|

市場調查報告書

商品編碼

1998804

可折疊瓦楞紙包裝市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。Folding Carton Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

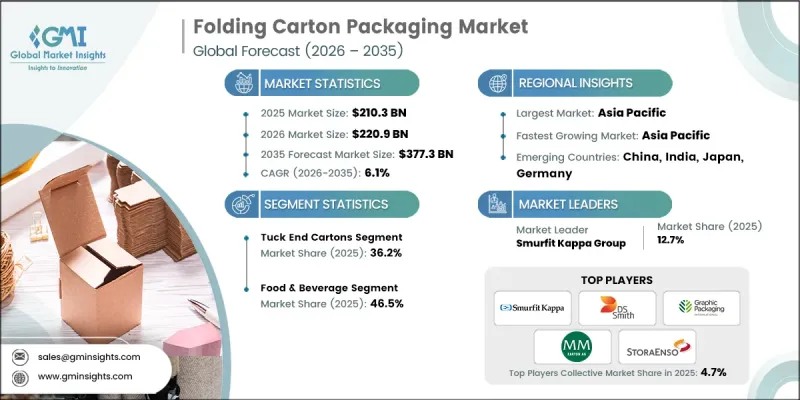

預計到 2025 年,全球可折疊瓦楞紙包裝市場價值將達到 2,103 億美元,年複合成長率為 6.1%,到 2035 年將達到 3,773 億美元。

可折疊瓦楞紙包裝市場的成長主要得益於全球對永續包裝材料的轉型以及可回收纖維基解決方案的日益普及。許多地區政府和監管機構正在實施更嚴格的包裝法規,旨在減少環境影響並促進循環經濟實踐。這些政策正在加速從硬質塑膠包裝到紙板基替代品的轉變,後者兼顧了可回收性和減少環境影響。此外,電子商務和現代零售分銷管道的快速發展也增加了對既能保護產品又能保持強大品牌識別度的二次包裝形式的需求。製藥、醫療保健、化妝品和個人護理等行業也越來越依賴高品質的可折疊紙盒來滿足包裝安全要求和監管標準。同時,品牌越來越重視能夠提升產品吸引力並強化品牌形象的高階包裝設計。這些不斷變化的需求,加上紙盒製造和印刷流程的持續技術進步,將繼續支撐全球可折疊紙盒包裝市場的長期成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 2103億美元 |

| 預測金額 | 3773億美元 |

| 複合年成長率 | 6.1% |

可折疊瓦楞紙包裝市場也受到強烈的監管趨勢的影響,這些趨勢鼓勵企業採用可回收纖維性包裝解決方案。各國政府和環保組織正在實施更嚴格的廢棄物管理政策和永續性目標,要求製造商減少包裝廢棄物並提高可回收性。因此,許多行業正在轉向輕質紙板箱,這種包裝既具有環境效益,又能提高材料利用率。這種方法使企業能夠在最佳化包裝結構的同時降低整體材料消耗。原物料成本的上漲和對碳足跡報告日益成長的關注進一步促使企業提高包裝效率並減少對環境的影響。

預計2026年至2035年間,展示型紙盒市場將以8.6%的複合年成長率成長,反映出現代零售環境的強勁需求。這類包裝形式因其簡化了零售店內商品的搬運和展示流程而日益普及。展示型紙盒能夠將產品運輸和貨架展示整合於單一包裝結構中,從而提高零售商的營運效率並減少補貨所需的工作量。零售商和消費品製造商越來越傾向於選擇兼具物流效率和卓越視覺效果的包裝形式。隨著有組織零售業的持續擴張和消費者在零售環境中競爭的加劇,對展示型紙盒包裝解決方案的需求預計將穩定成長。

預計到2025年,塗佈再生紙板(CRB)的市場規模將達到699億美元。由於其成本效益高且再生纖維含量高,這種材料持續廣泛應用,使其成為尋求環保包裝解決方案的企業的理想選擇。 CRB在各種包裝應用中都能提供可靠的結構性能,特別適用於那些對外觀要求不高的場合。日益成長的監管壓力促使包裝產品中再生材料的比例不斷提高,從而推動了CRB在各行各業的廣泛應用。那些希望在控制成本的同時提升永續性績效的企業往往會優先考慮再生紙板材料,這也鞏固了CRB在可折疊瓦楞紙包裝市場的主導地位。

