|

市場調查報告書

商品編碼

2019159

超音波冷卻計市場機會、成長要素、產業趨勢分析及2026-2035年預測Ultrasonic Cooling Meters Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

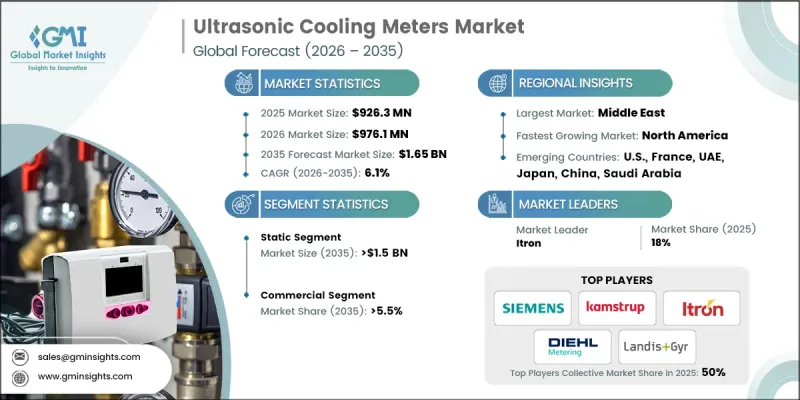

預計到 2025 年,全球超音波冷卻計市場價值將達到 9.263 億美元,年複合成長率為 6.1%,到 2035 年將達到 16.5 億美元。

市場擴張的驅動力來自商業、工業和住宅系統中對節能冷卻解決方案日益成長的需求。超音波冷卻計量器透過發射和接收聲波,精確測量水冷和液體冷卻系統的能耗,使操作人員能夠最佳化能耗並降低營運成本。隨著政府嚴格的能源效率法規和建築能源效率標準的推動,這些設備的應用日益普及,確保符合報告要求和能源效率標準。與智慧電錶平台整合,可實現即時監控和遠端數據訪問,從而支援物聯網建築管理系統。快速的都市化、數位化以及發展中地區區域供冷系統的普及也創造了巨大的成長機會。隨著企業和地方政府致力於減少碳足跡和提高永續性,超音波冷卻計量器正成為其能源管理策略的核心組成部分。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 9.263億美元 |

| 預測金額 | 16.5億美元 |

| 複合年成長率 | 6.1% |

預計到2035年,靜態超音波冷卻流量計市場規模將達到15億美元,這主要得益於其在流量和能耗測量方面的高精度,而流量和能耗測量對於區域供冷應用至關重要。高精度至關重要,因為即使是微小的誤差也會導致巨大的經濟損失和運作效率的降低。與機械式流量計相比,靜態流量計具有更高的可靠性和更長的使用壽命,能夠在較長時間內提供持續且準確的數據。這些優勢使其成為需要精確監測的大規模裝置的理想選擇,從而支撐了市場的強勁成長動能。

預計到2035年,商業領域的年複合成長率將達到5.5%。冷凍系統在商業建築的能源消耗中佔據很大比例,而超音波製冷計量器能夠提供精準的數據,從而最佳化暖通空調(HVAC)性能、減少能源浪費並降低營運成本。將其整合到能源審計中,有助於識別系統效率低下之處,並透過設備升級和調整來提升整體能源性能。整合到智慧建築平台後,透過實現自動化控制、數據驅動決策和持續性能監測,進一步提升了其價值,從而推動了這些計量器在商業基礎設施中的應用。

預計到2035年,美國超音波冷卻表市場規模將達到4.25億美元。這一區域成長主要得益於嚴格的能源效率法規以及建築規範的強制執行,這些規範要求在商業和住宅項目中進行精確測量。與智慧建築管理系統整合,使設施管理人員能夠即時監控能耗、最佳化系統性能並實現自動化控制。此外,物聯網技術的興起正在加速智慧電錶(包括超音波冷卻表)的普及,從而提高營運效率並節省能源。這種對能源最佳化和永續性的關注,持續推動著美國市場的強勁成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 產業生態系統

