|

市場調查報告書

商品編碼

2027520

家用健身器材市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Home Gym Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

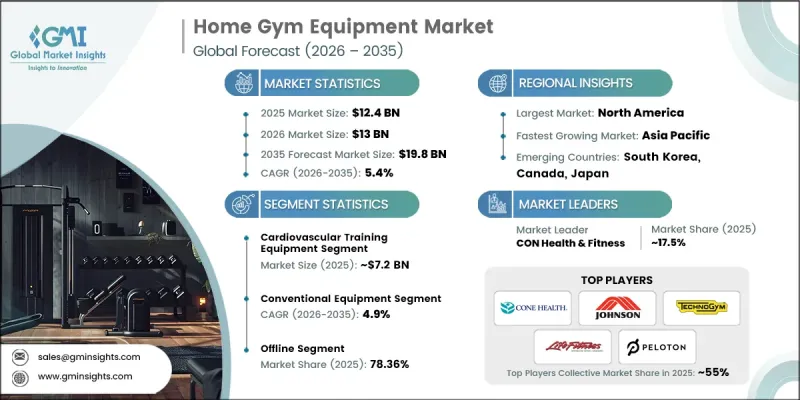

預計到 2025 年,全球家用健身器材市場規模將達到 124 億美元,年複合成長率為 5.4%,到 2035 年將達到 198 億美元。

隨著消費者越來越重視健身的便利性和柔軟性,市場正穩步擴張。許多人正在遠離傳統的健身中心,轉而投資個人化的家庭健身解決方案。緊湊型多功能健身器材尤其受到空間有限的都市區的青睞,因為它們無需大規模設施即可實現高效訓練。遠距辦公和混合辦公等工作方式的轉變進一步加速了對家庭健身解決方案的需求。日益增強的健康意識也發揮著重要作用,消費者專注於規律的體能活動以控制體重並降低文明病的風險。透過零售商店和電商平台輕鬆購買,以及豐富的價格選擇,持續推動不同消費族群對居家健身產品的接受度。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 起始金額 | 124億美元 |

| 預測金額 | 198億美元 |

| 複合年成長率 | 5.4% |

預計到2025年,有氧運動器材市場規模將達到72億美元,並在2026年至2035年間以5.5%的複合年成長率成長。該細分市場之所以能夠推動成長,是因為它能有效提高耐力、心血管健康和整體健身水平。專為有氧運動設計的器材在家庭環境中越來越受歡迎,因為它們能夠滿足不同健身水平的需求,並支援靈活的訓練計劃。人們對文明病的日益關注進一步推動了市場需求,而緊湊型設計和性能追蹤功能的進步也提高了其在住宅環境中的易用性。

預計到2025年,傳統健身器材市佔率將達到73.3%,並在2035年之前以4.9%的複合年成長率成長。其強大的市場地位得益於價格實惠、操作簡便和易於使用。這些產品無需高科技或連網功能即可提供可靠的基礎訓練效能,因此深受廣大消費者的青睞。其耐用性、低維護成本和成本績效持續吸引尋求實用高效家用健身解決方案的用戶。

美國家用健身器材市場預計到2025年將達到35億美元,並在2026年至2035年間以5.1%的複合年成長率成長。市場成長的主要驅動力是人們健康意識的提高、對健身日益成長的興趣以及居家運動的便利性。消費者尤其青睞節省空間、功能多樣的器材,以適應有限的生活空間。彈性辦公模式的普及也進一步加速了市場擴張。製造商正致力於打造耐用的產品設計、直覺的介面以及與數位健身平台的整合,以提升用戶體驗,同時也在拓展零售和電商管道,以改善產品供應和供應鏈。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 成長促進因素

- 人們越來越傾向於選擇便利靈活的居家健身解決方案

- 健康意識的提高以及對健身和健康的日益關注

- 遠距辦公和混合辦公模式的普及

- 潛在風險和挑戰

- 高級家用健身器材的初始成本較高

- 都市區家庭收納空間不足

- 機會

- 對訂閱制的虛擬健身平台的需求日益成長

- 折疊式和模組化設備設計的應用日益廣泛

- 成長促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析(基於初步研究)

- 根據業務類型分類的定價策略(高階/價值/成本加成)(基於初步調查)

- 智慧型設備價格溢價分析

- 區域價格波動與購買力平價

- 折扣和促銷策略

- 貿易資料分析(HS編碼9506.9)(基於付費資料庫)

- 進出口量和進口額趨勢(基於付費資料庫)

- 主要貿易走廊和關稅的影響(基於初步調查)

- 主要出口國(中國、台灣、越南)

- 主要進口國(美國、德國、英國)

- HS編碼分類與貿易流量趨勢

- 分銷基礎設施和通路滲透狀況(基於初步調查)

- 按地區和類型(現代零售與傳統零售)分類的通路覆蓋率(基於初步調查)

- 最後一公里基礎設施差異和新分銷管道的變化(基於初步研究)

- 電子商務履約能力與配送挑戰

- 零售商店密度和區域分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依設備類型分類,2022-2035年

