|

市場調查報告書

商品編碼

1936630

2026年至2035年花卉市場機會、成長要素、產業趨勢分析及預測Floriculture Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

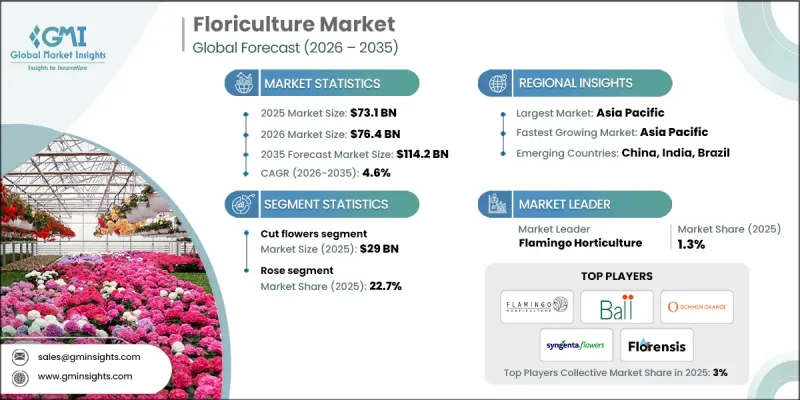

全球園藝市場預計到 2025 年將達到 731 億美元,到 2035 年將達到 1,142 億美元,年複合成長率為 4.6%。

市場成長的促進因素包括觀賞植物需求的增加、可支配收入的提高以及鮮花在禮品贈送、活動策劃、園林綠化和室內裝飾等領域日益普及。園藝產業涵蓋新鮮切花、盆栽植物、苗圃和觀賞植物的種植,已發展成為一個高度商業化和出口導向的產業。都市化、生活方式的改變以及有組織的零售和電子商務平台的擴張,導致已開發經濟體和新興經濟體的鮮花消費量顯著成長。此外,溫室栽培、精準灌溉和採後後處理等技術的進步,提高了鮮花的產量、品質、保存期限和全年供應,從而支撐了市場的持續成長。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 731億美元 |

| 預測金額 | 1142億美元 |

| 複合年成長率 | 4.6% |

鮮花在婚禮、節日慶典、企業活動和酒店等場所的日益普及,進一步支撐了市場需求,因為在這些場合,鮮花的美學價值扮演著至關重要的角色。人們對鮮花帶來的情感和心理益處的認知不斷提高,以及鮮花在住宅裝飾和健康空間中應用的日益廣泛,都對消費者需求產生了積極影響。出口導向生產基地也受惠於低溫運輸基礎設施的完善和國際貿易協定,使生產商能夠進入高附加價值的全球市場。永續性舉措,例如環保種植方式和減少化學品使用,正變得越來越重要,尤其是在那些為具有環保意識的消費者提供優質園藝產品的地區。

按產品類型分類,鮮切花市場預計到2025年將創造290億美元的收入,佔總收入的最大佔有率。玫瑰、菊花、康乃馨、百合和非洲菊等鮮切花廣泛用於禮物、裝飾和慶祝用途,全年需求穩定。鮮切花具有巨大的出口潛力、較高的利潤率以及廣泛的跨文化接受度,使其成為最具商業性價值的細分市場。育種技術、可控環境農業和物流的進步顯著提高了鮮花的品質和瓶插壽命,進一步鞏固了鮮切花在國內外市場的主導地位。

2025年,B2B領域佔最大佔有率,主要得益於批發商、出口商、活動組織者、飯店、企業辦公室、超級市場和園林綠化承包商的強勁需求。這些買家批量採購鮮花和觀賞植物,以滿足持續的商業用途,因此B2B貿易成為花卉供應鏈的基礎。該領域依賴長期供應協議、集中競標和有組織的批發市場,以確保品質穩定、價格穩定和及時交付。對低溫運輸物流和合約種植的日益依賴進一步強化了B2B運營,實現了全年供應並減少了採後損失。

預計到2025年,美國園藝市場將佔80%的市場佔有率,市場規模達111億美元。北美園藝市場的發展得益於美國和加拿大消費者對觀賞植物和鮮切花的強勁需求,尤其是在情人節和母親節等節日期間。鮮花作為禮品和家居裝飾品依然廣受歡迎,這些節日也持續推動著鮮花的銷售。先進的溫室技術使北美種植者能夠全年培育高品質的花卉和植物。這種能力不僅確保了穩定的供應,也使零售商和線上花店能夠獲得遠高於國際市場的利潤率,這反映了其卓越的品質和持續的消費者需求。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 產業影響因素

