|

市場調查報告書

商品編碼

1936537

海藻風味市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)Seaweed Flavor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

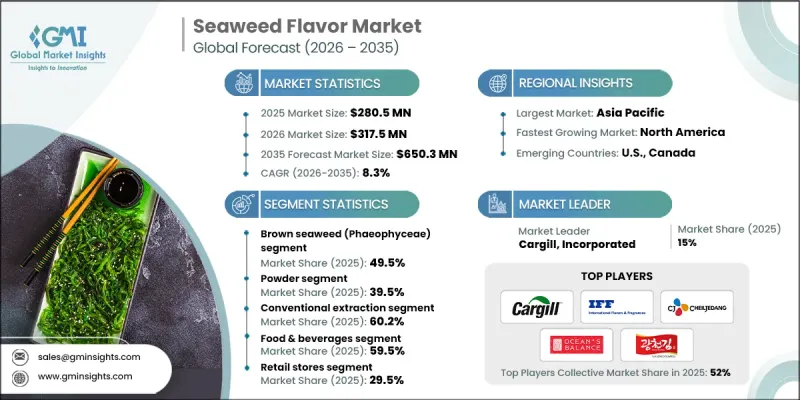

全球海藻調味料市場預計到 2025 年將達到 2.805 億美元,到 2035 年將達到 6.503 億美元,年複合成長率為 8.3%。

市場成長主要受人們對健康和保健日益成長的興趣所驅動。海藻天然營養豐富且熱量低,因此深受注重健康的消費者青睞。潔淨標示趨勢推崇加工最少、天然的風味,使海藻成為合成香料的理想替代品。隨著植物來源飲食的日益普及,海藻風味被應用於湯、醬汁、蒸餾和即食食品等創新食品中,不僅增強了鮮味,還提供了碘和抗氧化劑等功能性益處。海藻的環境永續性和天然複雜的風味也擴大被添加到調味料、香辛料和替代蛋白產品中。亞太地區憑藉其文化親和性和烹飪應用引領市場,而歐洲則因其天然和永續的吸引力而需求不斷成長。北美則受惠於融合菜系和植物性食品運動。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 2.805億美元 |

| 預測金額 | 6.503億美元 |

| 複合年成長率 | 8.3% |

褐藻(Phaeophyceae)市佔率佔比達49.5%,預計到2035年將以8%的複合年成長率成長。褐藻因其濃郁的鮮味和豐富的礦物質含量而備受推崇,非常適合用於湯、醬汁和調味料等食品的調味。其濃郁的風味和穩定的性能使其成為眾多食品生產商尋求天然鮮味增強劑的首選。

預計到2025年,粉狀海藻香精市場佔有率將達到39.5%,並在2035年之前以7.9%的複合年成長率成長。海藻粉用途廣泛,風味穩定,易於添加到乾粉混合物、零食和調味料中,在需要風味均勻和保存期限長的領域中發揮重要作用。液體萃取物因其溶解迅速、風味濃郁,是飲料和醬料的首選;而固態萃取物則具有高營養密度和濃郁風味,是高階機能性食品的理想選擇。

預計到2025年,北美海藻香精市場將佔據20.4%的市場佔有率,且成長速度正在加快。消費者對植物來源和潔淨標示產品的接受度不斷提高,以及食品技術的進步,正在推動市場需求。該地區先進的製造能力和對永續解決方案的監管重點,促進了環保創新香精產品的生產,使北美成為海藻香精的關鍵市場。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 植物來源食品革命

- 強制減少鹽的攝取量和日益增強的健康意識

- 關於永續性和再生農業的思考

- 產業潛在風險與挑戰

- 人們對重金屬和碘污染的擔憂

- 有機認證標準的碎片化

- 市場機遇

- 生物精煉的商業化

- 擴大在北美和歐洲的生產規模

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續努力

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 考慮到碳足跡

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 按類型分類的市場估算與預測,2022-2035年

- 褐藻(Phaeophyceae)

- 海帶(Laminaria、Saccharina)

- 裙帶菜(Undaria pinnatifida)

- 結節藻

- 其他褐藻(巨藻、岩藻)

- 紅藻(Rhodophyceae)

- 海苔(紫菜屬/紫菜屬)

- 紅藻(Palmaria palmata)

- 產生鹿角菜膠的海藻(真須海藻、卡帕藻、江蘺)

- 其他紅藻

- 綠藻(Chlorophyceae)

- 海藻(滸苔屬)

- 其他綠藻

第6章 按類型分類的市場估算與預測,2022-2035年

- 粉末

- 液體萃取物

- 固態萃取物

- 薄片

- 床單和包裝紙

- 整葉

7. 按加工技術分類的市場估算與預測,2022-2035 年

- 常規萃取方法

- 鹼萃取

- 水萃取

- 先進的萃取技術

- 酵素輔助萃取方法(EAE)

