|

市場調查報告書

商品編碼

2019039

造粒機市場機會、成長要素、產業趨勢分析及2026-2035年預測。Pelletizer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

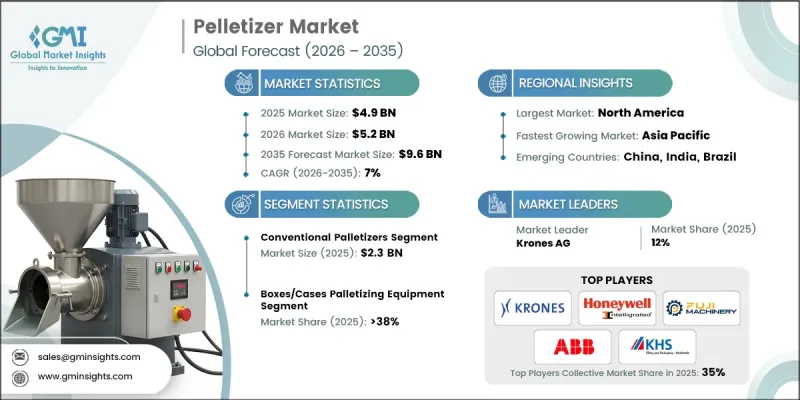

2025年全球造粒機市場價值49億美元,預計2035年將以7%的複合年成長率成長至96億美元。

企業正致力於提升營運效率和工作流程的穩定性,這推動了先進造粒系統的應用。曾經被視為生產設備輔助組件的系統,如今已成為管理日常營運和應對日益成長的產量的關鍵要素。由於供應鏈日益複雜,以及對營運效率的期望不斷提高,企業正在投資易於整合、易於使用且能適應各種生產環境的系統。此外,對職場安全和穩定產量的日益重視也影響著系統設計,製造商正在開發只需極少監控且能與現有設備無縫整合的解決方案。對能夠適應不同產品形式的靈活設備的需求不斷成長,進一步塑造了市場格局,企業正在尋求兼顧效率和適應性的技術。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 49億美元 |

| 預測金額 | 96億美元 |

| 複合年成長率 | 7% |

預計到2025年,傳統造粒機市場規模將達到23億美元,主要得益於其在高產量、重複性、標準化生產環境中的成本效益。這些系統非常適合穩定的生產條件,並具有可靠的加工能力和較長的運作。與現有生產佈局的兼容性進一步鞏固了其市場地位,尤其是在基礎設施升級面臨挑戰的工廠中。傳統系統的可靠性和耐用性持續推動其在成熟的工業環境中廣泛應用。

預計到2025年,紙箱和包裝盒市佔率將達到38%。該細分市場之所以能保持其主導地位,是因為標準化包裝形式在自動化生產和物流流程中得到了廣泛應用。其統一的結構使得自動化系統能夠有效率地處理並簡化操作。專為該細分市場設計的設備能夠與其他包裝流程有效整合,從而提高整體營運效率。對結構化包裝形式的持續依賴,鞏固了該細分市場在更廣泛的市場格局中的強勢地位。

美國造粒機市場佔84%的佔有率,預計2025年市場規模將達到13億美元。美國之所以能維持主導地位,主要得益於其製造業和物流業自動化程度高。勞動力短缺和安全標準的持續挑戰正在加速向自動化解決方案的轉型。強大的工業基礎設施和對先進技術的持續投資進一步推動了市場成長。成熟的自動化生態系統促進了創新,並支持造粒系統在各行業的廣泛應用。

目錄

第1章:調查方法

- 研究途徑

- 品質改進計劃

- GMI人工智慧政策和資料完整性計劃

- 資訊來源一致性協議

- GMI人工智慧政策和資料完整性計劃

- 調查軌跡和置信度評分

- 調查和路線的組成部分

- 評分組成部分

- 數據收集

- 主要來源部分列表

- 資料探勘資訊來源

- 付費資訊來源

- 區域資訊來源

- 付費資訊來源

- 基本估算和計算方法

- 每種方法中基準年的計算

- 預測模型

- 量化市場影響分析

- 生長參數對預測的數學影響

- 量化市場影響分析

- 關於調查透明度的補充信息

- 資訊來源歸屬框架

- 品質保證指標

- 對信任的承諾

第2章執行摘要

第3章業界考察

- 生態系分析

- 生態系測繪

- OEM

- 積分器

- 最終用戶

- 零件供應商

- 相關人員之間的相互依存關係

- 價值鏈分析(基於初步研究)