- 促進要素

- 消費者對觀賞植物的需求不斷成長

- 擴展送禮文化

- 人們越來越關注健康和保健

- 拓展電子商務與數位平台

- 產業潛在風險與挑戰

- 產品新鮮度保持

- 來自人造花卉產品的競爭日益加劇

- 機會

- 永續性與生態創新的商業化

- 引進精密農業和人工智慧驅動的物流

- 促進要素

- 成長潛力分析

- 關鍵市場趨勢與顛覆性因素

- 未來市場趨勢

- 風險及緩解分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 監管環境

- 標準和合規要求

- 認證標準

- 消費者購買行為分析

- 購買模式

- 偏好分析

- 消費行為的區域差異

- 電子商務如何影響購買決策

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 依產品類型分類的市場估算與預測,2022-2035年

- 鮮切花

- 盆栽植物

- 盆栽植物

- 室內植物

- 其他

第6章 按花卉類型分類的市場估算與預測,2022-2035年

- 玫瑰

- 菊花

- 鬱金香

- 百合

- 非洲菊

- 康乃馨

- 德克薩斯藍鈴花

- 小蒼蘭

- 繡球花

- 其他

7. 2022-2035年按分銷管道分類的市場估算與預測

- B to B

- B to C

- 線上

- 離線

第8章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 馬來西亞

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Beekenkamp Group

- Danziger

- Dummen Orange

- Esmeralda Farms

- Flamingo Horticulture

- Florance Flora

- Florensis Flower Seeds

- Forest Produce

- Marginpar

- Native Floral Group

- Bohemian Flowers

- Proven Winners

- Selecta Cut Flowers

- Syngenta

- Ball Horticultural Company

- Anthura

- Deliflor Chrysanten BV

- Schreurs

- Konst Alstroemeria BV

The Global Floriculture Market was valued at USD 73.1 billion in 2025 and is estimated to grow at a CAGR of 4.6% to reach USD 114.2 billion by 2035.

Market growth is driven by rising demand for ornamental plants, increasing disposable incomes, and the growing popularity of flowers for gifting, events, landscaping, and interior decoration. Floriculture, which includes the cultivation of cut flowers, potted plants, bedding plants, and ornamental foliage, has evolved into a highly commercialized and export-oriented industry. Urbanization, lifestyle changes, and the expansion of organized retail and e-commerce platforms have significantly increased flower consumption across both developed and emerging economies. Additionally, technological advancements in greenhouse cultivation, precision irrigation, and post-harvest handling have improved yield quality, shelf life, and year-round availability, supporting sustained market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $73.1 Billion |

| Forecast Value | $114.2 Billion |

| CAGR | 4.6% |

The market is further supported by the rising use of flowers in weddings, festivals, corporate events, and hospitality settings, where aesthetic appeal plays a crucial role. Increasing awareness of the emotional and psychological benefits of flowers, along with their growing use in home decor and wellness spaces, is positively influencing consumer demand. Export-oriented production hubs are also benefiting from improved cold chain infrastructure and international trade agreements, enabling growers to access high-value global markets. Sustainability initiatives, including eco-friendly cultivation practices and reduced chemical usage, are becoming increasingly important, especially in regions supplying premium floriculture products to environmentally conscious consumers.

Based on product type, the cut flowers segment generated USD 29 billion in 2025, accounting for the largest share of total revenue. Cut flowers such as roses, chrysanthemums, carnations, lilies, and gerberas are widely used for gifting, decoration, and ceremonial purposes, driving consistent demand throughout the year. Their strong export potential, higher margins, and widespread acceptance across cultures cut flowers the most commercially valuable segment. Advancements in breeding techniques, controlled environment agriculture, and logistics have significantly enhanced flower quality and vase life, further strengthening the dominance of this segment in both domestic and international markets.

The B2B segment held the largest share in 2025, driven by strong demand from wholesalers, exporters, event management companies, hotels, corporate offices, supermarkets, and landscaping contractors. These buyers procure flowers and ornamental plants in large volumes to support continuous commercial usage, making B2B transactions the backbone of the floriculture supply chain. The segment benefits from long-term supply contracts, centralized auctions, and organized wholesale markets that ensure consistent quality, pricing stability, and timely delivery. Increasing reliance on cold chain logistics and contract farming arrangements has further strengthened B2B operations, enabling year-round availability and reduced post-harvest losses.

United States Floriculture Market held 80% share, generating USD 11.1 billion in 2025. The North American floriculture market benefits from robust consumer demand in both the U.S. and Canada for ornamental plants and cut flowers, particularly during seasonal occasions like Valentine's Day and Mother's Day. These celebrations remain key drivers of floral sales, as flowers continue to be highly favored for gifting and home decoration. The adoption of advanced greenhouse technologies enables growers in North America to cultivate high-quality flowers and plants year-round. This capability not only ensures a consistent supply but also allows retailers and online florists to command significantly higher margins compared to international markets, reflecting the premium quality and sustained consumer demand.

