|

市場調查報告書

商品編碼

2027553

即時乘客資訊系統市場機會、成長要素、產業趨勢分析及2026-2035年預測。Real-Time Passenger Information Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

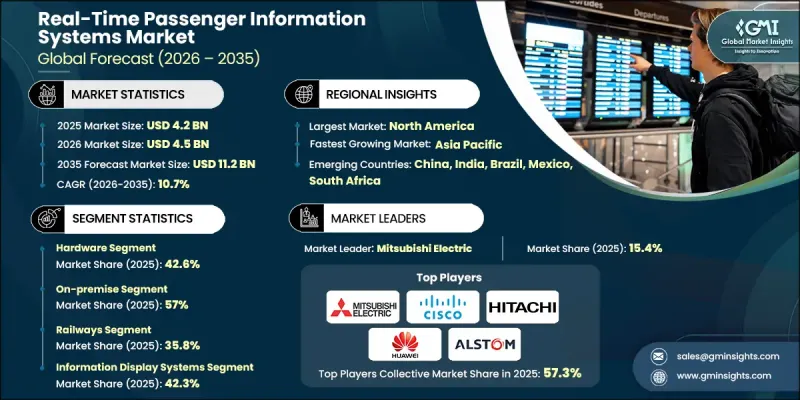

全球即時旅客資訊系統市場預計到 2025 年將達到 42 億美元,並將以 10.7% 的複合年成長率成長,到 2035 年達到 112 億美元。

快速的都市化和日益嚴重的交通堵塞是推動市場成長的主要因素,迫使城市實施先進的交通解決方案,以提高營運效率並減少延誤。即時乘客資訊系統在公共交通轉型中發揮著至關重要的作用,它提供準確及時的運營信息,使乘客能夠就路線、時間和換乘做出明智的選擇。這些系統透過最大限度地減少不確定性並最佳化出行規劃,提升了通勤者的體驗。此外,對綜合出行解決方案的日益重視正在加速將多種交通途徑連接成單一網路的平台的普及。隨著公共交通系統的不斷發展,對不同交通管道之間無縫協調的需求持續成長。對數位基礎設施的投入增加以及互聯技術的普及進一步強化了市場需求。隨著越來越多的通勤者掌握數位化技術,交通管理部門正在優先發展能夠提高服務可靠性和效率的智慧通訊系統,並將即時乘客資訊系統定位為現代城市出行生態系統的重要組成部分。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 42億美元 |

| 預測金額 | 112億美元 |

| 複合年成長率 | 10.7% |

公共運輸業者和政府機構持續投資於先進的數位基礎設施,以滿足日益成長的互聯用戶需求。多模態網路的轉型進一步提升了對能夠同步各種交通服務的整合式即時乘客資訊系統的需求。同時,技術供應商和交通解決方案開發商之間的合作也推動了軌道運輸系統的持續發展,從而提升了系統性能並促進了創新。

預計到2025年,硬體部分將佔據42.6%的市場佔有率,並在2026年至2035年間以10.6%的複合年成長率成長。該部分涵蓋了顯示單元、通訊設備、車載處理系統以及安裝在交通環境中的網路基礎設施等關鍵組件,這些組件構成了交通系統的基礎。這些組件確保了即時音訊和影像資訊的穩定傳輸,使乘客能夠在旅途中獲取可靠的出行資訊。隨著服務期望的不斷提高,交通運輸業者正致力於部署耐用、高效能的硬體解決方案,以支援長期的營運效率。

到2025年,本地部署方案將佔據57%的市場佔有率,預計到2035年將以4.4%的複合年成長率成長。這一主導地位主要歸功於公共交通系統嚴格的資料保護要求和網路安全法規。交通管理部門仍然傾向於採用本地部署方案,以更好地控制敏感數據,確保符合監管標準,並在高需求交通網路中提供不間斷的服務。

美國即時乘客資訊系統市場預計到2025年將達到13億美元,並在2026年至2035年間以10.8%的複合年成長率成長。這一區域成長主要得益於對先進通訊技術和基礎設施投資的增加,旨在提升整個公共交通網路的乘客體驗。公共運輸業者正在採用整合平台,提供即時更新、精準的到站預測和營運通知,從而提高整個系統的可靠性和效率。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 智慧交通解決方案的需求日益成長

- 政府為公共交通現代化所做的努力

- 通訊技術的進步

- 人們越來越關注安全問題

- 產業潛在風險與挑戰

- 高昂的初始成本和維修成本

- 對數據的準確性和可靠性有擔憂

- 市場機遇

- 智慧城市舉措的擴展

- 出行即服務 (MaaS) 的普及

- 人工智慧與預測分析的融合

- 已開發國家市場老舊交通基礎建設的現代化

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國聯邦交通管理局 (FTA) 制定的公共交通現代化和無障礙標準

