|

市場調查報告書

商品編碼

1692454

液氫-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Liquid Hydrogen - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

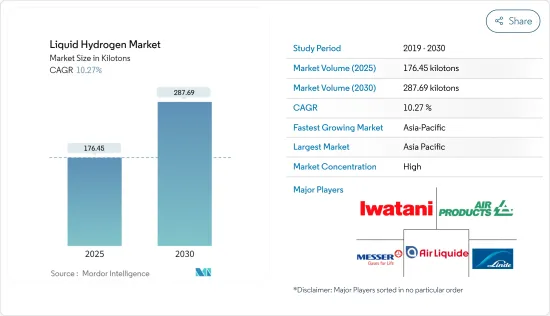

液氫市場規模預計在 2025 年為 176.45 千噸,預計在 2030 年達到 287.69 千噸,預測期內(2025-2030 年)的複合年成長率為 10.27%。

由於所有行業都停止了生產流程,COVID-19 對市場產生了負面影響。封鎖、社交隔離和貿易制裁已對全球供應鏈網路造成嚴重破壞。不過,預計這種情況將在 2021 年恢復,有利於預測期內的市場。

主要亮點

- 從中期來看,太空探勘對液態氫的需求不斷成長以及商用汽車對氫燃料電池的日益普及是推動市場發展的關鍵因素。

- 然而,與處理和儲存相關的高成本可能會抑制市場成長。

- 人們對氫氣作為船用燃料的使用日益重視以及航太工業的技術創新可能會在未來幾年為市場提供機會。

- 亞太地區貢獻了最高的市場佔有率,並可能在預測期內佔據市場主導地位。

液氫市場趨勢

航太航太業佔市場主導地位

- 航太工業代表了液氫在各種應用中的應用,從機場行李處理到氫動力飛機推進,再到太空產業的低溫引擎。

- 對於推進應用,液氫與液態氧等氧化劑結合用作燃料。這種組合使其具有已知火箭推進劑中最高的比衝,或相對於消耗的推進劑量的效率。

- 根據國際航空運輸協會(IATA)的預測,2021年全球商業航空公司的銷售額將達到4,720億美元,2022年將達到7,270億美元,與前一年同期比較去年同期成長43.6%。預計到 2023 年底將達到 7,790 億美元。

- 隨著空中交通從疫情引發的放緩中復甦,各國正加強溫室氣體排放法規,推動航空業走向碳中和。例如,2022年6月,美國聯邦航空管理局提案了新的氣候規則,以遏止溫室氣體排放。新規則將適用於已投入使用的飛機,並允許製造商改善動態和引擎效率。該規則對尚未獲得認證的新型亞音速噴射機、大型渦輪螺旋槳飛機和螺旋槳飛機以及2028年1月後製造的飛機提出了效率要求。

- 世界各地的太空計畫都依賴液態氫作為各種航太計畫的火箭燃料。近年來,太空計畫的成長推動了對液態氫的需求。

- 2022年,全球各國政府在太空計畫上的支出大幅增加。以美國為例,政府支出從2021年的545.9億美元增加到2022年的619.7億美元。

- 技術進步的快速成長正在產生對更先進衛星的需求。結果,2022 年嘗試了 186 次以上的軌道發射,其中 180 次成功。

- 據美國國家航空暨太空總署太空總署稱,太空梭的火箭引擎在每次發射過程中消耗約 50 萬加侖的冷凍液氫,另外在儲存蒸發和轉移操作中還會消耗 239,000 加侖。每次發射的消費量增加以及發射頻率的增加正在推動對液氫的需求。

- 因此,預計預測期內航太工業對液氫的需求將會成長。

亞太地區佔市場主導地位

- 由於中國、印度和日本等國家對液氫的需求不斷增加,預計亞太地區將在預測期內成為最大的液氫市場。

- 由於對替代燃料的需求強勁,尤其是在航太和汽車產業,中國已成為液氫強大且利潤豐厚的市場。隨著航太領域的顯著成長,包括衛星發射和火箭任務數量的增加,對液氫的需求正在急劇增加,因為它在火箭燃料中發揮著至關重要的作用。

- 中國燃料電池汽車銷售和產量的不斷成長也促進了液氫燃料電池的需求成長。根據中國工業協會預測,2022年氫燃料電池汽車產銷將分別達到3,626輛和3,367輛,較前一年增加一倍以上。

