2025年,北美將佔全球市場佔有率的9.4%,反映出該地區正經歷從依賴進口到擴大國內製造能力的結構性轉變。政策支持措施正在顯著加速產能擴張,並加強區域太陽能製造生態系統。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系統

- 原物料供應商

- 零件製造商

- 模組製造商

- 銷售代理和系統整合商

- 最終用戶和專案開發人員

- 監理情勢

- 全球政策和獎勵計劃

- 淨計量及上網電價制度

- 排碳權和可再生能源認證標準

- 貿易政策與反傾銷法規

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 波特的分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- PESTLE分析

- 成本結構分析

- 材料清單細分

- 製造成本和學習曲線的趨勢

- 系統平衡(BOS)成本趨勢

- 價格趨勢分析

- 對過去價格趨勢的分析

- 定價策略:按業務類型分類

- 貿易數據分析

- 進出口額趨勢

- 主要貿易路線及關稅的影響

- 生產能力和運轉率

- 各國具體生產能力

- 運轉率和擴張計劃

- 人工智慧和生成式人工智慧對市場的影響

- 預測性維護和故障檢測

- 電網最佳化和負載預測

- 利用數位雙胞胎進行模擬和測試

- 風險、限制和監管考量

- 新機會和趨勢

- 數位化和物聯網整合

- 投資分析及未來展望

第4章 競爭情勢

- 介紹

- 企業市佔率分析:按地區分類

- 北美洲

- 歐洲

- 亞太地區

- 中東

- 非洲

- 拉丁美洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

- 按公司規模進行基準測試

- 排名分類標準與遴選標準

- 按銷售額、地區和創新能力分類的層級定位矩陣。

第5章 市場規模及預測:依技術分類,2022-2035年

- 薄膜

- 碲化鎘

- 非晶質

- 銅銦鎵二硒

- 晶體矽

第6章 市場規模與預測:依產品分類,2022-2035年

- 單晶

- PERC

- TopCon

- HJT

- IBC/TBC

- 多晶

第7章 市場規模及預測:依性別分類的互聯互通情況,2021-2034年

- 並網型

- 離網

第8章 市場規模及預測:依安裝方式分類,2022-2035年

- 地面安裝

- 屋頂

第9章 市場規模及預測:依最終用途分類,2022-2035年

- 住宅

- 商業和工業

- 公用事業

第10章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 奧地利

- 挪威

- 丹麥

- 芬蘭

- 法國

- 德國

- 義大利

- 瑞士

- 西班牙

- 瑞典

- 英國

- 荷蘭

- 波蘭

- 比利時

- 愛爾蘭

- 波羅的海國家

- 葡萄牙

- 亞太地區

- 中國

- 澳洲

- 印度

- 日本

- 韓國

- 泰國

- 菲律賓

- 越南

- 馬來西亞

- 新加坡

- 中東

- 以色列

- 沙烏地阿拉伯

- UAE

- 約旦

- 阿曼

- 科威特

- 土耳其

- 非洲

- 南非

- 埃及

- 阿爾及利亞

- 奈及利亞

- 摩洛哥

- 拉丁美洲

- 巴西

- 智利

- 阿根廷

- 秘魯

第11章:公司簡介

- Aiko Solar Technology

- Adani Solar

- CsunSolarTech

- Canadian Solar

- DAS Solar

- Emmvee Solar

- First Solar

- GCL-SI

- Huasan Energy

- Hanwha Group

- Jinko Solar

- JA SOLAR Technology

- LONGi

- RENESOLA

- Risen Energy

- REC Solar Holdings

- SunPower Corporation

- Solaria Corporation

- Trina Solar

- Tongwei Solar

- Vikram Solar

- Waaree Energies

- Yingli Energy

The Global Solar PV Module Market was valued at USD 395.1 billion in 2025 and is estimated to grow at a CAGR of 7.8% to reach USD 809.1 billion by 2035.

Solar PV modules are designed to convert sunlight directly into electricity using photovoltaic cells embedded within semiconductor-based materials, primarily silicon. These modules function by capturing solar radiation and converting it into direct current electricity, which can then be scaled into larger systems through interconnected arrays to meet diverse energy requirements. The market is strongly influenced by falling technology costs driven by manufacturing efficiency improvements, technological innovation, and optimized installation methods. Expanding government support through incentives, policy frameworks, and financial assistance programs for grid-connected solar projects is further strengthening investment attractiveness. Increasing global awareness of climate change and the urgent need to reduce greenhouse gas emissions is also accelerating the shift toward renewable energy adoption. In addition, corporations, governments, and households are increasingly integrating solar solutions into their sustainability strategies, further boosting demand and supporting long-term market expansion. The continuous transition toward cleaner energy systems and supportive regulatory environments is expected to sustain strong growth momentum across global solar PV deployments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $395.1 Billion |

| Forecast Value | $809.1 Billion |

| CAGR | 7.8% |

The on-grid segment is projected to reach USD 790 billion by 2035, driven by continuous improvements in solar module efficiency, including advancements in monocrystalline and bifacial technologies that enhance energy output and system performance. Supportive policy frameworks, including subsidies, tax benefits, and rebate programs, are encouraging widespread adoption of grid-connected solar systems across multiple regions. The expansion of structured incentive mechanisms across major economies is further strengthening the deployment of on-grid solar infrastructure.

