|

市場調查報告書

商品編碼

1959551

施工機械租賃市場機會、成長要素、產業趨勢分析及2026年至2035年預測Construction Equipment Rental Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

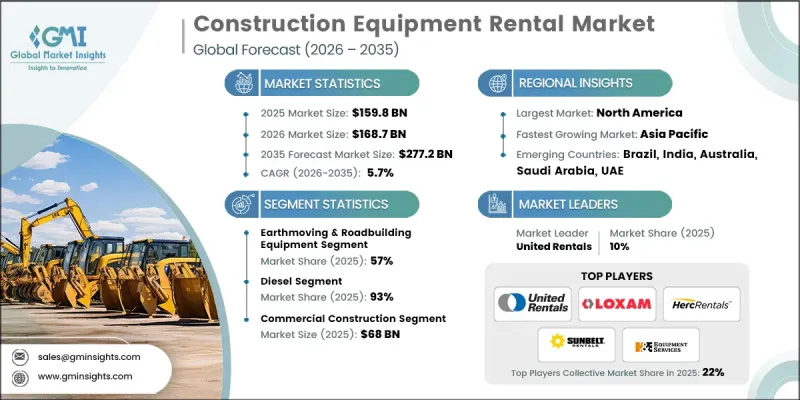

2025年全球施工機械租賃市場價值1,598億美元,預計2035年將達2,772億美元,年複合成長率為5.7%。

在住宅、商業和大型基礎設施計劃中,對土木工程施工機械、物料輸送設備和高空作業平台的需求日益成長。中小型承包商是租賃解決方案最積極的採用者,而大型承包商也在擴大租賃設備的使用,以滿足尖峰時段需求,並在無需長期投資的情況下獲得專用設備。租賃公司正在轉型經營模式,專注於客戶維繫、服務商品搭售和可預測的定價。透過擴大設備規模,瞄準可再生能源、隧道建設和大型基礎設施等高價值行業,供應商可以提供客製化設計的設備,計劃專屬契約,並建立忠實的基本客群。這種方式使租賃公司能夠在滿足不斷變化的建築需求的同時,提高營運效率和盈利。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 1598億美元 |

| 預測金額 | 2772億美元 |

| 複合年成長率 | 5.7% |

預計到 2025 年,土木工程和道路施工設備領域將佔據 57% 的市場佔有率,並從 2026 年到 2035 年以 4.9% 的複合年成長率成長。各公司正在整合其車隊並收購互補業務,以提供更廣泛的機械選擇,擴大其區域影響力,並服務大規模的現有基本客群。

柴油動力設備市佔率高達93%,預計2026年至2035年將以5.2%的複合年成長率成長。憑藉其可靠性、動力性和高效性,柴油機械仍然是土木工程、鋪路和混凝土施工等重型作業的首選。 Rental Fleet將繼續專注於柴油動力設備,以滿足承包商在無法採用傳統動力解決方案的計劃中的需求。

預計到2025年,美國施工機械租賃市場規模將達756億美元。美國市場的成長主要得益於強勁的基礎建設支出、成熟的商業建築市場以及完善的租賃行業。承包商越來越依賴租賃設備來擴大營運規模、降低資本支出,並為短期或高需求計劃取得專用機械。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 成本結構

- 利潤率

- 每個階段增加的價值

- 垂直整合趨勢

- 顛覆者

- 影響因素

- 促進因素

- 聯網汽車和軟體定義汽車的日益普及。

- 消費者對個人化和免持操作的需求日益成長。

- 電動車 (EV) 和自動駕駛汽車領域的擴張

- 售後市場和軟體升級機會增加

- 產業潛在風險與挑戰

- 聯網汽車和軟體定義汽車的日益普及。

- 消費者對個人化和免持操作的需求日益成長。

- 市場機遇

- AI驅動的預測和生成助手

- 多模態人機介面實施現狀

- 雲端連線和OTA更新

- 智慧駕駛座區域部署狀況

- 促進因素

- 技術趨勢與創新生態系統

- 目前技術

- 新興技術

- 成長潛力分析

- 監理情勢

- 北美洲

- 職業安全與健康管理局(OSHA)

- 美國環保署(EPA)排放標準

- 加拿大運輸部職場安全與設備法規

- 歐洲

- 歐盟機械指令 (MD) 和 CE 認證

- 歐盟第五階段排放氣體法規

- ISO 20474(土木工程施工機械安全標準)

