|

市場調查報告書

商品編碼

1998789

2026 年至 2035 年海洋來源蛋白質的市場機會、成長要素、產業趨勢與預測。Marine Derived Proteins Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

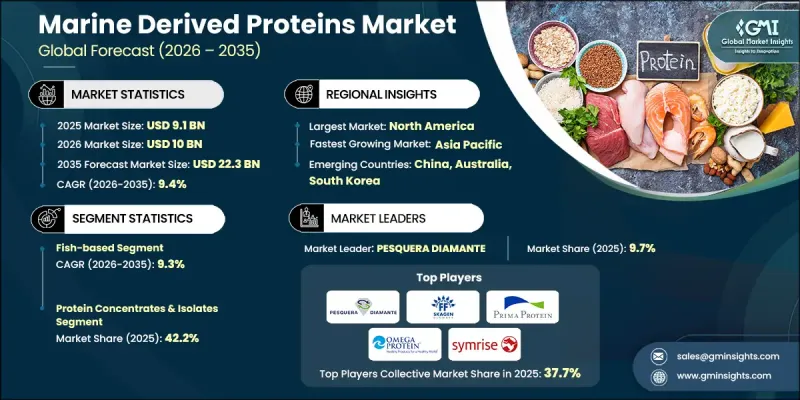

預計到 2025 年,全球海洋蛋白市場規模將達到 91 億美元,並有望以 9.4% 的複合年成長率成長,到 2035 年達到 223 億美元。

市場成長主要受消費者對海洋蛋白營養價值認知度不斷提高的推動。這些蛋白質富含必需胺基酸、ω脂肪酸和生物活性化合物,有助於維持整體健康,因此廣受認可。消費者對永續和負責任的營養來源日益關注,進一步增強了市場需求,他們正在尋找環保蛋白質替代品來取代傳統的蛋白質來源。海洋蛋白在膳食補充劑、機能性食品和營養保健品領域備受關注,推動了該行業的穩定擴張。此外,動物飼料和水產飼料領域對經濟高效且營養豐富的原料的需求不斷成長,也促進了海洋蛋白的普及。加工技術的進步使製造商能夠在保持永續性標準的同時提高產品品質。人們對健康、健身和運動表現導向營養的日益關注也推動了海洋蛋白消費量的成長。隨著全球對永續食品體系的認知不斷提高,預計海洋蛋白市場將迎來顯著的長期成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 91億美元 |

| 預測金額 | 223億美元 |

| 複合年成長率 | 9.4% |

預計到2025年,魚蛋白市佔率將達到67.8%,並在2035年之前以9.3%的複合年成長率成長。其市場主導地位得益於高蛋白濃度、完善的提取基礎設施和穩定的原料供應。由於其公認的營養價值,這些蛋白質仍然是膳食補充劑和機能性食品配方中不可或缺的一部分。負責任的採購和資源管理實踐的不斷改進進一步增強了穩定的供應和市場信心。

預計到2025年,濃縮蛋白和分離蛋白將佔據42.2%的市場。其主導地位歸功於其高純度和在運動營養、膳食補充劑和機能性食品等領域的廣泛應用。消費者對潔淨標示、易消化蛋白質來源的需求不斷成長,正在加速該細分市場的成長。同時,蛋白質水解物和生物活性胜肽因其優異的吸收特性和針對性的營養益處,正迅速獲得市場認可,尤其是在運動營養和臨床營養領域。

預計2026年至2035年,北美海洋蛋白市場將以9.3%的複合年成長率成長。該地區市場擴張的驅動力在於機能性食品、膳食補充劑和個人保健產品中對永續、潔淨標示成分的需求不斷成長。該地區的消費者越來越傾向於負責任的採購和環保的營養解決方案,這進一步促進了產品的普及和創新。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 富含必需營養素

- 提升運動能力

- 認知功能改善

- 產業潛在風險與挑戰

- 污染和污染物

- 市場機遇

- 健康保健產品對天然和永續蛋白質來源的需求日益成長。

- 海洋蛋白在運動營養和膳食補充劑中的應用日益廣泛,有助於肌肉恢復和整體健康。

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依來源分類,2022-2035年

- 魚類來源

- 源自甲殼類動物

- 藻類來源的

- 其他

第6章 市場估算與預測:依產品類型分類,2022-2035年

- 蛋白質濃縮物和分離物

- 魚蛋白濃縮物(FPC)

