|

市場調查報告書

商品編碼

2045823

狗鞋類市場機會、成長要素、產業趨勢分析及2026-2035年預測Dog Footwear Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

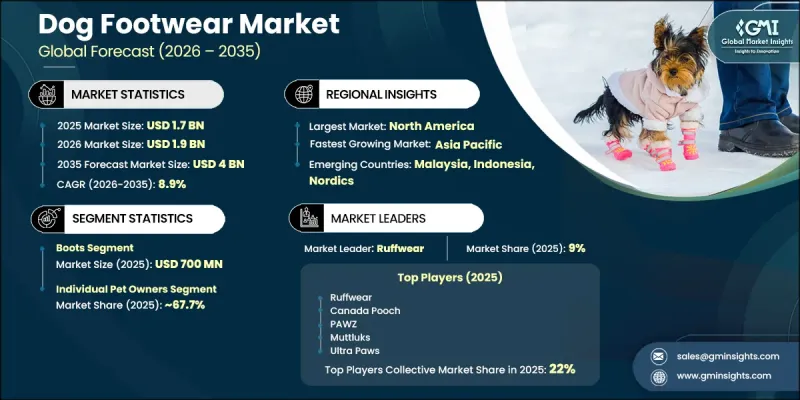

2025年全球狗鞋類市場價值為17億美元,預計2035年將以8.9%的複合年成長率成長至40億美元。

由於寵物「擬人化」趨勢的日益成長,寵物鞋產業正蓬勃發展。人們越來越認知到,狗不僅是伴侶動物,更是家庭成員。這種轉變正在重新定義消費者對舒適、防護和生活方式導向寵物護理產品的期望,並穩步提升高階狗鞋類的需求。寵物飼主越來越傾向選擇兼具功能性防護、現代設計美學並能體現自身生活方式的產品。人們對寵物健康、舒適度和預防保健的日益關注,也促使人們將狗鞋類視為必需品而非奢侈品。此外,可支配收入的成長,尤其是在都市區,也推動了高階寵物照護解決方案支出的增加。消費者越來越願意投資購買能夠增強狗狗爪子在各種環境條件下安全性的防護性鞋履。這些消費者行為的轉變降低了價格敏感度,並刺激了產品創新、客製化和材料進步,進而支持了全球各地市場的長期擴張。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 17億美元 |

| 預計金額 | 40億美元 |

| 複合年成長率 | 8.9% |

寵物鞋類市場受益於人們對寵物在惡劣環境下的安全意識不斷提高以及都市化進程的加速。寵物照護支出的增加和高階寵物生活方式產品的日益普及進一步推動了市場需求。持續的產品創新和專業防護配件的不斷普及預計將維持已開發市場和新興市場的成長勢頭。

預計到2025年,犬靴市場規模將達到7億美元。該產品類型憑藉其卓越的防護性、耐用性和在各種環境條件下的多功能性,正引領市場發展。與輕便犬靴相比,犬靴的覆蓋範圍更廣,能夠有效抵抗極端溫度、崎嶇地形、尖銳物體和地面化學物質的侵害。其結構化的設計增強了抓地力、保暖性和長期耐用性,使其適用於從日常都市區漫步到戶外探險等各種活動。功能性防護和耐用性的完美結合,持續推動消費者對此品類的強勁需求。

到2025年,個人寵物飼主將佔據67.7%的市場。這一主導地位源自於人們對寵物飼養態度的轉變。狗狗越來越被視為家庭成員,它們的健康和舒適需求也日益受到重視。個人消費者積極投資專業的寵物護理產品,尤其是那些旨在提升寵物在日常環境中安全性和防護性的產品。人們對寵物爪子健康以及保護寵物免受極端溫度和都市區路面傷害的意識不斷提高,也顯著增加了個人寵物飼主對狗鞋類的需求。

美國狗鞋類市場佔據81%的市場佔有率,預計2025年市場規模將達到5.3億美元。美國市場的強勁成長得益於高度發展的寵物照護產業以及消費者對高階寵物產品的旺盛消費。除了高寵物擁有率外,飼主與寵物之間深厚的情感紐帶也持續推動對功能性強、品質優良的狗鞋的需求。此外,人們日益重視在城市環境和極端天氣條件下保護寵物爪子的重要性,也進一步促進了美國狗鞋市場的持續成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章:行業洞察