- 氫燃料已顯示出作為飛機和汽車動力來源的潛力,印度正在大力發展和努力推動氫引擎的發展。例如,2023年2月,信實工業有限公司和阿蕭克利蘭推出了印度首款氫內燃機(H2-ICE)驅動的重型卡車。該卡車將使用氫氣驅動,同時保留傳統的柴油內燃機結構。 H2-ICE 卡車的負載容量為 19 至 35 噸,能夠以相對較低的成本差異快速過渡到更清潔的能源。

- 根據汽車檢查和登記資訊協會 (AIRIA) 的數據,截至 2022 年 3 月 31 日,日本共有約 7,110 輛氫燃料電池汽車投入使用,高於 2021 會計年度的 5,280 輛。這些氫燃料電池汽車大部分是以氫氣為動力的乘用車。

- 因此,受上述因素影響,預計預測期內亞太地區液氫需求將會增加。

液氫產業概況

液氫市場高度整合。市場的主要企業(不分先後順序)包括液化空氣集團、空氣產品和化學品公司、林德集團、巖谷公司和梅塞爾Group Limited。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 太空探勘對液態氫的需求不斷增加

- 氫燃料電池在商用車輛的應用日益增多

- 限制因素

- 高成本

- 其他阻礙因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔

- 分配

- 低溫儲罐

- 高壓管拖車

- 最終用戶產業

- 車

- 航太(包括航太)

- 海洋

- 其他最終用戶產業

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 世界其他地區

- 南美洲

- 中東和非洲

- 亞太地區

第6章競爭格局

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- Air Liquide

- Air Products and Chemicals, Inc.

- Iwatani Corporation

- Linde PLC

- Messer Group GMBH

- Nippon Sanso Holdings Corporation

- Universal Industrial Gases Inc.

第7章 市場機會與未來趨勢

- 氫氣作為船用燃料日益受到重視

- 航太工業技術創新的進步

The Liquid Hydrogen Market size is estimated at 176.45 kilotons in 2025, and is expected to reach 287.69 kilotons by 2030, at a CAGR of 10.27% during the forecast period (2025-2030).

COVID-19 negatively impacted the market as all the industries halted their manufacturing processes. Lockdowns, social distances, and trade sanctions triggered massive disruptions to global supply chain networks. However, the condition is recovered in 2021, which is expected to benefit the market during the forecast period.

Key Highlights

- In the medium term, the major factors driving the market studied are the growing demand for liquid hydrogen for space exploration and the increasing adoption of hydrogen fuel cells in commercial vehicles.

- On the flip side, the high cost associated with handling and storage is likely to restrain the market growth.

- Growing emphasis on utilizing hydrogen as a marine fuel and increasing innovations in the aerospace industry are likely to act as opportunities for the market in the coming years.

- Asia-Pacific accounted for the highest market share, and the region is likely to dominate the market during the forecast period.

Liquid Hydrogen Market Trends

Aerospace Industry to Dominate the Market

- Aerospace industries imply the application of liquid hydrogen for various applications ranging from airport bagging handling to hydrogen aircraft propulsion to cryogenic engines in the space industry.

- In propulsion applications, liquid hydrogen is used in combination with an oxidizer, such as liquid oxygen, to serve as fuel. This combination yields the highest specific impulse, or efficiency in relation to the amount of propellant consumed, of any known rocket propellant.

- According to the International Air Transport Association (IATA), the global revenue for commercial airlines was valued at USD 472 billion in 2021 and USD 727 billion in 2022, registering a growth rate of 43.6% Y-o-Y. Furthermore, the revenue is expected to reach USD 779 billion by the end of 2023.

- As air traffic recovers from the pandemic slowdown, the regulations on controlling greenhouse gas emissions are being tightened in different economies to head forward with the transition to carbon neutrality in the aviation sector. For instance, the Federal Aviation Administration, in June 2022, proposed new climate rules for curtailing GHG emissions. The new rules will be applied to planes already in service, allowing manufacturers to improve aerodynamics and engine efficiency. The rules would enforce efficiency requirements for new subsonic jet aircraft, large turboprop and propellor planes that are not yet certified, and planes built after January 2028.

- Space programs across the world rely on liquid hydrogen as the rocket fuel for various aerospace operations. The recent growth in space programs has been driving the demand for liquid hydrogen in recent years.

- In 2022, global government expenditure for space programs in various countries increased considerably. For instance, in the United States, government spending grew from USD 54.59 billion in 2021 to USD 61.97 billion in 2022.

- Rapid growth in technological advancements is creating the demand for more advanced satellites. As a result, in 2022, over 186 attempts of orbital launches, of which 180 were successful.

