|

市場調查報告書

商品編碼

2027664

唇部及臉部妝前乳市場:商機、成長要素、產業趨勢分析及2026-2035年預測Lip and Face Primer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

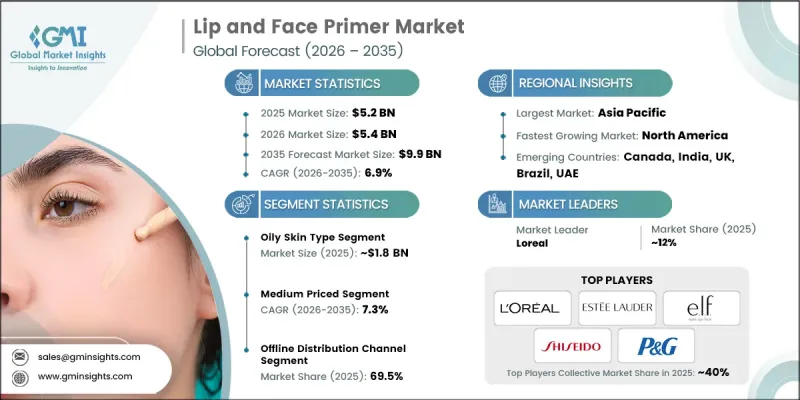

全球唇部和臉部妝前乳市場預計在 2025 年達到 52 億美元,預計到 2035 年將以 6.9% 的複合年成長率成長至 99 億美元。

消費者對持久無瑕妝容日益成長的需求正在推動這一市場的發展。無論是在工作、社交活動或線上互動中,消費者都越來越傾向於選擇能讓他們全天保持精緻妝容的產品。現代生活方式的特點是螢幕使用時間延長、混合辦公環境以及頻繁的社交互動,這些都促使人們需要能夠抵禦汗水、油脂和環境壓力的彩妝產品。妝前乳在改善膚質、控制油光和增強妝容持久度方面發揮著至關重要的作用,使其成為日常護膚和化妝步驟中不可或缺的一部分。年輕消費者和職場人士尤其注重打造「隨時上鏡」的妝容,並儘量減少補妝次數,這推動了唇部和臉部妝前乳的廣泛應用、重複購買以及市場滲透率的提升。

| 市場規模 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 52億美元 |

| 預測金額 | 99億美元 |

| 複合年成長率 | 6.9% |

預計到2025年,油性肌膚妝前乳市場規模將達到18億美元,並在2026年至2035年間以9.4%的複合年成長率成長。這類產品在炎熱潮濕的氣候和都市區已成為必備品,因為它們能夠有效解決油脂分泌過剩、毛孔粗大、妝容脫落和膚質不均等問題。具有吸油、霧面妝效、收縮毛孔和防汗等功效的產品,正受到注重產品功能性的彩妝使用者的青睞。

預計到2025年,中價位妝前乳市佔率將達到48.4%,並在2026年至2035年間以7.3%的複合年成長率成長。這些妝前乳提供專業級的妝效,例如縮小毛孔、持久持妝和平滑肌膚紋理,同時價格親民,滿足追求品質的消費者的需求。許多全球和區域品牌正將創新重心放在這一價位區間,推出融合了透明酸、菸鹼醯胺、防曬成分和控油劑等護膚成分的混合配方。強大的線上線下零售通路佈局,以及行銷宣傳活動和網紅代言的支持,進一步提升了品牌知名度和市場接受度。

美國唇部及臉部妝前乳市場預計在2025年達到12億美元,並在2026年至2035年間以7.4%的複合年成長率成長。這一成長主要得益於消費者對完美肌膚、持久妝效和柔滑肌膚效果的日益關注,尤其是在社交媒體和混合辦公模式下,千禧世代和Z世代消費者追求精緻且「上鏡」的妝容。高階和藥妝品牌的高滲透率也支撐了市場成長,這些品牌提供的多功能妝前乳集保濕、遮蓋毛孔、控油、防曬和抗衰老功效於一體,滿足了消費者對「滋養肌膚」型彩妝產品日益成長的需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 對持久妝容的需求日益成長。

- 人們越來越偏好選擇天然成分、無動物實驗、不致粉刺的產品。

- 配方方面的持續創新

- 產業潛在風險與挑戰

- 產品飽和和激烈競爭

- 消費者對成分的敏感性和皮膚反應

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按業務類型分類的定價策略(溢價/價值/成本加成)

- 各地區價格波動

- 原物料成本對價格的影響

- 貿易資料分析(HS編碼3304.99)