- 工業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響因素

- 促進因素

- 產業潛在風險與挑戰

- 機會

- 成長潛力分析

- 未來市場趨勢

- 技術與創新展望

- 材料創新趨勢

- 製造技術的進步

- 客製化和3D列印技術

- 智慧鞋類與穿戴式裝置的融合

- 開發永續和環保材料

- 監理框架

- 寵物產品的區域安全法規

- 材料和化學品合規標準

- 進出口限制和關稅

- 展示包裝要求

- 價格分析

- 對過去價格趨勢的分析

- 根據參與企業的類型(高階、價值、成本加成)所製定的定價策略

- 區域價格波動及其影響因素

- 按消費者群體分類的價格敏感度分析

- 波特的分析

- PESTLE分析

- 貿易資料分析 HS編碼:(4201.00.6000): 狗靴

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 區域貿易平衡

- 新的貿易路線和商業機會

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 基於細分市場的生成式人工智慧的應用案例和部署藍圖

- 風險、限制和監管考量

- 人工智慧在產品設計與客製化的應用

- 人工智慧驅動的尺寸和合身度提案

- 目前分銷基礎設施和通路滲透情況

- 以區域業態(現代零售與傳統零售)分類的通路覆蓋率

- 缺乏最後一公里基礎設施和不斷變化的管道

- 對全通路零售的採用率和成熟度進行評估

- 消費者購買行為分析

- 人口趨勢和寵物飼養模式

- 寵物飼主的心理特徵細分

- 影響購買決策的因素

- 優先考慮產品偏好和功能

- 期望價格範圍和支付意願

- 主要分銷通路分析

- 品牌忠誠度與轉換行為

- 社群媒體和線上評論的影響

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 靴子

- 全地形靴

- 冬季雪靴

- 防水靴

- 時尚靴子

- 鞋類

- 休閒日常鞋類

- 煥新性能鞋類

- 室內鞋類

- 襪子

- 防滑襪

- 治療/醫用襪

- 時尚襪子

- 涼鞋

- 夏季涼鞋

- 透氣涼鞋

- 足部保護器

- 一次性足部保護器

- 可重複使用的足部保護器

- 爪墊蠟膏替代品

第6章 市場估計與預測:依材料分類,2022-2035年

- 皮革

- 全粒面皮革

- 合成皮革

- 橡皮

- 天然橡膠

- 合成

- 氯丁橡膠

- 尼龍

- 聚酯纖維

- 其他(可生物分解材料、回收材料等)

第7章 市場估計與預測:依價格區間分類,2022-2035年

- 低的

- 中等的

- 高的

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 全地形/戶外活動

- 健行和步道活動

- 跑步和慢跑

- 在崎嶇道路上行駛時的保護

- 天氣對策

- 寒冷氣候和雪災應變措施

- 高溫路面/夏季應對措施

- 應對雨水和潮濕環境的措施

- 室內/休閒用途

- 居家及地板保護

- 光保護

- 出於時尚和美學目的

- 醫療

- 傷後恢復及傷口保護

- 為老年犬提供交通支持

- 預防疾病

- 表演/運動

- 專業培訓

- 工作犬(警犬、搜救犬、軍犬)

- 競爭活動

第9章 市場估價與預測:依最終用戶分類,2022-2035年

- 個人寵物飼主

- 企業用戶

- 動物診所

- 專業培訓師

- 寵物美容和寵物護理服務

- 育種者

- 工作犬訓導員

第10章 市場估價與預測:依通路分類,2022-2035年

- 線上管道

- 電子商務

- 企業網站

- 離線頻道

- 超級市場和大賣場

- 寵物專賣店

- 其他(百貨公司等)

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- 全球主要公司

- Ruffwear

- Muttluks

- Kurgo

- PawZ Dog Boots

- Ultra Paws

- Neo-Paws

- Canada Pooch

- 當地公司

- Hurtta

- Rukka Pets

- RC Pet Products

- Guangzhou Voyager Pet Products

- Non-stop Dogwear

- Healers Petcare

- Saltsox

- 新興企業

- Dogsoxx

- Bark Brite

- Woodrow Wear(Power Paws)

- Walkee Paws

- Fetchers

- Spark Paws

- RIFRUF

The Global Dog Footwear Market was valued at USD 1.7 billion in 2025 and is estimated to grow at a CAGR of 8.9% to reach USD 4 billion by 2035.

