|

市場調查報告書

商品編碼

1998745

光收發器市場機會、成長要素、產業趨勢分析及2026-2035年預測。Optical Transceiver Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球光收發器市場預計到 2025 年價值 134 億美元,預計到 2035 年將達到 481 億美元,年複合成長率為 13.5%。

企業、雲端和電信網路向高頻寬數位基礎設施的持續轉型是推動市場成長的主要因素。通訊傳輸領域連貫的廣泛應用、分散式邊緣運算設施的擴展以及對高速互連以支援雲端原生應用和內容傳送平台日益成長的需求,都進一步刺激了市場需求。為實現 800G 和 1.6T 連接,超大規模資料中心的投資不斷增加,加上海底光纜容量的擴展,正在增強全球資料傳輸能力。都會區網路的持續升級、DSP 效率的提高、端口密度交換器的普及以及基於標準的連貫光技術的應用,都在加速這一趨勢的實施。最初由 2020 年前後 400ZR 插件模組標準化引發的解耦式連貫光技術發展趨勢,預計將持續到 2030 年,從而促進供應商多元化和靈活的網路架構。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 134億美元 |

| 預測金額 | 481億美元 |

| 複合年成長率 | 13.5% |

由於10-100 Gbps頻寬在企業、通訊聚合和行動接取網路的廣泛應用,預計到2025年,該細分市場的規模將達到50億美元。 10G、25G和50G頻寬連結在全球範圍內仍廣泛部署,因此持續存在替換和升級需求。這些解決方案經濟高效,並與現有交換基礎設施保持高度相容性,從而維持了企業和通訊環境中的出貨量。

預計到2025年,包括SFP+、SFP28和SFP56模組在內的SFP系列產品將佔據35.7%的市場。其向下相容性、經濟性和對1G至25G應用的適應性使其在企業網路、城域存取和傳統資料中心廣泛應用。寬頻匯聚和企業交換領域的持續成長也確保了成熟市場和新興市場對SFP系列產品的穩定需求。

預計到2025年,北美光收發器市佔率將達到28.3%。這一成長主要得益於大規模超大規模資料中心的擴張、人工智慧基礎設施的快速部署以及400G和800G互連技術的升級。北美擁有眾多雲端服務供應商,推動了對增強連貫傳輸網路和寬頻骨幹網路的持續投資。政府和通訊業者為提升海底光網路和城域網路基礎設施所做的努力,進一步鞏固了該地區的技術領先地位,這一趨勢預計將持續到2035年。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 部署 800G 和 1.6T 超大規模資料中心

- 用於人工智慧/機器學習集群間互連的頻寬擴展

- 海底電纜容量擴充計劃

- 5G去程傳輸和中傳中的高密度光纖。

- 共封裝光學元件開發方面的舉措

- 產業潛在風險與挑戰

- 高密度機架溫度控管的複雜性

- 800G模組的高功耗

- 市場機遇

- 矽光電整合技術的商業化

- 邊緣資料中心的光纖通訊升級週期

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

- 地緣政治和貿易趨勢

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 主要企業的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係與合作

- 技術進步

- 擴張和投資策略

- 數位轉型計劃

- 新興競爭對手和Start-Ups競爭對手的發展趨勢

第5章 市場估算與預測:依外型尺寸分類,2022-2035年

- SFP光束(SFP、SFP+、SFP28、SFP56、SFP112、SFP-DD)

- QSFP組(QSFP、QSFP+、QSFP28、QSFP56、QSFP-DD)

- OSFP

- CFP家族(CFP、CFP2、CFP4)

- XFP

- CXP

第6章 市場估計與預測:依資料傳輸速度分類,2022-2035年

- 小於 10 Gbps

- 10 至 100 Gbps

- 100-400 Gbps

- 400-800 Gbps

- 800 Gbps 或更高

第7章 市場估計與預測:依通訊協定,2022-2035年

- 乙太網路

- 光纖通道

- InfiniBand

- OTN(光纖傳輸網路)

