|

市場調查報告書

商品編碼

1936679

施工機械市場機會、成長要素、產業趨勢分析及2026年至2035年預測Construction Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

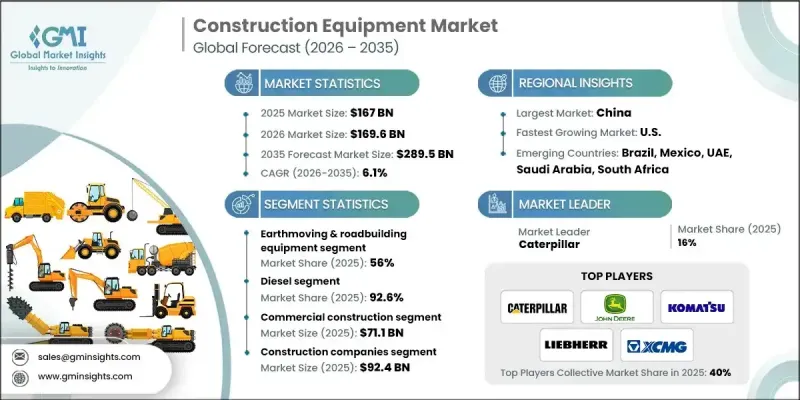

全球施工機械市場預計到 2025 年將達到 1,670 億美元,到 2035 年將達到 2,895 億美元,年複合成長率為 6.1%。

市場擴張的驅動力主要來自基礎設施和建築業作為經濟發展引擎的重要性,以及政府對大型公共基礎設施計劃的投資不斷增加。快速的都市化、日益成長的工業化以及對先進交通網路需求的不斷成長,都催生了對先進施工機械的強勁需求。智慧施工解決方案和數位化整合等技術創新正在透過提高工作效率、精度和安全性,改變工程機械的運作方式。自動化、遠端資訊處理和人工智慧輔助設備的日益普及,以及設備製造商和技術供應商之間的策略聯盟,正在加速整個產業的數位轉型。此外,施工機械租賃服務的擴展,使得高階設備更容易獲得,並促進了其在新興市場的應用。整體而言,由於建設活動的增加、技術的進步以及政府主導的各項舉措,市場呈現強勁成長動能。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 起始值 | 2895億美元 |

| 預測金額 | 2895億美元 |

| 複合年成長率 | 6.1% |

預計到2025年,土木工程和施工機械領域將佔據56%的市場佔有率,並在2035年之前以5.5%的複合年成長率成長。由於大規模基礎設施計劃和不斷擴展的道路網路,挖土機、後鏟挖土機、裝載機和壓路機等機械的需求預計將持續旺盛。政府致力於改善都市區和偏遠地區的連結性和可及性,從而持續推動對高品質機械的需求。此外,正在進行的公共工程項目也需要專用設備進行精準的土木工程和建築作業,這進一步促進了該領域的成長。該領域的領先地位凸顯了道路建設和基礎設施發展在推動施工機械市場發展方面發揮的核心作用。

2025年,柴油引擎設備市佔率佔比高達92.6%,預計2026年至2035年將以5.6%的複合年成長率成長。製造商正將先進技術融入柴油引擎,以提高燃油效率、減少排放氣體並提升機器的整體性能。遠端資訊處理技術的整合,結合了GPS追蹤、車載診斷和遠端監控,實現了即時效能分析和預測性維護。租賃公司和承包商正擴大採用配備遠端資訊處理技術的設備來管理車隊、最佳化營運效率並減少停機時間。基於雲端的解決方案使操作人員能夠監控設備、追蹤使用情況並制定維護計劃,使柴油動力機械對大型計劃和租賃業務更具吸引力。

預計2025年,中國施工機械市場將佔據全球50%的市場佔有率,市場規模達387億美元。該地區的成長主要得益於快速的都市化、工業擴張以及為應對不斷上漲的人事費用而日益普及的施工機械租賃模式。中國製造商和租賃業者正優先發展技術先進、自動化程度高、燃油效率高且具備遠端資訊處理功能的工程機械,以吸引承包商和大型基礎設施開發商。不斷成長的基礎設施投資與經濟高效的租賃解決方案相結合,正在增強市場需求,並推動高性能施工機械在全部區域的普及。

目錄

第1章調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 都市化和基礎設施發展

- 政府加大對智慧城市和公共工程的投資

- 技術進步

- 向電動和混合動力施工機械的過渡

- 租賃市場快速成長

- 產業潛在風險與挑戰

- 高昂的資本和維護成本

- 原物料價格波動

- 熟練操作人員短缺

- 監管和排放氣體合規要求

- 來自租賃和二手設備的激烈競爭

- 市場機遇

- 加速電動和混合動力設備的引入

- 自主建造與人工智慧融合

- 精密施工技術及GPS導

- 設備即服務經營模式(EaaS)