The industry is gaining momentum due to the rising trend of pet humanization, where dogs are increasingly regarded as integral family members rather than companion animals alone. This shift is reshaping consumer expectations around comfort, protection, and lifestyle-oriented pet care products, driving consistent demand for premium dog footwear. Pet owners are increasingly seeking products that combine functional protection with modern design aesthetics, reflecting their own lifestyle preferences. Growing focus on pet health, comfort, and preventive care is also contributing to the perception of dog footwear as an essential accessory rather than a discretionary item. In addition, rising disposable incomes, especially in urban regions, are enabling higher spending on premium pet care solutions. Consumers are increasingly willing to invest in advanced protective footwear that enhances paw safety across varying environmental conditions. This evolving spending behavior is reducing price sensitivity and encouraging product innovation, customization, and material advancements, thereby supporting long-term market expansion across global regions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.7 Billion |

| Forecast Value | $4 Billion |

| CAGR | 8.9% |

The dog footwear market is also benefiting from increasing awareness of pet safety in harsh environmental conditions and growing urbanization. Expanding pet care expenditure patterns and the rising popularity of premium pet lifestyle products are further strengthening market demand. Continuous product innovation and growing adoption of specialized protective accessories are expected to sustain growth momentum across both developed and emerging economies.

The boots segment accounted for USD 700 million in 2025. This product category leads the market due to its superior protective performance, durability, and versatility across a wide range of conditions. Dog boots provide enhanced coverage compared to lighter alternatives, offering protection from extreme temperatures, rough terrain, sharp objects, and surface chemicals. Their structured build improves grip, insulation, and long-term usability, making them suitable for both everyday urban walks and outdoor activities. The combination of functional protection and durability continues to drive strong consumer preference for this segment.

The individual pet owners segment held a share of 67.7% in 2025. This segment's leadership is driven by changing perceptions of pet ownership, where dogs are increasingly treated as family members with prioritized health and comfort needs. Individual consumers are actively investing in specialized pet care products, particularly those designed to enhance safety and protection in daily environments. Growing awareness of paw health and protection against temperature extremes and urban surfaces has significantly increased demand for dog footwear among private pet owners.

U.S. Dog Footwear Market held an 81% share, generating USD 0.53 billion in 2025. Market strength in the United States is supported by a highly developed pet care industry and strong consumer spending on premium pet accessories. High pet ownership rates, combined with deep emotional attachment between owners and pets, continue to drive demand for functional and high-quality dog footwear. Increasing awareness of paw protection needs in urban environments and extreme weather conditions further supports sustained market growth across the country.

Major companies operating in the Global Dog Footwear Market include Ruffwear, Muttluks, Kurgo, PawZ Dog Boots, Ultra Paws, Neo Paws, Canada Pooch, Hurtta, Rukka Pets, RC Pet Products, Non-stop Dogwear, Woodrow Wear, Walkee Paws, Bark Brite, RIFRUF, Dogsoxx, Fetchers, Spark Paws, and Guangzhou Voyager Pet Products. Companies operating in the dog footwear market are adopting multiple strategies to strengthen their competitive positioning and expand consumer reach. Manufacturers are focusing on product innovation by developing ergonomic, weather-resistant, and durable footwear designed for different climates and terrains. Emphasis on premium materials and improved comfort features is helping brands differentiate their offerings in a competitive market. Companies are also investing in customization options, allowing pet owners to select sizes, designs, and functional features tailored to specific needs. Expansion of online retail channels and direct-to-consumer platforms is improving accessibility and brand visibility across global markets. Strategic partnerships with pet specialty retailers and veterinary channels are further strengthening distribution networks.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Material

- 2.2.4 Application

- 2.2.5 Price range

- 2.2.6 End user

- 2.2.7 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology/innovation landscape

- 3.5.1 Material innovation trends

- 3.5.2 Manufacturing technology advancements

- 3.5.3 Customization & 3D printing technologies

- 3.5.4 Smart footwear & wearable integration

- 3.5.5 Sustainability & Eco-Friendly Material Development

- 3.6 Regulatory Framework

- 3.6.1 Pet product safety regulations by region

- 3.6.2 Material & chemical compliance standards

- 3.6.3 Import/export regulations & tariffs

- 3.6.4 Labeling & packaging requirements

- 3.7 Pricing Analysis (Driven by Primary Research)

- 3.7.1 Historical price trend analysis (driven by primary research)

- 3.7.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.7.3 Regional price variations & factors

- 3.7.4 Price sensitivity analysis by consumer segment

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Trade data analysis HS Code: (4201.00.6000): Dog booties/boots (Driven by paid database)

- 3.10.1 Import/export volume & value trends

- 3.10.2 Key trade corridors & tariff impact

- 3.10.3 Trade balance by region

- 3.10.4 Emerging trade routes & opportunities

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 GenAI use cases & adoption roadmap by segment

