|

市場調查報告書

商品編碼

2038797

合成生物學市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測Synthetic Biology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

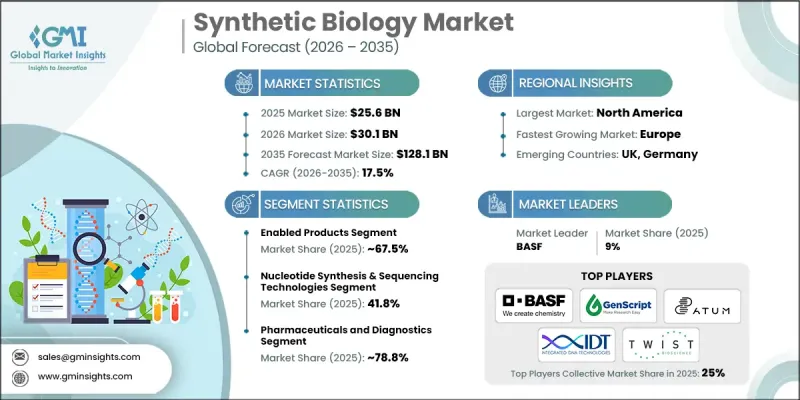

全球合成生物學市場預計到 2025 年將價值 256 億美元,預計到 2035 年將以 17.5% 的複合年成長率成長至 1,281 億美元。

合成生物學將工程原理與生物系統結合,用於設計和建構新型生物組件、裝置和系統,市場發展勢頭強勁。該領域已從傳統的基因工程方法顯著發展到能夠精確、可程式設計控制細胞行為的先進平台。 DNA定序和合成技術、計算生物學工具的快速進步以及對生物系統設計的深刻理解加速了這一轉變。此生態系涵蓋了寡核苷酸、酵素和宿主生物等基礎投入,合成基因、修飾細胞和DNA文庫等關鍵交付物,以及從藥物和工業化學品到生質燃料和生物材料等下游應用。基因組編輯技術(尤其是基於CRISPR的平台)的日益普及,進一步拓展了其在醫療保健、農業和工業生物技術領域的應用範圍,從而推動了整體市場成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 256億美元 |

| 預測金額 | 1281億美元 |

| 複合年成長率 | 17.5% |

預計到2025年,「實用化產品」細分市場將佔據67.5%的市場佔有率,並在2035年之前以17.4%的複合年成長率成長。此細分市場是推動市場成長的主要動力,因為它涵蓋了商業性可行性的產品,例如工程生物分子、工業酵素、生物基化學品、永續燃料、先進材料、農業生技藥品製劑和治療解決方案。直接在工業領域的商業化以及與多個終端應用領域的廣泛整合,為其強勁的產生收入提供了有力支撐。

預計到2025年,醫藥和診斷領域將佔據78.8%的市場佔有率,並在2035年之前以17.2%的複合年成長率成長。該領域仍然是最成熟的應用領域,其成長主要得益於藥物發現、疫苗開發、基因和細胞治療研究以及分子診斷等領域的設計生物系統。合成生物學正在實現高度精確、可重複和可客製化的醫療解決方案,從而加速先進治療和診斷平台的發展。

預計到 2025 年,北美合成生物學市場將佔據 39.6% 的佔有率。該地區憑藉先進的研究基礎設施、對創新生物技術的早期應用以及高度發達的生態系統(包括學術機構、初創企業和大型生物技術及製藥公司),保持著強勁的市場地位,而這些反過來又支持著技術的持續進步和商業化。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 擴大 CRISPR 和基因組編輯技術在精準基因改造的應用。