The ground-mounted solar segment is expected to grow at a CAGR of 6.5% through 2035. Rising deployment is supported by advancements in high-efficiency photovoltaic technologies, including monocrystalline and bifacial panels, which enable higher energy output per installation area. Improvements in thin-film photovoltaic technology are also contributing to increased adoption due to their lightweight structure and flexibility, making them suitable for large-scale installations.

U.S. Solar PV Module Market is projected to reach USD 57 billion by 2035. North America accounted for 9.4% of the global market share in 2025, reflecting a structural shift from import reliance toward expanding domestic manufacturing capabilities. Policy support mechanisms have significantly accelerated production capacity growth, strengthening the regional solar manufacturing ecosystem.

Major companies operating in the Global Solar PV Module Industry include Jinko Solar, Trina Solar, Canadian Solar, First Solar, LONGi, JA Solar Technology, Hanwha Group, Risen Energy, REC Group, SunPower Corporation, Vikram Solar, Adani Solar, Tongwei Solar, Yingli Energy, Waaree Energies, DAS Solar, Emmvee Solar, GCL-SI, Aiko Solar Technology, CsunSolarTech, Huasan Energy, Renesola, Solaria Corporation, and SunPower Corporation. Companies operating in the Solar PV Module Market are actively adopting diversified strategies to strengthen their global competitiveness and market presence. Industry participants are investing heavily in advanced photovoltaic technologies to improve conversion efficiency, durability, and overall system performance. Expansion of large-scale manufacturing capacities is being prioritized to achieve cost advantages and meet rising global demand. Strategic partnerships with energy developers, utilities, and government-backed projects are helping companies expand distribution networks and project pipelines. Firms are also focusing on vertical integration to enhance supply chain control and reduce production costs. Continuous research and development efforts are enabling innovation in next-generation solar technologies, including high-efficiency cell architectures and lightweight module designs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360-degree synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Technology trends

- 2.4 Product trends

- 2.5 Mounting trends

- 2.6 Connectivity trends

- 2.7 End Use trends

- 2.8 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Raw Material Suppliers

- 3.1.2 Component Manufacturers

- 3.1.3 Module Manufacturers

- 3.1.4 Distributors & System Integrators

- 3.1.5 End Users & Project Developers

- 3.2 Regulatory landscape

- 3.2.1 Global Policy & Incentive Programs

- 3.2.2 Net Metering & Feed-in Tariff Mechanisms

- 3.2.3 Carbon Credit & Renewable Energy Certification Standards

- 3.2.4 Trade Policies & Anti-Dumping Regulations

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis

- 3.7.1 Bill of Materials Breakdown

- 3.7.2 Manufacturing Cost Evolution & Learning Curve

- 3.7.3 Balance of System Cost Trends

- 3.8 Price trend analysis (Driven by Primary Research)

- 3.8.1 Historical price trend analysis

- 3.8.2 Pricing strategy by player type

- 3.9 Trade data analysis (Driven by Primary Research)

- 3.9.1 Import/export value trends

- 3.9.2 Key trade corridors & tariff impact

- 3.10 Production capacity & utilization (Driven by Primary Research)

- 3.10.1 Production capacity by country

- 3.10.2 Utilization rates and expansion pipeline

- 3.11 Impact of AI & generative AI on the market [SOLUTION CORE]

- 3.11.1 Predictive maintenance & fault detection

- 3.11.2 Grid optimization & load forecasting

- 3.11.3 Digital twin simulation & testing

- 3.11.4 Risks, limitations & regulatory considerations

- 3.12 Emerging opportunities & trends

- 3.13 Digitalization & IoT integration

- 3.14 Investment analysis and future outlook

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East

- 4.2.5 Africa

- 4.2.6 Latin America

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Technology, 2022 - 2035 (USD Billion & MW)

- 5.1 Key trends

- 5.2 Thin Film

- 5.2.1 Cadmium Telluride

- 5.2.2 Amorphous Silicon

- 5.2.3 Copper Indium Gallium Diselenide

- 5.3 Crystalline Silicon

Chapter 6 Market Size and Forecast, By Product, 2022 - 2035 (USD Billion & MW)

- 6.1 Key trends

- 6.2 Monocrystalline

- 6.2.1 PERC

- 6.2.2 TopCon

- 6.2.3 HJT

- 6.2.4 IBC/TBC

- 6.3 Polycrystalline

Chapter 7 Market Size and Forecast, By Connectivity, 2021 - 2034 (USD Billion & MW)

- 7.1 Key trends

- 7.2 On Grid

- 7.3 Off Grid

Chapter 8 Market Size and Forecast, By Mounting, 2022 - 2035 (USD Billion & MW)

