|

市場調查報告書

商品編碼

1959341

聯網汽車安全市場機會、成長要素、產業趨勢分析及2026年至2035年預測Connected Car Security Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

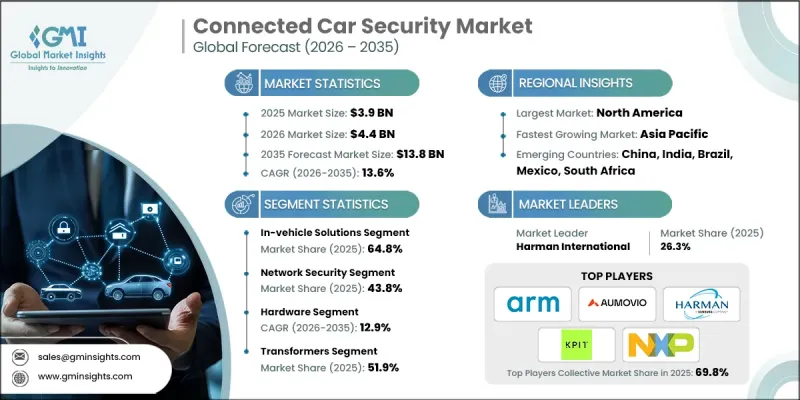

2025 年全球聯網汽車安全市場價值 39 億美元,預計到 2035 年將達到 138 億美元,年複合成長率為 13.6%。

隨著聯網汽車技術的快速普及,對整個車輛生態系統、車隊管理平台和雲端連接服務中強大的網路安全的需求變得尤為迫切。汽車製造商和企業正擴大將安全功能直接整合到車輛電子架構、後端伺服器和雲端平台中,以降低營運風險並減少對人工監控的依賴。邊緣人工智慧處理器、V2X 通訊和車輛軟體平台的持續進步正在提升安全解決方案的效能、擴充性和響應速度。即時入侵偵測、安全資料交換和空中下載 (OTA) 更新正逐漸成為保護大規模車隊的標準配備。汽車製造商、網路安全供應商和雲端營運商之間的策略聯盟、合併和合作正在加速將安全性整合到車輛生命週期、車隊營運和出行服務。聯網汽車安全正從傳統的監控模式演變為以人工智慧驅動的主動威脅分析系統,從而保護軟體定義的車輛和出行平台。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 39億美元 |

| 預測金額 | 138億美元 |

| 複合年成長率 | 13.6% |

預計到2025年,汽車解決方案產業將佔據64.8%的市場佔有率,並在2035年之前以12.1%的複合年成長率成長。這些解決方案為電控系統、網域控制器、遠端資訊處理模組和資訊娛樂系統提供嵌入式安全功能,從而實現即時監控、入侵防禦和安全通訊。汽車製造商正將汽車安全放在首位,以滿足法規和安全標準,並確保車輛系統能夠抵禦網路攻擊。

預計到2025年,網路安全領域的市佔率將達到43.8%,並在2026年至2035年間以12.8%的複合年成長率成長。網路安全透過提供強大的通訊協定、即時監控和入侵防禦,保護車輛通訊網路、車載資料匯流排和雲端連線免受網路威脅。維護系統完整性仍然是原始設備製造商 (OEM)、車隊營運商和旅遊服務供應商的關鍵需求。

預計到2025年,美國聯網汽車安全市場規模將達到14億美元,隨著汽車製造商、車隊營運商和科技公司持續投資於先進的網路安全平台,該市場將持續成長。各公司正在部署整合硬體和軟體解決方案,以保護車載資訊系統、V2X通訊和車載網路,同時確保符合內燃機汽車和電動車的安全標準和法規要求。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 聯網汽車和軟體定義汽車的日益普及。

- 針對汽車系統的網路安全威脅日益增加。

- 監管要求和安全標準

- 電動車、自動駕駛汽車和共用出行汽車的成長

- 產業潛在風險與挑戰

- 保障異質車輛架構安全的複雜性

- 與資料隱私和跨境監管合規相關的挑戰。

- 市場機遇

- 將安全功能整合到車輛軟體平台和OTA生態系統中

- V2X、5G 和基於雲端的車輛服務的擴展

- 擴大基於硬體的安全解決方案的採用範圍

- 人們越來越關注自動駕駛和ADAS安全性

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國國家公路交通安全管理局(NHTSA)