- 監理情勢

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 波特五力分析

- PESTEL 分析

- 成本結構分析

- 價格趨勢分析,2022-2035年

- 透過使用

- 按地區

- 新機會和趨勢

- 數位化和物聯網整合

- 投資分析及未來展望

第4章 競爭情勢

- 介紹

- 企業市佔率分析:按地區分類

- 北美洲

- 歐洲

- 亞太地區

- 中東

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場規模及預測:依技術分類,2022-2035年

- 機械的

- 靜止的

第6章 市場規模與預測:依應用領域分類,2022-2035年

- 住宅

- 商業的

- 學院和高等教育機構

- 辦公大樓

- 政府大樓

- 其他

- 工業的

第7章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 波蘭

- 瑞典

- 義大利

- 法國

- 芬蘭

- 奧地利

- 挪威

- 亞太地區

- 中國

- 日本

- 韓國

- 新加坡

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 阿曼

- 科威特

第8章:公司簡介

- Axioma Metering

- BMETERS Srl

- Diehl Stiftung & Co. KG

- Danfoss

- Engelmann Sensor GmbH

- Honeywell International Inc.

- Ista Energy Solutions

- Itron Inc.

- Kamstrup A/S

- Landis+Gyr

- QUNDIS GmbH

- Secure Meters Ltd.

- Schneider Electric

- Siemens AG

- Sontex SA

- Techem GmbH

- Wasion Group

- Zenner International GmbH & Co. KG

- Zelsius GmbH

- Diehl Metering

The Global Ultrasonic Cooling Meters Market was valued at USD 926.3 million in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 1.65 billion by 2035.

The market expansion is fueled by increasing demand for energy-efficient cooling solutions in commercial, industrial, and residential systems. Ultrasonic cooling meters provide precise measurement of energy usage in water- or liquid-based cooling systems by transmitting and receiving sound waves, enabling operators to optimize energy consumption and reduce operational costs. Governments' stringent energy efficiency regulations and building energy codes are driving adoption, as these devices ensure compliance with reporting and efficiency standards. Integration with smart metering platforms allows real-time monitoring and remote data access, supporting IoT-enabled building management systems. Rapid urbanization, digitalization, and the adoption of district cooling systems in developing regions are also creating significant growth opportunities. As organizations and municipalities aim to reduce carbon footprints and improve sustainability, ultrasonic cooling meters have become central to energy management strategies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $926.3 Million |

| Forecast Value | $1.65 Billion |

| CAGR | 6.1% |

The static ultrasonic cooling meters segment is expected to reach USD 1.5 billion by 2035, driven by their high accuracy in measuring flow and energy consumption, which is critical for district cooling applications. Precision is essential because even minor inaccuracies can lead to significant financial losses and operational inefficiencies. Static meters offer superior reliability and longer operational life compared to mechanical alternatives, providing consistent and accurate data over extended periods. These advantages make them ideal for large-scale installations requiring precise monitoring, supporting the market's robust growth trajectory.

The commercial segment is projected to grow at a 5.5% CAGR through 2035. Cooling systems constitute a major portion of energy expenditure in commercial buildings, and ultrasonic cooling meters provide precise data to optimize HVAC performance, reduce energy wastage, and lower operating costs. Their deployment in energy audits helps identify system inefficiencies, enabling equipment upgrades or adjustments to enhance overall energy performance. Integration into smart building platforms further amplifies their value by enabling automated control, data-driven decision-making, and continuous performance monitoring, strengthening the adoption of these meters across commercial infrastructure.

U.S. Ultrasonic Cooling Meters Market is expected to reach USD 425 million by 2035. Growth in the region is supported by strict energy efficiency regulations and the enforcement of building codes that mandate accurate metering in commercial and residential projects. Integration with smart building management systems allows facility managers to monitor energy consumption in real time, optimize system performance, and implement automated controls. Additionally, the rise of IoT technologies has accelerated the adoption of smart meters, including ultrasonic cooling meters, enhancing operational efficiency and energy savings. This focus on energy optimization and sustainability continues to drive robust market growth across the United States.