- 亞太地區

- 日本產業安全衛生法

- 中國國家施工機械標準(GB標準)

- 印度AIS/排放氣體和安全指南

- 拉丁美洲

- 巴西INMETRO認證

- 哥倫比亞勞動部安全法規

- 阿根廷施工機械安全指南

- 中東和非洲

- 阿拉伯聯合大公國聯邦人力資源及資源機構及ESMA標準

- 阿曼勞動部設備安全規章

- 南非SABS施工機械標準

- 北美洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- OEM定價模式

- 售後市場價格趨勢

- 訂閱購買模式

- 區域價格波動

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 碳足跡考量

- 資產利用率和車隊生產力基準測試

- 電氣化準備與轉型藍圖

- 租賃滲透率與所有權模式轉換分析

- 數位化和遠端資訊處理的影響分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 競爭定位矩陣

- 戰略展望矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估價與預測:依產品分類,2022-2035年

- 土木工程及道路施工機械

- 後鏟

- 挖土機

- 裝載機

- 壓實設備

- 其他

- 物料輸送和起重機

- 儲存和運輸設備

- 工程系統

- 工業車輛

- 散裝物料輸送設備

- 混凝土設備

- 混凝土泵

- 破碎機

- 運輸攪拌車

- 瀝青鋪築機

- 混凝土攪拌站

第6章 市場估計與預測:依促進因素分類,2022-2035年

- 柴油引擎

- CNG/LNG

- 電的

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 住宅

- 商業建築

- 工業建築

- 採礦和採石

第8章 市場估算與預測:依最終用途分類,2022-2035年

- 建設公司

- 礦業營運商

- 租賃公司

- 政府/市政當局

- 工業用戶

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 比利時

- 荷蘭

- 瑞典

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 新加坡

- 韓國

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 世界公司

- Ashtead Technology(Sunbelt Rentals)

- Capital Equipment Rental

- Elliott Equipment Company

- Herc Rentals

- Hertz Equipment Rentals

- JLG

- John Deere Rental

- Loxam

- Ritchie Bros. Auctioneers

- United Rentals

- 當地公司

- Allmand Brothers

- Atlas Rents

- Bakersfield Rental

- Maxim Crane Works

- NESCO Rentals

- Riwal

- Stephenson's Rental Services

- Sunstate Equipment

- Toromont CAT

- WesternOne

- 新興企業

- Allmand Brothers

- Capital Equipment Rental

- Bakersfield Rental

- Sunstate Equipment

The Global Construction Equipment Rental Market was valued at USD 159.8 billion in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 277.2 billion by 2035.

The industry is witnessing high demand for earthmoving, materials handling, and aerial lift equipment across residential, commercial, and large infrastructure projects. Small and mid-sized contractors are among the fastest adopters of rental solutions, while large contractors are increasingly using rented machinery to meet peak demands and access specialized equipment without long-term investment. Rental companies are shifting their business models, focusing on customer retention, service bundling, and predictable pricing. Expansion of fleets targeted to high-value sectors, such as renewable energy, tunneling, and major infrastructure, allows providers to offer purpose-built equipment, secure project-specific contracts, and develop loyal customer bases. This approach ensures rental companies can cater to evolving construction demands while improving operational efficiency and profitability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $159.8 Billion |

| Forecast Value | $277.2 Billion |

| CAGR | 5.7% |

The earthmoving and roadbuilding equipment segment held a 57% share in 2025 and is projected to grow at a CAGR of 4.9% from 2026 to 2035. Companies are consolidating fleets and acquiring complementary businesses to provide diversified machinery options, expand regional presence, and serve larger established customer bases.

The diesel-powered equipment segment held a 93% share and is expected to grow at a CAGR of 5.2% between 2026 and 2035. Diesel machinery remains the preferred choice for heavy-duty operations due to its reliability, power, and efficiency in earthmoving, paving, and concrete applications. Rental fleets continue to focus on diesel-powered units to meet contractor needs in projects where electricity-based solutions are not feasible.

U.S. Construction Equipment Rental Market reached USD 75.6 billion in 2025. Growth in the U.S. is driven by robust infrastructure spending, mature commercial construction, and the established rental industry. Contractors increasingly rely on rental equipment to scale operations, reduce capital expenditure, and access specialized machinery for short-term or high-demand projects.