- 超臨界流體萃取(SFE)

- 微波輔助和超音波萃取

- 脈衝電場(PEF)

- 生物精煉和級聯工藝

第8章 按應用領域分類的市場估算與預測,2022-2035年

- 飲食

- 植物來源肉替代品

- 機能飲料

- 小吃

- 調味料和香辛料

- 湯、高湯醬汁、高湯

- 麵包糖果甜點

- 乳製品及乳製品替代品

- 烹飪原料(供餐飲服務業使用)

- 營養保健品和膳食補充劑

- 動物飼料和寵物食品

- 化妝品和個人護理

9. 2022-2035年按分銷管道分類的市場估算與預測

- 零售店

- 線上零售

- 餐飲服務及旅館業

- 批發商

第10章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第11章 公司簡介

- Cargill, Incorporated

- IFF(International Flavors &Fragrances Inc.)

- CJ CheilJedang/bibigo

- Ocean's Balance(Formerly Maine Coast Sea Vegetables)

- KwangcheonKim Co., Ltd.

- Nagai Nori Co., Ltd.

- Seaweed &Co.

- Mara Seaweed

- This is Seaweed Ltd.

- Wild Irish Seaweeds

- Hispanagar

- Seagarden AS

- The Seaweed Company

- Green Fresh(Fujian)Foodstuff Co., Ltd.

- Marusan

- Ocean Organics

The Global Seaweed Flavor Market was valued at USD 280.5 million in 2025 and is estimated to grow at a CAGR of 8.3% to reach USD 650.3 million by 2035.

The market's growth is driven by the rising focus on health and wellness, as seaweed is naturally nutrient-rich while remaining low in calories, appealing strongly to health-conscious consumers. Clean-label trends favor minimally processed, natural flavoring agents, positioning seaweed as a preferred alternative to synthetic flavors. Plant-based diets are gaining traction, and seaweed flavor is increasingly used in innovative food applications, enhancing the savory profile of soups, sauces, snacks, and ready-to-eat meals while contributing functional benefits like iodine and antioxidants. Environmentally sustainable and naturally complex in flavor, seaweed is being adopted in seasonings, condiments, and alternative protein products. Asia-Pacific leads the market due to cultural familiarity and culinary use, Europe is experiencing uptake for its natural and sustainable appeal, and North America benefits from fusion cuisine trends and the plant-based food movement.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $280.5 Million |

| Forecast Value | $650.3 Million |

| CAGR | 8.3% |

The brown seaweed (Phaeophyceae) segment held a 49.5% share and is projected to grow at a CAGR of 8% by 2035. Brown seaweed is favored for its rich umami taste and mineral content, making it highly suitable for savory applications like soups, sauces, and seasonings. Its flavor depth and consistent performance have established it as the go-to choice for many food manufacturers seeking natural savory enhancement.

The powdered seaweed flavor segment held a share of 39.5% in 2025 and is expected to grow at a CAGR of 7.9% through 2035. Powdered seaweed is highly versatile, offering stability and ease of blending into dry mixes, snacks, and seasonings where uniform flavor and extended shelf life are critical. Liquid extracts are preferred in beverages and sauces for quick solubility and concentrated flavor delivery, while solid extracts are ideal for premium functional foods, providing dense nutrition and strong taste.

North America Seaweed Flavor Market accounted for a 20.4% share in 2025, and its growth is accelerating. Consumer adoption of plant-based and clean-label products, combined with advancements in food technology, is driving demand. The region's advanced manufacturing capabilities and regulatory emphasis on sustainable solutions are encouraging the production of eco-friendly and innovative flavor offerings, positioning North America as a significant market for seaweed flavor products.

Key players in the Global Seaweed Flavor Market include CJ CheilJedang / bibigo, Ocean Organics, Cargill, Incorporated, Green Fresh (Fujian) Foodstuff Co., Ltd., Mara Seaweed, KwangcheonKim Co., Ltd., Ocean's Balance, Seaweed & Co., Nagai Nori Co., Ltd., Seagarden AS, This is Seaweed Ltd., The Seaweed Company, Marusan, Wild Irish Seaweeds, and Hispanagar. Companies in the seaweed flavor market strengthen their position through product innovation, introducing new forms like powders, liquids, and solid extracts to cater to diverse applications. They focus on sustainability by sourcing eco-friendly seaweed and promoting traceability to appeal to conscious consumers. Strategic collaborations with food and beverage manufacturers enable tailored flavor solutions, while R&D investments enhance umami and functional profiles. Geographic expansion, marketing campaigns emphasizing natural and clean-label benefits, and partnerships with culinary professionals help increase visibility and adoption.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Form

- 2.2.4 Processing technology

- 2.2.5 Application

- 2.2.6 Distribution channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Plant-based food revolution

- 3.2.1.2 Salt reduction mandates & health consciousness

- 3.2.1.3 Sustainability & regenerative agriculture narrative

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Heavy metal & iodine contamination concerns

- 3.2.2.2 Fragmented organic certification standards

- 3.2.3 Market opportunities

- 3.2.3.1 Biorefinery commercialization

- 3.2.3.2 North American & European production expansion

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Brown seaweeds (Phaeophyceae)

- 5.2.1 Kombu (laminaria spp., saccharina spp.)