- 傳統設備改造與升級市場

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 美國環保署(EPA)

- 加拿大標準協會,CSA C225-00

- 歐洲

- 歐洲施工機械委員會(CECE)

- 施工機械標準與法規委員會(CESRC)

- 建築產品法規(歐盟 2011/305)(CPR)

- 亞太地區

- ICEMA-印度施工機械製造商協會

- 中國施工機械工業協會(CCMA)

- 國際清潔交通委員會

- 拉丁美洲

- 智利建設業協會(CChC)

- 國際清潔交通委員會(ICCT)

- 巴西監管標準(NR)

- 中東和非洲

- ASTM國際標準

- 總統令第7/11號

- 駕駛機器規則

- 北美洲

- 波特五力分析

- PESTEL 分析

- 專利分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 成本細分分析

- 原料成本

- 動力傳動系統與推進系統成本

- 液壓和機械系統成本

- 電氣和電子元件成本

- 製造和組裝成本

- 生產統計

- 生產基地

- 進出口

- 主要進口國

- 永續性和環境方面

- 永續努力

- 減少廢棄物策略

- 生產中的能源效率

- 環保措施

- 碳足跡考量

- 客戶和需求側智慧

- 買房還是租房子的抉擇

- 總擁有成本 (TCO) 考量

- 品牌忠誠度與價格敏感度

- 更新週期和車隊更新趨勢

- 供需缺口及運轉率分析

- 運轉率(OEM 與本地製造商)

- 供需不符熱點地區

- 短期和長期產能展望

- 售後市場與生命週期收入分析

- 零件和業務收益分成

- 維護合約和服務商品搭售

- 數位服務貨幣化

- 對OEM利潤率的影響

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 企業擴張計畫和資金籌措

第5章 2022-2034年按產品分類的市場估算與預測

- 土木工程及道路施工機械

- 後鏟

- 挖土機

- 裝載機

- 壓實設備

- 其他

- 物料輸送和起重機

- 倉儲及運輸設備

- 工程系統

- 工業車輛

- 散裝物料輸送設備

- 混凝土設備

- 混凝土泵

- 破碎機

- 運輸攪拌車

- 瀝青鋪築機

- 混凝土攪拌站

6. 2022-2034年按推進方式分類的市場估計與預測

- 柴油引擎

- CNG/LNG

- 電的

第7章 按應用領域分類的市場估算與預測,2022-2034年

- 住宅

- 商業建築

- 工業建築

- 採礦和採石

8. 依最終用途分類的市場估計與預測,2022-2034 年

- 建設公司

- 礦業營運商

- 租賃公司

- 政府/市政當局

- 工業用戶

第9章 2022-2034年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 丹麥

- 芬蘭

- 挪威

- 瑞典

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ANZ

- 新加坡

- 泰國

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 世界玩家

- Caterpillar

- Komatsu

- John Deere

- Volvo

- Liebherr

- Hitachi

- JCB

- Sany

- 區域冠軍公司

- Case

- New Holland

- Doosan

- Hyundai

- XCMG

- Zoomlion

- Terex

- Manitou

- Wacker Neuson

- 新興企業和服務供應商

- United Rentals

- Ashtead/Sunbelt Rentals

- H&E Equipment Services

- Home Depot Tool Rental

- Built Robotics

- SafeAI

- Trimble

- Topcon

The Global Construction Equipment Market was valued at USD 167 billion in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 289.5 billion by 2035.

Market expansion is fueled by the critical role of infrastructure and construction in driving economic development, alongside significant government investments in large-scale public infrastructure projects. Rapid urbanization, increasing industrialization, and rising demand for improved transportation networks are creating strong demand for advanced construction machinery. Technological innovations, including smart construction solutions and digital integration, are transforming operations, enabling improved productivity, precision, and safety. The rising adoption of automation, telematics, and AI-assisted equipment, coupled with strategic partnerships among equipment manufacturers and technology providers, is accelerating the digital shift across the sector. Additionally, growing rental services for construction machinery are making high-end equipment more accessible, enhancing market penetration in emerging economies. Overall, the market is witnessing robust growth driven by increasing construction activity, technological evolution, and government-backed initiatives.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $289.5 Billion |

| Forecast Value | $289.5 Billion |

| CAGR | 6.1% |

The earthmoving and road-building equipment segment held 56% share in 2025 and is expected to grow at a CAGR of 5.5% through 2035. Equipment such as excavators, backhoes, loaders, and compactors is experiencing high demand due to large-scale infrastructure projects and road network expansions. Governments' focus on improving connectivity and accessibility in urban and remote regions is creating sustained demand for high-quality machinery. The segment's growth is further supported by ongoing public works programs, which require specialized equipment for precise earthmoving and construction operations. This segment's dominance underscores the central role of road-building and infrastructure development in driving the construction equipment market.