到2025年,北美可折疊紙盒包裝市佔率將達到29.1%。由於嚴格的環境法規以及各消費品行業對可回收包裝材料需求的不斷成長,該地區的紙盒包裝行業持續擴張。在北美營運的公司擴大採用紙板包裝解決方案來取代傳統的塑膠包裝。此外,零售商也敦促供應商根據其永續發展計劃,轉向使用可回收包裝。該地區對先進製造技術的投資也在增加,旨在提高瓦楞紙板的加工效率,並支持更高水準的產品客製化。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 推動制定纖維基可回收包裝材料的相關法規

- 電子商務對二次包裝的需求不斷成長。

- 從塑膠翻蓋式容器過渡到紙盒

- 藥品序列化和合規性要求

- 化妝品和個人護理用品包裝盒的優質化

- 產業潛在風險與挑戰

- 原生紙漿和紙板價格波動

- 先進模切設備的高昂資本投資成本

- 市場機遇

- 使用阻隔塗層的可再生板

- 將智慧包裝與QR碼和NFC功能整合

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

- 貿易數據分析(基於付費資料庫)

- 進出口量及進口額趨勢

- 主要貿易走廊及關稅的影響

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 市場集中度分析

- 主要企業的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與發展(R&D)

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係與合作

- 技術進步

- 業務拓展與投資策略

- 數位轉型計劃

- 新興/Start-Ups競爭對手的發展趨勢

第5章 市場估價與預測:依紙箱結構分類,2022-2035年

- 折疊式紙箱

- 自動鎖扣/底部易碎紙箱

- 套筒紙箱

- 鎖底紙箱

- 適用於展示的紙箱

- 其他折疊結構

第6章 市場估算與預測:紙板等級分類,2022-2035年

- 固態漂白硫酸漿(SBS)

- 未漂白工藝外套 (CUK)

- 塗佈再生紙板(CRB)

- 無塗布紙板

第7章 市場估價與預測:依印刷技術分類,2022-2035年

- 膠印光刻

- 柔版印刷

- 數位印刷

- 凹版印刷

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 食品/飲料

- 個人護理和化妝品

- 製藥和醫療保健

- 家用物品/消費品

- 菸草

- 其他

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 主要企業

- DS Smith Plc

- Graphic Packaging International

- Huhtamaki Oyj

- Mayr-Melnhof Karton AG

- Oji Holdings Corporation

- Rengo Co., Ltd.

- Smurfit Kappa Group

- Stora Enso Oyj

- 按地區分類的主要企業

- 北美洲

- All Packaging Company

- American Carton Company

- Diamond Packaging

- Georgia-Pacific LLC

- Green Bay Packaging Inc.

- Meyers

- Seaboard Folding Box Company Inc.

- Wynalda Packaging

- 亞太地區

- Plastech Group Ltd.

- 歐洲

- Schur Pack Germany GmbH

- 北美洲

- 特殊玩家/干擾者

- August Faller GmbH & Co. KG

The Global Folding Carton Packaging Market was valued at USD 210.3 billion in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 377.3 billion by 2035.

Growth in the folding carton packaging market is largely driven by the global transition toward sustainable packaging materials and the increasing adoption of recyclable fiber-based solutions. Governments and regulatory authorities across many regions are introducing stricter packaging regulations aimed at reducing environmental impact and encouraging circular economy practices. These policies are accelerating the shift away from rigid plastic packaging toward paperboard-based alternatives that offer recyclability and lower environmental footprints. In addition, the rapid growth of e-commerce and modern retail distribution channels has created a stronger demand for secondary packaging formats that protect products while maintaining strong branding visibility. Industries such as pharmaceuticals, healthcare, cosmetics, and personal care are also increasing their reliance on high-quality folding cartons to meet packaging safety requirements and regulatory standards. At the same time, brands are placing greater emphasis on premium packaging designs that enhance product appeal and strengthen brand identity. These evolving requirements, combined with continuous technological improvements in carton manufacturing and printing processes, continue to support long-term expansion of the global folding carton packaging market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $210.3 Billion |

