|

市場調查報告書

商品編碼

1939018

先進封裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Advanced Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

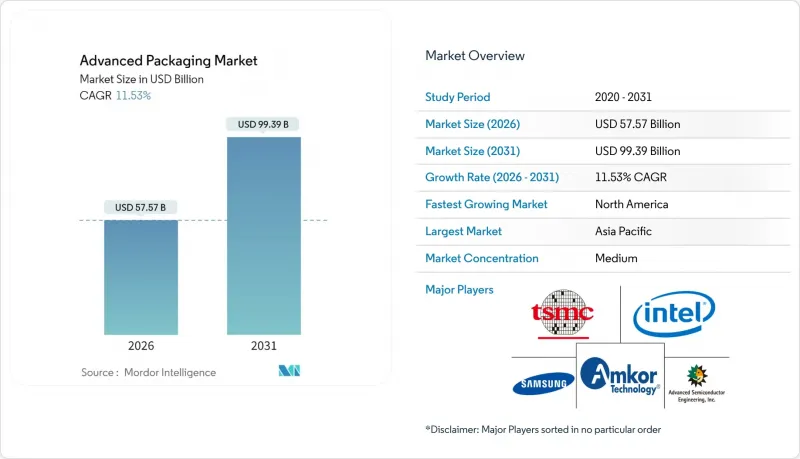

預計先進封裝市場將從 2025 年的 516.2 億美元成長到 2026 年的 575.7 億美元,到 2031 年將達到 993.9 億美元,2026 年至 2031 年的複合年成長率為 11.53%。

由於異質整合對於人工智慧 (AI) 處理器至關重要,而傳統封裝的散熱和互連能力又無法滿足需求,因此市場需求超出了最初的預期。為因應這項需求,整合裝置製造商 (IDM) 和外包半導體組裝測試 (OSAT) 服務商加快了資本投資,各國政府也推出了大規模激勵措施,以促進組裝能的本土化。先進封裝市場也受惠於玻璃芯基板的研發、面板級加工的試點部署以及超大規模資料中心對光共封裝技術的快速應用。然而,由於 BT 樹脂基板短缺和工程人才匱乏,產能擴張無法及時進行,導致供應仍然緊張。隨著晶圓代工廠將封裝業務內部化以確保對 AI 供應鏈的端到端控制,競爭日益激烈,傳統 OSAT 服務商的利潤空間受到擠壓,並促使其進行策略性專業化轉型。

全球先進封裝市場趨勢與洞察

人工智慧和高效能運算對異質整合的需求日益成長

人工智慧工作負載對運算密度和記憶體頻寬的要求遠超傳統封裝技術。台積電的CoWoS平台將晶片組和高頻寬記憶體整合於單一結構中,正迅速被主流人工智慧加速器廠商所採用。三星的SAINT技術採用混合鍵結技術實現下一代HBM4堆疊,也達到了類似的目標,凸顯了自主研發先進封裝技術的戰略價值。熱感界面材料、專用基板和主動中介層的引入,使得封裝成本佔半導體製造材料總成本的15%至20%(相較之下,主流CPU的封裝成本僅佔5%至8%)。因此,先進封裝產能與尖端晶圓廠同等重要,共同決定人工智慧系統的上市時間。由此可見,先進封裝市場的發展與前端製程的轉型同步進行,而非落後於其後。

消費性電子設備的微型化推動了WLP技術的普及。

智慧型手機、穿戴式裝置和耳機等裝置對超薄設計和功能密度提出了更高的要求。扇出型晶圓級封裝 (FOWLP) 能夠將多個晶粒整合到厚度小於 0.5 毫米的超薄封裝中,從而在不犧牲散熱性能的前提下支援旗艦級移動處理器。從扇入型晶圓級封裝 (WLP) 過渡到 FOWLP 可省去底部填充、焊線和層壓基板等工序,從而降低高達 25% 的系統總成本。小型化趨勢也延伸到了植入式醫療電子產品領域,尺寸在這個領域至關重要。無引線封裝製造商利用 WLP 技術將元件尺寸縮小了 93%,同時滿足了嚴格的可靠性要求。因此,消費和醫療領域的需求構成了永續的基礎,保護了先進封裝市場免受個人電腦終端市場週期性波動的影響。