Key players operating in the Global Floriculture Market include Dummen Orange, Syngenta Flowers, Ball Horticultural Company, Selecta One, Karuturi Global, Oserian Development Company, Finlays, Beekenkamp Group, and Washington Bulb Co. These companies focus on high-quality planting material, innovative flower varieties, and advanced cultivation techniques to maintain competitiveness in global markets. Companies in the floriculture market are strengthening their market position through investment in advanced cultivation technologies, product innovation, and global distribution expansion. Leading players are focusing on developing new flower varieties with longer vase life, improved color, and higher resistance to pests and diseases to meet evolving consumer preferences. Expansion into high-growth regions through contract farming and strategic partnerships with local growers is a key strategy. Companies are also leveraging cold chain logistics, digital sales platforms, and direct-to-consumer models to improve market reach and reduce post-harvest losses.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 By regional

- 2.2.2 By product type

- 2.2.3 By flower type

- 2.2.4 By distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer demand for ornamental plant

- 3.2.1.2 Increasing popularity of gifting culture

- 3.2.1.3 Growing wellness and health awareness

- 3.2.1.4 Expansion of e-commerce and digital platforms

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Perishability of products

- 3.2.2.2 Increasing competition from artificial flowers

- 3.2.3 Opportunities

- 3.2.3.1 Commercialization of sustainability and eco-innovation

- 3.2.3.2 Adoption of precision agriculture and AI-driven logistics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Major market trends and disruption

- 3.5 Future market trends

- 3.6 Risk and mitigation Analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.9 Regulatory landscape

- 3.9.1 Standards and compliance requirement

- 3.9.2 Certification standards

- 3.10 Consumer buying behaviour analysis

- 3.10.1 Purchasing patterns

- 3.10.2 Preference analysis

- 3.10.3 Regional variations in consumer behavior

- 3.10.4 Impact of e-commerce on buying decisions

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022-2035 (USD Billion) (Tons)

- 5.1 Key trends

- 5.2 Cut flowers

- 5.3 Potted plants

- 5.4 Bedding plants

- 5.5 Foliage plants

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Flower Type, 2022-2035 (USD Billion) (Tons)

- 6.1 Key trends

- 6.2 Rose

- 6.3 Chrysanthemum

- 6.4 Tulip

- 6.5 Lily

- 6.6 Gerbera

- 6.7 Carnations

- 6.8 Texas bluebell

- 6.9 Freesia

- 6.10 Hydrangea

- 6.11 Others

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Tons)

- 7.1 Key trends

- 7.2 B to B

- 7.3 B to C

- 7.3.1 Online

- 7.3.2 Offline

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.4.6 Malaysia

- 8.4.7 Indonesia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Beekenkamp Group

- 9.2 Danziger

- 9.3 Dummen Orange

- 9.4 Esmeralda Farms

- 9.5 Flamingo Horticulture

- 9.6 Florance Flora

- 9.7 Florensis Flower Seeds

- 9.8 Forest Produce

- 9.9 Marginpar

- 9.10 Native Floral Group

- 9.11 Bohemian Flowers

- 9.12 Proven Winners

- 9.13 Selecta Cut Flowers

- 9.14 Syngenta

- 9.15 Ball Horticultural Company

- 9.16 Anthura

- 9.17 Deliflor Chrysanten B.V.

- 9.18 Schreurs

- 9.19 Konst Alstroemeria B.V

花卉市場-2026-2032年全球市場預測

花卉市場-2026-2032年全球市場預測 花卉市場:按產品類型、應用和地區分類

花卉市場:按產品類型、應用和地區分類 花卉市場規模、佔有率及成長分析(依產品類型、花卉類型、最終用途、通路及地區分類)-2026-2033年產業預測

花卉市場規模、佔有率及成長分析(依產品類型、花卉類型、最終用途、通路及地區分類)-2026-2033年產業預測 消費花卉市場:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)花卉產業:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)

消費花卉市場:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)花卉產業:全球市場佔有率和排名、總收入和需求預測(2025-2031 年) 2032 年園藝和花卉市場預測:按產品類型、栽培類型、技術、分銷管道、應用、最終用戶和地區進行的全球分析

2032 年園藝和花卉市場預測:按產品類型、栽培類型、技術、分銷管道、應用、最終用戶和地區進行的全球分析 全球花卉市場2030 年花卉市場預測:按產品類型、花卉類型、銷售管道和地區進行的全球分析

全球花卉市場2030 年花卉市場預測:按產品類型、花卉類型、銷售管道和地區進行的全球分析