|

市場調查報告書

商品編碼

2027494

液氫市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測Liquid Hydrogen Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

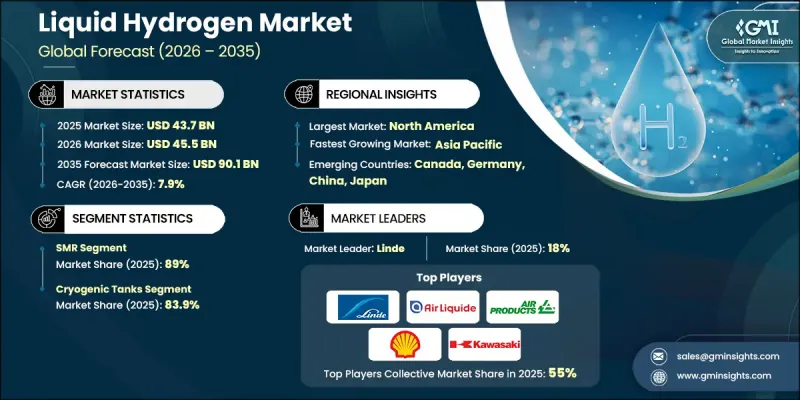

預計到 2025 年,全球液氫市場價值將達到 437 億美元,並預計以 7.9% 的複合年成長率成長,到 2035 年達到 901 億美元。

市場擴張主要得益於氫能樞紐的興起,這些樞紐實現了氫氣的集中生產、儲存和分銷,從而提高了營運效率,並加速了氫氣在各行業的應用。對脫碳目標的日益重視,以及主要經濟體對氫能策略的持續推進,進一步刺激了市場需求。產業相關人員正積極在交通運輸、工業活動和能源系統中部署氫能解決方案,同時不斷擴展基礎設施並進行長期戰略投資。氫能技術的進步以及技術供應商和能源公司之間合作的加強正在重塑競爭格局。同時,跨境夥伴關係和全球協作正在整合供應鏈並加速基礎設施建設。公私合營的增加和策略性投資的推進進一步推動了產業成長。液化和低溫儲存技術的進步提高了擴充性和部署效率。此外,包括蒸汽甲烷重整、煤基製程和電解在內的生產方法的革新,正在增強供給能力。這些發展,加上監管獎勵、成本最佳化策略以及更清潔的原料和碳捕獲技術的整合,正在促進排放和更廣泛的市場滲透。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 437億美元 |

| 預測金額 | 901億美元 |

| 複合年成長率 | 7.9% |

預計到2025年,蒸汽甲烷重整製氫領域將佔據89%的市場佔有率,並在2035年之前保持7.5%的複合年成長率。生產設施的擴建和現代化改造日益受到重視,這是推動該領域成長的主要動力。為滿足各產業日益成長的氫氣需求,大型氫氣生產廠的建設正在加速推進,同時碳捕獲技術的應用也提升了環境績效。氫氣作為主要能源載體的日益普及,進一步加速了此氫氣方法在長期能源轉型策略中的應用。

預計到2035年,管道運輸環節的複合年成長率將達到8.5%。氫能基礎設施網路的擴張,以及互聯互通的工業設施和眾多終端用戶的支持,正在推動該環節的成長。這些供應系統在提高特定區域供應效率的同時,也為大規模部署提供了支援。對安全標準和法規結構的日益重視,以及技術的不斷進步,正在增強氫能運輸系統的可靠性和性能。此外,特定條件下的氫氣管理需求也推動了管道設計和營運方法的創新。

預計到2025年,美國液氫市場將佔據77.5%的全球佔有率,市場規模將達到167億美元。美國市場成長的主要驅動力是交通運輸業的擴張以及旨在減少對傳統燃料依賴的氫動力出行解決方案的日益普及。政府的各項措施和財政獎勵在加速氫能技術的應用方面發揮著至關重要的作用,而對大規模基礎設施項目的投資則進一步推動了市場擴張。對先進氫能生態系統的支持正在促進氫能技術融入各種工業和能源應用領域,有助於維持市場需求的持續成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 產業生態系統