高資本密集度限制了市場進入。

2.5D 和 3D 製程的設備成本將達到每腔室 1,000 萬至 1,500 萬美元,遠高於傳統生產線通常的 300 萬美元。台積電已為 2025 年的資本支出預算了 420 億美元,其中很大一部分將用於先進封裝的擴張。這使得規模較小的 OSAT(外包半導體組裝和測試)廠商難以在產品生命週期快速縮短的情況下攤銷投資,迫使它們專注於細分領域並進行防禦性併購。預計如此高的門檻將擴大頂級公司與區域追隨者之間的技術差距,從而在 2024 年至 2026 年期間限制先進封裝市場的新增資本支出。

細分市場分析

受消費性電子和工業應用的大批量需求驅動,覆晶封裝將在2025年繼續保持領先地位,佔據48.30%的市場佔有率。然而,2.5D/3D封裝將實現最快成長,預計複合年成長率將達到13.05%,因為人工智慧加速器需要邏輯和記憶體接近性,而這超出了覆晶的限制。預計到2031年,2.5D/3D解決方案的先進封裝市場規模將達到389億美元,佔平台總收入的39.15%。

三星的SAINT平台實現了10μm以下的混合鍵合,與焊線相比,訊號延遲降低了30%,熱裕度提高了40%。台積電的CoWoS在2025年新增了三條生產線,消除了12個月的訂單。嵌入式晶粒和扇出型WLP封裝發展成為互補的選擇:嵌入式封裝滿足了空間受限的汽車產業的需求,而扇出型WLP封裝則應用於5G基地台和毫米波雷達設計。這些趨勢共同推動了2.5D/3D封裝在下一代裝置發展藍圖中佔據核心地位,鞏固了其作為先進封裝市場關鍵價值促進因素的地位。

2025年,家用電子電器將佔總出貨量的39.20%,但其成長率將趨於個位數。相較之下,汽車和電動車的需求預計將以12.32%的複合年成長率成長,到2031年,其在先進封裝市場的佔有率將提升至18.6%。預計到預測期結束時,汽車電子先進封裝的市場規模將超過185億美元。

目前,電動車牽引逆變器、車載充電器和網域控制器均採用車規級扇出型雙面冷卻功率模組和射出成型的系統級封裝(SiP) 組件。資料中心基礎設施是另一個高成長領域。人工智慧伺服器採用先進封裝技術,可實現接近 1000 W/cm² 的功率密度,這需要開發創新的熱感蓋和底部填充材料。同時,醫療產業需要生物相容性塗層和密封外殼,這導致平均售價更高,且替換需求穩定。這些細分領域的趨勢共同促成了收入來源的多元化,並降低了先進封裝市場對智慧型手機更新周期的依賴。

先進封裝市場按封裝平台(覆晶、嵌入式晶粒、扇入式晶圓級封裝等)、終端用戶產業(家用電子電器、汽車/電動車、資料中心/高效能運算等)、裝置架構(2D IC、2.5D 中介層、3D IC)、南美洲互通技術(焊料凸塊、銅柱、混合鍵結)及歐洲地區(北美、非洲、亞焊球、銅柱、混合鍵結)及歐洲地區(北美、非洲、亞焊球、銅柱、混合鍵結)及歐洲地區(北美、非洲、歐洲地區)。

區域分析

到2025年,亞太地區將佔總營收的74.10%,位置位於台灣、韓國和中國當地的大多數前端晶圓廠和基板供應商。台積電宣佈在美國投資1,650億美元,這反映了其多元化戰略,而非取代台灣基地,旨在確保亞洲在中期內保持主導地位。中國本土的OSAT(外包組裝和測試)企業實現了兩位數的銷售成長,並拓展至汽車封裝領域,但對極紫外線(EUV)設備的嚴格監管限制了它們獲得尖端晶圓製造流程的機會。

北美地區以12.38%的複合年成長率成為成長最快的地區,這主要得益於《晶片封裝和整合法案》(CHIPS Act)的激勵措施。安姆科(Amcor)位於亞利桑那州、投資20億美元的工廠將於2027年全面運作,屆時將整合凸塊級、晶圓級和麵板級生產線,成為美國系統整合商附近首個大型外包中心。英特爾、蘋果和英偉達已預訂了部分產能,以降低地緣政治供應鏈中斷的風險,並將先前流向東亞OSAT(外包組裝和測試)公司的大量生產轉移至北美。因此,先進封裝市場如今擁有了可靠的北美供應鏈,能夠支援大量人工智慧產品的生產。