- 根據美國《殘障人士法案》(ADA),乘客資訊無障礙要求

- 美國聯邦通訊委員會(FCC)關於運輸和通訊基礎設施的標準

- 歐洲

- 歐盟互通性技術規範 (TSI) 中的乘客資訊要求

- EN 50132 和 EN 50121 鐵路通訊和標誌標準

- 亞太地區

- 中國國家標準:智慧型運輸系統(GB/T標準)

- 印度:鐵路部旅客資訊系統指南

- 拉丁美洲

- 巴西:ANTT(國家陸路交通管理局)公共交通數位化標準

- 墨西哥:交通運輸部部(SCT)實施的交通管制措施

- 中東和非洲

- 阿拉伯聯合大公國和海灣國家:智慧運輸和智慧型運輸系統(ITS)政策

- 沙烏地阿拉伯:2030願景智慧交通與數位基礎設施框架

- 非洲聯盟(非盟):數位交通與智慧運輸政策框架

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢分析

- 經營模式和獲利框架

- 收入模式

- 價值鍊和生態系統

- 打入市場策略

- 資料管治、網路安全與系統風險

- 乘客資料隱私和合規性

- 交通運輸網路和系統的安全

- 營運和服務連續性風險

- 系統結構

- 多層旅客資訊提供模式

- 多模態網路的整合與連結性

- 專利分析

- 威脅的整體情況

- 永續性和環境方面

- 交通運輸技術引進中的永續實踐

- 顯示和通訊基礎設施的能源效率

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估計與預測:依組件分類,2022-2035年

- 硬體

- 展示

- 網路裝置

- 感應器

- 通訊設備

- 其他

- 軟體

- 資料管理軟體

- 資訊顯示軟體

- 服務

- 專業服務

- 託管服務

第6章 市場估計與預測:依運輸方式分類,2022-2035年

- 路

- 鐵路

- 航空

- 水路

第7章 市場估計與預測:依發展階段分類,2022-2035年

- 現場

- 基於雲端的

第8章 市場估算與預測:依解法分類,2022-2035年

- 資訊顯示系統

- 導航系統

- 應急通訊系統

- 其他

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 俄羅斯

- 挪威

- 丹麥

- 荷蘭

- 比利時

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 越南

- 印尼

- 新加坡

- 馬來西亞

- 泰國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 世界公司

- Advantech Co. Ltd.

- Alstom SA

- Cisco Systems Inc.

- Cubic Corporation

- Hitachi, Ltd.

- Huawei Technologies Co., Ltd.

- Indra Sistemas SA

- Mitsubishi Electric Corporation

- Nokia

- Siemens Mobility

- ST Engineering Ltd

- Thales Group

- Wabtec Corporation

- 當地公司

- Dysten Sp. z oo

- Efftronics Systems Pvt Ltd

- Icon Multimedia

- Medha Servo Drives Pvt Ltd

- r2p Group

- Teleste Corporation

- Televic Group

- Eke-Electronics

- Quester Tangent

- Simpleway

- Passio Technologies

The Global Real-Time Passenger Information Systems Market was valued at USD 4.2 billion in 2025 and is estimated to grow at a CAGR of 10.7% to reach USD 11.2 billion by 2035.

Market growth is driven by rapid urbanization and increasing congestion levels, prompting cities to adopt advanced transit solutions that enhance operational efficiency and reduce delays. Real-time passenger information systems are playing a crucial role in transforming public transportation by delivering accurate, up-to-date travel information that enables passengers to make informed decisions regarding routes, timing, and connectivity. These systems improve the commuter experience by minimizing uncertainty and optimizing travel planning. Additionally, the growing emphasis on integrated mobility solutions is accelerating the adoption of platforms capable of connecting multiple transportation modes into a unified network. As public transit systems evolve, the need for seamless coordination across various transport channels continues to rise. Increasing investments in digital infrastructure and the expansion of connected technologies are further strengthening market demand. With the growing number of digitally engaged commuters, transportation authorities are prioritizing intelligent communication systems that enhance service reliability and efficiency, positioning real-time passenger information systems as a vital component of modern urban mobility ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.2 Billion |

| Forecast Value | $11.2 Billion |

| CAGR | 10.7% |

Public transportation operators and government agencies are continuing to invest in advanced digital frameworks to support rising demand from connected users. The shift toward multimodal transportation networks is further driving the requirement for integrated real-time passenger information systems capable of synchronizing various transit services. At the same time, ongoing advancements in rail systems are being supported through collaborative efforts between technology providers and transportation solution developers, contributing to improved system performance and innovation.