- SONET/SDH

- PON(無源光纖網路)

- CPRI/eCPRI(通用公共無線電介面)

- PCIe 透過光纖傳輸

第8章 市場估算與預測:依採購管道分類,2022-2035年

- OEM捆綁採購

- 直接向製造商採購

- 第三方相容/售後市場採購

- 透過分銷管道進行採購

- 透過系統整合商/承包解決方案進行採購

第9章 市場估算與預測:依部署環境分類,2022-2035年

- 資料中心網路

- 通訊/運營商網路

- 企業園區/區域網路

- 工業/OT網路

- 國防和軍事網路

第10章 市場估價與預測:依連接器類型分類,2022-2035年

- LC(朗訊連接器)

- SC(用戶連接器)

- MPO/MTP(多芯光纖推入/拉出)

- FC(套圈連接器)

- ST(直尖)

- RJ45(銅線介面)

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- 主要企業

- Cisco Systems, Inc.

- Broadcom Inc.

- Coherent Corp.

- Lumentum Holdings Inc.

- Sumitomo Electric Industries, Ltd.

- 按地區分類的主要企業

- 北美洲

- Applied Optoelectronics, Inc.

- Molex, LLC

- 亞太地區

- Accelink Technologies Co., Ltd.

- Eoptolink Technology Inc., Ltd.

- Fujitsu Optical Components Limited

- Hisense Broadband

- Linktel Technologies Co., Ltd.

- Source Photonics, Inc.

- 歐洲

- Smiths Interconnect

- 北美洲

- 特殊玩家/干擾者

- ATOP Corporation

- ColorChip Ltd.

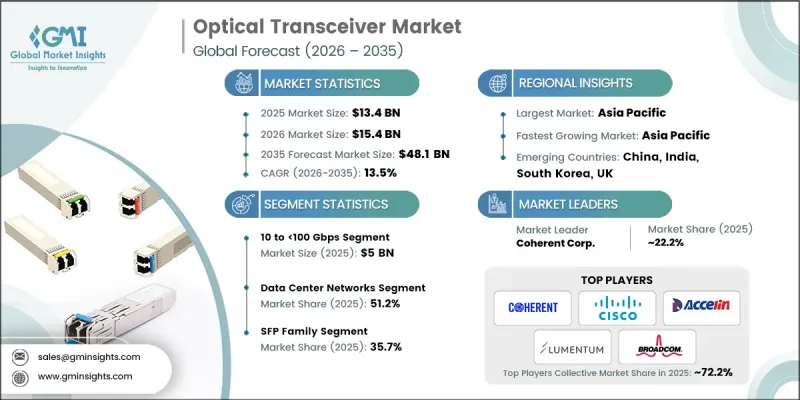

The Global Optical Transceiver Market was valued at USD 13.4 billion in 2025 and is estimated to grow at a CAGR of 13.5% to reach USD 48.1 billion by 2035.

The market growth is driven by the ongoing shift toward high-bandwidth digital infrastructure across enterprises, cloud, and telecom networks. Demand is fueled by the widespread deployment of coherent pluggables in telecom transport, the expansion of distributed edge computing facilities, and the rising need for high-speed interconnects to support cloud-native applications and content delivery platforms. Increasing investments in hyperscale data centers to implement 800G and 1.6T connectivity, combined with submarine cable capacity expansions, are enhancing global data transmission capabilities. Continued upgrades of metro networks, improved DSP efficiency, higher port-density switches, and adoption of standard-based coherent optics accelerate deployment. The trend toward disaggregated coherent optics, first catalyzed by 400ZR pluggable standardization around 2020, is expected to continue through 2030, promoting vendor diversification and flexible network architectures.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.4 Billion |

| Forecast Value | $48.1 Billion |

| CAGR | 13.5% |

The 10 to <100 Gbps segment reached USD 5 billion in 2025, due to its widespread presence across enterprise, telecom aggregation, and mobile access networks. Links in the 10G, 25G, and 50G range remain extensively deployed worldwide, resulting in consistent replacement and upgrade demand. These solutions are cost-effective and maintain high compatibility with existing switching infrastructure, sustaining shipment volumes in enterprise and telecom environments.