| Forecast Value | $377.3 Billion |

| CAGR | 6.1% |

The folding carton packaging market is also influenced by strong regulatory momentum encouraging companies to adopt recyclable fiber-based packaging solutions. Governments and environmental organizations are implementing stricter waste management policies and sustainability targets that require manufacturers to reduce packaging waste and improve recyclability. As a result, many industries are shifting toward lightweight paperboard cartons that offer both environmental benefits and efficient material utilization. This approach allows companies to optimize packaging structures while lowering overall material consumption. Rising costs of raw materials and increased focus on carbon footprint reporting are further motivating organizations to improve packaging efficiency and reduce environmental impact.

The display-ready cartons segment is projected to grow at a CAGR of 8.6% during 2026-2035, reflecting strong demand across modern retail environments. These packaging formats are gaining popularity because they simplify product handling and merchandising processes within retail stores. Display-ready cartons allow products to be transported and presented on retail shelves using a single packaging structure, which improves operational efficiency for retailers and reduces labor requirements during product stocking. Retailers and consumer goods companies increasingly prefer packaging formats that combine logistical efficiency with strong visual presentation. As organized retail continues to expand and consumer competition intensifies across store environments, the demand for display-ready carton packaging solutions is expected to increase steadily.

The coated recycled paperboard (CRB) segment reached USD 69.9 billion in 2025. This material remains widely used due to its cost efficiency and high recycled fiber content, making it an attractive option for companies seeking environmentally responsible packaging solutions. CRB offers reliable structural performance for various packaging applications where a premium visual appearance is not a primary requirement. Increasing regulatory pressure to incorporate higher levels of recycled materials into packaging products has strengthened the adoption of CRB across multiple industries. Companies aiming to enhance their sustainability performance while maintaining cost control often prioritize recycled paperboard materials, which continues to support the leading position of this segment within the folding carton packaging market.

North America Folding Carton Packaging Market accounted for 29.1% share in 2025. The industry in this region continues to expand due to strict environmental regulations and growing demand for recyclable packaging materials across several consumer industries. Businesses operating in North America are increasingly adopting paperboard-based packaging solutions as alternatives to conventional plastic packaging. In addition, retailers are encouraging suppliers to transition toward recyclable packaging formats that align with sustainability commitments. The region has also seen increasing investment in advanced manufacturing technologies designed to improve carton converting efficiency and support higher levels of product customization.

Key companies operating in the Global Folding Carton Packaging Market include Graphic Packaging International, DS Smith Plc, Smurfit Kappa Group, Stora Enso Oyj, Mayr-Melnhof Karton AG, Huhtamaki Oyj, Georgia-Pacific LLC, Oji Holdings Corporation, Rengo Co., Ltd., Green Bay Packaging Inc., American Carton Company, Diamond Packaging, Meyers, Schur Pack Germany GmbH, August Faller GmbH & Co. KG, Seaboard Folding Box Company Inc., Wynalda Packaging, All Packaging Company, and Plastech Group Ltd. Companies active in the Global Folding Carton Packaging Market are implementing several strategic initiatives to strengthen their competitive position and expand their market presence. Many organizations are investing in advanced converting technologies and automated production lines to improve manufacturing efficiency and reduce operational costs. Expanding sustainable packaging portfolios has become a major priority, with companies developing recyclable and lightweight paperboard materials that align with environmental regulations. Strategic partnerships with consumer goods brands and retail companies allow packaging manufacturers to create customized solutions that meet evolving product packaging requirements. Businesses are also increasing investments in digital printing and design technologies to offer flexible packaging customization and faster product launches.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Carton structure trends

- 2.2.2 Paperboard grade trends

- 2.2.3 Printing technology trends

- 2.2.4 Application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Regulatory push toward fiber-based recyclable packaging

- 3.2.1.2 Growth of e-commerce secondary packaging demand

- 3.2.1.3 Shift from plastic clamshells to paperboard cartons

- 3.2.1.4 Pharmaceutical serialization and compliance requirements

- 3.2.1.5 Premiumization in cosmetics and personal care cartons

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatility in virgin pulp and paperboard prices