歐洲選擇走專業化路線,而非以大規模生產主導。安森美半導體位於捷克的工廠專注於生產用於汽車電源的碳化矽元件,其生產與當地原始設備製造商(OEM)的電氣化目標相契合。德國弗勞恩霍夫研究所主導了面板級技術的研究,但製造商對投資新建大型工廠仍持謹慎態度。同時,新加坡加強了其樞紐功能。美光半導體的HBM工廠和科磊的製程控制擴建項目,在同一司法管轄區內建構了一個垂直整合的生態系統,支援人工智慧記憶體和計量技術的發展。印度推出了50%的資本成本分攤制度,並吸引了先進封裝領域的試點計畫提案,預計該領域在中期內將實現成長,但人才招募仍然是一項挑戰。

這些措施共同拓展了系統OEM廠商的地理分佈,並重新平衡了先進封裝市場。儘管如此,亞太地區預計到2031年仍將維持60%以上的市場佔有率,因為其現有的基礎設施、供應鏈叢集和規模經濟優勢將繼續優於新進入者。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 宏觀經濟因素的影響

- 市場促進因素

- 人工智慧和高效能運算對異質整合的需求日益成長

- 消費性電子設備的微型化推動了WLP技術的普及。

- 政府對半導體產業的補貼(例如,《晶片法案》、《歐盟晶片法案》)

- 電動汽車電力電子裝置的可靠性要求(先進封裝)

- 新型玻璃芯基板實現面板級封裝

- 超大規模資料中心對共封閉式光元件的需求

- 市場限制

- 先進包裝生產線的高資本密集度

- 產業重組降低了外包利潤率

- BT樹脂基板產能不足

- 高技能組裝工程師短缺

- 價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭強度

- 投資分析

第5章 市場規模與成長預測

- 透過包裝平台

- 覆晶

- 內建晶粒

- 扇入式 WLP

- 扇出 WLP

- 2.5D/3D

- 按最終用戶行業分類

- 家用電子電器

- 汽車和電動車

- 資料中心和高效能運算

- 工業和物聯網

- 醫學/醫療技術

- 依設備架構

- 2D IC

- 2.5D 中介層

- 3D IC(TSV/混合鍵結)

- 透過互連技術

- 焊料凸塊

- 銅柱

- 混合鍵

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 荷蘭

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 台灣

- 韓國

- 日本

- 新加坡

- 馬來西亞

- 印度

- 亞太其他地區

- 中東和非洲

- 中東

- 以色列

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Amkor Technology, Inc.

- Taiwan Semiconductor Manufacturing Company Limited

- Advanced Semiconductor Engineering, Inc.

- JCET Group Co., Ltd.

- Samsung Electronics Co., Ltd.

- Intel Corporation

- Chipbond Technology Corporation

- ChipMOS Technologies Inc.

- Powertech Technology Inc.

- TongFu Microelectronics Co., Ltd.

- Nepes Corporation

- STATS ChipPAC Pte. Ltd.

- Siliconware Precision Industries Co., Ltd.

- UTAC Holdings Ltd.

- Walton Advanced Engineering, Inc.

- Xintec Inc.

- Tianshui Huatian Technology Co., Ltd.

- King Yuan Electronics Co., Ltd.

- Signetics Corporation

- GlobalFoundries Inc.

- Semiconductor Manufacturing International Corporation

- SFA Semicon Co., Ltd.

- Nantong Fujitsu Microelectronics Co., Ltd.

- Hana Micron Inc.

- Unisem(M)Berhad

第7章 市場機會與未來展望

The advanced packaging market is expected to grow from USD 51.62 billion in 2025 to USD 57.57 billion in 2026 and is forecast to reach USD 99.39 billion by 2031 at 11.53% CAGR over 2026-2031.

Demand outpaced earlier projections because heterogeneous integration became indispensable for artificial-intelligence (AI) processors that exceed the thermal and interconnect limits of conventional packages. In response, integrated-device manufacturers (IDMs) and outsourced semiconductor assembly and test (OSAT) providers accelerated capital spending, while governments earmarked large incentives to localize assembly capacity. The advanced packaging market also benefited from glass-core substrate R&D, panel-level processing pilots, and the rapid adoption of co-packaged optics in hyperscale data centers. Supply remained tight, however, as BT-resin substrate shortages and scarce engineering talent hindered timely capacity additions. Competitive intensity rose as foundries internalized packaging to secure end-to-end control of AI supply chains, squeezing traditional OSAT margins and prompting strategic specialization.

