|

市場調查報告書

商品編碼

2019213

2026 年至 2035 年醫藥玻璃包裝的市場機會、成長要素、產業趨勢分析與預測。Pharmaceutical Glass Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

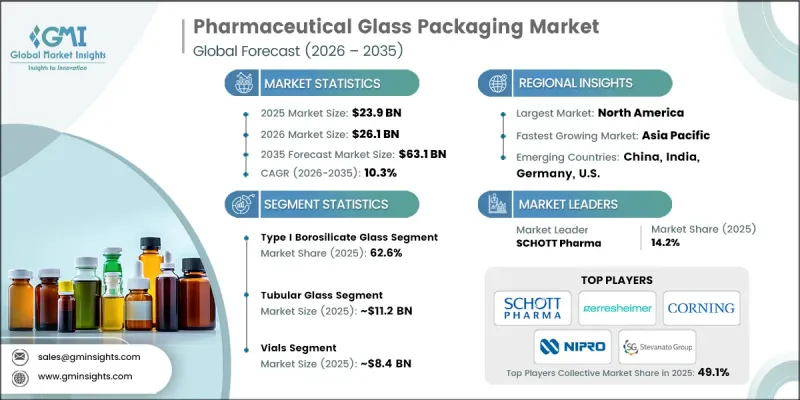

2025 年全球醫藥玻璃包裝市場價值 239 億美元,預計到 2035 年將達到 631 億美元,年複合成長率為 10.3%。

醫藥玻璃包裝市場的發展動力源於對高品質包裝日益成長的需求,以確保產品的完整性和穩定性。人口結構變化和慢性病負擔加重推動了藥品需求的成長,進而加速了產業的擴張。玻璃因其優異的耐化學性和長期維持藥物療效的能力,仍是首選材料。製造商正致力於開發兼具耐用性和高性能的先進包裝。玻璃材料的持續創新——更輕、更防碎、更永續性——正在提升安全標準並滿足監管要求。這些進展鞏固了玻璃包裝在醫藥供應鏈中的關鍵地位。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 239億美元 |

| 預測金額 | 631億美元 |

| 複合年成長率 | 10.3% |

醫藥玻璃包裝市場也受到嚴格的監管要求的影響,這些要求旨在確保藥品安全和防止污染。全球衛生監管機構正在實施全面的標準,要求包裝材料在各種條件下保持產品穩定性。這推動了對更高品質材料的轉向,特別是那些具有更優異的耐化學性和熱穩定性的材料。因此,製造商擴大採用先進的玻璃成分,以滿足合規標準並提高包裝的整體可靠性。

預計到2025年,I型硼矽酸玻璃將佔62.6%的市佔率。該細分市場發展勢頭強勁,這主要得益於其優異的耐化學腐蝕性能以及在寬廣溫度範圍內保持穩定性的能力。此外,對高靈敏度藥物製劑需求的不斷成長也進一步推動了該材料的應用。監管法規對高性能包裝材料的使用要求也促進了I型硼矽酸玻璃在整個行業的廣泛應用。

預計到2025年,管狀玻璃市場規模將達到112億美元。該細分市場以其精密性、耐用性和對先進製藥應用的適用性而廣受認可。其穩定的結構特性和優異的耐化學腐蝕性使其成為關鍵包裝需求的理想選擇。此外,與自動化生產系統的兼容性不斷增強也推動了其應用,使製造商即使在大規模生產中也能提高效率並維持產品品質。

至2025年,北美醫藥玻璃包裝市場將佔全球市場佔有率的35.3%。該地區高度重視品質標準、法規遵循和永續生產實踐。對先進醫藥包裝解決方案日益成長的需求推動了高純度玻璃材料和創新塗層技術的應用。對產品安全和污染預防的日益關注進一步促進了高性能玻璃包裝解決方案的使用。此外,政府推廣永續材料的措施也推動了全部區域向先進玻璃包裝的轉型。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 嚴格的藥品安全法規

- 老化與慢性疾病

- 全球對藥品的需求不斷成長

- 玻璃包裝技術的進步

- 偏好即用型軟體包

- 產業潛在風險與挑戰

- 損壞/損壞風險

- 玻璃包裝高成本

- 市場機遇

- 1. 採用永續和環保的玻璃包裝解決方案。

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 主要企業的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係和聯盟

- 技術進步

- 業務拓展與投資策略

- 數位轉型計劃

- 新興競爭對手和Start-Ups競爭對手的發展趨勢

第5章 市場估算與預測:依材料類型分類,2022-2035年

- I型硼硼矽酸玻璃

- II 型處理鈉鈣玻璃

- 第三型標準鈉鈣玻璃

第6章 市場估價與預測:依製造流程分類,2022-2035年

- 管狀玻璃

- 模壓玻璃

第7章 市場估算與預測:依產品類型分類,2022-2035年

- 管瓶

- 瓶子

- 安瓿

- 墨水匣和注射器

第8章 市場估計與預測:依給藥途徑分類,2022-2035年

- 注射藥物

- 口服藥物

- 眼藥水

- 外用藥物

- 其他

第9章 市場估價與預測:依最終用戶分類,2022-2035年

- 製藥公司

- 契約製造組織

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- 全球公司:

- Ardagh Group SA

- Bormioli Pharma SpA

- Corning Incorporated

- Gerresheimer AG

- Nipro Corporation

- Owens-Illinois, Inc.