The hardware segment accounted for 42.6% share in 2025 and is expected to grow at a CAGR of 10.6% from 2026 to 2035. This segment forms the backbone of these systems, encompassing essential components such as display units, communication devices, onboard processing systems, and network infrastructure installed across transit environments. These elements ensure the consistent delivery of real-time audio and visual updates, allowing passengers to access reliable travel information throughout their journey. As service expectations increase, transit operators are focusing on deploying durable and high-performance hardware solutions that support long-term operational efficiency.

The on-premise segment held a 57% share in 2025 and is projected to grow at a CAGR of 4.4% through 2035. This dominance is largely attributed to stringent data protection requirements and cybersecurity regulations governing public transportation systems. Transit authorities continue to favor on-premise deployments to maintain control over sensitive data, ensure compliance with regulatory standards, and deliver uninterrupted service across high-demand transit networks.

U.S. Real-Time Passenger Information Systems Market reached USD 1.3 billion in 2025 and is anticipated to grow at a CAGR of 10.8% between 2026 and 2035. Growth in this region is being supported by increasing investments in advanced communication technologies and infrastructure aimed at improving passenger experience across transportation networks. Transit agencies are implementing integrated platforms that provide real-time updates, accurate arrival predictions, and service notifications, enhancing overall system reliability and efficiency.

Key players operating in the Global Real-Time Passenger Information Systems Market include Alstom, Cisco Systems, Hitachi, Huawei Technologies, Indra Sistemas, Mitsubishi Electric, Nokia, Siemens Mobility, Thales, and Wabtec. Companies in the Global Real-Time Passenger Information Systems Market are strengthening their market position through continuous innovation, strategic collaborations, and expansion of digital capabilities. They are investing in advanced software platforms, cloud integration, and data analytics to deliver more accurate and scalable solutions. Partnerships with transit authorities and infrastructure providers are helping companies expand their global footprint and improve system interoperability. Market participants are also focusing on enhancing hardware reliability and integrating emerging technologies such as IoT and AI to optimize performance. In addition, companies are aligning their solutions with regulatory requirements and cybersecurity standards to ensure data protection. Expanding service portfolios and offering customized solutions tailored to specific transit networks are further supporting long-term growth and competitive advantage.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Mode of Transport

- 2.2.4 Deployment Type

- 2.2.5 Solution

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased demand for smart transportation solutions

- 3.2.1.2 Government initiatives for modernizing public transport

- 3.2.1.3 Advancements in communication technologies

- 3.2.1.4 Increasing Focus on Safety and Security

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation and maintenance costs

- 3.2.2.2 Data accuracy and reliability concern

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of Smart City Initiatives

- 3.2.3.2 Rising Adoption of Mobility-as-a-Service (MaaS)

- 3.2.3.3 Integration of AI and Predictive Analytics

- 3.2.3.4 Modernization of Aging Transit Infrastructure in Developed Markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Federal Transit Administration (FTA) Public Transit Modernization & Accessibility Standards

- 3.4.1.2 Americans with Disabilities Act (ADA) Passenger Information Accessibility Requirements

- 3.4.1.3 Federal Communications Commission (FCC) Transit Communication Infrastructure Standards

- 3.4.2 Europe

- 3.4.2.1 EU Technical Specification for Interoperability (TSI) Passenger Information Requirements

- 3.4.2.2 EN 50132 & EN 50121 Railway Communication and Display Standards

- 3.4.3 Asia Pacific

- 3.4.3.1 China National Standards for Intelligent Transportation Systems (GB/T Standards)

- 3.4.3.2 India: Ministry of Railways Passenger Information System Guidelines

- 3.4.4 Latin America

- 3.4.4.1 Brazil: ANTT (National Land Transportation Agency) Transit Digital Standards

- 3.4.4.2 Mexico: SCT (Secretariat of Communications and Transportation) Transit Regulations

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE & Gulf States: Smart Mobility & Intelligent Transport System Policy

- 3.4.5.2 Saudi Arabia: Vision 2030 Smart Transportation & Digital Infrastructure Framework

- 3.4.5.3 African Union (AU): Digital Transport & Smart Mobility Policy Framework