Prominent players in the Global Ultrasonic Cooling Meters Market include Kamstrup A/S, Itron Inc., Landis+Gyr, Schneider Electric, Axioma Metering, BMETERS Srl, Sontex SA, Zelsius GmbH, ZENNER International GmbH & Co. KG, Danfoss, Techem GmbH, Honeywell International Inc., Engelmann Sensor GmbH, Secure Meters Ltd., Diehl Stiftung & Co. KG, Ista Energy Solutions, Siemens AG, and QUNDIS GmbH. These companies focus on innovation, reliability, and digital integration to drive growth and maintain a competitive advantage. Companies operating in the Ultrasonic Cooling Meters Market are leveraging strategies such as technological innovation, strategic partnerships, and enhanced service offerings to solidify their market position. Key initiatives include developing advanced ultrasonic sensors with improved accuracy and reliability, integrating meters with smart building and IoT platforms, and offering turnkey solutions with installation, calibration, and maintenance support. Firms are also pursuing partnerships with HVAC contractors, utilities, and energy management companies to expand market reach. Emphasis on R&D for cost-effective, energy-efficient, and durable meters strengthens competitiveness, while geographic expansion and participation in sustainability programs enhance brand presence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & Confidence Scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates & calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Technology trends

- 2.4 Application trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis

- 3.8 Price trend analysis, 2022-2035

- 3.8.1 By Application

- 3.8.2 By Region

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.10 Investment analysis & future outlook

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans & funding

Chapter 5 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million & MW)

- 5.1 Key trends

- 5.2 Mechanical

- 5.3 Static

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & MW)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

- 6.3.1 College/University

- 6.3.2 Office Building

- 6.3.3 Government Building

- 6.3.4 Others

- 6.4 Industrial

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & MW)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 Poland

- 7.3.3 Sweden

- 7.3.4 Italy

- 7.3.5 France

- 7.3.6 Finland

- 7.3.7 Austria

- 7.3.8 Norway

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 South Korea

- 7.4.4 Singapore

- 7.5 Middle East

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Oman

- 7.5.5 Kuwait

Chapter 8 Company Profiles

- 8.1 Axioma Metering

- 8.2 BMETERS Srl

- 8.3 Diehl Stiftung & Co. KG

- 8.4 Danfoss

- 8.5 Engelmann Sensor GmbH

- 8.6 Honeywell International Inc.

- 8.7 Ista Energy Solutions

- 8.8 Itron Inc.

- 8.9 Kamstrup A/S

- 8.10 Landis+Gyr

- 8.11 QUNDIS GmbH

- 8.12 Secure Meters Ltd.

- 8.13 Schneider Electric

- 8.14 Siemens AG

- 8.15 Sontex SA

- 8.16 Techem GmbH

- 8.17 Wasion Group

- 8.18 Zenner International GmbH & Co. KG

- 8.19 Zelsius GmbH

- 8.20 Diehl Metering

慣性核融合市場預測至2034年-全球市場促進因素、燃料類型、雷射技術、設施類型、應用及區域分析可再生能源專案開發和EPC服務市場預測至2034年—按服務類型、能源來源、專案規模、最終用戶和地區分類的全球分析能源接取和微電網解決方案市場預測至2034年—按容量範圍、所有權和營運模式、技術、應用和區域分類的全球分析低碳寵物食品市場預測至2034年-全球分析(按產品類型、成分類型、寵物類型、生命階段、價格範圍、包裝類型、分銷管道、最終用戶和地區分類)節水型食品生產市場預測至2034年-按生產環境、作物類型、最終用戶和地區分類的全球分析

慣性核融合市場預測至2034年-全球市場促進因素、燃料類型、雷射技術、設施類型、應用及區域分析可再生能源專案開發和EPC服務市場預測至2034年—按服務類型、能源來源、專案規模、最終用戶和地區分類的全球分析能源接取和微電網解決方案市場預測至2034年—按容量範圍、所有權和營運模式、技術、應用和區域分類的全球分析低碳寵物食品市場預測至2034年-全球分析(按產品類型、成分類型、寵物類型、生命階段、價格範圍、包裝類型、分銷管道、最終用戶和地區分類)節水型食品生產市場預測至2034年-按生產環境、作物類型、最終用戶和地區分類的全球分析 2026-2030年全球清潔能源技術市場Power-to-X技術市場預測至2034年:按類型、組件、應用、最終用戶和地區分類的全球分析低碳化學品生產市場預測至2034年:按技術、應用和區域分類的全球分析

2026-2030年全球清潔能源技術市場Power-to-X技術市場預測至2034年:按類型、組件、應用、最終用戶和地區分類的全球分析低碳化學品生產市場預測至2034年:按技術、應用和區域分類的全球分析 商用冷卻計量市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)冷凍量表市場機會、成長要素、產業趨勢分析及2026-2035年預測

商用冷卻計量市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)冷凍量表市場機會、成長要素、產業趨勢分析及2026-2035年預測