|

市場調查報告書

商品編碼

1928921

自主最後一公里配送市場機會、成長要素、產業趨勢分析及預測(2026-2035)Autonomous Last Mile Delivery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

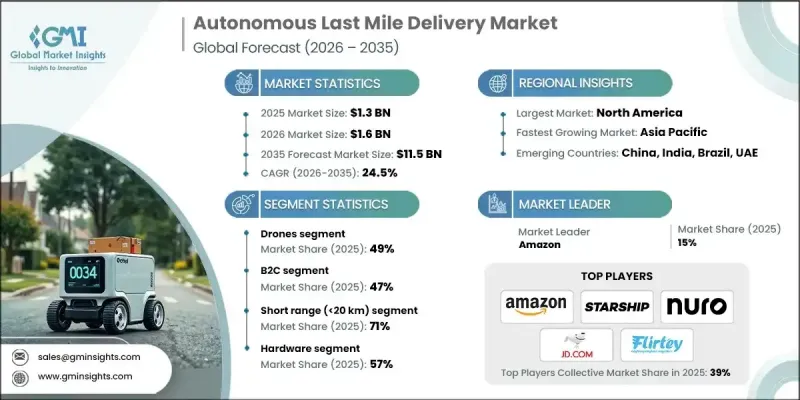

全球自主最後一公里配送市場預計到 2025 年價值 13 億美元,到 2035 年達到 115 億美元,年複合成長率為 24.5%。

自主末端配送被廣泛認為是一種創新的物流解決方案,它利用人工智慧、機器人和自動駕駛車輛,在無需人工干預的情況下將貨物從配送中心運送至最終用戶。這項技術涵蓋了多種平台,旨在有效地運作各種不同的配送環境。市場成長的驅動力來自數位商務的快速發展、人事費用的上升以及自主系統能力的提升。日益成長的線上購物活動顯著提升了對擴充性、柔軟性配送模式的需求。同時,技術成本的下降和營運效率的提高也增強了自主配送解決方案的經濟可行性,使其更具競爭力,足以與傳統配送方式相提並論。監管政策的發展也為商業化進程提供了支持,清晰的政策框架降低了營運商的不確定性。這些趨勢正在匯聚,重塑物流策略,影響消費者對配送的預期,並推動都市區和郊區基礎設施規劃的變革。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 13億美元 |

| 預測金額 | 115億美元 |

| 複合年成長率 | 24.5% |

預計到2025年,無人機配送市佔率將達到49%,並在2026年至2035年間以22.8%的複合年成長率成長。無人機平台因其能夠快速配送並避免地面擁塞(尤其是在管制較少的空域)而日益受到青睞。動力系統、導航軟體和運行可靠性的不斷改進,正在拓展無人機的實際應用場景並提高配送效率。

預計到2025年,B2C領域將佔據47%的市場佔有率,並以24.2%的複合年成長率(CAGR)實現最快成長,直至2035年。該領域的成長主要受消費者對更快產品交付速度和更靈活交付時間的日益成長的需求所驅動。自主配送解決方案憑藉其持續營運和降低的配送成本,能夠很好地滿足這些需求。

預計到2024年,北美自動駕駛最後一公里配送市場將佔據36%的市場佔有率,並在2035年之前以22.1%的複合年成長率成長。該地區的主導地位得益於先進的數位零售基礎設施、有利的法規環境、不斷提高的自動化應用率以及技術開發商的高度集中。美國憑藉其早期應用和大規模部署舉措,繼續成為該地區成長的主要貢獻者。

目錄

第1章調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 電子商務的成長推動了對最後一公里配送的需求。

- 人事費用上升推動自動化

- 人工智慧和機器人技術的進步提高了效率

- 都市化加快和交通堵塞加劇,推動了對自動配送的需求。

- 永續性舉措將推動電動車和自動駕駛汽車的普及。

- 產業潛在風險與挑戰

- 監管和法律障礙減緩了普及率。

- 高昂的初始投資是廣泛採用的障礙。

- 市場機遇

- 智慧城市融入配送走廊

- 醫療和藥品配送

- 車隊即服務 (FaaS) 模式

- 跨產業夥伴關係

- 在新興市場拓展業務

- 成長潛力分析

- 監管環境

- 北美洲

- 美國 - 聯邦機動車輛安全標準 (FMVSS) 人行道機器人(400 磅以下)豁免模板,取代個人豁免申請流程。

- 加拿大-擬議修改超視距飛行(BVLOS)操作法規和新的無人機送貨重量限制,將加強都市區作業的安全標準。

- 歐洲

- 德國聯邦交通和數位基礎設施部計劃開發自動駕駛汽車測試基礎設施(投資 32 億歐元),並在漢堡和慕尼黑建立專門的自動駕駛汽車測試區(Emergen Research)。

- 英國—《2024年自動駕駛汽車法案》將建立一個全面的法律體制,預計2027年將推出配套法規。

- 在法國,為了明確事故責任並確保透明度,從 2025 年起,所有自動駕駛汽車都必須配備黑盒子記錄設備。

- 亞太地區

- 中國—《北京自動駕駛汽車管理條例(2025年4月版)》是由工業和資訊化部頒布的條例,規定了自動駕駛汽車測試的申請程序並解決了安全問題。

- 印度 - 2025 年民用無人機(促進和監管)法案(草案)規定了無人機登記、分配唯一識別號碼 (UIN)、無人機製造商的強制性型號認證,以及對商用無人駕駛飛行器 (UAV) 徵收 5% 的商品和服務稅 (GST)。