- 原物料供應及採購分析

- 供應鏈韌性與風險因素

- 配電網路分析

- 監理情勢

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 波特五力分析

- PESTEL 分析

- 成本結構分析

- 價格趨勢分析,2022-2035年

- 透過生產方法

- 國家

- 新機會和趨勢

- 數位化和物聯網整合

- 投資分析及未來展望

第4章 競爭情勢

- 介紹

- 企業市佔率分析:按地區分類

- 北美洲

- 歐洲

- 亞太地區

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場規模及預測:依製造方法分類,2022-2035年

- 煤炭氣化

- SMR

- 電解

第6章 市場規模及預測:以分銷方式分類,2022-2035年

- 管道

- 低溫儲罐

第7章 市場規模及預測:依應用領域分類,2022-2035年

- 運輸

- 化學

- 其他

第8章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 世界其他地區

第9章:公司簡介

- Air Products and Chemicals

- Air Liquide

- Chart Industries

- Cryospain

- Cryostar

- Cummins

- ENGIE

- GE Appliances

- GENH2

- HTEC

- INOX India Limited

- Iwatani Corporation

- Kawasaki Heavy Industries

- Linde plc

- Matheson Tri-Gas

- Messer

- Plug Power

- Sarnia-Lambton

- Salzburger Aluminium Group

- Shell plc

The Global Liquid Hydrogen Market was valued at USD 43.7 billion in 2025 and is estimated to grow at a CAGR of 7.9% to reach USD 90.1 billion by 2035.

Market expansion is supported by the emergence of hydrogen hubs that enable centralized production, storage, and distribution, thereby improving operational efficiency and accelerating adoption across industries. Increasing emphasis on decarbonization targets, along with the growing implementation of hydrogen-focused strategies across major economies, is further strengthening demand. Industry participants are actively deploying hydrogen solutions across transportation, industrial operations, and energy systems while simultaneously expanding infrastructure and making long-term strategic investments. Advancements in hydrogen technologies and increasing collaboration among technology providers and energy companies are shaping the competitive landscape. At the same time, cross-border partnerships and global alliances are enhancing supply chain integration and accelerating infrastructure development. Rising public-private collaborations and strategic investments are further supporting industry expansion. Progress in liquefaction and cryogenic storage technologies is improving scalability and deployment efficiency. In addition, evolving production methods, including steam methane reforming, coal-based processes, and electrolysis, are enhancing supply capabilities. These developments, combined with regulatory incentives, cost optimization strategies, and the integration of cleaner feedstocks and carbon capture technologies, are contributing to lower emissions and broader market adoption.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $43.7 Billion |

| Forecast Value | $90.1 Billion |

| CAGR | 7.9% |

The steam methane reforming segment accounted for 89% share in 2025 and is expected to grow at a CAGR of 7.5% through 2035. Increasing focus on expanding and upgrading production facilities is driving the growth of this segment. The development of large-scale production plants to meet rising hydrogen demand across industries is gaining momentum, while the integration of carbon capture technologies is improving environmental performance. The recognition of hydrogen as a key energy carrier is further encouraging the adoption of this production method as part of long-term energy transition strategies.

The pipeline segment is anticipated to grow at a CAGR of 8.5% by 2035. Expanding hydrogen infrastructure networks, supported by interconnected industrial facilities and multiple end users, are driving segment growth. These distribution systems are enhancing supply efficiency within defined regions while supporting large-scale deployment. Increasing attention to safety standards and regulatory frameworks, along with continuous technological improvements, is strengthening the reliability and performance of hydrogen transportation systems. The need to manage hydrogen under specialized conditions is also encouraging innovation in pipeline design and operational practices.

United States Liquid Hydrogen Market held a share of 77.5% in 2025, generating USD 16.7 billion. Market growth in the country is supported by the expanding transportation sector and the increasing adoption of hydrogen-powered mobility solutions aimed at reducing reliance on conventional fuels. Government initiatives and financial incentives are playing a crucial role in accelerating adoption, while investments in large-scale infrastructure projects are further strengthening market expansion. Support for advanced hydrogen ecosystems is encouraging the integration of hydrogen technologies into multiple industrial and energy applications, contributing to sustained demand growth.