- 美國商務部/工業與安全局(BIS)

- 聯邦貿易委員會(FTC)

- 歐洲

- 聯合國歐洲經濟委員會WP.29條例(聯合國條例R155和R156)

- EN/ISO汽車標準

- 亞太地區

- 中國國家車輛網路安全標準

- 印度汽車標準(AIS 189 和 AIS 190)

- 拉丁美洲

- 巴西:LGPD(通用資料保護法)

- 墨西哥:NOM 標準

- 中東和非洲

- 阿拉伯聯合大公國(阿拉伯聯合大公國)與海灣國家:物聯網與車聯網安全政策

- 沙烏地阿拉伯:SDAIA汽車人工智慧框架

- 非洲聯盟(非盟):資料政策框架

- 北美洲

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢分析

- 專利分析

- 永續性和環境方面

- 永續實踐

- 生產中的能源效率

- 碳足跡考量

- 資料管治、網路安全與模型風險

- 資料隱私與合規

- 模型安全

- 操作風險和系統性風險

- 安全架構

- 多層安全模型

- 車聯網(V2X)安全

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估計與預測:依證券類型分類,2022-2035年

- 端點安全

- 應用程式安全

- 網路安全

- 雲端安全

第6章 市場估計與預測:依類型分類,2022-2035年

- 汽車解決方案

- 外部雲端服務

第7章 市場估計與預測:依解法分類,2022-2035年

- 軟體

- 硬體

- 硬體安全模組(HSM)

- 安全微控制器

- 可信任平台模組(TPM)

- 安全閘道器

- 其他

第8章 市場估價與預測:依車輛類型分類,2022-2035年

- 掀背車

- 轎車

- SUV

第9章 市場估計與預測:依促進因素分類,2022-2035年

- 內燃機(ICE)

- 電動車

- 電池式電動車(BEV)

- 插電式混合動力車(PHEV)

- 混合動力電動車(HEV)

- 燃料電池電動車(FCEV)

第10章 市場估價與預測:依應用領域分類,2022-2035年

- 車載資訊控制單元(TCU)

- 資訊娛樂系統

- 進階駕駛輔助系統與自動駕駛系統

- 通訊模組

- 其他

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 俄羅斯

- 挪威

- 丹麥

- 荷蘭

- 比利時

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ANZ

- 越南

- 印尼

- 新加坡

- 馬來西亞

- 泰國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- 世界公司

- BlackBerry

- NXP Semiconductors

- Harman International

- Thales

- ARM

- Trend Micro

- Keysight Technologies

- Intertek

- T-Systems International

- KPIT Technologies

- Tata Elxsi

- 本地球員

- AUMOVIO

- Vector Informatik

- ETAS

- ASTEMO

- Autocrypt

- Secunet Security Networks

- Trustonic

- Device Authority

- WirelessCar

- 新興企業

- Upstream Security

- Trillium Secure

- Karamba Security

- Intertrust Technologies

- GuardKnox

The Global Connected Car Security Market was valued at USD 3.9 billion in 2025 and is estimated to grow at a CAGR of 13.6% to reach USD 13.8 billion by 2035.

The rapid adoption of connected car technologies has created an urgent need for robust cybersecurity across vehicle ecosystems, fleet management platforms, and cloud-connected services. Automakers and enterprises are increasingly embedding security features directly into vehicle electronic architectures, backend servers, and cloud platforms to reduce operational risks and reliance on manual monitoring. Continuous advancements in edge AI processors, V2X communications, and vehicle software platforms are enhancing the performance, scalability, and responsiveness of security solutions. Real-time intrusion detection, secure data exchange, and over-the-air updates are becoming standard to protect large vehicle fleets. Strategic alliances, mergers, and collaborations among automotive OEMs, cybersecurity providers, and cloud operators are accelerating the integration of security into the vehicle lifecycle, fleet operations, and mobility services. Connected car security is evolving from conventional monitoring to AI-powered, proactive threat analysis systems that safeguard software-defined vehicles and mobility platforms.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.9 Billion |

| Forecast Value | $13.8 Billion |

| CAGR | 13.6% |

The In-vehicle solutions segment held 64.8% share in 2025 and is expected to grow at a CAGR of 12.1% through 2035. These solutions provide embedded security across electronic control units, domain controllers, telematics modules, and infotainment systems, enabling real-time monitoring, intrusion prevention, and secure communications. OEMs prioritize in-vehicle security to meet regulatory and safety standards while ensuring vehicle systems are resilient to cyberattacks.