- 3.11.3 Risks, limitations & regulatory considerations

- 3.11.4 AI in product design & customization

- 3.11.5 AI-powered sizing & fit recommendations

- 3.12 Distribution infrastructure & channel penetration landscape (driven by primary research)

- 3.12.1 Channel coverage by region & format (modern vs. traditional trade) (driven by primary research)

- 3.12.2 Last-mile infrastructure gaps & emerging channel shifts (driven by primary research)

- 3.12.3 Omnichannel retail penetration & maturity assessment

- 3.13 Consumer buying behavior analysis

- 3.13.1 Demographic trends & pet ownership patterns

- 3.13.2 Psychographic segmentation of pet owners

- 3.13.3 Factors affecting purchase decisions

- 3.13.4 Product preference & feature prioritization

- 3.13.5 Preferred price range & willingness to pay

- 3.13.6 Preferred distribution channel analysis

- 3.13.7 Brand loyalty & switching behavior

- 3.13.8 Influence of social media & online reviews

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Boots

- 5.2.1 All-terrain boots

- 5.2.2 Winter/snow boots

- 5.2.3 Waterproof boots

- 5.2.4 Fashion boots

- 5.3 Shoes

- 5.3.1 Casual/everyday shoes

- 5.3.2 Sport/performance shoes

- 5.3.3 Indoor shoes

- 5.4 Socks

- 5.4.1 Non-slip socks

- 5.4.2 Therapeutic/medical socks

- 5.4.3 Fashion socks

- 5.5 Sandals

- 5.5.1 Summer sandals

- 5.5.2 Breathable sandals

- 5.6 Paw protectors

- 5.6.1 Disposable paw protectors

- 5.6.2 Reusable paw protectors

- 5.6.3 Paw wax & balm alternatives

Chapter 6 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Leather

- 6.2.1 Full-grain leather

- 6.2.2 Synthetic leather

- 6.3 Rubber

- 6.3.1 Natural

- 6.3.2 Synthetic

- 6.4 Neoprene

- 6.5 Nylon

- 6.6 Polyester

- 6.7 Others (biodegradable materials, recycled materials, etc.)

Chapter 7 Market Estimates and Forecast, By Price Range, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 All-Terrain/outdoor activities

- 8.2.1 Hiking & trail activities

- 8.2.2 Running & jogging

- 8.2.3 Rough terrain protection

- 8.3 Weather protection

- 8.3.1 Cold weather/snow protection

- 8.3.2 Hot pavement/summer protection

- 8.3.3 Rain & wet condition protection

- 8.4 Indoor/casual use

- 8.4.1 Home use & floor protection

- 8.4.2 Light protection

- 8.4.3 Fashion & aesthetic use

- 8.5 Medical/therapeutic

- 8.5.1 Injury recovery & wound protection

- 8.5.2 Mobility support for senior dogs

- 8.5.3 Protection for medical conditions

- 8.6 Performance/Sport

- 8.6.1 Professional training

- 8.6.2 Working dogs (police, search & rescue, Military)

- 8.6.3 Competitive activities

Chapter 9 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Individual pet owners

- 9.3 Professional users

- 9.3.1 Veterinary clinics

- 9.3.2 Professional trainers

- 9.3.3 Groomers & pet care services

- 9.3.4 Breeders

- 9.3.5 Working dog handlers

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Online channels

- 10.2.1 E-commerce

- 10.2.2 Company websites

- 10.3 Offline channels

- 10.3.1 Supermarkets/hypermarkets

- 10.3.2 Specialty pet stores

- 10.3.3 Others (departmental stores, etc.)

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Top Global Players

- 12.1.1 Ruffwear

- 12.1.2 Muttluks

- 12.1.3 Kurgo

- 12.1.4 PawZ Dog Boots

- 12.1.5 Ultra Paws

- 12.1.6 Neo-Paws

- 12.1.7 Canada Pooch

- 12.2 Regional Players

- 12.2.1 Hurtta

- 12.2.2 Rukka Pets

- 12.2.3 RC Pet Products

- 12.2.4 Guangzhou Voyager Pet Products

- 12.2.5 Non-stop Dogwear

- 12.2.6 Healers Petcare

- 12.2.7 Saltsox

- 12.3 Emerging Players

- 12.3.1 Dogsoxx

- 12.3.2 Bark Brite

- 12.3.3 Woodrow Wear (Power Paws)

- 12.3.4 Walkee Paws

- 12.3.5 Fetchers

- 12.3.6 Spark Paws

- 12.3.7 RIFRUF