Global Advanced Packaging Market Trends and Insights

Rising demand for heterogeneous integration for AI and HPC

AI workloads require compute density and memory bandwidth unattainable with legacy packaging. TSMC's CoWoS platform integrates chiplets and high-bandwidth memory in a single structure, gaining rapid adoption among leading AI accelerator vendors. Samsung's SAINT technology achieved similar objectives using hybrid bonding that supports forthcoming HBM4 stacks, underscoring the strategic value of in-house advanced packaging. Thermal interface materials, specialized substrates, and active interposers raised package cost to 15-20% of the total semiconductor build-to-materials, up from 5-8% for mainstream CPUs. As a result, advanced packaging capacity became as critical as leading-edge fabs in determining time-to-market for AI systems. The advanced packaging market, therefore, grew in tandem with, rather than lagging, front-end process migrations.

Miniaturization of consumer devices boosting WLP adoption

Smartphones, wearables, and hearables consistently demand thinner profiles and higher functional density. Fan-out wafer-level packaging (FOWLP) enables multiple dies to be embedded in ultra-thin packages below 0.5 mm, supporting flagship mobile processors without compromising thermal performance. The shift from fan-in WLP to FOWLP reduced overall system cost by up to 25% because under-fill, wire-bonding, and laminate substrates were eliminated. Miniaturization also moved into implantable medical electronics, where dimensions are life-critical; leadless pacemakers benefited from WLP to cut device size by 93% while meeting stringent reliability targets. Consequently, consumer and medical demand created a recurring baseline that insulated the advanced packaging market from cyclical swings in PC end-markets.

High capital intensity constraining market entry

Tooling for 2.5D and 3D processes can cost USD 10-15 million per chamber, vastly exceeding the USD 3 million typical for legacy lines. TSMC budgeted USD 42 billion in 2025 capital outlays, of which a material share targeted advanced packaging expansions. Smaller OSATs, therefore, struggled to amortize investments across rapidly shrinking product life cycles, prompting niche specialization or defensive mergers. The elevated hurdle rate widened the technological gap between tier-one providers and regional followers, dampening fresh capacity in the advanced packaging market during 2024-2026.

Other drivers and restraints analyzed in the detailed report include:

- Government semiconductor subsidies accelerating infrastructure development

- EV power-electronics reliability transforming packaging requirements

- BT-resin substrate bottlenecks limiting production capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flip-chip packages retained leadership with 48.30% revenue in 2025, anchored by high-volume consumer and industrial applications. Yet 2.5D/3D configurations delivered the fastest gains, achieving a 13.05% CAGR outlook as AI accelerators demanded logic-to-memory proximity beyond flip-chip limits. The advanced packaging market size for 2.5D/3D solutions is forecast to reach USD 38.9 billion by 2031, equal to 39.15% of total platform revenue.

Samsung's SAINT platform attained sub-10 µm hybrid bonds, reducing signal latency by 30% and extending thermal headroom by 40% relative to wire-bonded stacks. TSMC's CoWoS ramped three additional lines in 2025 to clear a 12-month backlog. Embedded-die and fan-out WLP progressed as complementary options: embedded packages suited space-constrained automotive domains, while fan-out WLP captured 5G base-station and mmWave radar designs. Collectively, these dynamics embedded 2.5D/3D packaging at the center of next-generation device roadmaps, guaranteeing its role as the prime value driver inside the advanced packaging market.

Consumer electronics absorbed 39.20% of 2025 shipments, but its growth plateaued at single digits. In contrast, automotive and EV demand is projected to expand at a 12.32% CAGR, lifting its share of the advanced packaging market to 18.6% by 2031. The advanced packaging market size for automotive electronics is estimated to surpass USD 18.5 billion by the end of the forecast period.

EV traction inverters, on-board chargers, and domain controllers now specify automotive-grade fan-out, double-side cooled power modules, and over-molded system-in-package (SiP) assemblies. Data-center infrastructure provided another high-growth niche: AI servers utilize advanced packages with power densities reaching 1,000 W/cm2, dictating innovative thermal lid and under-fill chemistries. Healthcare, meanwhile, requires biocompatible coatings and hermetic enclosures, attributes that carry premium average selling prices and stable replacement demand. Cumulatively, these segment trends diversified revenue streams and reduced dependence on cyclical smartphone refresh cycles within the advanced packaging market.