The diesel-powered equipment segment held a 92.6% share in 2025 and is forecasted to grow at a CAGR of 5.6% from 2026 to 2035. Manufacturers are incorporating advanced technologies in diesel engines to improve fuel efficiency, reduce emissions, and enhance overall machine performance. Integration of telematics, combining GPS tracking, onboard diagnostics, and remote monitoring, is allowing real-time performance analysis and predictive maintenance. Rental companies and contractors are increasingly adopting telematics-enabled equipment for fleet management, optimizing operational efficiency and reducing downtime. Cloud-based solutions allow operators to monitor machinery, track usage, and plan maintenance schedules, reinforcing the appeal of diesel-powered machines in both large-scale projects and rental operations.

China Construction Equipment Market held 50% share in 2025, generating USD 38.7 billion in 2025. The region's growth is driven by rapid urbanization, industrial expansion, and the rising adoption of construction equipment rental models to offset labor cost increases. Chinese manufacturers and rental providers are emphasizing technologically advanced machinery with enhanced automation, fuel efficiency, and telematics integration to attract contractors and large-scale infrastructure developers. The combination of rising infrastructure investments and cost-effective rental solutions is strengthening market demand and driving the adoption of high-performance construction equipment throughout the region.

Key players operating in the Global Construction Equipment Market include Caterpillar, CNH Industrial, Deere & Co., Doosan, Hitachi Construction Machinery, Komatsu, Liebherr, Sany, Terex, Volvo, and XCMG. Companies in the construction equipment market are adopting multiple strategies to consolidate their presence and expand market share. These include investing heavily in R&D to develop smart, energy-efficient, and telematics-enabled machinery. Firms are entering strategic partnerships with technology providers to integrate AI, IoT, and automation into their products. Expanding service networks and rental solutions enhance accessibility, particularly in emerging markets. Companies are also pursuing mergers and acquisitions to strengthen their global footprint, optimize supply chains, and gain access to new customer bases.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Propulsion

- 2.2.4 Application

- 2.2.5 End use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Urbanization and infrastructure development

- 3.2.1.2 Rising government investments in smart cities & public works

- 3.2.1.3 Technological advancements

- 3.2.1.4 Shift toward electric and hybrid construction equipment

- 3.2.1.5 Rental and leasing boom

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital and maintenance costs

- 3.2.2.2 Volatility in raw material prices

- 3.2.2.3 Shortage of skilled operators

- 3.2.2.4 Regulatory and emission compliance requirements

- 3.2.2.5 Intense competition from rental and used equipment

- 3.2.3 Market opportunities

- 3.2.3.1 Electric & Hybrid Equipment Adoption Acceleration

- 3.2.3.2 Autonomous Construction Operations & AI Integration

- 3.2.3.3 Precision Construction Technology & GPS Guidance

- 3.2.3.4 Equipment-as-a-Service (EaaS) Business Models

- 3.2.3.5 Retrofit & Upgrade Market for Legacy Equipment

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Environmental Protection Agency (EPA)

- 3.4.1.2 Canadian Standards Association, CSA C225-00

- 3.4.2 Europe

- 3.4.2.1 Committee for European Construction Equipment (CECE)

- 3.4.2.2 Construction Equipment Standards and Regulations Committee (CESRC)

- 3.4.2.3 Construction Products Regulation (EU 2011/305) (CPR)

- 3.4.3 Asia Pacific

- 3.4.3.1 ICEMA - Indian Construction Equipment Manufacturers’ Association

- 3.4.3.2 China Construction Machinery Association (CCMA)

- 3.4.3.3 The International Council on Clean Transportation

- 3.4.4 Latin America

- 3.4.4.1 Chilean Construction Chamber (CChC)

- 3.4.4.2 International Council on Clean Transportation (ICCT)

- 3.4.4.3 Brazilian Regulatory Standards (NR)

- 3.4.5 MEA

- 3.4.5.1 ASTM international standards

- 3.4.5.2 Presidential Legislative Decree 7/11

- 3.4.5.3 Driven machinery regulations

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Patent analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By product

- 3.10 Cost breakdown analysis

- 3.10.1 Raw material costs

- 3.10.2 Powertrain & propulsion system costs

- 3.10.3 Hydraulic & mechanical system costs

- 3.10.4 Electrical & electronic component costs

- 3.10.5 Manufacturing & assembly costs

- 3.11 Production statistics

- 3.11.1 Production hubs

- 3.11.2 Import and export

- 3.11.3 Major import countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Customer & demand-side intelligence

- 3.13.1 Purchase vs rental decision drivers

- 3.13.2 Total cost of ownership (TCO) considerations

- 3.13.3 Brand loyalty vs price sensitivity

- 3.13.4 Replacement cycle & fleet renewal trends

- 3.14 Demand-supply gap & capacity utilization analysis

- 3.14.1 Capacity utilization rates (OEM vs regional players)