The SFP family segment held a 35.7% share in 2025, encompassing SFP+, SFP28, and SFP56 modules. Their backward compatibility, affordability, and suitability for 1G to 25G applications make them widely adopted across enterprise networks, metro access, and legacy data centers. Continued deployment in broadband aggregation and enterprise switching ensures steady demand across both mature and emerging markets.

North America Optical Transceiver Market accounted for 28.3% share in 2025. The region's growth is supported by large-scale hyperscale data center expansions, rapid AI infrastructure adoption, and upgrades to 400G and 800G interconnects. North America hosts a significant concentration of cloud service providers, driving sustained capital expenditure on coherent transport networks and broadband backbone enhancements. Government and operator initiatives to strengthen subsea and metro infrastructure further reinforce the region's technology leadership, expected to continue through 2035.

Prominent players in the Global Optical Transceiver Market include Accelink Technologies Co., Ltd., Eoptolink Technology Inc., Cisco Systems, Inc., Applied Optoelectronics, Inc., Coherent Corp. (formerly II-VI Incorporated), Fujitsu Optical Components Limited, Lumentum Holdings Inc., Molex, LLC, Sumitomo Electric Industries, Ltd., ATOP Corporation, ColorChip Ltd., Linktel Technologies Co., Ltd., Smiths Interconnect, Broadcom Inc., Hisense Broadband, and Source Photonics, Inc. Companies in the Optical Transceiver Market are strengthening their position by investing heavily in research and development to launch high-speed, energy-efficient, and scalable transceivers. Strategic partnerships with telecom operators, hyperscale cloud providers, and data center integrators enable faster adoption and market penetration. Firms are diversifying their portfolios to include coherent pluggables, high-bandwidth SFP modules, and disaggregated solutions to meet evolving network needs. Expansion of global manufacturing and logistics capabilities ensures timely delivery and scalability. Additionally, companies are focusing on standard compliance, interoperability testing, and collaborative ecosystem development to maintain credibility and expand their share in both mature and emerging markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Form factor trends

- 2.2.2 Data rate trends

- 2.2.3 Protocol trends

- 2.2.4 Deployment environment trends

- 2.2.5 Procurement channel trends

- 2.2.6 Connector type trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 800G and 1.6T hyperscale data center deployments

- 3.2.1.2 AI/ML cluster interconnect bandwidth expansion

- 3.2.1.3 Submarine cable capacity expansion projects

- 3.2.1.4 5G fronthaul and midhaul fiber densification

- 3.2.1.5 Co-packaged optics development initiatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Thermal management complexity in dense racks

- 3.2.2.2 High 800G module power consumption

- 3.2.3 Market opportunities

- 3.2.3.1 Silicon photonics integration commercialization

- 3.2.3.2 Edge data center optical upgrade cycles

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Form Factor, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 SFP family (SFP, SFP+, SFP28, SFP56, SFP112, SFP-DD)

- 5.3 QSFP family (QSFP, QSFP+, QSFP28, QSFP56, QSFP-DD)

- 5.4 OSFP

- 5.5 CFP family (CFP, CFP2, CFP4)

- 5.6 XFP

- 5.7 CXP

Chapter 6 Market Estimates and Forecast, By Data Rate, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Less than 10 Gbps

- 6.3 10 to <100 Gbps

- 6.4 100 to <400 Gbps

- 6.5 400 to <800 Gbps

- 6.6 800 Gbps and above

Chapter 7 Market Estimates and Forecast, By Protocol, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Ethernet

- 7.3 Fibre channel

- 7.4 InfiniBand

- 7.5 OTN (optical transport network)

- 7.6 SONET/SDH

- 7.7 PON (passive optical network)

- 7.8 CPRI/eCPRI (common public radio interface)