Advanced Packaging Market is Segmented by Packaging Platform (Flip-Chip, Embedded Die, Fan-In WLP, and More), End-User Industry (Consumer Electronics, Automotive and EV, Data Center and HPC, and More), Device Architecture (2D IC, 2. 5D Interposer, and 3D IC), Interconnect Technology (Solder Bump, Copper Pillar, and Hybrid Bond), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Geography Analysis

Asia-Pacific generated 74.10% of 2025 revenue because Taiwan, South Korea, and mainland China house the bulk of front-end fabs and substrate suppliers. TSMC announced a USD 165 billion U.S. investment, reflecting a diversification strategy rather than the displacement of its Taiwan base, ensuring Asia retains leadership in the medium term. China's domestic OSATs delivered double-digit sales gains and expanded into automotive packaging, but tight controls on extreme-ultraviolet (EUV) tools limited their move into leading-edge wafer-fab processes.

North America emerged as the fastest-growing region at a 12.38% CAGR thanks to the CHIPS Act incentives. Amkor's USD 2 billion Arizona site will combine bump, wafer-level, and panel-level lines once fully ramped in 2027, providing the first large-scale outsourced option near U.S. system integrators. Intel, Apple, and NVIDIA pre-booked a portion of this capacity to de-risk geopolitical supply interruptions, redirecting meaningful volumes that historically flowed to East Asian OSATs. Consequently, the advanced packaging market now includes a credible North American supply node capable of high-volume AI product support.

Europe pursued specialization rather than volume leadership. onsemi's Czech facility addressed silicon-carbide devices for automotive power, aligning with local OEM electrification targets. Germany's Fraunhofer institutes led panel-level research, but manufacturers stayed cautious on green-field megasite commitments. Meanwhile, Singapore strengthened its hub role; Micron's HBM plant and KLA's process-control expansion created a vertically coherent ecosystem that supports AI memory and metrology under one jurisdiction. India introduced a 50% capital cost-sharing scheme, attracting proposals for advanced packaging pilots that promise medium-term upside yet remain contingent on talent availability.

Collectively, these developments diversified geographic risk for system OEMs and rebalanced the advanced packaging market. Even so, Asia-Pacific is forecast to maintain more than 60% share in 2031 because existing infrastructure, supply clusters, and economies of scale still surpass new regional entrants.

- Amkor Technology, Inc.

- Taiwan Semiconductor Manufacturing Company Limited

- Advanced Semiconductor Engineering, Inc.

- JCET Group Co., Ltd.

- Samsung Electronics Co., Ltd.

- Intel Corporation

- Chipbond Technology Corporation

- ChipMOS Technologies Inc.

- Powertech Technology Inc.

- TongFu Microelectronics Co., Ltd.

- Nepes Corporation

- STATS ChipPAC Pte. Ltd.

- Siliconware Precision Industries Co., Ltd.

- UTAC Holdings Ltd.

- Walton Advanced Engineering, Inc.

- Xintec Inc.

- Tianshui Huatian Technology Co., Ltd.

- King Yuan Electronics Co., Ltd.

- Signetics Corporation

- GlobalFoundries Inc.

- Semiconductor Manufacturing International Corporation

- SFA Semicon Co., Ltd.

- Nantong Fujitsu Microelectronics Co., Ltd.

- Hana Micron Inc.

- Unisem (M) Berhad

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors

- 4.3 Market Drivers

- 4.3.1 Rising demand for heterogeneous integration for AI and HPC

- 4.3.2 Miniaturization of consumer devices boosting WLP adoption

- 4.3.3 Government semiconductor subsidies (e.g., CHIPS, EU Chips Act)

- 4.3.4 EV power-electronics reliability needs (advanced power packages)

