|

市場調查報告書

商品編碼

2019156

環保食品包裝市場機會、成長要素、產業趨勢分析及2026-2035年預測Eco-friendly Food Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

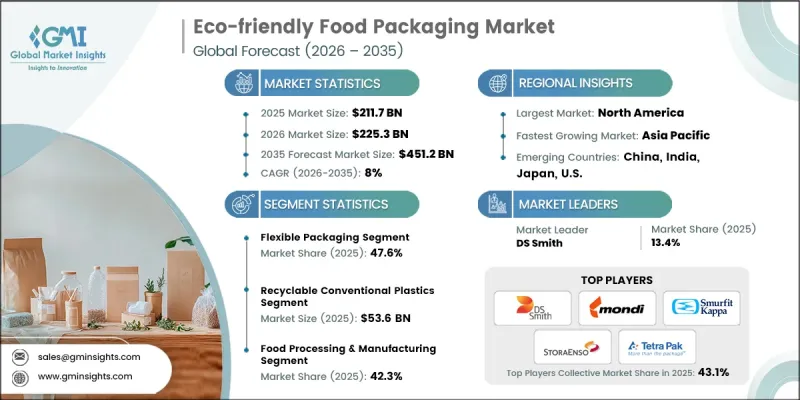

預計到 2025 年,全球環保食品包裝市場價值將達到 2,117 億美元,並預計以 8% 的複合年成長率成長,到 2035 年達到 4,512 億美元。

市場成長的驅動力來自於旨在減少塑膠廢棄物的法規結構的強化,以及食品飲料產業對永續包裝解決方案的日益普及。對環保替代品的需求不斷成長,加上食品配送服務的快速擴張,正在加速向可回收和可堆肥的材料轉變。生物基包裝技術的持續創新也有助於提升產品性能和永續性。製造商致力於在保持包裝效率和耐用性的同時,減少對環境的影響。隨著循環經濟實踐的日益重視,企業正在推廣可有效重複使用或回收的材料。此外,向永續消費模式的轉變正在推動對環保包裝的需求,使環保食品包裝成為全球供應鏈的關鍵關注領域。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 2117億美元 |

| 預測金額 | 4512億美元 |

| 複合年成長率 | 8% |

由於主要經濟體針對一次性塑膠製品推出了更嚴格的法規,環保意識強的食品包裝產業正展現出強勁的發展勢頭。監管機構正在執行更嚴格的合規標準,以最大限度地減少對環境的影響,迫使企業轉向永續的替代方案。同時,食品和飲料製造商正努力透過採用可回收和可堆肥材料來實現更高的永續性目標。隨著企業致力於取代傳統的塑膠包裝,向紡織品和紙質包裝解決方案的轉變正在加速。產業相關人員正日益將包裝策略與循環經濟原則相契合,並專注於材料的回收和再利用。這種轉變正在重塑產品開發和供應鏈策略,並刺激永續材料應用的創新。

預計到2025年,軟包裝市佔率將達到47.6%,主要得益於其輕量化結構、材料用量減少和成本效益。這種包裝形式有助於延長產品保存期限並最佳化物流,從而促進其在食品供應鏈中的廣泛應用。可回收單一材料結構和永續複合解決方案的不斷進步進一步提升了其吸引力。兼顧性能與環保因素的能力持續推動市場對軟包裝解決方案的強勁需求。

預計到2025年,可回收傳統塑膠市場規模將達536億美元。該市場之所以依然重要,是因為其兼具永續性和功能性。完善的回收基礎設施、成本優勢以及與現有生產系統的兼容性,都為其持續應用提供了支撐。此類材料能夠有效保護產品、延長保存期限,符合監管要求,並有助於循環經濟的發展。

受監管壓力和企業日益重視永續發展的推動,預計到2025年,北美環保食品包裝市場佔有率將達到46.2%。可回收、可堆肥和纖維基包裝形式在該地區食品相關產業中已廣泛應用。對先進材料和包裝技術的投資正在增強創新能力。食品零售、包裝商品和配送服務的需求不斷成長,推動了市場擴張,預計到2035年,該地區將在永續包裝的採用方面發揮主導作用。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 歐盟、印度和北美嚴格禁止使用一次性塑膠製品

- 制定目標,推出可回收和可堆肥包裝的快速消費品品牌。

- 電子商務驅動的食品配送正在推動可生物分解包裝材料的需求。

- 企業ESG措施正在加速包裝材料的轉型。

- 生物基聚合物的進步提高了阻隔性能

- 產業潛在風險與挑戰

- 新興國家缺乏工業堆肥基礎設施

- 水分和氧氣阻隔性能的限制

- 市場機遇

- 模塑纖維包裝在速食店的推廣

- 都市區食品配送可重複使用包裝系統的發展

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 市場集中度分析

- 主要企業的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與發展(R&D)

