|

市場調查報告書

商品編碼

1959630

UV黏合劑市場機會、成長要素、產業趨勢分析及2026年至2035年預測。UV Adhesives Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

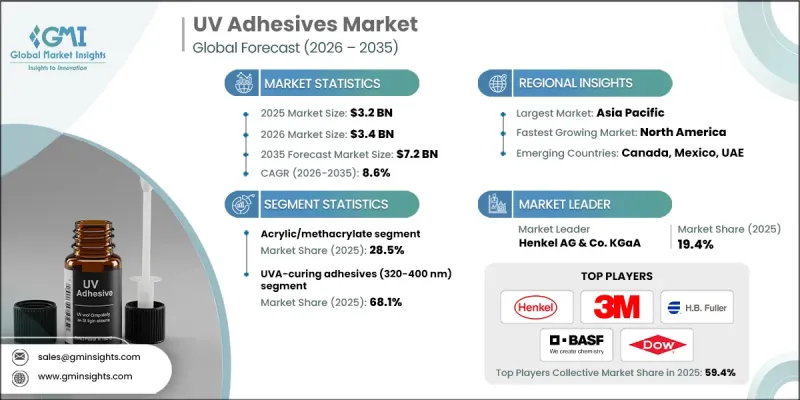

2025 年全球 UV黏合劑市場價值為 32 億美元,預計到 2035 年將達到 72 億美元,年複合成長率為 8.6%。

UV黏合劑是一種快速固化黏合劑,可在紫外光照射下聚合,從而在多種材料之間形成牢固持久的粘合。其獨特的固化特性使其適用於包括電子、汽車、醫療和消費品在內的眾多工業應用領域。電子和半導體產業對精確、高強度黏合的需求,以及工業生產的快速發展,顯著推動了UV黏合劑的需求成長。電動車的普及進一步加速了UV膠黏劑的應用,而出於安全性和可靠性的要求,UV膠黏劑成為電池組件、線路和電子模組的首選材料。在醫療領域,UV丙烯酸酯膠黏劑的生物相容性和無菌固化製程使其在外科器械和植入中的應用日益廣泛。配方技術的進步提高了UV黏合劑的固化速度、黏合深度、柔軟性和耐化學性,使其成為現代複雜製造流程中不可或缺的黏合劑。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 32億美元 |

| 預測金額 | 72億美元 |

| 複合年成長率 | 8.6% |

到2025年,丙烯酸/甲基丙烯酸酯黏合劑將佔據28.5%的市場佔有率。由於其兼具柔軟性、耐久性和快速固化等優異性能,該細分市場正穩步成長。丙烯酸/甲基丙烯酸黏合劑對包括塑膠、金屬和玻璃在內的多種表面具有高黏合力,在電子、汽車和消費品應用領域用途廣泛。其對不同基材的適應性以及即使在嚴苛條件下也能保持穩定的性能,進一步鞏固了其競爭優勢。

同時,波長在320-400奈米範圍內固化的UVA固化黏合劑預計到2025年將佔據68.1%的市場佔有率。其廣泛的適用性、快速固化和深層滲透性使其在電子、醫療設備和工業包裝領域尤為有效。快速固化和對多種材料具有強黏合力的雙重優勢,正推動其在多個工業領域中廣泛應用。

預計2026年至2035年,北美紫外線黏合劑市場將以8.7%的複合年成長率成長。人們日益關注永續製造、污水回收和工業污水管理,這符合循環經濟的原則,並推動紫外線黏合劑的應用範圍不斷擴大。醫療、個人護理和工業領域消費者環保意識的增強以及對環保產品需求的增加,促使製造商開發符合嚴格環保標準的紫外線黏合劑,從而進一步促進市場擴張。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 電子和半導體製造業的快速成長

- 擴大電動車(EV)的生產

- 醫療設備市場擴張

- 產業潛在風險與挑戰

- 高昂的初始投資成本

- 技術限制和應用限制

- 市場機遇

- 3D列印與積層製造的新應用領域

- 智慧型功能型黏合劑技術

- 促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續努力

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 公司矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依產品分類,2022-2035年

- 丙烯酸/甲基丙烯酸酯

- 環氧樹脂

- 環氧丙烯酸酯雜化物

- 胺甲酸乙酯丙烯酸酯

- 矽酮

- 氰基丙烯酸酯

- 聚酯纖維

- 其他

第6章 市場估算與預測:依固化技術分類,2022-2035年

- UVA固化黏合劑(320-400奈米)