- 7.9 PCIe over optical

Chapter 8 Market Estimates and Forecast, By Procurement Channel, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 OEM-bundled procurement

- 8.3 Direct manufacturer procurement

- 8.4 Third-party compatible/aftermarket procurement

- 8.5 Distribution channel procurement

- 8.6 System integrator/turnkey solution procurement

Chapter 9 Market Estimates and Forecast, By Deployment Environment, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Data center networks

- 9.3 Telecom/carrier networks

- 9.4 Enterprise campus/LAN networks

- 9.5 Industrial/OT networks

- 9.6 Defense & military networks

Chapter 10 Market Estimates and Forecast, By Connector Type, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 LC (lucent connector)

- 10.3 SC (subscriber connector)

- 10.4 MPO/MTP (multi-fiber push-on/pull)

- 10.5 FC (ferrule connector)

- 10.6 ST (straight tip)

- 10.7 RJ45 (copper interface)

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 Cisco Systems, Inc.

- 12.1.2 Broadcom Inc.

- 12.1.3 Coherent Corp.

- 12.1.4 Lumentum Holdings Inc.

- 12.1.5 Sumitomo Electric Industries, Ltd.

- 12.2 Regional key players

- 12.2.1 North America

- 12.2.1.1 Applied Optoelectronics, Inc.

- 12.2.1.2 Molex, LLC

- 12.2.2 Asia Pacific

- 12.2.2.1 Accelink Technologies Co., Ltd.

- 12.2.2.2 Eoptolink Technology Inc., Ltd.

- 12.2.2.3 Fujitsu Optical Components Limited

- 12.2.2.4 Hisense Broadband

- 12.2.2.5 Linktel Technologies Co., Ltd.

- 12.2.2.6 Source Photonics, Inc.

- 12.2.3 Europe

- 12.2.3.1 Smiths Interconnect

- 12.2.1 North America

- 12.3 Niche Players/Disruptors

- 12.3.1 ATOP Corporation

- 12.3.2 ColorChip Ltd.

光收發器市場-2026-2032年全球市場預測第三方光收發器市場:2026-2032年全球市場預測(按外形尺寸、連接器類型、光纖模式、協定係列、光纖數量、應用和最終用戶分類)

光收發器市場-2026-2032年全球市場預測第三方光收發器市場:2026-2032年全球市場預測(按外形尺寸、連接器類型、光纖模式、協定係列、光纖數量、應用和最終用戶分類) 全球光收發器及測試儀銷售市場報告、競爭分析及區域商機(2026-2032年)

全球光收發器及測試儀銷售市場報告、競爭分析及區域商機(2026-2032年) 全球光收發器市場(2026-2036 年)

全球光收發器市場(2026-2036 年) 光收發器市場規模、佔有率和成長分析:按外形尺寸、資料速率、光纖類型、傳輸距離、連接器、協定、應用和地區分類-2026年至2033年產業預測

光收發器市場規模、佔有率和成長分析:按外形尺寸、資料速率、光纖類型、傳輸距離、連接器、協定、應用和地區分類-2026年至2033年產業預測 光收發器市場:按協定、資料速率、應用和地區分類

光收發器市場:按協定、資料速率、應用和地區分類 光收發器市場分析及預測(至2035年):類型、產品、技術、組件、應用、形狀、材料類型、最終用戶、模組、功能

光收發器市場分析及預測(至2035年):類型、產品、技術、組件、應用、形狀、材料類型、最終用戶、模組、功能 2026年全球多模光收發器市場報告2026年全球光收發器市場報告

2026年全球多模光收發器市場報告2026年全球光收發器市場報告 光收發器市場:按光纖類型、波長、外形尺寸、連接器、應用、距離、資料速率、國家和地區分類-產業分析、市場規模、佔有率和預測(2025-2032年)

光收發器市場:按光纖類型、波長、外形尺寸、連接器、應用、距離、資料速率、國家和地區分類-產業分析、市場規模、佔有率和預測(2025-2032年)