- 魚蛋白隔離群

- 海藻蛋白濃縮物

- 蛋白質水解物和生物活性胜肽

- 酵素水解物

- 酸鹼水解物

- 生物活性胜肽組分

- 膠原蛋白和明膠

- 海洋膠原蛋白

- 魚明膠

- 水解膠原蛋白肽

- 魚粉/魚油

- 功能性海洋化合物

第7章 市場估價與預測:依通路分類,2022-2035年

- 直銷(B2B)

- 銷售代理

- 線上管道

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 飲食

- 蛋白質強化

- 機能性食品

- 凝膠劑和穩定劑

- 肉類和水產品

- 麵包糖果甜點

- 其他

- 營養保健品(膳食補充品)

- Omega-3補充劑

- 膠原蛋白補充劑

- 關節和骨骼健康

- 體重管理

- 其他

- 藥品和治療藥物

- 化妝品和個人護理

- 抗衰老產品

- 肌膚水分和彈性

- 頭髮和指甲護理

- 其他

- 水產養殖和動物飼料

- 運動營養

- 蛋白粉棒

- 恢復補充劑

- 其他

- 其他

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第10章:公司簡介

- Cargill

- Epax

- FF Skagen A/S

- Gelita

- Gensei Global Industries Co.,Ltd

- Hofseth BioCare

- Omega Protein Corporation

- PESQUERA DIAMANTE

- Prima Protein AS

- Symrise AG

The Global Marine Derived Proteins Market was valued at USD 9.1 billion in 2025 and is estimated to grow at a CAGR of 9.4% to reach USD 22.3 billion by 2035.

Market growth is fueled by rising consumer awareness of the nutritional benefits associated with marine-based protein sources. These proteins are widely recognized for containing essential amino acids, omega fatty acids, and bioactive compounds that support overall wellness. Increasing interest in sustainable and responsibly sourced nutrition is further strengthening demand, as consumers seek environmentally conscious alternatives to traditional protein sources. Marine-derived proteins are gaining traction across dietary supplements, functional foods, and nutraceutical formulations, contributing to consistent industry expansion. In addition, the need for cost-effective and nutrient-dense ingredients in animal nutrition and aquaculture feed applications is supporting broader adoption. Advancements in processing technologies are enabling manufacturers to enhance product quality while maintaining sustainability standards. Growing focus on health, fitness, and performance-oriented nutrition is also encouraging higher consumption of marine proteins. As awareness of sustainable food systems continues to increase globally, the marine derived proteins market is positioned for substantial long-term growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.1 Billion |

| Forecast Value | $22.3 Billion |

| CAGR | 9.4% |

The fish-based proteins segment accounted for 67.8% share in 2025 and is expected to grow at a CAGR of 9.3% through 2035. Their dominance is supported by high protein concentration, established extraction infrastructure, and consistent raw material availability. These proteins remain integral to supplement and functional nutrition formulations due to their recognized nutritional profile. Continued improvements in responsible sourcing and resource management practices are further reinforcing stable supply and market confidence.

The protein concentrates and isolates segment held 42.2% share in 2025. Their leadership position stems from high purity levels and versatile applications across sports nutrition, dietary supplements, and functional food products. Increasing demand for clean-label and easily digestible protein ingredients is accelerating segment growth. At the same time, protein hydrolysates and bioactive peptides are experiencing rapid adoption because of their enhanced absorption characteristics and targeted nutritional benefits, particularly within performance and clinical nutrition segments.

North America Marine Derived Proteins Market is projected to grow at a CAGR of 9.3% between 2026 and 2035. Regional expansion is driven by heightened demand for sustainable, clean-label ingredients across functional foods, dietary supplements, and personal care formulations. Consumers in the region are demonstrating a stronger preference for responsibly sourced and environmentally friendly nutritional solutions, further supporting product adoption and innovation.

