|

市場調查報告書

商品編碼

1936654

聚丙烯醯胺市場機會、成長要素、產業趨勢分析及2026年至2035年預測Polyacrylamide Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

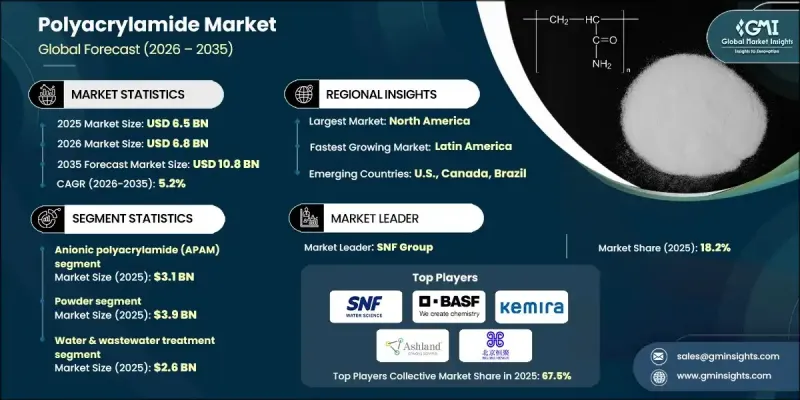

全球聚丙烯醯胺市場預計到 2025 年將達到 65 億美元,到 2035 年將達到 108 億美元,年複合成長率為 5.2%。

受水處理和污水管理系統技術的進步推動,市場正經歷顯著擴張。快速的都市化、日益嚴格的環境法規以及對高效水資源管理解決方案不斷成長的需求,促使各國政府和企業對市政和工業水處理基礎設施進行大規模投資。聚丙烯醯胺作為高性能凝聚劑,在污泥脫水、固液分離和廢水淨化方面發揮關鍵作用。對水質和法規遵循的長期承諾持續推動市場需求。此外,採礦和紡織等行業的成長也促進了市場擴張。在採礦業,聚丙烯醯胺有助於尾礦管理和水資源回收,從而提高營運效率和資源利用率。在紡織業,它支持上漿、染色和污水處理等工藝,契合了人們對永續生產和廢水管理日益成長的關注。總而言之,監管力道的加大和工業用水量的增加,持續為全球聚丙烯醯胺市場創造強勁的成長機會。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 65億美元 |

| 預測金額 | 108億美元 |

| 複合年成長率 | 5.2% |

陰離子聚丙烯醯胺(APAM)市場預計到2025年將達到31億美元,主要得益於其在市政和工業污水處理、採礦製程以及石油開採等領域的廣泛應用。 APAM具有絮凝效率高、成本效益好以及符合監管要求等優點,使其成為大規模固液分離和廢水處理的首選材料,尤其是在環境法規嚴格的地區。在用水量大的工業領域持續使用,進一步鞏固了其在產品組合中的主導地位。

預計2025年,水和污水處理市場規模將達26億美元,預測期內複合年成長率(CAGR)為4.7%。聚丙烯醯胺在該領域發揮重要作用,尤其是在市政和工業污水處理廠的絮凝、污泥處理和固液分離方面,因此受益匪淺。都市化加快、廢水法規日益嚴格以及處理基礎設施的現代化,正在推動該領域的成長。市場對高效且價格合理的水處理解決方案的需求,將確保成熟市場和新興市場都能保持持續的高銷售量。

預計到2025年,北美聚丙烯醯胺市場將佔據20%的佔有率,其中美國將貢獻該地區的大部分收入。該地區的成長得益於完善的水處理基礎設施和強勁的油氣產業。嚴格的污水排放環境法規、市政污水處理廠的廣泛應用以及聚合物在石油開採中的重要作用是推動市場需求的主要因素。北美市場已趨於成熟,預計在持續的基礎設施投資和高品質水處理解決方案日益普及的推動下,該市場將保持穩定成長。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 全球推廣先進的廢棄物處理和處置技術

- 採礦和紡織業的趨勢

- 頁岩氣和緻密油產量不斷成長

- 產業潛在風險與挑戰

- 原物料價格波動

- 對殘留單體實施嚴格監管

- 與丙烯醯胺毒性相關的環境問題

- 市場機遇

- 水處理應用需求不斷成長

- 提高石油採收率(EOR)和採礦擴張

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 產品類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計(HS編碼)(註:僅提供主要國家的貿易統計)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續努力