- 有氧運動器材

- 跑步機

- 健身腳踏車

- 划船機

- 橢圓機及其他物品

- 爬樓機/踏步機

- 其他

- 肌力訓練器材

- 啞鈴

- 槓鈴

- 車身桿

- 壺鈴

- 阻力帶

- 其他

第6章 市場估計與預測:依類別分類,2022-2035年

- 常規飛機

- 智慧型裝置

第7章 市場估計與預測:依價格區間分類,2022-2035年

- 低的

- 中等的

- 高級/特級

第8章 市場估算與預測:依通路分類,2022-2035年

- 線上

- 電子商務

- 第三方網站/企業網站

- 離線

- 超級市場/大賣場

- 多品牌商店

- 體育用品專賣店/獨立百貨商店

- 專賣店/運動連鎖店

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第10章:公司簡介

- Assault Fitness

- Body-Solid

- Echelon Fitness

- Hydrow

- ICON Health & Fitness

- Johnson Health Tech

- Life Fitness

- Nautilus, Inc.

- NOHrD

- Peloton Interactive

- Precor(Amer Sports)

- Speediance

- Technogym

- Tonal Systems

- TRUE Fitness

The Global Home Gym Equipment Market was valued at USD 12.4 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 19.8 billion by 2035.

The market is expanding steadily as consumers increasingly prioritize convenience and flexibility in their fitness routines. Many individuals are shifting away from traditional fitness centers and investing in personalized workout solutions within their homes. Compact and multifunctional equipment is gaining strong traction, especially among urban households with limited space, as it enables effective workouts without requiring large setups. Changing work patterns, including remote and hybrid arrangements, have further accelerated the demand for at-home fitness solutions. Rising health awareness is also playing a crucial role, with consumers focusing on regular physical activity to manage weight and reduce the risk of lifestyle-related conditions. The ease of purchasing through retail stores and e-commerce platforms, combined with a wide range of products across price points, continues to support strong adoption across diverse consumer segments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.4 Billion |

| Forecast Value | $19.8 Billion |

| CAGR | 5.4% |

The cardiovascular training equipment segment generated USD 7.2 billion in 2025 and is expected to grow at a CAGR of 5.5% from 2026 to 2035. This segment dominates due to its effectiveness in improving endurance, heart health, and overall fitness levels. Equipment designed for cardiovascular workouts is widely adopted in home settings because it accommodates varying fitness levels and supports flexible routines. Growing awareness of lifestyle-related health concerns has further strengthened demand, while advancements in compact design and performance tracking features enhance usability in residential environments.

The conventional equipment segment accounted for 73.3% share in 2025 and is projected to grow at a CAGR of 4.9% through 2035. Its strong market position is driven by affordability, simplicity, and ease of use. These products deliver reliable performance for basic workouts without requiring advanced technology or connectivity, making them accessible to a broad consumer base. Their durability, low maintenance requirements, and cost-effectiveness continue to attract users seeking practical and efficient fitness solutions at home.

United States Home Gym Equipment Market captured USD 3.5 billion in 2025 and is expected to grow at a CAGR of 5.1% from 2026 to 2035. Market growth is supported by rising health consciousness, increasing interest in fitness, and the convenience of home-based workouts. Consumers are showing a strong preference for space-efficient and multifunctional equipment suited for smaller living spaces. The growing influence of flexible work lifestyles has further accelerated adoption. Manufacturers are focusing on durable designs, intuitive interfaces, and integration with digital fitness platforms to enhance user experience, while expanding retail and e-commerce channels to improve accessibility and product availability.

Key players operating in the Global Home Gym Equipment Market include Assault Fitness, Body-Solid, Echelon Fitness, Hydrow, ICON Health & Fitness, Johnson Health Tech, Life Fitness, Nautilus, Inc., NOHrD, Peloton Interactive, Precor (Amer Sports), Speediance, Technogym, Tonal Systems, and TRUE Fitness. Companies in the Home Gym Equipment Market strengthen their position by investing in product innovation, focusing on compact, multifunctional, and space-saving designs tailored for modern households. Integration of digital technologies, including connected fitness platforms and performance tracking, enhances user engagement and differentiation. Strategic partnerships with fitness platforms and subscription-based services help expand recurring revenue streams. Brands also emphasize omnichannel distribution, leveraging both online and offline retail networks to maximize reach. Marketing initiatives, influencer collaborations, and personalized fitness experiences further improve brand visibility. Additionally, companies prioritize durability, affordability, and customization options to cater to diverse consumer needs, ensuring sustained growth and competitive advantage in the evolving market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment Type

- 2.2.3 Category

- 2.2.4 Price Range

- 2.2.5 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing preference for convenient and flexible workout solutions at home

- 3.2.1.2 Rising health awareness and focus on fitness and wellness

- 3.2.1.3 Expansion of remote work and hybrid lifestyles

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High upfront cost of advanced home gym equipment

- 3.2.2.2 Limited space availability in urban households

- 3.2.3 Opportunities

- 3.2.3.1 Growing demand for subscription-based virtual fitness platforms

- 3.2.3.2 Rising adoption of foldable and modular equipment designs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Pricing analysis (driven by primary research)