- 5.2.2 Wakame (Undaria pinnatifida)

- 5.2.3 Ascophyllum nodosum

- 5.2.4 Other brown seaweeds (macrocystis, fucus)

- 5.3 Red seaweeds (Rhodophyceae)

- 5.3.1 Nori (Porphyra/Pyropia spp.)

- 5.3.2 Dulse (Palmaria palmata)

- 5.3.3 Carrageenan-producing seaweeds (Eucheuma, Kappaphycus, Gracilaria)

- 5.3.4 Other red seaweeds

- 5.4 Green seaweeds (Chlorophyceae)

- 5.4.1 Sea lettuce (Ulva spp.)

- 5.4.2 Other green seaweeds

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Powder

- 6.3 Liquid extract

- 6.4 Solid extract

- 6.5 Flakes

- 6.6 Sheets & wraps

- 6.7 Whole-leaf

Chapter 7 Market Estimates and Forecast, By Processing Technology, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Conventional extraction

- 7.2.1 Alkaline extraction

- 7.2.2 Water-based extraction

- 7.3 Advanced extraction technologies

- 7.3.1 Enzyme-assisted extraction (EAE)

- 7.3.2 Supercritical fluid extraction (SFE)

- 7.3.3 Microwave-assisted & ultrasound extraction

- 7.3.4 Pulsed electric fields (PEF)

- 7.4 Biorefinery & cascade processing

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Food & beverages

- 8.2.1 Plant-based meat alternatives

- 8.2.2 Functional beverages

- 8.2.3 Snacks

- 8.2.4 Seasonings & condiments

- 8.2.5 Soups, broths & dashi

- 8.2.6 Bakery & confectionery

- 8.2.7 Dairy & dairy alternatives

- 8.3 Culinary ingredients (food service)

- 8.4 Nutraceuticals & dietary supplements

- 8.5 Animal feed & pet food

- 8.6 Cosmetics & personal care

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Retail stores

- 9.3 Online retail

- 9.4 Food service & hospitality

- 9.5 Wholesale distributors

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Cargill, Incorporated

- 11.2 IFF (International Flavors & Fragrances Inc.)

- 11.3 CJ CheilJedang / bibigo

- 11.4 Ocean's Balance (Formerly Maine Coast Sea Vegetables)

- 11.5 KwangcheonKim Co., Ltd.

- 11.6 Nagai Nori Co., Ltd.

- 11.7 Seaweed & Co.

- 11.8 Mara Seaweed

- 11.9 This is Seaweed Ltd.

- 11.10 Wild Irish Seaweeds

- 11.11 Hispanagar

- 11.12 Seagarden AS

- 11.13 The Seaweed Company

- 11.14 Green Fresh (Fujian) Foodstuff Co., Ltd.

- 11.15 Marusan

- 11.16 Ocean Organics

海藻市場分析及預測(至2035年):類型、產品類型、形態、應用、最終用戶、技術、組成成分、簡介、製程

海藻市場分析及預測(至2035年):類型、產品類型、形態、應用、最終用戶、技術、組成成分、簡介、製程 全球高級海藻調味料市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球高級海藻調味料市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 商業褐藻市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)

商業褐藻市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年) 商業褐藻市場規模、佔有率和成長分析(按等級、應用、培養技術、產品形態、收穫方法和地區分類)—產業預測(2026-2033 年)

商業褐藻市場規模、佔有率和成長分析(按等級、應用、培養技術、產品形態、收穫方法和地區分類)—產業預測(2026-2033 年) 全球美食海藻調味品市場海帶產品的世界市場

全球美食海藻調味品市場海帶產品的世界市場 到 2030 年全球海藻香料市場預測:按類型、形式、分銷管道、應用和地區分類世界海藻市場

到 2030 年全球海藻香料市場預測:按類型、形式、分銷管道、應用和地區分類世界海藻市場 全球海帶產品市場規模、佔有率及趨勢分析報告,依形式(粉末、液體和片狀)、依應用(農業、食品、藥品等)、依類型(新鮮、乾和鹹)、區域展望和預測, 2024 - 2031

全球海帶產品市場規模、佔有率及趨勢分析報告,依形式(粉末、液體和片狀)、依應用(農業、食品、藥品等)、依類型(新鮮、乾和鹹)、區域展望和預測, 2024 - 2031