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 依產品類型分類的市場估算與預測,2022-2035年

- 陰離子聚丙烯醯胺(APAM)

- 陽離子聚丙烯醯胺(CPAM)

- 非離子型聚丙烯醯胺(NPAM)

- 兩性聚丙烯醯胺

- 其他

第6章 按類型分類的市場估算與預測,2022-2035年

- 粉末

- 乳液

- 液體

- 其他

第7章 按應用領域分類的市場估算與預測,2022-2035年

- 水和污水處理

- 提高石油採收率(EOR)

- 採礦和礦物加工

- 農業

- 纖維和染色

- 化妝品和個人護理

- 其他

第8章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- SNF Group

- Kemira Oyj

- BASF SE

- Ashland Global Holdings Inc.

- NNA Polymers, Inc.

- Wego Chemical Group Inc.

- Catalynt Solutions, Inc.

- Chinafloc Chemical Co. Ltd

- Henan Hangrui Environmental Protection Technology

- Shandong Shuiheng Chemical Co. Ltd

- Anhui Tianrun Chemicals Co. Ltd

- Zibo East Polymer Co. Ltd

- Welldone Chemical Group

- Henan Secco Environmental Protection Tech Co. Ltd

- Beijing Hengju Chemical Group Co., Ltd.

The Global Polyacrylamide Market was valued at USD 6.5 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 10.8 billion by 2035.

The market is experiencing significant expansion, driven by advancements in water treatment and wastewater management systems. Rapid urbanization, stricter environmental regulations, and the need for efficient water management solutions are encouraging governments and industries to invest heavily in municipal and industrial water treatment infrastructure. Polyacrylamide, a high-performance flocculant, plays a vital role in these systems by aiding sludge dewatering, solid-liquid separation, and effluent purification. Long-term commitments to water quality and regulatory compliance are continuously driving demand. Furthermore, growth in sectors such as mining and textiles is expanding the market footprint. In mining operations, polyacrylamide supports tailings management and water recovery, improving operational efficiency and resource utilization. In the textile industry, it assists in processes like sizing, dyeing, and wastewater treatment, aligning with the growing emphasis on sustainable production and effluent management. Overall, increasing regulatory enforcement and industrial water consumption continue to create strong growth opportunities for polyacrylamide globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.5 Billion |

| Forecast Value | $10.8 Billion |

| CAGR | 5.2% |

The anionic polyacrylamide (APAM) segment reached USD 3.1 billion in 2025. Its widespread adoption in municipal and industrial wastewater treatment, mining processes, and oil recovery applications is a key driver. High flocculation efficiency, cost-effectiveness, and regulatory compliance make APAM the preferred choice for large-scale solid-liquid separation and effluent management, particularly in regions with stringent environmental laws. The polymer's continued use in water-intensive industries strengthens its dominance within the product mix.

The water and wastewater treatment segment was valued at USD 2.6 billion in 2025 and is estimated to grow at a CAGR of 4.7% during the forecast period. As the primary application of polyacrylamide, this segment benefits from its critical role in flocculation, sludge handling, and solid-liquid separation in municipal and industrial plants. Rising urbanization, regulatory oversight of effluent discharge, and upgrades in treatment infrastructure reinforce the segment's growth potential. The demand for effective, affordable water treatment solutions ensures sustained high-volume sales in both mature and emerging markets.

North America Polyacrylamide Market accounted for 20% share in 2025, with the majority of regional revenue coming from the United States. Growth in this region is supported by extensive water treatment infrastructure and a robust oil and gas sector. Stringent environmental regulations on wastewater discharge, widespread use in municipal purification facilities, and polymers' role in oil recovery are key factors driving demand. North America is a mature market offering stable growth due to continuous infrastructure investment and increasing adoption of high-quality water treatment solutions.