- 8.1 Key trends

- 8.2 Ground Mounted

- 8.3 Roof Top

Chapter 9 Market Size and Forecast, By End Use, 2022 - 2035 (USD Billion & MW)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial & Industrial

- 9.4 Utility

Chapter 10 Market Size and Forecast, By Region, 2022 - 2035 (USD Billion & MW)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Austria

- 10.3.2 Norway

- 10.3.3 Denmark

- 10.3.4 Finland

- 10.3.5 France

- 10.3.6 Germany

- 10.3.7 Italy

- 10.3.8 Switzerland

- 10.3.9 Spain

- 10.3.10 Sweden

- 10.3.11 UK

- 10.3.12 Netherlands

- 10.3.13 Poland

- 10.3.14 Belgium

- 10.3.15 Ireland

- 10.3.16 Baltics

- 10.3.17 Portugal

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Australia

- 10.4.3 India

- 10.4.4 Japan

- 10.4.5 South Korea

- 10.4.6 Thailand

- 10.4.7 Philippines

- 10.4.8 Vietnam

- 10.4.9 Malaysia

- 10.4.10 Singapore

- 10.5 Middle East

- 10.5.1 Israel

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

- 10.5.4 Jordan

- 10.5.5 Oman

- 10.5.6 Kuwait

- 10.5.7 Turkey

- 10.6 Africa

- 10.6.1 South Africa

- 10.6.2 Egypt

- 10.6.3 Algeria

- 10.6.4 Nigeria

- 10.6.5 Morocco

- 10.7 Latin America

- 10.7.1 Brazil

- 10.7.2 Chile

- 10.7.3 Argentina

- 10.7.4 Peru

Chapter 11 Company Profiles

- 11.1 Aiko Solar Technology

- 11.2 Adani Solar

- 11.3 CsunSolarTech

- 11.4 Canadian Solar

- 11.5 DAS Solar

- 11.6 Emmvee Solar

- 11.7 First Solar

- 11.8 GCL-SI

- 11.9 Huasan Energy

- 11.10 Hanwha Group

- 11.11 Jinko Solar

- 11.12 JA SOLAR Technology

- 11.13 LONGi

- 11.14 RENESOLA

- 11.15 Risen Energy

- 11.16 REC Solar Holdings

- 11.17 SunPower Corporation

- 11.18 Solaria Corporation

- 11.19 Trina Solar

- 11.20 Tongwei Solar

- 11.21 Vikram Solar

- 11.22 Waaree Energies

- 11.23 Yingli Energy

太陽能組件材料市場預測(2034 年)—按組件、材料類型、組件技術、應用和地區分類的全球分析

太陽能組件材料市場預測(2034 年)—按組件、材料類型、組件技術、應用和地區分類的全球分析 太陽能發電系統平衡市場-2026-2032年全球市場預測太陽能發電工程、採購和施工 (EPC) 市場:2026-2032 年全球市場預測(按服務類型、太陽光電技術、追蹤器類型、容量、安裝類型和最終用途分類)全球公用事業規模太陽能發電市場預測至2034年—按安裝類型、容量範圍、所有權/營運、技術、應用和地區分類的分析

太陽能發電系統平衡市場-2026-2032年全球市場預測太陽能發電工程、採購和施工 (EPC) 市場:2026-2032 年全球市場預測(按服務類型、太陽光電技術、追蹤器類型、容量、安裝類型和最終用途分類)全球公用事業規模太陽能發電市場預測至2034年—按安裝類型、容量範圍、所有權/營運、技術、應用和地區分類的分析 屋頂太陽能發電組件市場機會、成長要素、產業趨勢分析及2026-2035年預測。

屋頂太陽能發電組件市場機會、成長要素、產業趨勢分析及2026-2035年預測。 太陽能板市場規模、佔有率和成長分析:按技術類型、併網方式、安裝類型、安裝結構、電池類型、輸出和地區分類-2026-2033年產業預測

太陽能板市場規模、佔有率和成長分析:按技術類型、併網方式、安裝類型、安裝結構、電池類型、輸出和地區分類-2026-2033年產業預測 太陽能發電組件市場-全球產業規模、佔有率、趨勢、機會和預測:按技術、產品、連接方式、安裝方式、最終用途、地區和競爭格局分類,2021-2031年住宅太陽能發電組件市場機會、成長要素、產業趨勢分析及2026-2035年預測。商業及工業太陽能發電組件市場機會、成長要素、產業趨勢分析及2026-2035年預測

太陽能發電組件市場-全球產業規模、佔有率、趨勢、機會和預測:按技術、產品、連接方式、安裝方式、最終用途、地區和競爭格局分類,2021-2031年住宅太陽能發電組件市場機會、成長要素、產業趨勢分析及2026-2035年預測。商業及工業太陽能發電組件市場機會、成長要素、產業趨勢分析及2026-2035年預測 全球太陽能材料,2025-2032年

全球太陽能材料,2025-2032年