- SCHOTT AG

- SGD Pharma(SGD SA)

- Stevanato Group SpA

- Stolzle Glass Group

- 本地公司:

- Beatson Clark Ltd.

- DWK Life Sciences/DWK Life Sciences GmbH

- Shandong Pharmaceutical Glass Co., Ltd.

- Local Players:

- Hindustan National Glass &Industries Ltd.

- Piramal Glass Limited

The Global Pharmaceutical Glass Packaging Market was valued at USD 23.9 billion in 2025 and is estimated to grow at a CAGR of 10.3% to reach USD 63.1 billion by 2035.

The pharmaceutical glass packaging market is being driven by the rising need for high-quality packaging that ensures product integrity and stability. Increasing demand for pharmaceutical products, supported by demographic shifts and a growing burden of long-term health conditions, is accelerating industry expansion. Glass remains a preferred material due to its superior chemical resistance and ability to maintain drug efficacy over time. Manufacturers are focusing on developing advanced packaging solutions that combine durability with improved performance. Continuous innovation in lightweight, break-resistant, and environmentally sustainable glass materials is enhancing safety standards while meeting regulatory expectations. These developments are strengthening the role of glass packaging as a critical component in pharmaceutical supply chains.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $23.9 Billion |

| Forecast Value | $63.1 Billion |

| CAGR | 10.3% |

The pharmaceutical glass packaging market is also influenced by strict regulatory requirements focused on ensuring drug safety and preventing contamination. Global health authorities are enforcing comprehensive standards that require packaging materials to maintain product stability under various conditions. This has encouraged a shift toward higher-grade materials, particularly those offering enhanced chemical resistance and thermal stability. As a result, manufacturers are increasingly adopting advanced glass compositions to meet compliance standards and improve overall packaging reliability.

In 2025, the Type I borosilicate glass segment held a 62.6% share. This segment is gaining strong traction due to its superior resistance to chemical interactions and its ability to maintain stability under varying temperature conditions. The growing demand for sensitive pharmaceutical formulations is further supporting the adoption of this material. Regulatory requirements emphasizing the use of high-performance packaging materials are also contributing to the increased utilization of Type I borosilicate glass across the industry.

The tubular glass segment reached USD 11.2 billion in 2025. This segment is widely recognized for its precision, durability, and compatibility with advanced pharmaceutical applications. Its consistent structural properties and high resistance to chemical reactions make it suitable for critical packaging needs. Additionally, its compatibility with automated production systems has increased its adoption, allowing manufacturers to achieve greater efficiency and maintain product quality across large-scale operations.

North America Pharmaceutical Glass Packaging Market accounted for 35.3% share in 2025. The region is characterized by a strong focus on quality standards, regulatory compliance, and sustainable manufacturing practices. Increasing demand for advanced pharmaceutical packaging solutions is encouraging the adoption of high-purity glass materials and innovative coating technologies. The growing emphasis on product safety and contamination prevention is further supporting the use of high-performance glass packaging solutions. Additionally, government initiatives promoting sustainable materials are reinforcing the shift toward advanced glass packaging across the region.

Key companies operating in the Global Pharmaceutical Glass Packaging Market include Ardagh Group S.A., Beatson Clark Ltd., Bormioli Pharma S.p.A., Corning Incorporated, DWK Life Sciences GmbH, Gerresheimer AG, Hindustan National Glass & Industries Ltd., Nipro Corporation, Owens Illinois, Inc., Piramal Glass Limited, Schott AG, SGD Pharma (SGD S.A.), Shandong Pharmaceutical Glass Co., Ltd., Stevanato Group S.p.A., and Stolzle Glass Group. Companies in the Global Pharmaceutical Glass Packaging Market are strengthening their market position through continuous innovation, strategic collaborations, and capacity expansion. They are investing in research and development to create advanced glass formulations with improved chemical resistance and durability. Partnerships with pharmaceutical manufacturers are enabling better alignment with evolving packaging requirements. Companies are also expanding production capabilities to meet rising global demand and ensure a consistent supply. Sustainability initiatives, including the development of lightweight and recyclable glass solutions, are becoming a key focus area.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Material type trends