- 進出口數量和價值的變化趨勢

- 主要貿易路線及關稅的影響

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 波特的分析

- PESTEL 分析

- 消費行為分析

- 購買模式

- 偏好分析

- 消費行為的區域差異

- 電子商務對購買決策的影響

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依組件分類,2022-2035年

- 妝前乳

- 能盡量減少毛孔的妝前乳

- 保濕滋潤妝前乳

- 霧面飾面,控油底漆

- 發光/亮澤妝前乳

- 顏色校正底漆

- 唇部打底

- 唇部打底市場

- 豐盈唇部打底

- 持久唇部打底

- 多用途底漆

第6章 市場估算與預測:依製劑類型分類,2022-2035年

- 乳霜型妝前乳

- 凝膠底漆

- 矽基底漆

- 水性底漆

- 粉末底火

- 棒狀底火

- 其他

第7章 市場估計與預測:依原料類型分類,2022-2035年

- 自然的

- 合成

第8章 市場估計與預測:依價格分類,2022-2035年

- 低價位

- 中等的

- 高的

第9章 市場估價與預測:依通路分類,2022-2035年

- 線上

- 電子商務網站

- 品牌官方網站

- 離線

- 超級市場/大賣場

- 專賣店

- 其他

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 馬來西亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第11章:公司簡介

- Avon Products, Inc.

- Beiersdorf AG

- Clarins Group

- Coty Inc.

- 雅詩蘭黛公司

- Johnson &Johnson

- Kose Corporation

- Kylie Cosmetics, Inc.

- L'Oreal Group

- LVMH Moet Hennessy Louis Vuitton

- Mary Kay Inc.

- Procter &Gamble Co.

- Revlon Inc.

- Shiseido Company, Limited

- Unilever

The Global Lip and Face Primer Market was valued at USD 5.2 billion in 2025 and is estimated to grow at a CAGR of 6.9% to reach USD 9.9 billion by 2035.

The growing demand for long-lasting, flawless makeup is driving this market as consumers increasingly seek products that maintain a polished appearance throughout extended workdays, social engagements, and virtual interactions. Modern lifestyles, characterized by prolonged screen exposure, hybrid work environments, and frequent social interactions, have heightened the need for makeup solutions that resist sweat, oil, and environmental stressors. Primers play a crucial role by smoothing skin texture, controlling shine, and improving makeup adherence, making them an essential step in daily routines. Younger consumers and working professionals prioritize achieving a camera-ready look with minimal touch-ups, which has led to increased adoption, repeat purchases, and higher market penetration for lip and face primers.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.2 Billion |

| Forecast Value | $9.9 Billion |

| CAGR | 6.9% |

The primers designed for oily skin accounted for USD 1.8 billion in 2025 and are expected to grow at a CAGR of 9.4% from 2026 to 2035. These formulations address issues such as excess sebum, enlarged pores, makeup breakdown, and uneven texture, making them indispensable in hot, humid, and urban climates. Products offering oil absorption, mattifying effects, pore minimization, and sweat resistance have gained traction among performance-oriented makeup users.

The medium-priced primers segment held a 48.4% share in 2025 and is projected to grow at a CAGR of 7.3% from 2026 to 2035. These primers provide professional-grade results, including pore blurring, long-lasting wear, and texture smoothing, while remaining accessible to aspirational consumers. Many global and regional brands focus their innovation on this tier, introducing hybrid formulas enriched with skincare ingredients such as hyaluronic acid, niacinamide, SPF, and oil-control actives. Strong presence across offline and online retail channels, supported by marketing campaigns and influencer endorsements, further boosts visibility and adoption.

U.S. Lip and Face Primer Market captured USD 1.2 billion in 2025 and is expected to grow at a CAGR of 7.4% from 2026 to 2035. Growth is driven by rising awareness of complexion perfection, long-wear makeup, and skin-smoothing benefits, particularly among millennials and Gen Z consumers seeking polished, camera-ready looks for social media and hybrid work lifestyles. The market is supported by high penetration of premium and dermocosmetic brands that offer multifunctional primers with hydration, pore-blurring, oil-control, SPF, and anti-aging properties, meeting the rising demand for "skinified" makeup products.

Key players in the Global Lip and Face Primer Industry include L'Oreal Group, Mary Kay Inc., Avon Products, Inc., Clarins Group, Procter & Gamble Co., Shiseido Company, Limited, Johnson & Johnson, Kylie Cosmetics, Inc., Estee Lauder Companies Inc., Coty Inc., Beiersdorf AG, Unilever, Revlon Inc., Kose Corporation, and LVMH Moet Hennessy Louis Vuitton. Companies in the Lip and Face Primer Market strengthen their foothold by investing in R&D to develop multifunctional products combining skincare and cosmetic benefits. Expansion into medium-priced segments allows brands to reach aspirational consumers, while premium lines target high-end clientele. Firms leverage influencer marketing, social media campaigns, and omnichannel distribution strategies to enhance visibility and consumer engagement. Product innovation, including hybrid primers with SPF, oil control, and anti-aging benefits, supports repeat purchases. Brands also prioritize sustainability, clean-label formulations, and eco-friendly packaging to appeal to environmentally conscious buyers, reinforcing brand loyalty and market position in competitive regions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Skin type