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係與合作

- 技術進步

- 業務拓展與投資策略

- 數位轉型計劃

- 新興/Start-Ups競爭對手的發展趨勢

第5章 市場估算與預測:依材料類型分類,2022-2035年

- 紙張和紙板

- 可再生傳統塑膠

- 再生塑膠

- 生物基和生物分解性塑膠

- 金屬

- 玻璃

- 其他

第6章 市場估價與預測:依包裝類型分類,2022-2035年

- 硬包裝

- 軟包裝

- 半剛性包裝

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 生鮮食品

- 乳製品

- 冷凍食品(包括冷凍甜點)

- 加工食品

- 飲料

- 醬汁、調味料和佐料

- 其他

第8章 市場估算與預測:依最終使用者分類,2022-2035年

- 食品加工/製造

- 餐廳經營者

- 零售及自有品牌包裝

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 主要企業

- Amcor

- DS Smith

- Mondi

- Smurfit Kappa

- Stora Enso

- Tetra Pak

- Huhtamaki

- Sonoco Products

- WestRock

- International Paper

- 按地區分類的主要企業

- 北美洲

- Genpak

- 亞太地區

- Biopak

- 歐洲

- Elopak

- Karl Knauer

- Nordic Paper

- 北美洲

- 小眾公司/顛覆者

- Biomass Packaging

- PacknWood

- 蘇帕克

- TIPA

- Vegware

The Global Eco-friendly Food Packaging Market was valued at USD 211.7 billion in 2025 and is estimated to grow at a CAGR of 8% to reach USD 451.2 billion by 2035.

Market growth is driven by stricter regulatory frameworks aimed at reducing plastic waste, along with the rising adoption of sustainable packaging solutions across the food and beverage sector. Increasing demand for environmentally responsible alternatives, combined with rapid expansion in food delivery services, is accelerating the transition toward recyclable and compostable materials. Continuous innovation in bio-based packaging technologies is also enhancing product performance and sustainability credentials. Manufacturers are focusing on reducing environmental impact while maintaining packaging efficiency and durability. The growing emphasis on circular economy practices is encouraging companies to adopt materials that can be reused or recycled efficiently. In addition, the shift toward sustainable consumption patterns is reinforcing demand for eco-conscious packaging formats, making eco-friendly food packaging a key focus area across global supply chains.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $211.7 Billion |

| Forecast Value | $451.2 Billion |

| CAGR | 8% |

The eco-friendly food packaging industry is experiencing strong momentum due to tightening regulations targeting single-use plastics across major economies. Regulatory bodies are enforcing stricter compliance standards to minimize environmental impact, prompting companies to transition toward sustainable alternatives. At the same time, food and beverage manufacturers are committing to higher sustainability targets by adopting recyclable and compostable materials. The shift toward fiber-based and paper-based packaging solutions is gaining traction as businesses aim to replace traditional plastic formats. Industry participants are increasingly aligning their packaging strategies with circular economy principles, focusing on material recovery and reuse. This transition is reshaping product development and supply chain strategies, encouraging innovation in sustainable material applications.

The flexible packaging segment accounted for 47.6% share in 2025 owing to its lightweight structure, reduced material usage, and cost efficiency. This packaging format supports improved product preservation and optimized logistics, contributing to its widespread adoption across the food supply chain. Ongoing advancements in recyclable mono-material structures and sustainable laminate solutions are further enhancing its appeal. The ability to balance performance with environmental considerations continues to drive strong demand for flexible packaging solutions.

The recyclable conventional plastics segment generated USD 53.6 billion in 2025. This segment remains prominent as it offers a practical balance between sustainability and functionality. Established recycling infrastructure, cost advantages, and compatibility with existing production systems support its continued use. Materials within this category provide effective product protection, extend shelf life, and comply with regulatory requirements while contributing to circular economy initiatives.

North America Eco-friendly Food Packaging Market held a 46.2% share in 2025, supported by regulatory pressure and increasing corporate focus on sustainability. The region is witnessing the broad adoption of recyclable, compostable, and fiber-based packaging formats across food-related industries. Investments in advanced materials and packaging technologies are strengthening innovation capabilities. Growing demand from food retail, packaged goods, and delivery services is sustaining market expansion, positioning the region as a leader in sustainable packaging adoption through 2035.