The network security segment accounted for 43.8% share in 2025 and is projected to grow at a CAGR of 12.8% from 2026 to 2035. Network security safeguards vehicle communication networks, in-vehicle data buses, and cloud connections against cyber threats, providing robust protocols, real-time monitoring, and breach mitigation. It remains a critical requirement for OEMs, fleet operators, and mobility service providers to maintain system integrity.

US Connected Car Security Market generated USD 1.4 billion in 2025, and continues to grow as automakers, fleet operators, and technology firms invest in advanced cybersecurity platforms. Companies deploy integrated hardware and software solutions to protect telematics, V2X communications, and in-vehicle networks, ensuring compliance with safety and regulatory requirements for both internal combustion and electric vehicles.

Leading players in the Global Connected Car Security Market include ARM, AUMOVIO, BlackBerry, Harman International, Intertek, Keysight Technologies, KPIT Technologies, NXP Semiconductors, Secunet Security Networks, and Thales. Companies in the Global Connected Car Security Market are strengthening their foothold by investing in AI-powered intrusion detection, over-the-air threat management, and secure vehicle software stacks. They are forming strategic partnerships with OEMs, mobility service providers, and cloud vendors to integrate security across vehicle lifecycles and connected platforms. Firms are prioritizing R&D for edge AI, V2X protection, and secure telematics modules while expanding global deployment of security solutions. Emphasis is placed on compliance with automotive cybersecurity regulations, predictive threat intelligence, and real-time network monitoring.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Security

- 2.2.3 Form

- 2.2.4 Solution

- 2.2.5 Vehicle

- 2.2.6 Propulsion

- 2.2.7 Application

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of connected and software-defined vehicles

- 3.2.1.2 Increasing cybersecurity threats targeting automotive systems

- 3.2.1.3 Regulatory mandates and safety standards

- 3.2.1.4 Growth of electric, autonomous, and shared mobility vehicles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complexity of securing heterogeneous vehicle architectures

- 3.2.2.2 Data privacy and cross-border regulatory compliance issues

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of security into vehicle software platforms and OTA ecosystems

- 3.2.3.2 Expansion of V2X, 5G, and cloud-based vehicle services

- 3.2.3.3 Rising adoption of hardware-based security solutions

- 3.2.3.4 Growing focus on autonomous driving and ADAS security

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.2 U.S. Department of Commerce / Bureau of Industry and Security (BIS)

- 3.4.1.3 Federal Trade Commission (FTC)

- 3.4.2 Europe

- 3.4.2.1 UNECE WP.29 Regulations (UN R155 & R156)

- 3.4.2.2 EN / ISO Automotive Standards

- 3.4.3 Asia Pacific

- 3.4.3.1 China National Standards for Vehicle Cybersecurity

- 3.4.3.2 India Automotive Standards (AIS 189 & AIS 190)

- 3.4.4 Latin America

- 3.4.4.1 Brazil: LGPD (Lei Geral de Protecao de Dados)

- 3.4.4.2 Mexico: NOM Standards

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE & Gulf States: IoT & V2X Security Policy

- 3.4.5.2 Saudi Arabia: SDAIA Automotive AI Framework

- 3.4.5.3 African Union (AU): Data Policy Framework

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing trend analysis

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Energy efficiency in production

- 3.10.3 Carbon footprint considerations

- 3.11 Data Governance, Cybersecurity, and Model Risk

- 3.11.1 Data Privacy and Compliance

- 3.11.2 Model Security

- 3.11.3 Operational and Systemic Risks

- 3.12 Security Architecture

- 3.12.1 Multi-layer Security Models

- 3.12.2 Vehicle-to-Everything (V2X) Security

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Security, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Endpoint security

- 5.3 Application security

- 5.4 Network security

- 5.5 Cloud security

Chapter 6 Market Estimates & Forecast, By Form, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 In-Vehicle Solutions