Key companies operating in the Global Marine Derived Proteins Market include Cargill, Symrise AG, Hofseth BioCare, Omega Protein Corporation, Gelita, Epax, PESQUERA DIAMANTE, Prima Protein AS, FF Skagen A/S, and Gensei Global Industries Co., Ltd. Companies in the Marine Derived Proteins Market are strengthening their competitive position through continuous product innovation, sustainability initiatives, and expanded distribution networks. Leading manufacturers are investing in advanced material technologies to enhance durability, stain resistance, and environmental performance. Strategic partnerships with residential developers and commercial contractors are increasing project-based sales opportunities. Businesses are also adopting omnichannel retail strategies that integrate digital platforms with traditional showrooms to improve customer engagement. Capacity modernization and supply chain optimization are helping reduce operational costs and delivery timelines.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Source

- 2.2.3 Product Type

- 2.2.4 Distribution channel

- 2.2.5 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rich in essential nutrients

- 3.2.1.2 Improved athletic performance

- 3.2.1.3 Enhanced cognitive function

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Pollution and contaminants

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for natural and sustainable protein sources in health and wellness products

- 3.2.3.2 Increasing adoption of marine proteins in sports nutrition and dietary supplements for muscle recovery and overall health

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Source, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Fish-based

- 5.3 Shellfish-based

- 5.4 Algae-based

- 5.5 Other

Chapter 6 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Protein concentrates & isolates

- 6.2.1 Fish protein concentrate (fpc)

- 6.2.2 Fish protein isolate

- 6.2.3 Seaweed protein concentrate

- 6.3 Protein hydrolysates & bioactive peptides

- 6.3.1 Enzymatic hydrolysates

- 6.3.2 Acid/alkali hydrolysates

- 6.3.3 Bioactive peptide fractions

- 6.4 Collagen & gelatin

- 6.4.1 Marine collagen

- 6.4.2 Fish gelatin

- 6.4.3 Hydrolyzed collagen peptides

- 6.5 Fishmeal & fish oil

- 6.6 Functional marine compounds

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Direct sales (B2B)

- 7.3 Distributors

- 7.4 Online channels

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Food & beverages

- 8.2.1 Protein fortification

- 8.2.2 Functional foods

- 8.2.3 Gelling & stabilizing agents

- 8.2.4 Meat & seafood products

- 8.2.5 Bakery & confectionery

- 8.2.6 Others

- 8.3 Dietary supplements & nutraceuticals

- 8.3.1 Omega-3 supplements

- 8.3.2 Collagen supplements

- 8.3.3 Joint & bone health

- 8.3.4 Weight management

- 8.3.5 Others

- 8.4 Pharmaceuticals & therapeutics

- 8.5 Cosmetics & personal care

- 8.5.1 Anti-aging products

- 8.5.2 Skin hydration & elasticity

- 8.5.3 Hair & nail care

- 8.5.4 Others

- 8.6 Aquaculture & animal feed

- 8.7 Sports nutrition

- 8.7.1 Protein powders & bars

- 8.7.2 Recovery supplements

- 8.7.3 Others

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Cargill

- 10.2 Epax

- 10.3 FF Skagen A/S

- 10.4 Gelita

- 10.5 Gensei Global Industries Co.,Ltd

- 10.6 Hofseth BioCare

- 10.7 Omega Protein Corporation

- 10.8 PESQUERA DIAMANTE

- 10.9 Prima Protein AS

- 10.10 Symrise AG

水解玉米蛋白市場規模、佔有率及成長分析(按類型、應用、理化性質及地區分類)-2026-2033年產業預測

水解玉米蛋白市場規模、佔有率及成長分析(按類型、應用、理化性質及地區分類)-2026-2033年產業預測 蛋白質市場規模、佔有率和成長分析(按來源類型、形態、應用、通路和地區分類)-2026-2033年產業預測

蛋白質市場規模、佔有率和成長分析(按來源類型、形態、應用、通路和地區分類)-2026-2033年產業預測 微生物蛋白市場規模、佔有率和成長分析(按微生物來源、功能、生產方法、應用、形態和地區分類)-2026-2033年產業預測

微生物蛋白市場規模、佔有率和成長分析(按微生物來源、功能、生產方法、應用、形態和地區分類)-2026-2033年產業預測 全球海洋蛋白市場全球水解玉米蛋白市場浮萍蛋白的全球市場全球草飼蛋白質市場全球BETA-乳球蛋白市場

全球海洋蛋白市場全球水解玉米蛋白市場浮萍蛋白的全球市場全球草飼蛋白質市場全球BETA-乳球蛋白市場 海洋蛋白的全球市場 - 全球產業分析,規模,佔有率,成長,趨勢,預測(2032年)

海洋蛋白的全球市場 - 全球產業分析,規模,佔有率,成長,趨勢,預測(2032年) 乳蛋白質脆餅市場至2030年的預測:按口味、包裝、形式、分銷管道、應用和地區的全球分析

乳蛋白質脆餅市場至2030年的預測:按口味、包裝、形式、分銷管道、應用和地區的全球分析