- 4.3.5 Emerging glass-core substrates enabling panel-level packaging

- 4.3.6 Co-packaged optics demand in hyperscale datacenters

- 4.4 Market Restraints

- 4.4.1 High capital intensity of advanced packaging lines

- 4.4.2 Industry consolidation squeezing outsourced margins

- 4.4.3 BT-resin substrate capacity bottlenecks

- 4.4.4 Shortage of advanced assembly talent

- 4.5 Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Rivalry

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Packaging Platform

- 5.1.1 Flip-Chip

- 5.1.2 Embedded Die

- 5.1.3 Fan-in WLP

- 5.1.4 Fan-out WLP

- 5.1.5 2.5D / 3D

- 5.2 By End-User Industry

- 5.2.1 Consumer Electronics

- 5.2.2 Automotive and EV

- 5.2.3 Data Center and HPC

- 5.2.4 Industrial and IoT

- 5.2.5 Healthcare / Med-tech

- 5.3 By Device Architecture

- 5.3.1 2D IC

- 5.3.2 2.5D Interposer

- 5.3.3 3D IC (TSV / Hybrid-Bond)

- 5.4 By Interconnect Technology

- 5.4.1 Solder Bump

- 5.4.2 Copper Pillar

- 5.4.3 Hybrid Bond

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Netherlands

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Taiwan

- 5.5.4.3 South Korea

- 5.5.4.4 Japan

- 5.5.4.5 Singapore

- 5.5.4.6 Malaysia

- 5.5.4.7 India

- 5.5.4.8 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Israel

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Saudi Arabia

- 5.5.5.1.4 Turkey

- 5.5.5.1.5 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amkor Technology, Inc.

- 6.4.2 Taiwan Semiconductor Manufacturing Company Limited

- 6.4.3 Advanced Semiconductor Engineering, Inc.

- 6.4.4 JCET Group Co., Ltd.

- 6.4.5 Samsung Electronics Co., Ltd.

- 6.4.6 Intel Corporation

- 6.4.7 Chipbond Technology Corporation

- 6.4.8 ChipMOS Technologies Inc.

- 6.4.9 Powertech Technology Inc.

- 6.4.10 TongFu Microelectronics Co., Ltd.

- 6.4.11 Nepes Corporation

- 6.4.12 STATS ChipPAC Pte. Ltd.

- 6.4.13 Siliconware Precision Industries Co., Ltd.

- 6.4.14 UTAC Holdings Ltd.

- 6.4.15 Walton Advanced Engineering, Inc.

- 6.4.16 Xintec Inc.

- 6.4.17 Tianshui Huatian Technology Co., Ltd.

- 6.4.18 King Yuan Electronics Co., Ltd.

- 6.4.19 Signetics Corporation

- 6.4.20 GlobalFoundries Inc.

- 6.4.21 Semiconductor Manufacturing International Corporation

- 6.4.22 SFA Semicon Co., Ltd.

- 6.4.23 Nantong Fujitsu Microelectronics Co., Ltd.

- 6.4.24 Hana Micron Inc.

- 6.4.25 Unisem (M) Berhad

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

先進半導體封裝市場-2026-2032年全球市場預測

先進半導體封裝市場-2026-2032年全球市場預測 全球先進半導體封裝市場:按技術、產品、應用和最終用戶分類-市場規模、產業動態、機會分析和預測(2026-2035 年)

全球先進半導體封裝市場:按技術、產品、應用和最終用戶分類-市場規模、產業動態、機會分析和預測(2026-2035 年) GPU晶片封裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)

GPU晶片封裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年) 2026-2034年全球食品飲料先進包裝市場規模、佔有率、趨勢和成長分析報告全球先進半導體封裝市場(2027-2037 年)

2026-2034年全球食品飲料先進包裝市場規模、佔有率、趨勢和成長分析報告全球先進半導體封裝市場(2027-2037 年) 半導體先進封裝市場預測至2034年-按封裝類型、材料、應用、最終用戶和地區分類的全球分析

半導體先進封裝市場預測至2034年-按封裝類型、材料、應用、最終用戶和地區分類的全球分析 從 2026 年到 2035 年,採用玻璃基板的先進封裝市場的商業機會、成長要素、產業趨勢分析和預測。

從 2026 年到 2035 年,採用玻璃基板的先進封裝市場的商業機會、成長要素、產業趨勢分析和預測。 2026-2030年全球先進半導體封裝市場先進封裝市場:規模、佔有率和成長率;全球產業分析;按類型、應用和地區分類;未來預測(2026-2034 年)晶片封裝及測試技術市場:依封裝技術、測試類型、最終用戶、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

2026-2030年全球先進半導體封裝市場先進封裝市場:規模、佔有率和成長率;全球產業分析;按類型、應用和地區分類;未來預測(2026-2034 年)晶片封裝及測試技術市場:依封裝技術、測試類型、最終用戶、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測