- 6.3 External Cloud Services

Chapter 7 Market Estimates & Forecast, By Solution, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Software

- 7.3 Hardware

- 7.3.1 Hardware security modules (HSM)

- 7.3.2 Secure microcontrollers

- 7.3.3 Trusted platform modules (TPM)

- 7.3.4 Secure gateways

- 7.3.5 Others

Chapter 8 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Hatchback

- 8.3 Sedan

- 8.4 SUV

Chapter 9 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 Internal combustion engine (ICE)

- 9.3 Electric vehicle

- 9.3.1 Battery electric vehicle (BEV)

- 9.3.2 Plug-in hybrid electric vehicle (PHEV)

- 9.3.3 Hybrid electric vehicle (HEV)

- 9.3.4 Fuel cell electric vehicle (FCEV)

Chapter 10 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 Telematics control units (TCUS)

- 10.3 Infotainment systems

- 10.4 Adas & autonomous driving systems

- 10.5 Communication modules

- 10.6 Others

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Nordics

- 11.3.7 Russia

- 11.3.8 Norway

- 11.3.9 Denmark

- 11.3.10 Netherlands

- 11.3.11 Belgium

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Vietnam

- 11.4.7 Indonesia

- 11.4.8 Singapore

- 11.4.9 Malaysia

- 11.4.10 Thailand

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global companies

- 12.1.1 BlackBerry

- 12.1.2 NXP Semiconductors

- 12.1.3 Harman International

- 12.1.4 Thales

- 12.1.5 ARM

- 12.1.6 Trend Micro

- 12.1.7 Keysight Technologies

- 12.1.8 Intertek

- 12.1.9 T-Systems International

- 12.1.10 KPIT Technologies

- 12.1.11 Tata Elxsi

- 12.2 Regional players

- 12.2.1 AUMOVIO

- 12.2.2 Vector Informatik

- 12.2.3 ETAS

- 12.2.4 ASTEMO

- 12.2.5 Autocrypt

- 12.2.6 Secunet Security Networks

- 12.2.7 Trustonic

- 12.2.8 Device Authority

- 12.2.9 WirelessCar

- 12.3 Emerging players

- 12.3.1 Upstream Security

- 12.3.2 Trillium Secure

- 12.3.3 Karamba Security

- 12.3.4 Intertrust Technologies

- 12.3.5 GuardKnox

互聯社區安全生態系統市場預測至2034年:按組件、部署模式、最終用戶和地區分類的全球分析

互聯社區安全生態系統市場預測至2034年:按組件、部署模式、最終用戶和地區分類的全球分析 汽車網路安全市場規模、佔有率和趨勢分析報告:按安全類型、車輛類型、服務、應用、地區和細分市場預測(2026-2033 年)

汽車網路安全市場規模、佔有率和趨勢分析報告:按安全類型、車輛類型、服務、應用、地區和細分市場預測(2026-2033 年) 汽車網路安全市場:按車輛類型、安全類型、部署模式、組件類型和最終用戶分類-2026-2032年全球市場預測

汽車網路安全市場:按車輛類型、安全類型、部署模式、組件類型和最終用戶分類-2026-2032年全球市場預測 汽車網路安全市場報告:按安全類型、形式、車輛類型、應用程式和地區分類(2026-2034 年)

汽車網路安全市場報告:按安全類型、形式、車輛類型、應用程式和地區分類(2026-2034 年) 2026年全球汽車網路安全市場報告

2026年全球汽車網路安全市場報告 汽車網路安全市場:按應用程式、安全類型和地區分類互聯行動安全解決方案市場預測至2034年:按產品類型、連接類型、技術、應用、最終用戶和地區分類的全球分析2026年全球外部雲端汽車保全服務市場報告

汽車網路安全市場:按應用程式、安全類型和地區分類互聯行動安全解決方案市場預測至2034年:按產品類型、連接類型、技術、應用、最終用戶和地區分類的全球分析2026年全球外部雲端汽車保全服務市場報告 汽車網路安全市場規模、佔有率、成長率和全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

汽車網路安全市場規模、佔有率、成長率和全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 汽車軟體開發與安全解決方案

汽車軟體開發與安全解決方案