- 2.2.4 Formulation type

- 2.2.5 Ingredient type

- 2.2.6 Price range

- 2.2.7 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for long-lasting makeup

- 3.2.1.2 Rising preference for natural, cruelty-free, and non-comedogenic products

- 3.2.1.3 Ongoing innovation in formulations

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High product saturation and intense competition

- 3.2.2.2 Consumer sensitivity to ingredients and skin reactions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Pricing analysis (driven by primary research)

- 3.7.1 Historical Price Trend Analysis

- 3.7.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.7.3 Regional Price Variations

- 3.7.4 Impact of Raw Material Costs on Pricing

- 3.8 Trade data analysis (HS Code 3304.99)

- 3.8.1 Import/export volume & value trends

- 3.8.2 Key trade corridors & tariff impact

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 AI-driven disruption of existing business models

- 3.9.2 GenAI use cases & adoption roadmap by segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

- 3.12 Consumer behavior analysis

- 3.12.1 Purchasing patterns

- 3.12.2 Preference analysis

- 3.12.3 Regional variations in consumer behavior

- 3.12.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Face Primer

- 5.2.1 Pore-minimizing primers

- 5.2.2 Hydrating/moisturizing primers

- 5.2.3 Mattifying/oil-control primers

- 5.2.4 Illuminating/glow primers

- 5.2.5 Color-correcting primers

- 5.3 Lip Primer

- 5.3.1 Smoothing lip primers

- 5.3.2 Plumping lip primers

- 5.3.3 Long-wear lip primers

- 5.4 Multi-Purpose Primer

Chapter 6 Market Estimates & Forecast, By Formulation Type, 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Cream-based primers

- 6.3 Gel-based primers

- 6.4 Silicone-based primers

- 6.5 Water-based primers

- 6.6 Powder primers

- 6.7 Stick primers

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By Ingredient Type, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Natural

- 7.3 Synthetic

Chapter 8 Market Estimates & Forecast, By Price, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Low

- 8.3 Mid

- 8.4 High

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Online

- 9.2.1 E-commerce websites

- 9.2.2 Brand-owned websites

- 9.3 Offline

- 9.3.1 Supermarkets/Hypermarkets

- 9.3.2 Specialty stores

- 9.3.3 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Indonesia

- 10.4.7 Malaysia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Avon Products, Inc.

- 11.2 Beiersdorf AG

- 11.3 Clarins Group

- 11.4 Coty Inc.

- 11.5 Estee Lauder Companies Inc.

- 11.6 Johnson & Johnson

- 11.7 Kose Corporation

- 11.8 Kylie Cosmetics, Inc.

- 11.9 L'Oreal Group

- 11.10 LVMH Moet Hennessy Louis Vuitton

- 11.11 Mary Kay Inc.

- 11.12 Procter & Gamble Co.

- 11.13 Revlon Inc.

- 11.14 Shiseido Company, Limited

- 11.15 Unilever

唇部護理產品市場-2026-2032年全球市場預測

唇部護理產品市場-2026-2032年全球市場預測 唇部護理產品市場報告:按產品類型、銷售管道和地區分類(2026-2034 年)唇部修復面膜市場:按成分類型、產品類型、價格範圍、應用和分銷管道分類,全球預測(2026-2032年)

唇部護理產品市場報告:按產品類型、銷售管道和地區分類(2026-2034 年)唇部修復面膜市場:按成分類型、產品類型、價格範圍、應用和分銷管道分類,全球預測(2026-2032年) 全球唇部護理產品市場規模、佔有率、趨勢及成長分析報告(2026-2034年)日本唇部護理產品市場規模、佔有率、趨勢和預測:按產品、分銷管道和地區分類,2026-2034年

全球唇部護理產品市場規模、佔有率、趨勢及成長分析報告(2026-2034年)日本唇部護理產品市場規模、佔有率、趨勢和預測:按產品、分銷管道和地區分類,2026-2034年 唇部護理產品市場-全球產業規模、佔有率、趨勢、機會和預測:按類型、產品類型、包裝、最終用戶、分銷管道、地區和競爭格局分類,2021-2031年

唇部護理產品市場-全球產業規模、佔有率、趨勢、機會和預測:按類型、產品類型、包裝、最終用戶、分銷管道、地區和競爭格局分類,2021-2031年 唇部護理產品市場規模、佔有率及成長分析(按產品、通路及地區分類)-2026-2033年產業預測

唇部護理產品市場規模、佔有率及成長分析(按產品、通路及地區分類)-2026-2033年產業預測 全球唇部和臉部底霜市場

全球唇部和臉部底霜市場 Ph 基潤唇膏市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

Ph 基潤唇膏市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測