Key players operating in the Global Construction Equipment Rental Market include Allmand Brothers, Ashtead Technology (Sunbelt Rentals), Atlas Rents, Bakersfield Rental, Herc Rentals, JLG, John Deere Rental, Loxam, Ritchie Bros. Auctioneers, and United Rentals. Companies in the Construction Equipment Rental Market are strengthening their position by expanding regional and sector-specific fleets, acquiring complementary rental businesses, and offering bundled services with predictable pricing. Firms are investing in purpose-built equipment for high-value projects, forming strategic alliances with contractors, and leveraging digital platforms for equipment tracking and maintenance. Focus on customer loyalty programs, flexible rental terms, and specialized training services enhances client retention while improving operational efficiency. Emphasis on renewable energy, tunneling, and infrastructure sectors ensures access to premium contracts and market growth opportunities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Propulsion

- 2.2.4 Application

- 2.2.5 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing adoption of connected and software-defined vehicles.

- 3.2.1.2 Rising consumer demand for personalization and hands-free operation

- 3.2.1.3 Expansion of EV and autonomous vehicle segments

- 3.2.1.4 Increasing aftermarket and software upgrade opportunities

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Growing adoption of connected and software-defined vehicles.

- 3.2.2.2 Rising consumer demand for personalization and hands-free operation

- 3.2.3 Market opportunities

- 3.2.3.1 AI-driven predictive and generative assistants

- 3.2.3.2 Multimodal HMI adoption

- 3.2.3.3 Cloud connectivity and OTA updates

- 3.2.3.4 Regional adoption of intelligent cockpits

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.2 Emerging technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 Occupational Safety and Health Administration (OSHA)

- 3.5.1.2 Environmental Protection Agency (EPA) Emission Standards

- 3.5.1.3 Transport Canada Workplace Safety & Equipment Regulations

- 3.5.2 Europe

- 3.5.2.1 EU Machinery Directive (MD) & CE Certification

- 3.5.2.2 EU Stage V Emission Standards

- 3.5.2.3 ISO 20474 (Earth-moving Machinery Safety Standards)

- 3.5.3 Asia-Pacific

- 3.5.3.1 Japan Industrial Safety & Health Act

- 3.5.3.2 China GB Standards for Construction Machinery

- 3.5.3.3 India AIS/Emission & Safety Guidelines

- 3.5.4 Latin America

- 3.5.4.1 Brazil INMETRO Certification

- 3.5.4.2 Colombia Ministry of Labor Safety Regulations

- 3.5.4.3 Argentina Construction Equipment Safety Guidelines

- 3.5.5 Middle East & Africa

- 3.5.5.1 UAE Federal Authority for Human Resources & ESMA Standards

- 3.5.5.2 Oman Ministry of Labor Equipment Safety Regulations

- 3.5.5.3 South Africa SABS Construction Equipment Standards

- 3.5.1 North America

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Price trends

- 3.8.1 OEM Pricing models

- 3.8.2 Aftermarket pricing trends

- 3.8.3 Subscription purchase models

- 3.8.4 Regional price variations

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Asset Utilization & Fleet Productivity Benchmarking

- 3.12 Electrification Readiness & Transition Roadmap

- 3.13 Rental Penetration & Ownership Shift Analysis

- 3.14 Digitalization & Telematics Impact Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Earthmoving & roadbuilding equipment

- 5.2.1 Backhoe

- 5.2.2 Excavator

- 5.2.3 Loader

- 5.2.4 Compaction equipment

- 5.2.5 Others

- 5.3 Material handling and cranes

- 5.3.1 Storage and handling equipment

- 5.3.2 Engineered systems

- 5.3.3 Industrial trucks

- 5.3.4 Bulk material handling equipment

- 5.4 Concrete equipment

- 5.4.1 Concrete pumps

- 5.4.2 Crusher

- 5.4.3 Transit mixers

- 5.4.4 Asphalt pavers

- 5.4.5 Batching plants

Chapter 6 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Diesel

- 6.3 CNG/LNG

- 6.4 Electric

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Residential Construction

- 7.3 Commercial Construction

- 7.4 Industrial Construction

- 7.5 Mining & Quarrying

Chapter 8 Market Estimates & Forecast, By End use, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Construction Companies