- 價值鏈的各個階段:製造、分銷、安裝、售後市場

- 依價值鏈階段進行利潤率分析

- 價值創造機制

- 生態系測繪

- 影響產業的因素

- 促進因素

- 製造業和倉儲業自動化應用日益普及

- 對電子商務和高速物料輸送。

- 人們對職場安全和人體工學的興趣日益濃厚

- 產業潛在風險與挑戰

- 高昂的初始投資和整合成本

- 對技術熟練的技工和維修人員的需求

- 機會

- 擴展機器人和協作式碼垛解決方案

- 人工智慧、視覺系統和智慧分析的整合

- 促進因素

- 成長潛力分析

- 在具有高成長潛力的地區,商業機會不容錯過。

- 高成長領域的機遇

- 新興應用領域

- 未來市場趨勢

- 科技與創新趨勢

- 新興科技的發展趨勢

- 按技術類型分類的創新藍圖

- 區域技術採納曲線

- 價格分析(基於初步調查)

- 過去價格趨勢分析(2022-2025)

- 以技術類型(機器人與傳統自動化)分類的價格波動

- 區域價格趨勢

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 貿易資料分析(基於一手調查)(HS編碼:8479)

- 進出口量及進口額趨勢

- 主要貿易走廊及關稅的影響

- 設備的跨境分銷模式

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有堆垛機業務模式

- 生成式人工智慧的應用案例與實施藍圖(預測性維護、路線最佳化)

- 風險、限制和監管考量

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 企業級基準測試(基於初步調查)

- 層級分類標準與選擇標準

- 撕裂定位矩陣

- BW Packaging相對於競爭對手的品牌定位

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 機器人堆垛機

- 關節型機器人(4軸/5軸/6軸)

- 龍門/傳送門機器人

- 協作機器人(cobots)

- 傳統堆垛機(非機器人型)

- 機械分層劑

- 線上常規系統

- 半自動堆垛機

- 手動碼堆垛機

第6章 市場估計與預測:依處理能力分類,2022-2035年

- 低速堆垛機(最大速度 10 箱/分鐘)

- 中速堆垛機(10-25箱/分鐘)

- 高速堆垛機(25-50箱/分鐘)

- 超高速堆垛機

第7章 市場估算與預測:依整合類型分類,2022-2035年

- 獨立式堆疊單元

- 整合線上系統

- 生產線末端托盤堆垛

- 多線碼垛

- 移動/靈活單元

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 袋裝托盤堆疊裝置

- 用於紙箱和紙盒的碼垛機

- 瓶罐托盤堆疊設備

- 用於桶裝和罐裝食品的碼垛設備

- 托盤堆疊裝置

- 混合物料輸送系統

- 其他

第9章 市場估計與預測:依最終用途產業分類,2022-2035年

- 食品/飲料

- 製藥

- 消費品

- 建材

- 化學品

- 其他

第10章 市場估價與預測:依通路分類,2022-2035年

- 直銷

- 間接銷售

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 其他拉丁美洲地區

- 中東和非洲(MEA)

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

- 其他中東和非洲地區

第12章:公司簡介

- ABB Group

- ARPAC LLC

- BEUMER Group GmbH &Co. KG

- Brenton Engineering(part of ProMach)

- Columbia Machine, Inc.

- Fanuc Corporation

- Fuji Machinery Co., Ltd.

- Gebo Cermex(part of Sidel Group)

- Honeywell Intelligrated

- Intralox, LLC(part of Laitram, LLC)

- KHS GmbH

- Krones AG

- Kuka AG

- Premier Tech Chronos

- Schneider Packaging Equipment Co., Inc.

The Global Pelletizer Market was valued at USD 4.9 billion in 2025 and is estimated to grow at a CAGR of 7% to reach USD 9.6 billion by 2035.