- UVB固化黏合劑(280-320奈米)

- UVC固化黏合劑(200-280奈米)

- 其他

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 黏合與組裝

- 密封件和墊圈

- 塗層和保護

- 灌封和封裝

- 層壓板

- 其他

第8章 市場估算與預測:依最終用途產業分類,2022-2035年

- 醫療保健

- 一次性醫療設備

- 診斷設備

- 手術器械和工具

- 穿戴式醫療設備

- 其他

- 電子和半導體

- 顯示組件

- 半導體封裝

- 相機模組組裝

- 其他

- 車

- 頭燈和尾燈組件

- 外部密封件和墊圈

- 內裝零件和儀表板黏合劑

- 其他

- 航太/國防

- 複合結構膠合劑

- 感測器和電子設備的灌封

- 內板黏合

- 其他

- 包裝

- 軟性包裝複合

- 硬包裝

- 藥品包裝

- 其他

- 光學和光電

- 化妝品和個人護理

- 凝膠指甲油和指甲藝術

- 黏合劑

- 其他

- 建築材料

- 其他

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第10章:公司簡介

- 3M Company

- Avery Dennison

- BASF SE

- Cartell UK Ltd

- DELO Industrial Adhesives

- Epoxy Technology, Inc

- HB Fuller Company

- Henkel AG &Co. KGaA

- Panacol-Elosol Gmbh

- Permabond Engineering Adhesives

- Sika AG

- The Dow Chemical Company

The Global UV Adhesives Market was valued at USD 3.2 billion in 2025 and is estimated to grow at a CAGR of 8.6% to reach USD 7.2 billion by 2035.

UV adhesives are fast-curing bonding agents that polymerize under ultraviolet light, providing strong and durable adhesion between diverse materials. Their unique curing properties allow application across industries such as electronics, automotive, healthcare, and consumer goods. Rapid industrial production and the need for precise, high-strength bonding in electronics and semiconductors have significantly boosted demand. The rise of electric vehicles further drives adoption, as UV adhesives are preferred for battery components, wiring, and electronic modules due to safety and reliability requirements. In the medical sector, UV acrylate adhesives are increasingly used for surgical instruments and implants, valued for their biocompatibility and sterile curing process. Advances in formulations have enhanced curing speed, bonding depth, flexibility, and chemical resistance, making UV adhesives essential for complex modern manufacturing processes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.2 Billion |

| Forecast Value | $7.2 Billion |

| CAGR | 8.6% |

In 2025, the acrylic/methacrylate adhesives accounted for 28.5% share. This segment is expanding steadily due to its balanced combination of flexibility, durability, and rapid curing. Acrylic/methacrylate adhesives provide high adhesion across a variety of surfaces, including plastics, metals, and glass, making them highly versatile for electronics, automotive, and consumer applications. Their adaptability to multiple substrates and consistent performance under challenging conditions contribute to their dominance.

The UVA-curing adhesives, operating within the 320-400 nm wavelength range, represented the 68.1% share in 2025. Their broad applicability, rapid curing, and deep penetration make them particularly effective for electronics, medical devices, and industrial packaging. The combination of fast curing and strong bonding capability across diverse materials has driven widespread adoption in multiple industrial sectors.

North American UV Adhesives Market is expected to grow at a CAGR of 8.7% from 2026 to 2035. Increased emphasis on sustainable manufacturing, recycling wastewater, and industrial effluent management has expanded UV adhesive applications, aligning with circular economy principles. Growing consumer awareness and demand for eco-friendly products in healthcare, personal care, and industrial sectors are motivating manufacturers to develop UV adhesives that meet stringent environmental standards, further supporting market expansion.

Key players in the UV Adhesives Market include Avery Dennison, 3M Company, Sika AG, Panacol-Elosol GmbH, DELO Industrial Adhesives, Henkel AG & Co. KGaA, Permabond Engineering Adhesives, BASF SE, Epoxy Technology, Inc., The Dow Chemical Company, Cartell UK Ltd, and HB Fuller Company. Companies in the UV adhesives market strengthen their presence through continuous innovation, expanding product portfolios, and investing in R&D to improve curing speed, bond strength, and chemical resistance. Strategic collaborations with electronics, automotive, and medical device manufacturers allow customized solutions that meet precise industry requirements. Firms emphasize sustainability by developing eco-friendly formulations compliant with environmental regulations. Global expansion strategies, including partnerships, acquisitions, and establishing regional production facilities, enhance accessibility and reduce delivery lead times.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Curing technology