- 3.9.1 Historical price trend analysis (driven by primary research)

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.9.3 Smart equipment price premium analysis

- 3.9.4 Regional price variations & purchasing power parity

- 3.9.5 Discounting & promotional strategies

- 3.10 Trade data analysis (HS code 9506.9) (driven by paid database)

- 3.10.1 Import/export volume & value trends (driven by paid database)

- 3.10.2 Key trade corridors & tariff impact (driven by primary research)

- 3.10.3 Top exporting countries (China, Taiwan, Vietnam)

- 3.10.4 Top importing countries (U.S., Germany, UK)

- 3.10.5 HS code classification & trade flow dynamics

- 3.11 Distribution infrastructure & channel penetration landscape (driven by primary research)

- 3.11.1 Channel coverage by region & format (modern vs. traditional trade) (driven by primary research)

- 3.11.2 Last-mile infrastructure gaps & emerging channel shifts (driven by primary research)

- 3.11.3 E-commerce fulfillment capacity & delivery challenges

- 3.11.4 Retail store density & geographic coverage analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Equipment Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Cardiovascular Training Equipment

- 5.2.1 Treadmills

- 5.2.2 Exercise Bikes

- 5.2.3 Rowing Machines

- 5.2.4 Elliptical and others

- 5.2.5 Stair Climber/Step mill

- 5.2.6 Others

- 5.3 Strength Training Equipment

- 5.3.1 Dumbbells

- 5.3.2 Barbells

- 5.3.3 Body Bars

- 5.3.4 Kettlebells

- 5.3.5 Resistance Band

- 5.3.6 Others

Chapter 6 Market Estimates & Forecast, By Category, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Conventional Equipment

- 6.3 Smart Equipment

Chapter 7 Market Estimates & Forecast, By Price Range, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High/Premium

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Online

- 8.2.1 E-commerce

- 8.2.2 Third Party Website/Company Website

- 8.3 Offline

- 8.3.1 Supermarkets/Hypermarkets

- 8.3.2 Multi-Brand Stores

- 8.3.3 Sport Stores/ Independent Departmental Stores

- 8.3.4 Specialty Stores/Sports Chain Outlets

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Assault Fitness

- 10.2 Body-Solid

- 10.3 Echelon Fitness

- 10.4 Hydrow

- 10.5 ICON Health & Fitness

- 10.6 Johnson Health Tech

- 10.7 Life Fitness

- 10.8 Nautilus, Inc.

- 10.9 NOHrD

- 10.10 Peloton Interactive

- 10.11 Precor (Amer Sports)

- 10.12 Speediance

- 10.13 Technogym

- 10.14 Tonal Systems

- 10.15 TRUE Fitness

健身器材市場:商機、成長要素、產業趨勢分析及2026-2035年預測

健身器材市場:商機、成長要素、產業趨勢分析及2026-2035年預測 全球數位化健身器材市場-按類型、最終用途、分銷管道、地區和競爭格局分類的行業規模、佔有率、趨勢、機會和預測(2021-2031年)智慧家庭健身器材市場-全球產業規模、佔有率、趨勢、機會及預測:依產品類型、通路、地區及競爭格局分類,2021-2031年

全球數位化健身器材市場-按類型、最終用途、分銷管道、地區和競爭格局分類的行業規模、佔有率、趨勢、機會和預測(2021-2031年)智慧家庭健身器材市場-全球產業規模、佔有率、趨勢、機會及預測:依產品類型、通路、地區及競爭格局分類,2021-2031年 家用健身器材市場規模、佔有率及成長分析(按產品類型、應用、分銷管道和地區分類)-2026-2033年產業預測

家用健身器材市場規模、佔有率及成長分析(按產品類型、應用、分銷管道和地區分類)-2026-2033年產業預測 日本健身器材市場規模、佔有率、趨勢及預測(按產品類型、配銷通路、買家類型和地區分類,2026-2034年)

日本健身器材市場規模、佔有率、趨勢及預測(按產品類型、配銷通路、買家類型和地區分類,2026-2034年) 全球居家健身器材市場

全球居家健身器材市場 2026 年至 2032 年家庭健身器材市場(依產品類型、通路和地區)全球智慧家庭健身器材市場

2026 年至 2032 年家庭健身器材市場(依產品類型、通路和地區)全球智慧家庭健身器材市場 智慧家庭健身設備市場(產品類型:心血管訓練設備和肌力訓練設備;類型:折疊式和固定式)- 2024-2034 年全球產業分析、規模、佔有率、成長、趨勢和預測

智慧家庭健身設備市場(產品類型:心血管訓練設備和肌力訓練設備;類型:折疊式和固定式)- 2024-2034 年全球產業分析、規模、佔有率、成長、趨勢和預測 印度健身器材市場評估:依產品、最終用戶、定價、分銷管道和地區劃分的機會和預測(2018-2032)

印度健身器材市場評估:依產品、最終用戶、定價、分銷管道和地區劃分的機會和預測(2018-2032)