Businesses are focusing on streamlining operations and improving workflow consistency, which is driving the adoption of advanced pelletizing systems. What was once considered a supplementary addition to production facilities is now becoming a critical component in managing daily operations and handling increasing production volumes. Rising complexity in supply chains and higher expectations for operational efficiency are encouraging companies to invest in systems that are easy to integrate, user-friendly, and adaptable to different production environments. In addition, the growing emphasis on workplace safety and consistent output is influencing system design, with manufacturers developing solutions that require minimal supervision and fit seamlessly into existing setups. Increasing demand for flexible equipment capable of handling varied product formats is further shaping the market, as businesses seek technologies that balance efficiency with adaptability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.9 Billion |

| Forecast Value | $9.6 Billion |

| CAGR | 7% |

The conventional pelletizers segment generated USD 2.3 billion in 2025, supported by their ability to deliver cost efficiency in high-volume production environments where operations are repetitive and standardized. These systems are well-suited for consistent production conditions, offering reliable throughput and long operational lifespans. Their compatibility with established manufacturing layouts further strengthens their position, particularly in facilities where upgrading infrastructure may present challenges. The dependability and durability of conventional systems continue to support their widespread adoption across established industrial environments.

The boxes and cases segment accounted for 38% share in 2025. This segment remains dominant due to the widespread use of standardized packaging formats in automated production and logistics processes. Their uniform structure allows for efficient handling and streamlined operations within automated systems. Equipment designed for this segment integrates effectively with other packaging processes, enhancing overall operational efficiency. The continued reliance on structured packaging formats supports the segment's strong position within the broader market landscape.

United States Pelletizer Market held an 84% share, generating USD 1.3 billion in 2025. The country maintains its leadership due to a high level of automation adoption across the manufacturing and logistics sectors. Ongoing challenges related to labor availability and safety standards are accelerating the shift toward automated solutions. Strong industrial infrastructure and continued investment in advanced technologies are further reinforcing market growth. The presence of established automation ecosystems supports innovation and widespread implementation of pelletizing systems across various industries.

Key companies operating in the Global Pelletizer Market include ABB Group, Krones AG, Fanuc Corporation, Kuka AG, BEUMER Group GmbH & Co. KG, Columbia Machine, Inc., Premier Tech Chronos, Schneider Packaging Equipment Co., Inc., Honeywell Intelligrated, ARPAC LLC, Gebo Cermex (part of Sidel Group), Brenton Engineering (part of ProMach), Fuji Machinery Co., Ltd., Intralox, LLC (part of Laitram, LLC), and KHS GmbH. Companies in the Global Pelletizer Market are strengthening their competitive position through technological innovation and strategic expansion initiatives. They are investing in advanced automation technologies to improve system efficiency, flexibility, and ease of integration. Expanding product portfolios to address diverse industry requirements is a key focus area. Businesses are also forming strategic partnerships and collaborations to enhance market reach and improve service capabilities. In addition, companies are emphasizing user-friendly designs and customizable solutions to meet evolving customer demands. Strengthening after-sales support and maintenance services is another important strategy to build long-term customer relationships.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Key Trends

- 2.2.1 Region

- 2.2.2 Product type

- 2.2.3 Handling capacity

- 2.2.4 Integration type

- 2.2.5 Application

- 2.2.6 End use industry

- 2.2.7 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Ecosystem mapping

- 3.1.1.1 OEM

- 3.1.1.2 Integrators

- 3.1.1.3 End-users

- 3.1.1.4 Component suppliers

- 3.1.2 Stakeholder interdependence

- 3.1.3 Value chain analysis (Driven by Primary Research)

- 3.1.3.1 Value chain stages: manufacturing, distribution, installation, aftermarket

- 3.1.3.2 Profit margin analysis by value chain stage

- 3.1.3.3 Value capture mechanisms

- 3.1.1 Ecosystem mapping

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising automation adoption across manufacturing and warehousing

- 3.2.1.2 Growing e-commerce and need for high-speed material handling

- 3.2.1.3 Increasing focus on workplace safety and ergonomics

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment and integration costs

- 3.2.2.2 Need for skilled technicians and maintenance personnel

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of robotic and collaborative palletizing solutions

- 3.2.3.2 Integration of ai, vision systems, and smart analytics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.3.1 High-growth regional opportunities

- 3.3.2 High-growth segment opportunities

- 3.3.3 Emerging application verticals

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Emerging technology trends

- 3.5.2 Innovation roadmap by technology type

- 3.5.3 Technology adoption curves by region

- 3.6 Pricing analysis (driven by primary research)

- 3.6.1 Historical price trend analysis (2022-2025)

- 3.6.2 Price variation by technology type (Robotic vs Conventional Automated)

- 3.6.3 Regional pricing dynamics

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade data analysis (driven by primary research) (HS Code: 8479)

- 3.8.1 Import/Export volume and value trends

- 3.8.2 Key trade corridors and tariff impact

- 3.8.3 Cross-border equipment flow patterns

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 AI-driven disruption of existing palletizer business models