Key players operating in the Global Polyacrylamide Market include Chinafloc Chemical Co. Ltd, BASF SE, SNF Group, Anhui Tianrun Chemicals Co. Ltd, Henan Hangrui Environmental Protection Technology, Kemira Oyj, Ashland Global Holdings Inc., Beijing Hengju Chemical Group Co., Ltd., Wego Chemical Group Inc., Catalynt Solutions, Inc., Shandong Shuiheng Chemical Co. Ltd, Zibo East Polymer Co. Ltd, NNA Polymers, Inc., Henan Secco Environmental Protection Tech Co. Ltd, and Welldone Chemical Group. To strengthen their position, companies in the polyacrylamide industry are focusing on several strategic initiatives. They are investing in R&D to produce more efficient, environmentally friendly, and cost-effective polymers. Strategic partnerships, mergers, and acquisitions allow them to expand geographically and gain access to new customer segments. Firms are adopting advanced manufacturing technologies to improve quality and operational efficiency while reducing production costs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Form

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Global advent of advanced waste treatment & disposal technologies

- 3.2.1.2 Developments across mining & textile industries

- 3.2.1.3 Expansion of shale gas & tight oil production

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatile raw material prices

- 3.2.2.2 Stringent residual monomer regulations

- 3.2.2.3 Environmental concerns over acrylamide toxicity

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand in water treatment applications

- 3.2.3.2 Expansion in enhanced oil recovery (EOR) and mining

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Anionic polyacrylamide (APAM)

- 5.3 Cationic polyacrylamide (CPAM)

- 5.4 Non-ionic polyacrylamide (NPAM)

- 5.5 Amphoteric polyacrylamide

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Form, 2022 - 2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Powder

- 6.3 Emulsion

- 6.4 Liquid

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Water & wastewater treatment

- 7.3 Enhanced oil recovery (EOR)

- 7.4 Mining & mineral processing

- 7.5 Agriculture

- 7.6 Textiles & dyeing

- 7.7 Cosmetics & personal care

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 SNF Group

- 9.2 Kemira Oyj

- 9.3 BASF SE

- 9.4 Ashland Global Holdings Inc.

- 9.5 NNA Polymers, Inc.

- 9.6 Wego Chemical Group Inc.

- 9.7 Catalynt Solutions, Inc.

- 9.8 Chinafloc Chemical Co. Ltd

- 9.9 Henan Hangrui Environmental Protection Technology

- 9.10 Shandong Shuiheng Chemical Co. Ltd

- 9.11 Anhui Tianrun Chemicals Co. Ltd

- 9.12 Zibo East Polymer Co. Ltd

- 9.13 Welldone Chemical Group

- 9.14 Henan Secco Environmental Protection Tech Co. Ltd

- 9.15 Beijing Hengju Chemical Group Co., Ltd.

2026年全球聚丙烯醯胺市場報告

2026年全球聚丙烯醯胺市場報告 聚丙烯醯胺奈米球市場:依合成方法、粒徑、分子量、應用及通路-2026-2032年全球預測聚丙烯醯胺市場(造紙用):依離子電荷、分子量、形態、應用和最終用途分類,全球預測(2026-2032年)

聚丙烯醯胺奈米球市場:依合成方法、粒徑、分子量、應用及通路-2026-2032年全球預測聚丙烯醯胺市場(造紙用):依離子電荷、分子量、形態、應用和最終用途分類,全球預測(2026-2032年) 聚丙烯醯胺:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

聚丙烯醯胺:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 聚丙烯醯胺市場-2026-2031年預測

聚丙烯醯胺市場-2026-2031年預測 濕強樹脂的全球市場:各類型樹脂,各用途 - 產業動態,市場規模,機會分析,預測(2025年~2033年)聚丙烯醯胺市場規模(按類型、應用、地區、範圍和預測)

濕強樹脂的全球市場:各類型樹脂,各用途 - 產業動態,市場規模,機會分析,預測(2025年~2033年)聚丙烯醯胺市場規模(按類型、應用、地區、範圍和預測) 全球聚丙烯醯胺市場(2025年)

全球聚丙烯醯胺市場(2025年) 聚丙烯醯胺(PAM)全球市場需求、預測分析(2018-2034)

聚丙烯醯胺(PAM)全球市場需求、預測分析(2018-2034) 聚丙烯醯胺市場:全球2025-2029

聚丙烯醯胺市場:全球2025-2029