- 3.2.2.2 High capital costs for advanced die-cutting equipment

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of barrier-coated recyclable paperboard

- 3.2.3.2 Smart packaging integration with QR/NFC features

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Trade Data Analysis (Based on Paid Databases)

- 3.13.1 Import/Export Volume & Value Trends

- 3.13.2 Key Trade Corridors & Tariff Impact

- 3.14 Impact of AI & Generative AI on the Market

- 3.14.1 AI-Driven Disruption of Existing Business Models

- 3.14.2 GenAI Use Cases & Adoption Roadmap by Segment

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Carton Structure, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Tuck end cartons

- 5.3 Auto-lock / crash bottom cartons

- 5.4 Sleeve cartons

- 5.5 Lock-bottom cartons

- 5.6 Display-ready cartons

- 5.7 Other folding structures

Chapter 6 Market Estimates and Forecast, By Paperboard Grade, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Solid bleached sulfate (SBS)

- 6.3 Coated unbleached kraft (CUK)

- 6.4 Coated recycled paperboard (CRB)

- 6.5 Uncoated paperboard

Chapter 7 Market Estimates and Forecast, By Printing Technology, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Offset lithography

- 7.3 Flexographic printing

- 7.4 Digital printing

- 7.5 Gravure

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Food & beverage

- 8.3 Personal care & cosmetics

- 8.4 Pharmaceuticals & healthcare

- 8.5 Household & consumer goods

- 8.6 Tobacco

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 DS Smith Plc

- 10.1.2 Graphic Packaging International

- 10.1.3 Huhtamaki Oyj

- 10.1.4 Mayr-Melnhof Karton AG

- 10.1.5 Oji Holdings Corporation

- 10.1.6 Rengo Co., Ltd.

- 10.1.7 Smurfit Kappa Group

- 10.1.8 Stora Enso Oyj

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 All Packaging Company

- 10.2.1.2 American Carton Company

- 10.2.1.3 Diamond Packaging

- 10.2.1.4 Georgia-Pacific LLC

- 10.2.1.5 Green Bay Packaging Inc.

- 10.2.1.6 Meyers

- 10.2.1.7 Seaboard Folding Box Company Inc.

- 10.2.1.8 Wynalda Packaging

- 10.2.2 Asia Pacific

- 10.2.2.1 Plastech Group Ltd.

- 10.2.3 Europe

- 10.2.3.1 Schur Pack Germany GmbH

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 August Faller GmbH & Co. KG

2025-2029年全球摺疊瓦楞紙包裝市場

2025-2029年全球摺疊瓦楞紙包裝市場 折疊瓦楞紙包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

折疊瓦楞紙包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 折疊瓦楞紙箱市場規模、佔有率及成長分析(按材料類型、訂單類型、最終用途產業和地區分類)-2026-2033年產業預測

折疊瓦楞紙箱市場規模、佔有率及成長分析(按材料類型、訂單類型、最終用途產業和地區分類)-2026-2033年產業預測 折疊式紙盒市場:未來預測(2025-2030)

折疊式紙盒市場:未來預測(2025-2030) 全球折疊紙盒市場未來展望(至2030年)

全球折疊紙盒市場未來展望(至2030年) 折疊式紙盒包裝市場規模、佔有率、趨勢分析報告:按最終用途、地區和細分市場預測,2025-2030 年印尼紙包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

折疊式紙盒包裝市場規模、佔有率、趨勢分析報告:按最終用途、地區和細分市場預測,2025-2030 年印尼紙包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年) 折疊式紙盒市場 - 成長、未來展望、競爭分析,2025 年至 2033 年泰國折疊式紙盒包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)全球折疊紙盒包裝市場規模:按材料類型、按產品類型、按最終用戶、按地區、範圍和預測

折疊式紙盒市場 - 成長、未來展望、競爭分析,2025 年至 2033 年泰國折疊式紙盒包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)全球折疊紙盒包裝市場規模:按材料類型、按產品類型、按最終用戶、按地區、範圍和預測