- 3.9.2 GenAI use cases and adoption roadmaps (predictive maintenance, route optimization)

- 3.9.3 Risks, limitations and regulatory considerations

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East and Africa

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Company tier benchmarking (Driven by Primary Research)

- 4.5.1 Tier classification criteria and qualifying thresholds

- 4.5.2 Tier positioning matrix

- 4.5.3 Brands positioning of BW Packaging against Competitors

- 4.6 Competitive positioning matrix

- 4.7 Key developments

- 4.7.1 Mergers & acquisitions

- 4.7.2 Partnerships & collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Robotic palletizers

- 5.2.1 Articulated arm robots (4/5/6-axis)

- 5.2.2 Gantry/portal robots

- 5.2.3 Collaborative robots (cobots)

- 5.3 Conventional palletizers (non-robotic)

- 5.3.1 Mechanical layer formers

- 5.3.2 In-line conventional systems

- 5.4 Semi-Automated palletizers

- 5.5 Manual palletizers

Chapter 6 Market Estimates & Forecast, By Handling Capacity, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Low-speed palletizers (up to 10 cases/min)

- 6.3 Medium-speed palletizers (10-25 cases/min)

- 6.4 High-speed palletizers (25-50 cases/min)

- 6.5 Ultra-high-speed palletizers

Chapter 7 Market Estimates & Forecast, By Integration Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Standalone palletizing cells

- 7.3 Integrated in-line systems

- 7.4 End-of-line palletizing

- 7.5 Multi-line palletizing

- 7.6 Mobile/flexible units

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Bags palletizing equipment

- 8.3 Boxes/cases palletizing equipment

- 8.4 Bottles/containers palletizing equipment

- 8.5 Drums/kegs palletizing equipment

- 8.6 Trays palletizing equipment

- 8.7 Mixed material handling systems

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By End Use Industry, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Food & beverage

- 9.3 Pharmaceuticals

- 9.4 Consumer goods

- 9.5 Building materials

- 9.6 Chemicals

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct Sales

- 10.3 Indirect Sales

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Rest of Latin America

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

- 11.6.4 Rest of MEA

Chapter 12 Company Profiles

- 12.1 ABB Group

- 12.2 ARPAC LLC

- 12.3 BEUMER Group GmbH & Co. KG

- 12.4 Brenton Engineering (part of ProMach)

- 12.5 Columbia Machine, Inc.

- 12.6 Fanuc Corporation

- 12.7 Fuji Machinery Co., Ltd.

- 12.8 Gebo Cermex (part of Sidel Group)

- 12.9 Honeywell Intelligrated

- 12.10 Intralox, LLC (part of Laitram, LLC)

- 12.11 KHS GmbH

- 12.12 Krones AG

- 12.13 Kuka AG

- 12.14 Premier Tech Chronos

- 12.15 Schneider Packaging Equipment Co., Inc.

先進封裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

先進封裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球先進封裝技術市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球先進封裝技術市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 先進封裝市場規模、佔有率、趨勢及預測(按類型、最終用途及地區分類),2026-2034年

先進封裝市場規模、佔有率、趨勢及預測(按類型、最終用途及地區分類),2026-2034年 2026年全球先進封裝技術市場報告

2026年全球先進封裝技術市場報告 先進封裝市場規模、佔有率和成長分析(按類型、最終用途和地區分類):產業預測(2026-2033 年)

先進封裝市場規模、佔有率和成長分析(按類型、最終用途和地區分類):產業預測(2026-2033 年) 先進封裝市場:依封裝類型、應用、終端用戶產業及地區分類

先進封裝市場:依封裝類型、應用、終端用戶產業及地區分類 GMIPulse - 包裝市場情報訂閱

GMIPulse - 包裝市場情報訂閱 先進封裝技術市場預測(至2032年):按封裝技術、互連方法、材料類型、裝置架構、最終用戶和地區進行的全球分析

先進封裝技術市場預測(至2032年):按封裝技術、互連方法、材料類型、裝置架構、最終用戶和地區進行的全球分析 美國飲料包裝設備市場:市場規模、佔有率、趨勢分析(按類型、自動化程度和應用)、細分市場預測(2025-2033)下一代封裝市場:按封裝類型、應用和地區分類

美國飲料包裝設備市場:市場規模、佔有率、趨勢分析(按類型、自動化程度和應用)、細分市場預測(2025-2033)下一代封裝市場:按封裝類型、應用和地區分類