- 2.2.2 Manufacturing process trends

- 2.2.3 Product type trends

- 2.2.4 Drug delivery route trends

- 2.2.5 End user trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent Regulations on Drug Safety

- 3.2.1.2 Aging Population and Chronic Disease

- 3.2.1.3 Rising Global Pharmaceutical Demand

- 3.2.1.4 Technological Advancement in Glass Packaging

- 3.2.1.5 Preference for Ready to Use Packaging

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Fragility and Breakage Risks

- 3.2.2.2 High Cost of Glass Packaging

- 3.2.3 Market opportunities

- 3.2.3. 1 Adoption of Sustainable and Eco-Friendly Glass Packaging Solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Billion & Million Units)

- 5.1 Key trends

- 5.2 Type I Borosilicate Glass

- 5.3 Type II Treated Soda Lime Glass

- 5.4 Type III Regular Soda Lime Glass

Chapter 6 Market Estimates and Forecast, By Manufacturing Process, 2022 - 2035 (USD Billion & Million Units)

- 6.1 Key trends

- 6.2 Tubular Glass

- 6.3 Molded Glass

Chapter 7 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion & Million Units)

- 7.1 Key trends

- 7.2 Vials

- 7.3 Bottles

- 7.4 Ampoules

- 7.5 Cartridges & Syringes

Chapter 8 Market Estimates and Forecast, By Drug Delivery Route, 2022 - 2035 (USD Billion & Million Units)

- 8.1 Key trends

- 8.2 Injectable Drugs

- 8.3 Oral Drugs

- 8.4 Ophthalmic Drugs

- 8.5 Topical Drugs

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Billion & Million Units)

- 9.1 Key trends

- 9.2 Pharmaceutical Companies

- 9.3 Contract Manufacturing Organizations

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion & Million Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players:

- 11.1.1 Ardagh Group S.A.

- 11.1.2 Bormioli Pharma S.p.A.

- 11.1.3 Corning Incorporated

- 11.1.4 Gerresheimer AG

- 11.1.5 Nipro Corporation

- 11.1.6 Owens-Illinois, Inc.

- 11.1.7 SCHOTT AG

- 11.1.8 SGD Pharma (SGD S.A.)

- 11.1.9 Stevanato Group S.p.A.

- 11.1.10 Stolzle Glass Group

- 11.2 Regional Players:

- 11.2.1 Beatson Clark Ltd.

- 11.2.2 DWK Life Sciences / DWK Life Sciences GmbH

- 11.2.3 Shandong Pharmaceutical Glass Co., Ltd.

- 11.3 Local Players:

- 11.3.1 Hindustan National Glass & Industries Ltd.

- 11.3.2 Piramal Glass Limited

安瓿和注射器市場:按產品類型、材料、最終用戶和地區分類

安瓿和注射器市場:按產品類型、材料、最終用戶和地區分類 醫藥玻璃包裝市場報告:按產品類型、藥品類型、應用和地區分類(2026-2034 年)

醫藥玻璃包裝市場報告:按產品類型、藥品類型、應用和地區分類(2026-2034 年) 醫藥玻璃包裝市場:按容器類型、玻璃類型、瓶蓋類型、最終用途和分銷管道分類-2026-2032年全球市場預測

醫藥玻璃包裝市場:按容器類型、玻璃類型、瓶蓋類型、最終用途和分銷管道分類-2026-2032年全球市場預測 2026-2034年全球醫藥玻璃包裝市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球醫藥玻璃包裝市場規模、佔有率、趨勢和成長分析報告 2026年全球醫藥玻璃器皿市場報告全球安瓿瓶和注射器市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

2026年全球醫藥玻璃器皿市場報告全球安瓿瓶和注射器市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 全球醫藥玻璃包裝市場:市場規模、佔有率和趨勢分析(按材料、產品、藥品和地區分類),細分市場預測(2026-2033 年)2026年全球低硼矽酸玻璃瓶市場報告

全球醫藥玻璃包裝市場:市場規模、佔有率和趨勢分析(按材料、產品、藥品和地區分類),細分市場預測(2026-2033 年)2026年全球低硼矽酸玻璃瓶市場報告 全球醫藥玻璃包裝市場-產業規模、佔有率、趨勢、機會及預測:依產品、藥品類型、地區及競爭格局分類,2021-2031年

全球醫藥玻璃包裝市場-產業規模、佔有率、趨勢、機會及預測:依產品、藥品類型、地區及競爭格局分類,2021-2031年 醫藥玻璃包裝市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

醫藥玻璃包裝市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)