Key players operating in the Global Liquid Hydrogen Market include Air Products & Chemicals, Linde Plc, Shell, ENGIE, Cummins, Mitsubishi Heavy Industries, Air Liquide, Iwatani Corporation, Chart Industries, Plug Power, Messer, Kawasaki Heavy Industries, Cryostar, Cryospain, GenH2, HTEC, Matheson Tri-Gas, Ayrton Energy, Sarnia-Lambton, and GE Appliances. Key strategies adopted by companies in the Liquid Hydrogen Market focus on expanding production capacity through large-scale facility development and enhancing technological capabilities in liquefaction and storage systems. Companies are actively forming strategic alliances and joint ventures to strengthen global supply chains and accelerate infrastructure deployment. Significant investments in research and development are enabling advancements in efficient production methods and carbon capture integration to reduce emissions. Market players are also focusing on geographic expansion by establishing hydrogen hubs and distribution networks to improve accessibility. Additionally, firms are prioritizing cost optimization strategies and adopting cleaner feedstocks to enhance sustainability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Production method trends

- 2.4 Distribution method trends

- 2.5 End use trends

- 2.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Supply chain resilience & risk factors

- 3.1.3 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis

- 3.8 Price trend analysis, 2022-2035

- 3.8.1 By Production Method

- 3.8.2 By Country

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.10 Investment analysis & future outlook

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans & funding

Chapter 5 Market Size and Forecast, By Production Method, 2022 - 2035 (USD Billion & MT)

- 5.1 Key trends

- 5.2 Coal Gasification

- 5.3 SMR

- 5.4 Electrolysis

Chapter 6 Market Size and Forecast, By Distribution Method, 2022 - 2035 (USD Billion & MT)

- 6.1 Key trends

- 6.2 Pipelines

- 6.3 Cryogenic Tanks

Chapter 7 Market Size and Forecast, By Application, 2022 - 2035 (USD Billion & MT)

- 7.1 Key trends

- 7.2 Transportation

- 7.3 Chemical

- 7.4 Others

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Billion & MT)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Rest of World

Chapter 9 Company Profiles

- 9.1 Air Products and Chemicals

- 9.2 Air Liquide

- 9.3 Chart Industries

- 9.4 Cryospain

- 9.5 Cryostar

- 9.6 Cummins

- 9.7 ENGIE

- 9.8 GE Appliances

- 9.9 GENH2

- 9.10 HTEC

- 9.11 INOX India Limited

- 9.12 Iwatani Corporation

- 9.13 Kawasaki Heavy Industries

- 9.14 Linde plc

- 9.15 Matheson Tri-Gas

- 9.16 Messer

- 9.17 Plug Power

- 9.18 Sarnia-Lambton

- 9.19 Salzburger Aluminium Group

- 9.20 Shell plc

北美液氫市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)液氫:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

北美液氫市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)液氫:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026 年至 2035 年電解氫的市場機會、成長要素、產業趨勢與預測。

2026 年至 2035 年電解氫的市場機會、成長要素、產業趨勢與預測。 液氫市場規模、佔有率和趨勢分析報告:按生產方法、分銷方法、地區和細分市場預測(2026-2033 年)

液氫市場規模、佔有率和趨勢分析報告:按生產方法、分銷方法、地區和細分市場預測(2026-2033 年) 化學液氫市場規模、佔有率和成長分析:按純度、製造方法、儲存類型、應用、最終用戶和地區分類-2026-2033年產業預測

化學液氫市場規模、佔有率和成長分析:按純度、製造方法、儲存類型、應用、最終用戶和地區分類-2026-2033年產業預測 液氫市場規模、佔有率及成長分析(依生產方式、分銷方式、終端用戶產業及地區分類)-2026-2033年產業預測

液氫市場規模、佔有率及成長分析(依生產方式、分銷方式、終端用戶產業及地區分類)-2026-2033年產業預測 全球煤炭氣化液氫市場全球電解液氫市場化學液氫全球市場全球液氫市場

全球煤炭氣化液氫市場全球電解液氫市場化學液氫全球市場全球液氫市場