|

市場調查報告書

商品編碼

1959286

發酵植物奶市場機會、成長要素、產業趨勢分析及2026年至2035年預測。Fermented Plant Milk Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

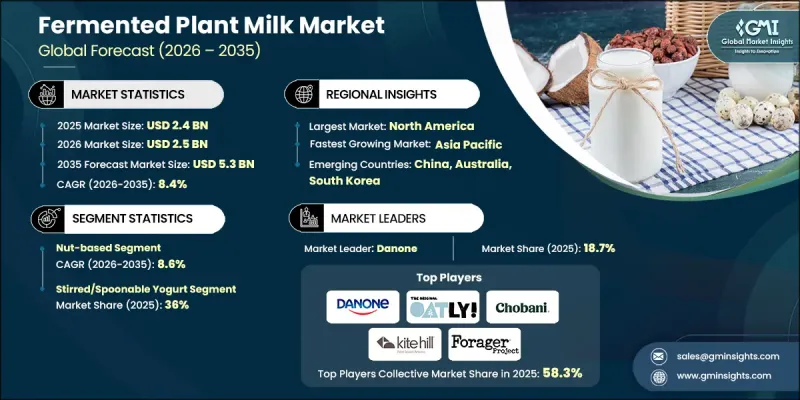

2025 年全球植物性發酵乳市場價值 24 億美元,預計到 2035 年將達到 53 億美元,年複合成長率為 8.4%。

這一強勁的成長勢頭凸顯了國際市場對發酵植物奶替代品日益成長的需求。發酵植物奶是指經過可控發酵製程的植物來源飲品,其目的是提高益生菌含量、豐富風味層次並提升整體營養價值。這些產品因其促進消化健康和提高營養物質生物利用度而廣受認可,使其成為傳統乳製品的理想替代品。乳糖不耐症和乳蛋白質過敏的日益普遍正在改變消費者的習慣,推動了植物來源替代品需求的成長。此外,出於倫理、環保和健康意識的驅動,全球純素和純素食者人數的持續成長也持續推動該品類的成長。發酵植物奶產品因其富含維生素、礦物質和有益菌等增強的營養成分而越來越受歡迎。全球對機能性食品和富含益生菌飲食的日益關注創造了巨大的市場機會。政府主導的旨在促進健康飲食習慣的營養政策也推動了市場需求。北美市場因消費者意識高和生產能力成熟而領先,而亞太地區是成長最快的地區,這得益於快速的都市化和日益增強的健康意識。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 24億美元 |

| 預測金額 | 53億美元 |

| 複合年成長率 | 8.4% |

預計到2025年,堅果類植物性飲品將佔據40.2%的市場佔有率,並在2035年之前以8.6%的複合年成長率成長。憑藉其高消費者接受度、均衡的營養成分和高階形象,該品類在更廣泛的植物性乳製品替代品行業中保持主導地位。其順滑的口感和適用於不同餐點的百搭特性,正不斷提升其在家庭中的滲透率。製造商持續將堅果發酵飲品定位為高價值產品,並投資於創新、包裝改進和配方最佳化,以保持競爭優勢。植物性飲食和特殊飲食模式的興起,進一步推動了注重健康的消費者對營養豐富、不含乳製品飲品的需求。

到2025年,即食優格將佔據發酵植物奶市場36%的佔有率。其濃郁的口感、便捷的食用方式以及適合全天不同場合的百搭特性,使其持續受到消費者的青睞。消費者越來越關注優格中的益生菌功效和功能性營養成分。優格的結構使其能夠添加額外的營養成分、活性乳酸菌以及不同的口味,從而吸引更廣泛的消費者群體。便利性以及消費者對消化和免疫健康益處的認知,持續推動優格在各個零售通路的強勁需求。

預計2026年至2035年,北美發酵植物奶市場將以8.4%的複合年成長率成長。該地區市場成長的主要驅動力是消費者對植物性營養益處的認知不斷提高,以及對無乳製品替代品的需求日益成長。發酵製程和產品開發技術的進步正在改善產品的口感、質地和營養價值,進一步加速其普及化。不斷擴大的零售分銷網路和強大的品牌策略也為該地區市場的持續擴張做出了貢獻。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 乳糖不耐症和乳製品過敏的發生率呈上升趨勢

- 純素和純素食者人數不斷增加

- 益生菌和機能性食品的需求日益成長

- 產業潛在風險與挑戰

- 高價產品與乳製品優格的比較

- 與口味和質地相關的挑戰

- 市場機遇

- 植物配方

- 蛋白質強化與營養強化產品

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按成分

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 公司矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依原料分類,2022-2035年

- 豆科植物

- 大豆

- 豌豆

- 羽扇豆

- 其他

- 堅果

- 杏仁

- 腰果

- 其他

- 穀物基

- 燕麥

- 米

- 其他

- 其他

第6章 市場估算與預測:依產品類型分類,2022-2035年

- 攪拌型優格/可以用湯匙吃的優格

- 希臘式優格/濃縮優格

- 飲用優格/優格飲料

- Kefir式發酵飲料

- 其他

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 直接消費

- 早餐和點心

- 外出時喝飲料

- 其他

- 烹飪和食品準備

- 烘焙和烹飪替代品

- 冰沙基底和飲料配料

- 其他

- 餐飲服務業/Horeka

- 飯店、餐廳、咖啡館

- 散裝包裝

- 工業/原料應用

- 麵包和糖果甜點

- 食品製造應用

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- Califia Farms

- Chobani

- Cocojune

- Daiya Foods

- Danone

- Forager Project

- Harmless Harvest

- Kite Hill

- Lavva

- Oatly

- Siggi's

- So Delicious Dairy Free

The Global Fermented Plant Milk Market was valued at USD 2.4 billion in 2025 and is estimated to grow at a CAGR of 8.4% to reach USD 5.3 billion by 2035.