- 2.2.4 Application

- 2.2.5 End use industry

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid growth in electronics & semiconductor manufacturing

- 3.2.1.2 Electric vehicle (EV) production expansion

- 3.2.1.3 Medical device market expansion

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment costs

- 3.2.2.2 Technical limitations & application constraints

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging applications in 3D printing & additive manufacturing

- 3.2.3.2 Smart & functional adhesive technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Acrylic/methacrylate

- 5.3 Epoxy

- 5.4 Epoxy acrylate hybrid

- 5.5 Urethane acrylate

- 5.6 Silicone

- 5.7 Cyanoacrylate

- 5.8 Polyester

- 5.9 Others

Chapter 6 Market Estimates and Forecast, By Curing Technology, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 UVA-curing adhesives (320-400 nm)

- 6.3 UVB-curing adhesives (280-320 nm)

- 6.4 UVC-curing adhesives (200-280 nm)

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Bonding & assembly

- 7.3 Sealing & gasketing

- 7.4 Coating & protective

- 7.5 Potting & encapsulation

- 7.6 Laminating

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Medical & healthcare

- 8.2.1 Disposable medical devices

- 8.2.2 Diagnostic devices

- 8.2.3 Surgical instruments & tools

- 8.2.4 Wearable medical devices

- 8.2.5 Others

- 8.3 Electronics & semiconductor

- 8.3.1 Display assembly

- 8.3.2 Semiconductor packaging

- 8.3.3 Camera module assembly

- 8.3.4 Others

- 8.4 Automotive

- 8.4.1 Headlight & taillight assembly

- 8.4.2 Exterior sealing & gasketing

- 8.4.3 Interior trim & dashboard bonding

- 8.4.4 Others

- 8.5 Aerospace & defense

- 8.5.1 Composite structure bonding

- 8.5.2 Sensor & electronics potting

- 8.5.3 Interior panel bonding

- 8.5.4 Others

- 8.6 Packaging

- 8.6.1 Flexible packaging lamination

- 8.6.2 Rigid packaging

- 8.6.3 Pharmaceutical packaging

- 8.6.4 Others

- 8.7 Optical & photonics

- 8.8 Cosmetics & personal care

- 8.8.1 Gel nail polish & nail art

- 8.8.2 False eyelash adhesives

- 8.8.3 Others

- 8.9 Construction & building materials

- 8.10 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 3M Company

- 10.2 Avery Dennison

- 10.3 BASF SE

- 10.4 Cartell UK Ltd

- 10.5 DELO Industrial Adhesives

- 10.6 Epoxy Technology, Inc

- 10.7 HB Fuller Company

- 10.8 Henkel AG & Co. KGaA

- 10.9 Panacol-Elosol Gmbh

- 10.10 Permabond Engineering Adhesives

- 10.11 Sika AG

- 10.12 The Dow Chemical Company

UV固化黏合劑市場:依樹脂類型、配方、應用和最終用戶分類-2026-2032年全球預測

UV固化黏合劑市場:依樹脂類型、配方、應用和最終用戶分類-2026-2032年全球預測 UV固化黏合劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

UV固化黏合劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 2026年全球UV固化黏合劑市場報告2026年全球紫外線黏合劑市場報告

2026年全球UV固化黏合劑市場報告2026年全球紫外線黏合劑市場報告 2026-2030年全球紫外光固化黏合劑市場

2026-2030年全球紫外光固化黏合劑市場 UV黏合劑市場規模、佔有率及成長分析(按產品類型、應用和地區分類)-2026-2033年產業預測

UV黏合劑市場規模、佔有率及成長分析(按產品類型、應用和地區分類)-2026-2033年產業預測 紫外線固化膠合劑市場-全球產業規模、佔有率、趨勢、機會和預測,按樹脂類型、應用、地區和競爭情況細分,2020-2030 年

紫外線固化膠合劑市場-全球產業規模、佔有率、趨勢、機會和預測,按樹脂類型、應用、地區和競爭情況細分,2020-2030 年 紫外線黏合劑市場 - 預測 2025-2030

紫外線黏合劑市場 - 預測 2025-2030 紫外線黏合劑市場(按產品類型、應用和地區)

紫外線黏合劑市場(按產品類型、應用和地區) UV硬化型黏劑的全球市場:樹脂類型·基材·終端用戶·不同地區的預測 (~2032年)

UV硬化型黏劑的全球市場:樹脂類型·基材·終端用戶·不同地區的預測 (~2032年)