- 人工智慧與生物資訊學工具的融合正在不斷推進。

- 各行各業對永續和環保生物產品的需求都在不斷成長。

- 產業潛在風險與挑戰

- 慢性病日益增多以及個人化醫療的發展趨勢

- 擴大業務需要大量資金。

- 市場機遇

- 在醫療保健、農業和永續生物製造領域提供創新解決方案,以應對全球挑戰。

- 個人化醫療和細胞療法的擴展

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 核心產品

- 合成核酸

- 遺傳元件載體

- 其他

- 粉底產品

- 基因合成與定序平台

- 基因工程試劑盒和試劑

- 其他

- 應用產品

- 治療性生物製藥和細胞療法

- 生物基化學品和材料

- 其他

第6章 市場估計與預測:依技術分類,2022-2035年

- 核苷酸合成與定序技術

- 基因工程技術

- 生物資訊學和計算生物學

- 微流體和小型化

- 其他

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 藥品和診斷劑

- 工業化學品/材料

- 農業和食品生產

- 能源與生質燃料

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- Novozymes

- BASF

- GenScript

- ATUM

- Integrated DNA Technologies

- Twist Bioscience

- Biomax Informatics

- Pareto Biotechnologies

- Blue Heron

- TeselaGen Syntax

- Thermo Fisher Scientific

- Gevo Inc

- Royal DSM

- Bristol-Myers Squibb

- Amyris

The Global Synthetic Biology Market was valued at USD 25.6 billion in 2025 and is estimated to grow at a CAGR of 17.5% to reach USD 128.1 billion by 2035.

The market is witnessing strong momentum as synthetic biology integrates engineering principles with biological systems to design and construct novel biological components, devices, and systems. The field has evolved significantly from traditional genetic engineering approaches toward advanced platforms that enable precise and programmable control of cellular behavior. This transformation has been accelerated by rapid advancements in DNA sequencing and synthesis technologies, computational biology tools, and deeper insights into biological system design. The ecosystem spans enabling inputs such as oligonucleotides, enzymes, and chassis organisms, core outputs including synthetic genes, engineered cells, and DNA libraries, and downstream applications across pharmaceuticals, industrial chemicals, biofuels, and biomaterials. Increasing adoption of genome editing technologies, particularly CRISPR-based platforms, is further expanding applications across healthcare, agriculture, and industrial biotechnology, supporting broad-based market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $25.6 Billion |

| Forecast Value | $128.1 Billion |

| CAGR | 17.5% |

The enabled products segment accounted for 67.5% share in 2025 and is expected to grow at a CAGR of 17.4% through 2035. This segment leads the market as it includes commercially deployable outputs such as engineered biomolecules, industrial enzymes, bio-based chemicals, sustainable fuels, advanced materials, agricultural biologicals, and therapeutic solutions. Strong revenue generation is supported by direct industrial commercialization and widespread integration across multiple end-use sectors.

The pharmaceuticals and diagnostics segment held a 78.8% share in 2025 and is projected to grow at a CAGR of 17.2% through 2035. It remains the most established application area, driven by engineered biological systems in drug discovery, vaccine development, gene and cell therapy research, and molecular diagnostics. Synthetic biology enables highly precise, reproducible, and customizable medical solutions, accelerating the development of advanced therapeutic and diagnostic platforms.

North America Synthetic Biology Market accounted for 39.6% share in 2025. The region maintains a strong position due to advanced research infrastructure, early adoption of biotechnology innovations, and a highly developed ecosystem that includes academic institutions, startups, and large biotechnology and pharmaceutical companies, supporting continuous technological advancement and commercialization.

Major players operating in the Global Synthetic Biology Industry include Twist Bioscience, GenScript, Integrated DNA Technologies, Thermo Fisher Scientific, Novozymes, BASF, Royal DSM, Amyris, Gevo Inc, and Bristol-Myers Squibb. Companies in the Synthetic Biology Market are prioritizing heavy investment in advanced genome engineering platforms, including CRISPR-based technologies and automated DNA synthesis systems, to improve precision and scalability. They are strengthening R&D capabilities through collaborations with academic institutions and biotechnology startups to accelerate innovation pipelines. Expansion into high-growth application areas such as therapeutics, sustainable chemicals, and industrial bioproducts is also a key focus to diversify revenue streams. Firms are increasingly adopting integrated platform strategies that combine software, automation, and biological design tools to reduce development timelines. Strategic partnerships and licensing agreements are being used to access proprietary technologies and expand global reach. In addition, companies are investing in scalable biomanufacturing infrastructure to support commercialization, while also focusing on regulatory compliance and quality assurance to ensure safe and efficient market adoption.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Technology

