|

市場調查報告書

商品編碼

2027644

氣泡酒市場機會、成長要素、產業趨勢分析及2026-2035年預測Sparkling Wine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

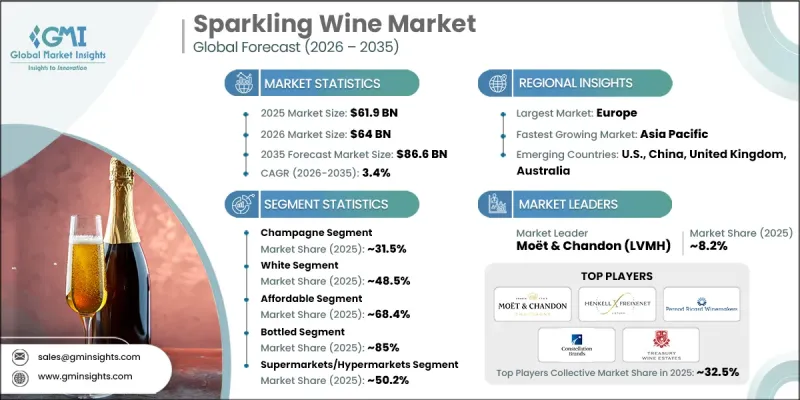

2025 年全球氣泡酒市場價值估計為 619 億美元,預計到 2035 年將達到 866 億美元,年複合成長率為 3.4%。

隨著消費者偏好轉向既適合慶祝場合又適合日常享用的優質酒精飲品,酒類產業也不斷發展。氣泡酒以其天然氣發泡和精緻口感而聞名,採用多種發酵工藝釀造,並擁有豐富的風格和甜度選擇。其適用於各種飲用場合,且價格區間廣泛,推動了全球需求。此外,消費者對兼具體驗和價值的高品質飲品的需求日益成長,也促進了市場發展。數位零售優質化的拓展和分銷網路的完善提高了產品的知名度和可及性。同時,永續性已成為關注的焦點,生產商紛紛採取環保措施,簡化包裝,並實施更清潔的生產流程。品牌、包裝和生產技術的持續創新,創造了競爭激烈且充滿活力的市場環境,為氣泡酒市場的長期成長提供了有力支撐。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 619億美元 |

| 預測金額 | 866億美元 |

| 複合年成長率 | 3.4% |

預計到2025年,香檳酒市佔率將達到31.5%,並在2035年之前維持3.6%的複合年成長率。其主導地位得益於其全球知名度高、高階定位以及嚴格的生產標準,這些標準確保了香檳酒始終如一的品質。香檳酒擁有成熟的品牌價值、嚴格的產地控制以及提升酒體複雜性和深度的精湛工藝,使其成為奢侈品消費群體的首選。

預計到2025年,白起泡酒市佔率將達到48.5%,研究期間的複合年成長率(CAGR)為3.5%。其市場主導地位得益於廣泛的消費者支持、對各種消費場合的適應性以及與多種菜餚的搭配性。該細分市場持續吸引消費者的關注,原因在於其均衡的口感、誘人的外觀以及從高級產品平價產品始終如一的高品質。

預計到2025年,美國氣泡酒市場規模將達到98億美元,顯著推動全部區域經濟成長。北美市場的擴張主要得益於消費者習慣的改變、對高階飲品日益成長的偏好,以及氣泡酒在休閒和正式場合的日益普及。強大的零售網路、不斷拓展的分銷管道以及消費者意識的提升,都持續支撐著市場的穩定發展。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依產品分類,2022-2035年

- 香檳酒

- 普羅塞克

- 卡瓦

- 其他

第6章 市場估計與預測:依類型分類,2022-2035年

- 紅色的

- 白色的

- 玫瑰

第7章 市場估計與預測:依價格分類,2022-2035年

- 奢華

- 價格實惠

第8章 市場估價與預測:依包裝類型分類,2022-2035年

- 瓶裝

- 罐頭

第9章 市場估價與預測:依通路分類,2022-2035年

- 超級市場/大賣場

- 專賣店

- 線上零售

- 其他

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第11章:公司簡介

- Moet & Chandon(LVMH)

- Henkell Freixenet

- Pernod Ricard Winemakers

- Constellation Brands

- Treasury Wine Estates

- E & J Gallo Winery

- Accolade Wines

- Casella Family Brands

- Vina Concha Y Toro

- Bronco Wine Company

- Schramsberg Vineyards

- Caviro Extra

- Giulio Cocchi Spumanti Srl

The Global Sparkling Wine Market was valued at USD 61.9 billion in 2025 and is estimated to grow at a CAGR of 3.4% to reach USD 86.6 billion by 2035.