- 8.3 Mining Operators

- 8.4 Rental Companies

- 8.5 Government & Municipalities

- 8.6 Industrial Users

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 9.1 North America

- 9.1.1 US

- 9.1.2 Canada

- 9.2 Europe

- 9.2.1 UK

- 9.2.2 Germany

- 9.2.3 France

- 9.2.4 Italy

- 9.2.5 Spain

- 9.2.6 Belgium

- 9.2.7 Netherlands

- 9.2.8 Sweden

- 9.2.9 Russia

- 9.3 Asia Pacific

- 9.3.1 China

- 9.3.2 India

- 9.3.3 Japan

- 9.3.4 Australia

- 9.3.5 Singapore

- 9.3.6 South Korea

- 9.3.7 Vietnam

- 9.3.8 Indonesia

- 9.4 Latin America

- 9.4.1 Brazil

- 9.4.2 Mexico

- 9.4.3 Argentina

- 9.5 MEA

- 9.5.1 South Africa

- 9.5.2 Saudi Arabia

- 9.5.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Companies

- 10.1.1 Ashtead Technology (Sunbelt Rentals)

- 10.1.2 Capital Equipment Rental

- 10.1.3 Elliott Equipment Company

- 10.1.4 Herc Rentals

- 10.1.5 Hertz Equipment Rentals

- 10.1.6 JLG

- 10.1.7 John Deere Rental

- 10.1.8 Loxam

- 10.1.9 Ritchie Bros. Auctioneers

- 10.1.10 United Rentals

- 10.2 Regional Companies

- 10.2.1 Allmand Brothers

- 10.2.2 Atlas Rents

- 10.2.3 Bakersfield Rental

- 10.2.4 Maxim Crane Works

- 10.2.5 NESCO Rentals

- 10.2.6 Riwal

- 10.2.7 Stephenson's Rental Services

- 10.2.8 Sunstate Equipment

- 10.2.9 Toromont CAT

- 10.2.10 WesternOne

- 10.3 Emerging Companies

- 10.3.1 Allmand Brothers

- 10.3.2 Capital Equipment Rental

- 10.3.3 Bakersfield Rental

- 10.3.4 Sunstate Equipment

2026-2030年全球施工機械租賃市場

2026-2030年全球施工機械租賃市場 施工機械租賃市場:2026-2032年全球市場預測(依設備類型、租賃期限、動力來源、營運方式、租賃模式及應用領域分類)

施工機械租賃市場:2026-2032年全球市場預測(依設備類型、租賃期限、動力來源、營運方式、租賃模式及應用領域分類) 施工機械租賃市場-全球產業規模、佔有率、趨勢、機會和預測:按設備類型、產品類型、應用類型、驅動類型、地區和競爭格局分類,2021-2031年

施工機械租賃市場-全球產業規模、佔有率、趨勢、機會和預測:按設備類型、產品類型、應用類型、驅動類型、地區和競爭格局分類,2021-2031年 施工機械租賃市場報告:按型號、驅動系統、應用和地區分類(2026-2034 年)

施工機械租賃市場報告:按型號、驅動系統、應用和地區分類(2026-2034 年) 施工機械租賃市場:按機器類型和地區分類

施工機械租賃市場:按機器類型和地區分類 2026年全球施工機械租賃市場報告2026年全球重型建築設備租賃市場報告

2026年全球施工機械租賃市場報告2026年全球重型建築設備租賃市場報告 施工機械及工具租賃平台市場預測至2034年-全球分析(依設備類型、租賃模式、定價模式、客戶類型、最終用戶及地區分類)重型施工機械租賃市場-全球產業規模、佔有率、趨勢、機會與預測:按設備類型、應用、地區和競爭格局分類,2021-2031年日本施工機械租賃市場報告:按解決方案、設備、類型、應用、產業和地區分類(2026-2034年)

施工機械及工具租賃平台市場預測至2034年-全球分析(依設備類型、租賃模式、定價模式、客戶類型、最終用戶及地區分類)重型施工機械租賃市場-全球產業規模、佔有率、趨勢、機會與預測:按設備類型、應用、地區和競爭格局分類,2021-2031年日本施工機械租賃市場報告:按解決方案、設備、類型、應用、產業和地區分類(2026-2034年)