The strong growth trajectory highlights the accelerating demand for fermented plant-based dairy alternatives across international markets. Fermented plant milk refers to plant-derived beverages that undergo controlled fermentation to enhance probiotic levels, improve flavor complexity, and elevate overall nutritional value. These products are widely recognized for supporting digestive health and offering improved nutrient bioavailability, making them a compelling alternative to traditional dairy products. Rising cases of lactose intolerance and milk protein sensitivities are reshaping consumption habits, encouraging consumers to seek plant-based substitutes. In addition, the steady expansion of vegan and vegetarian populations worldwide continues to fuel category growth, supported by ethical, environmental, and health-driven motivations. Fermented plant milk products are increasingly favored for their enriched profiles that include added vitamins, minerals, and beneficial cultures. The growing global focus on functional foods and probiotic-rich diets is creating substantial market opportunities. Government-backed nutrition initiatives promoting healthier eating frameworks are also contributing to demand. North America leads the market due to strong consumer awareness and well-established production capabilities, while Asia Pacific represents the fastest-growing region, supported by rapid urbanization and rising health consciousness.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.4 Billion |

| Forecast Value | $5.3 Billion |

| CAGR | 8.4% |

The nut-based segment accounted for 40.2% share in 2025 and is forecast to grow at a CAGR of 8.6% through 2035. This category maintains a leading position due to its strong consumer acceptance, balanced nutritional composition, and premium perception within the broader plant-based dairy alternatives industry. Its smooth consistency and adaptability across various meal occasions have strengthened its household penetration. Manufacturers continue to position nut-based fermented beverages as high-value offerings, often investing in innovation, packaging improvements, and enhanced formulations to sustain competitive advantage. The rise in plant-focused and specialty dietary patterns has further accelerated demand among health-conscious consumers seeking nutrient-dense and dairy-free beverage options.

The stirred and spoonable yogurt format captured 36% share in 2025 within the fermented plant milk market. This format remains highly popular because of its thick texture, convenience, and suitability for multiple consumption occasions throughout the day. Consumers are increasingly drawn to its probiotic benefits and functional nutrition profile. Its structure allows manufacturers to incorporate additional nutrients, live cultures, and flavor variations, making it attractive to a broad consumer base. The convenience factor, combined with the perception of digestive and immune health support, continues to drive strong demand for this segment across retail channels.

North America Fermented Plant Milk Market is anticipated to register a CAGR of 8.4% between 2026 and 2035. Market growth in the region is supported by rising awareness of plant-based nutrition benefits and increasing consumer preference for dairy-free alternatives. Technological progress in fermentation processes and product development techniques is enhancing taste, texture, and nutritional performance, further accelerating adoption. Expanding retail distribution networks and strong branding strategies are also contributing to sustained regional expansion.

Key companies operating in the Global Fermented Plant Milk Market include Danone, Oatly, Califia Farms, Kite Hill, Chobani, So Delicious Dairy Free, Lavva, Forager Project, Harmless Harvest, Cocojune, Siggi's, and Daiya Foods. These industry participants are actively competing through product differentiation, clean label positioning, and expansion into emerging markets. Companies in the Fermented Plant Milk Market are reinforcing their market position through continuous product innovation, strategic partnerships, and expansion of production capacities. Many players are investing heavily in research and development to enhance probiotic strains, improve taste profiles, and optimize nutritional content. Brand differentiation through clean label certifications, sustainable sourcing, and environmentally responsible packaging has become a central strategy. Firms are also leveraging mergers, acquisitions, and collaborations to broaden their geographic footprint and diversify product portfolios.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Raw material

- 2.2.3 Product format

- 2.2.4 End use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising lactose intolerance & dairy allergy prevalence

- 3.2.1.2 Growing vegan & vegetarian population

- 3.2.1.3 Increasing demand for probiotic & functional foods

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Higher price point vs. Dairy yogurt

- 3.2.2.2 Taste & texture challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Blended plant base formulations

- 3.2.3.2 Protein-enhanced & fortified products

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By raw material

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Raw Material, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Legume-based

- 5.2.1 Soy

- 5.2.2 Pea

- 5.2.3 Lupin

- 5.2.4 Others

- 5.3 Nut-based

- 5.3.1 Almond

- 5.3.2 Cashew

- 5.3.3 Others

- 5.4 Cereal-based

- 5.4.1 Oat

- 5.4.2 Rice

- 5.4.3 Others

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Product Format, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Stirred/spoonable yogurt

- 6.3 Greek-style/concentrated yogurt

- 6.4 Drinking/drinkable yogurt

- 6.5 Kefir-style cultured beverages

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Direct consumption

- 7.2.1 Breakfast & snacking

- 7.2.2 On-the-go beverages

- 7.2.3 Others

- 7.3 Culinary/cooking applications

- 7.3.1 Baking & cooking substitute

- 7.3.2 Smoothie base & beverage ingredient

- 7.3.3 Others

- 7.4 Food service/HoReCa

- 7.4.1 Hotels, restaurants & cafes

- 7.4.2 Bulk packaging

- 7.5 Industrial/ingredient use

- 7.5.1 Bakery & confectionery

- 7.5.2 Food manufacturing applications

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Califia Farms

- 9.2 Chobani

- 9.3 Cocojune

- 9.4 Daiya Foods

- 9.5 Danone

- 9.6 Forager Project

- 9.7 Harmless Harvest

- 9.8 Kite Hill

- 9.9 Lavva

- 9.10 Oatly

- 9.11 Siggi's

- 9.12 So Delicious Dairy Free