The industry continues to evolve as consumer preferences shift toward premium alcoholic beverages that align with both celebratory occasions and everyday indulgence. Sparkling wine, known for its natural effervescence and refined appeal, is produced using multiple fermentation techniques and is offered across a broad spectrum of styles and sweetness levels. Its versatility across consumption occasions, combined with growing accessibility across price tiers, has strengthened its global demand. The market is further supported by rising interest in premiumization, where consumers increasingly seek high-quality beverages that deliver both experience and value. Expanding digital retail channels and broader distribution networks are also enhancing product visibility and accessibility. Additionally, sustainability has become a central focus, with producers adopting environmentally responsible practices, improving packaging efficiency, and integrating cleaner production processes. Continuous innovation in branding, packaging formats, and production techniques is shaping a competitive and dynamic landscape, reinforcing the long-term growth outlook of the sparkling wine market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $61.9 Billion |

| Forecast Value | $86.6 Billion |

| CAGR | 3.4% |

The champagne segment accounted for 31.5% share in 2025 and is anticipated to grow at a CAGR of 3.6% through 2035. Its leadership position is supported by strong global recognition, premium positioning, and strict production standards that ensure consistent quality. The category benefits from established brand value, controlled origin practices, and a production process that enhances complexity and depth, making it a preferred choice in high-end consumption segments.

The white sparkling wine segment held a 48.5% in 2025 and is forecast to grow at a CAGR of 3.5% during the study period. Its dominance is driven by broad consumer acceptance, adaptability across various consumption occasions, and compatibility with a wide range of culinary pairings. The segment continues to attract demand due to its balanced flavor profile, visual appeal, and consistent performance across both premium and accessible product categories.

U.S. Sparkling Wine Market generated USD 9.8 billion in 2025, contributing significantly to regional growth. Market expansion in North America is supported by evolving consumption habits, increasing preference for premium beverages, and the rising popularity of sparkling wine in casual as well as formal settings. Strong retail presence, expanding distribution channels, and growing consumer awareness continue to support steady market development.

Key players operating in the Global Sparkling Wine Industry include Moet & Chandon (LVMH), Henkell Freixenet, Pernod Ricard Winemakers, Constellation Brands, Treasury Wine Estates, E & J Gallo Winery, Accolade Wines, Casella Family Brands, Vina Concha Y Toro, Bronco Wine Company, Schramsberg Vineyards, Caviro Extra, Giulio Cocchi Spumanti Srl, and Illinois Sparkling Co. Companies in the Sparkling Wine Market are strengthening their competitive position by focusing on premium product development, sustainable production practices, and brand differentiation strategies. Producers are investing in advanced fermentation technologies and improved vineyard management to enhance quality and consistency. Sustainability initiatives, including eco-friendly packaging and reduced carbon emissions, are becoming central to long-term strategies. Businesses are also expanding their presence through digital platforms and direct-to-consumer channels to improve accessibility and engagement. Strategic partnerships, acquisitions, and geographic expansion into emerging markets are helping companies broaden their customer base.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product

- 2.2.2 Type

- 2.2.3 Price

- 2.2.4 Packaging Type

- 2.2.5 Distribution channel

- 2.2.6 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product, 2022-2035 (USD Billion) (Million Litres)

- 5.1 Key trends

- 5.2 Champagne

- 5.3 Prosecco

- 5.4 Cava

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Million Litres)

- 6.1 Key trends

- 6.2 Red

- 6.3 White

- 6.4 Rose

Chapter 7 Market Estimates and Forecast, By Price, 2022-2035 (USD Billion) (Million Litres)

- 7.1 Key trends

- 7.2 Luxury

- 7.3 Affordable

Chapter 8 Market Estimates and Forecast, By Packaging Type, 2022-2035 (USD Billion) (Million Litres)

- 8.1 Key trends

- 8.2 Bottled

- 8.3 Canned

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Million Litres)

- 9.1 Key trends

- 9.2 Supermarkets/Hypermarkets

- 9.3 Specialty Stores

- 9.4 Online Retail

- 9.5 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Million Litres)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Moet & Chandon (LVMH)

- 11.2 Henkell Freixenet

- 11.3 Pernod Ricard Winemakers

- 11.4 Constellation Brands

- 11.5 Treasury Wine Estates

- 11.6 E & J Gallo Winery

- 11.7 Accolade Wines

- 11.8 Casella Family Brands

- 11.9 Vina Concha Y Toro

- 11.10 Bronco Wine Company

- 11.11 Schramsberg Vineyards

- 11.12 Caviro Extra

- 11.13 Giulio Cocchi Spumanti Srl