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing trend analysis

- 3.9 Business Models and Monetization Framework

- 3.9.1 Revenue Models

- 3.9.2 Value Chain and Ecosystem

- 3.9.3 Go-to-Market Strategy

- 3.10 Data Governance, Cybersecurity, and System Risk

- 3.10.1 Passenger Data Privacy and Compliance

- 3.10.2 Transit Network and System Security

- 3.10.3 Operational and Service Continuity Risks

- 3.11 System Architecture

- 3.11.1 Multi-layer Passenger Information Delivery Models

- 3.11.2 Multimodal Transit Network Integration and Connectivity

- 3.12 Patent analysis

- 3.13 Threat Landscape

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable Practices in Transit Technology Deployment

- 3.14.2 Energy Efficiency in Display and Communication Infrastructure

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Displays

- 5.2.2 Networking devices

- 5.2.3 Sensors

- 5.2.4 Communication devices

- 5.2.5 Others

- 5.3 Software

- 5.3.1 Data management software

- 5.3.2 Information display software

- 5.4 Services

- 5.4.1 Professional Services

- 5.4.2 Managed Services

Chapter 6 Market Estimates & Forecast, By Mode of Transport, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Roadways

- 6.3 Railways

- 6.4 Airways

- 6.5 Waterways

Chapter 7 Market Estimates & Forecast, By Deployment Type, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 On-premise

- 7.3 Cloud-based

Chapter 8 Market Estimates & Forecast, By Solution, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Information Display Systems

- 8.3 Announcement Systems

- 8.4 Emergency Communication Systems

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.3.8 Norway

- 9.3.9 Denmark

- 9.3.10 Netherlands

- 9.3.11 Belgium

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.4.8 Singapore

- 9.4.9 Malaysia

- 9.4.10 Thailand

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global companies

- 10.1.1 Advantech Co. Ltd.

- 10.1.2 Alstom SA

- 10.1.3 Cisco Systems Inc.

- 10.1.4 Cubic Corporation

- 10.1.5 Hitachi, Ltd.

- 10.1.6 Huawei Technologies Co., Ltd.

- 10.1.7 Indra Sistemas SA

- 10.1.8 Mitsubishi Electric Corporation

- 10.1.9 Nokia

- 10.1.10 Siemens Mobility

- 10.1.11 ST Engineering Ltd

- 10.1.12 Thales Group

- 10.1.13 Wabtec Corporation

- 10.2 Regional players

- 10.2.1 Dysten Sp. z o.o.

- 10.2.2 Efftronics Systems Pvt Ltd

- 10.2.3 Icon Multimedia

- 10.2.4 Medha Servo Drives Pvt Ltd

- 10.2.5 r2p Group

- 10.2.6 Teleste Corporation

- 10.2.7 Televic Group

- 10.2.8 Eke-Electronics

- 10.2.9 Quester Tangent

- 10.2.10 Simpleway

- 10.2.11 Passio Technologies

乘客資訊系統市場 - 全球產業規模、佔有率、趨勢、機會、預測:按組件、安裝位置、解決方案類型、運輸方式、地區和競爭格局分類,2021-2031年

乘客資訊系統市場 - 全球產業規模、佔有率、趨勢、機會、預測:按組件、安裝位置、解決方案類型、運輸方式、地區和競爭格局分類,2021-2031年 乘客資訊系統市場報告:按交通方式、組件、系統類型、安裝位置和地區分類,2026-2034 年飛機機艙乘客通訊系統市場報告:按組件、飛機、銷售管道和地區分類(2026-2034 年)

乘客資訊系統市場報告:按交通方式、組件、系統類型、安裝位置和地區分類,2026-2034 年飛機機艙乘客通訊系統市場報告:按組件、飛機、銷售管道和地區分類(2026-2034 年) 乘客資訊系統市場:按組件、通訊管道、應用、最終用戶和部署方式分類-2026-2032年全球市場預測

乘客資訊系統市場:按組件、通訊管道、應用、最終用戶和部署方式分類-2026-2032年全球市場預測 2026年全球旅客資訊系統市場報告自動化乘客資訊系統市場:按組件、系統類型、交付模式、最終用戶和部署類型分類-2026-2032年全球預測2026年全球自動乘客引導系統市場報告

2026年全球旅客資訊系統市場報告自動化乘客資訊系統市場:按組件、系統類型、交付模式、最終用戶和部署類型分類-2026-2032年全球預測2026年全球自動乘客引導系統市場報告 2026-2030年全球旅客資訊系統市場

2026-2030年全球旅客資訊系統市場 乘客資訊系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、模組及功能分類日本乘客資訊系統市場報告(按交通方式、組件、位置、系統類型和地區分類,2026-2034 年)

乘客資訊系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、模組及功能分類日本乘客資訊系統市場報告(按交通方式、組件、位置、系統類型和地區分類,2026-2034 年)