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of CRISPR and genome editing technologies for precise genetic modifications

- 3.2.1.2 Growing integration of artificial intelligence and bioinformatics tools

- 3.2.1.3 Rising demand for sustainable and eco-friendly bioproducts across industries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Rising prevalence of chronic diseases and personalized medicine approaches

- 3.2.2.2 High capital requirements for scale-up

- 3.2.3 Market opportunities

- 3.2.3.1 Innovative solutions in healthcare, agriculture, and sustainable biomanufacturing to address global challenges

- 3.2.3.2 Personalized medicine & cell therapy expansion

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Million)

- 5.1 Key trends

- 5.2 Core Products

- 5.2.1 Synthetic Nucleic Acids

- 5.2.2 Genetic Parts & Vectors

- 5.2.3 Others

- 5.3 Enabling Products

- 5.3.1 Gene Synthesis & Sequencing Platforms

- 5.3.2 Genetic Engineering Kits & Reagents

- 5.3.3 Others

- 5.4 Enabled Products

- 5.4.1 Therapeutic Biologics & Cell Therapies

- 5.4.2 Bio-Based Chemicals & Materials

- 5.4.3 Others

Chapter 6 Market Estimates and Forecast, By Technology, 2022-2035 (USD Million)

- 6.1 Key trends

- 6.2 Nucleotide Synthesis & Sequencing Technologies

- 6.3 Genetic Engineering Technologies

- 6.4 Bioinformatics & Computational Biology

- 6.5 Microfluidics & Miniaturization

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million)

- 7.1 Key trends

- 7.2 Pharmaceuticals and diagnostics

- 7.3 Industrial Chemicals & Materials

- 7.4 Agriculture & Food Production

- 7.5 Energy & Biofuels

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Novozymes

- 9.2 BASF

- 9.3 GenScript

- 9.4 ATUM

- 9.5 Integrated DNA Technologies

- 9.6 Twist Bioscience

- 9.7 Biomax Informatics

- 9.8 Pareto Biotechnologies

- 9.9 Blue Heron

- 9.10 TeselaGen Syntax

- 9.11 Thermo Fisher Scientific

- 9.12 Gevo Inc

- 9.13 Royal DSM

- 9.14 Bristol-Myers Squibb

- 9.15 Amyris

合成生物學市場:按產品、技術、應用和最終用戶分類-2026-2032年全球市場預測

合成生物學市場:按產品、技術、應用和最終用戶分類-2026-2032年全球市場預測 合成生物學平台市場預測至2034年—按類型、應用、最終用戶和地區分類的全球分析

合成生物學平台市場預測至2034年—按類型、應用、最終用戶和地區分類的全球分析 合成生物學市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終使用者及流程分類

合成生物學市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終使用者及流程分類 全球合成生物學工具市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球合成生物學市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球合成生物學工具市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球合成生物學市場規模、佔有率、趨勢和成長分析報告(2026-2034) 合成生物學市場-全球產業規模、佔有率、趨勢、機會及預測(依技術、產品、最終用戶、地區及競爭格局分類,2021-2031年)農業合成生物學市場按產品類型、技術平台、配方、應用領域和最終用戶分類-2026年至2032年全球預測

合成生物學市場-全球產業規模、佔有率、趨勢、機會及預測(依技術、產品、最終用戶、地區及競爭格局分類,2021-2031年)農業合成生物學市場按產品類型、技術平台、配方、應用領域和最終用戶分類-2026年至2032年全球預測 合成生物學市場規模、佔有率和趨勢分析報告:按產品、技術、應用、最終用途、地區和細分市場預測(2026-2033 年)分子開關作為治療標靶:藥物發現、藥物傳遞機制與適應症(2026)

合成生物學市場規模、佔有率和趨勢分析報告:按產品、技術、應用、最終用途、地區和細分市場預測(2026-2033 年)分子開關作為治療標靶:藥物發現、藥物傳遞機制與適應症(2026) 合成生物學市場規模、佔有率和成長分析(按工具、應用、技術和地區分類)-2026-2033年產業預測

合成生物學市場規模、佔有率和成長分析(按工具、應用、技術和地區分類)-2026-2033年產業預測