- According to the National Aeronautics and Space Administration (NASA), for each launch, the rocket engines of each shuttle flight burn about 500,000 gallons of cold liquid hydrogen, with another 239,000 gallons depleted by storage boil-off and transfer operations. The large volume of consumption per operation, coupled with the growing frequency of launches, is propelling the demand for liquid hydrogen.

- Therefore, the demand for liquid hydrogen is expected to grow in the aerospace industry during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to be the largest market for liquid hydrogen during the forecast period owing to the growing liquid hydrogen demand in China, India, and Japan, among others.

- China's strong inclination toward alternative fuels, particularly in the aerospace and automotive industries, positions the country as a robust and favorablemarket for liquid hydrogen. With substantial growth in the aerospace sector, including increased satellite launches and rocket missions, the demand for liquid hydrogen has witnessed a positive surge due to its essential role in rocket fuel.

- The rising sales and production of fuel cell vehicles in China have also contributed to the growing demand for liquid hydrogen-based fuel cells. According to the China Association of Automobile Manufacturers, the production and sales of hydrogen fuel cell vehicles in 2022 more than doubled compared to the previous year, with 3,626 and 3,367 units produced and sold, respectively.

- Hydrogen fuel presents opportunities for powering aircraft and automobiles, and significant developments and initiatives are taking place in India to advance hydrogen-powered engines. For instance, in February 2023, Reliance Industries Limited and Ashok Leyland launched India's first Hydrogen Internal Combustion Engine (H2-ICE) powered heavy-duty truck. This truck operates on hydrogen while maintaining a conventional diesel combustion engine architecture. With a 19 to 35 tons loading capacity, the H2-ICE truck enables a swift transition to cleaner energy at a relatively lower cost differential.

- According to the Automobile Inspection & Registration Information Association (AIRIA), as of March 31, FY 2022, Japan had approximately 7.11 thousand hydrogen fuel cell vehicles in use, representing an increase from 5.28 thousand in FY 2021. The majority of these hydrogen-fuel cell vehicles are hydrogen-fueled passenger cars.

- Hence, due to the abovementioned factors, the demand for liquid hydrogen in the Asia-Pacific region is expected to increase over the forecast period.

Liquid Hydrogen Industry Overview

The liquid hydrogen market is highly consolidated in nature. Some of the major companies in the market (not in any particular order) include Air Liquide, Air Products and Chemicals Inc., Linde PLC, Iwatani Corporation, and Messer Group GmbH.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand for Liquid Hydrogen for Space Exploration

- 4.1.2 Increasing Adoption of Hydrogen Fuel Cell in Commercial Vehicle

- 4.2 Restraints

- 4.2.1 High Cost Associated with Handling and Storage

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Distribution

- 5.1.1 Cryogenic Tank

- 5.1.2 High-Pressure Tube Trailers

- 5.2 End-user Industry

- 5.2.1 Automotive

- 5.2.2 Aerospace (including Outer Space)

- 5.2.3 Marine

- 5.2.4 Other End-User Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Air Liquide

- 6.4.2 Air Products and Chemicals, Inc.

- 6.4.3 Iwatani Corporation

- 6.4.4 Linde PLC

- 6.4.5 Messer Group GMBH

- 6.4.6 Nippon Sanso Holdings Corporation

- 6.4.7 Universal Industrial Gases Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Emphasis on Utilizing Hydrogen as a Marine Fuel

- 7.2 Increasing Innovations in Aerospace Industry

液氫市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測

液氫市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測 化學液氫市場規模、佔有率和成長分析:按純度、製造方法、儲存類型、應用、最終用戶和地區分類-2026-2033年產業預測

化學液氫市場規模、佔有率和成長分析:按純度、製造方法、儲存類型、應用、最終用戶和地區分類-2026-2033年產業預測 液氫市場規模、佔有率及成長分析(依生產方式、分銷方式、終端用戶產業及地區分類)-2026-2033年產業預測

液氫市場規模、佔有率及成長分析(依生產方式、分銷方式、終端用戶產業及地區分類)-2026-2033年產業預測 全球煤炭氣化液氫市場全球電解液氫市場化學液氫全球市場全球液氫市場化學液氫市場機會、成長動力、產業趨勢分析及2025-2034年預測

全球煤炭氣化液氫市場全球電解液氫市場化學液氫全球市場全球液氫市場化學液氫市場機會、成長動力、產業趨勢分析及2025-2034年預測 亞太液氫 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美液氫 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

亞太液氫 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美液氫 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)