Key companies operating in the Global Eco-friendly Food Packaging Market include Amcor, Biomass Packaging, Biopak, DS Smith, Elopak, Genpak, Huhtamaki, International Paper, Karl Knauer, Mondi, Nordic Paper, PacknWood, Smurfit Kappa, Sonoco Products, Stora Enso, Sulapac, Tetra Pak, TIPA, Vegware, and WestRock. Companies in the Global Eco-friendly Food Packaging Market are strengthening their competitive position through innovation, strategic partnerships, and sustainability-driven initiatives. Many firms are investing in research and development to create advanced bio-based and recyclable materials that meet performance and regulatory standards. Businesses are forming collaborations across the value chain to enhance recycling infrastructure and support circular economy models. Expansion of product portfolios with sustainable alternatives is helping companies address evolving consumer preferences. In addition, organizations are leveraging digital technologies to improve supply chain transparency and operational efficiency. Companies are also focusing on sustainable sourcing, eco-friendly manufacturing processes, and compliance with global environmental regulations to reinforce brand positioning and long-term market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Material type trends

- 2.2.2 Packaging format trends

- 2.2.3 Application trends

- 2.2.4 End-user trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent single-use plastic bans across EU, India, North America

- 3.2.1.2 FMCG brands adopting recyclable and compostable packaging targets

- 3.2.1.3 E-commerce food delivery driving need for biodegradable packaging

- 3.2.1.4 Corporate ESG commitments accelerating packaging material transitions

- 3.2.1.5 Advancements in bio-based polymers improving barrier performance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited industrial composting infrastructure in emerging economies

- 3.2.2.2 Performance limitations in moisture and oxygen barrier properties

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of molded fiber packaging in quick-service restaurants

- 3.2.3.2 Growth in reusable packaging systems for urban food delivery

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Paper & paperboard

- 5.3 Recyclable conventional plastics

- 5.4 Recycled plastics

- 5.5 Bio-based & biodegradable plastics

- 5.6 Metal

- 5.7 Glass

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Packaging Format, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Rigid packaging

- 6.3 Flexible packaging

- 6.4 Semi-rigid packaging

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Fresh food

- 7.3 Dairy products

- 7.4 Frozen food (including frozen desserts)

- 7.5 Processed food

- 7.6 Beverages

- 7.7 Sauces, dressings & condiments

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Food processing & manufacturing

- 8.3 Foodservice operators

- 8.4 Retail & private label packaging

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Amcor

- 10.1.2 DS Smith

- 10.1.3 Mondi

- 10.1.4 Smurfit Kappa

- 10.1.5 Stora Enso

- 10.1.6 Tetra Pak

- 10.1.7 Huhtamaki

- 10.1.8 Sonoco Products

- 10.1.9 WestRock

- 10.1.10 International Paper

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Genpak

- 10.2.2 Asia Pacific

- 10.2.2.1 Biopak

- 10.2.3 Europe

- 10.2.3.1 Elopak

- 10.2.3.2 Karl Knauer

- 10.2.3.3 Nordic Paper

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Biomass Packaging

- 10.3.2 PacknWood

- 10.3.3 Sulapac

- 10.3.4 TIPA

- 10.3.5 Vegware

2034 年可生物分解和可堆肥包裝替代品市場預測-按材料、包裝形式、分解類型、應用、分銷管道和地區進行全球分析。環保黏合劑市場預測至2034年-全球分析(按類型、原料、技術、配方、性能、終端應用產業、通路和地區分類)

2034 年可生物分解和可堆肥包裝替代品市場預測-按材料、包裝形式、分解類型、應用、分銷管道和地區進行全球分析。環保黏合劑市場預測至2034年-全球分析(按類型、原料、技術、配方、性能、終端應用產業、通路和地區分類) 環保食品包裝市場規模(至 2035 年):依材料類型、包裝類型、產品類型、技術、策略細分、應用領域、最終用戶、公司、地區、產業趨勢和預測

環保食品包裝市場規模(至 2035 年):依材料類型、包裝類型、產品類型、技術、策略細分、應用領域、最終用戶、公司、地區、產業趨勢和預測 環保食品包裝市場分析及預測(至2035年):類型、產品類型、材料類型、應用、技術、最終用戶、組件、製程、實施方案、解決方案

環保食品包裝市場分析及預測(至2035年):類型、產品類型、材料類型、應用、技術、最終用戶、組件、製程、實施方案、解決方案 全球甘蔗容器市場規模、佔有率、趨勢和成長分析報告(2026-2034年)環保食品包裝市場規模、佔有率、成長及全球產業分析:按類型和應用分類,區域的洞察,2026-2034年預測

全球甘蔗容器市場規模、佔有率、趨勢和成長分析報告(2026-2034年)環保食品包裝市場規模、佔有率、成長及全球產業分析:按類型和應用分類,區域的洞察,2026-2034年預測 2026年全球環保食品包裝市場報告永續包裝和環保食品解決方案市場預測至2032年:按包裝材料、產品類型、技術、分銷管道、最終用戶和地區分類的全球分析環保包裝材料市場預測至2032年:按包裝類型、材料、形式、工藝、應用和地區分類的全球分析

2026年全球環保食品包裝市場報告永續包裝和環保食品解決方案市場預測至2032年:按包裝材料、產品類型、技術、分銷管道、最終用戶和地區分類的全球分析環保包裝材料市場預測至2032年:按包裝類型、材料、形式、工藝、應用和地區分類的全球分析 甘蔗餐具市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

甘蔗餐具市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)