- 3.14.2 Demand-supply mismatch hotspots

- 3.14.3 Short-term vs long-term capacity outlook

- 3.15 Aftermarket & Lifecycle Revenue Analysis

- 3.15.1 Parts & service revenue share

- 3.15.2 Maintenance contracts & service bundling

- 3.15.3 Digital service monetization

- 3.15.4 Impact on OEM margins

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Earthmoving & roadbuilding equipment

- 5.2.1 Backhoe

- 5.2.2 Excavator

- 5.2.3 Loader

- 5.2.4 Compaction equipment

- 5.2.5 Others

- 5.3 Material handling and cranes

- 5.3.1 Storage and handling equipment

- 5.3.2 Engineered systems

- 5.3.3 Industrial trucks

- 5.3.4 Bulk material handling equipment

- 5.4 Concrete equipment

- 5.4.1 Concrete pumps

- 5.4.2 Crusher

- 5.4.3 Transit mixers

- 5.4.4 Asphalt pavers

- 5.4.5 Batching plants

Chapter 6 Market Estimates & Forecast, By Propulsion, 2022 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Diesel

- 6.3 CNG/LNG

- 6.4 Electric

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Residential construction

- 7.3 Commercial construction

- 7.4 Industrial construction

- 7.5 Mining & quarrying

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Construction companies

- 8.3 Mining operators

- 8.4 Rental companies

- 8.5 Government & municipalities

- 8.6 Industrial users

Chapter 9 Market Estimates & Forecast, By Region, 2022-2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Denmark

- 9.3.8 Finland

- 9.3.9 Norway

- 9.3.10 Sweden

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Singapore

- 9.4.7 Thailand

- 9.4.8 Indonesia

- 9.4.9 Vietnam

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Caterpillar

- 10.1.2 Komatsu

- 10.1.3 John Deere

- 10.1.4 Volvo

- 10.1.5 Liebherr

- 10.1.6 Hitachi

- 10.1.7 JCB

- 10.1.8 Sany

- 10.2 Regional Champions

- 10.2.1 Case

- 10.2.2 New Holland

- 10.2.3 Doosan

- 10.2.4 Hyundai

- 10.2.5 XCMG

- 10.2.6 Zoomlion

- 10.2.7 Terex

- 10.2.8 Manitou

- 10.2.9 Wacker Neuson

- 10.3 Emerging Players & Service Providers

- 10.3.1 United Rentals

- 10.3.2 Ashtead / Sunbelt Rentals

- 10.3.3 H&E Equipment Services

- 10.3.4 Home Depot Tool Rental

- 10.3.5 Built Robotics

- 10.3.6 SafeAI

- 10.3.7 Trimble

- 10.3.8 Topcon

施工機械市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、功率、應用、終端用戶產業、地區和競爭格局分類,2021-2031年

施工機械市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、功率、應用、終端用戶產業、地區和競爭格局分類,2021-2031年 施工機械市場規模、佔有率、趨勢和預測:按解決方案類型、機器類型、應用、行業和地區分類,2026-2034年

施工機械市場規模、佔有率、趨勢和預測:按解決方案類型、機器類型、應用、行業和地區分類,2026-2034年 2026年全球挖溝機市場報告2026年全球施工機械售後市場報告2026年全球水泥和砂漿測試設備市場報告

2026年全球挖溝機市場報告2026年全球施工機械售後市場報告2026年全球水泥和砂漿測試設備市場報告 施工機械市場:2026-2032年全球市場預測(依產品類型、功率輸出、燃料類型、設計類型、運作小時數、銷售管道和最終用戶分類)橡膠壓機市場:依橡膠類型、壓機類型、操作模式、產能、應用及通路分類-全球預測,2026-2032年電動施工機械市場:依設備類型、推進系統和應用分類-全球預測,2026-2032年自動液壓機市場:按壓機類型、控制類型、操作模式和終端用戶產業分類,全球預測,2026-2032年

施工機械市場:2026-2032年全球市場預測(依產品類型、功率輸出、燃料類型、設計類型、運作小時數、銷售管道和最終用戶分類)橡膠壓機市場:依橡膠類型、壓機類型、操作模式、產能、應用及通路分類-全球預測,2026-2032年電動施工機械市場:依設備類型、推進系統和應用分類-全球預測,2026-2032年自動液壓機市場:按壓機類型、控制類型、操作模式和終端用戶產業分類,全球預測,2026-2032年 2026 年至 2035 年施工機械輪胎市場的商業機會、成長要素、產業趨勢分析與預測。

2026 年至 2035 年施工機械輪胎市場的商業機會、成長要素、產業趨勢分析與預測。