- 日本-經濟產業省的藍圖(2025)旨在到 2023 年將功能更強大的自主最後一公里配送解決方案的應用範圍擴大到合法低速模式之外。

- 拉丁美洲

- 巴西-與聖保羅州合作L3級自動駕駛計程車區域試點計畫(2024年),國家框架尚未建立

- 中東和非洲

- 沙烏地阿拉伯—「2030願景」計畫旨在透過政府主導的投資和監管改革,消除普及障礙,使公共道路上的自動駕駛汽車數量增加50%。

- 北美洲

- 波特分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利分析

- 用例和成功案例

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

- 未來前景與機遇

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 企業擴張計畫和資金籌措

第5章 2022-2035年各平台市場估算與預測

- 無人機

- 多旋翼無人機

- 固定翼無人機

- 混合動力垂直起降無人機

- 機器人

- 人行道送貨機器人

- 自主地面車輛(AGV)

- 室內配送機器人

- 卡車和貨車

第6章 依交付方式分類的市場估算與預測,2022-2035年

- B2B

- B2C

- C2C

第7章 2022-2035年各地區市場估算與預測

- 短距離(小於20公里)

- 長途(超過20公里)

第8章 按解決方案分類的市場估算與預測,2022-2035年

- 硬體

- 汽車平臺

- 感測器(LiDAR、攝影機、超音波、雷達)

- 電池/電源系統

- 軟體

- 自主導航軟體

- 車隊管理平台

- 人工智慧/機器學習演算法

- 服務

- 維護和支援

- 系統整合和諮詢

第9章 按應用領域分類的市場估算與預測,2022-2035年

- 電子商務

- 食品和雜貨

- 小包裹和宅配服務

- 製藥

- 家具和家電

- 其他

第10章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 比荷盧經濟聯盟

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 新加坡

- 泰國

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- 世界公司

- Amazon

- DHL

- Flirtey

- JD.com

- Matternet

- Nuro

- Starship Technologies

- UPS

- Wing Aviation

- Zipline

- 當地公司

- JD Logistics

- Kiwibot

- Postmates

- RoboSense

- Segway Robotics

- SF Express

- Swiggy

- TeleRetail Robotics

- Yandex Delivery

- Zomato

- 新興科技創新者

- Flytrex

- Manna Aero

- Ottonomy.IO

- Refraction AI

- Serve Robotics

The Global Autonomous Last Mile Delivery Market was valued at USD 1.3 billion in 2025 and is estimated to grow at a CAGR of 24.5% to reach USD 11.5 billion by 2035.

Autonomous last-mile delivery is widely recognized as a transformative logistics solution that relies on artificial intelligence, robotics, and self-operating vehicles to move goods from fulfillment points to end users without human intervention. The technology spans a range of platforms designed to operate efficiently across varied delivery environments. Market growth is being fueled by the rapid expansion of digital commerce, escalating workforce expenses, and continuous improvements in autonomous system capabilities. Rising online purchasing activity has significantly increased demand for scalable and flexible delivery models. At the same time, declining technology costs and improved operational efficiency are enhancing the economic viability of autonomous delivery solutions, allowing them to compete more effectively with conventional delivery methods. Regulatory progress is also supporting commercialization, as clearer policy frameworks are reducing uncertainty for operators. Together, these dynamics are reshaping logistics strategies, influencing consumer delivery expectations, and prompting changes in urban and suburban infrastructure planning.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.3 Billion |

| Forecast Value | $11.5 Billion |

| CAGR | 24.5% |

The drone-based delivery segment held a share of 49% in 2025 and is forecast to grow at a CAGR of 22.8% from 2026 to 2035. Drone platforms are gaining traction due to their ability to support rapid deliveries while avoiding ground-level congestion, particularly in less densely regulated airspace. Ongoing improvements in power systems, navigation software, and operational reliability are expanding their practical use cases and delivery efficiency.

The business-to-consumer segment accounted for 47% share in 2025 and is projected to grow at the fastest pace, with a CAGR of 24.2% through 2035. Growth in this segment is attributed to increasing consumer expectations for faster fulfillment and flexible delivery windows. Autonomous delivery solutions are well-suited to meet these requirements through continuous operation and reduced delivery costs.

North America Autonomous Last Mile Delivery Market captured 36% share in 2024 and is expected to grow at a CAGR of 22.1% during 2035. The region's leadership is supported by advanced digital retail infrastructure, favorable regulatory developments, increasing automation adoption, and a strong concentration of technology developers. The United States remains the primary contributor to regional growth due to early adoption and large-scale deployment initiatives.

Key companies operating in the Global Autonomous Last Mile Delivery Market include Starship Technologies, Amazon, Wing Aviation, Nuro, Zipline, UPS, JD.com, Kiwibot, and Flirtey. Companies active in the Autonomous Last Mile Delivery Market are strengthening their positions through technology development, pilot deployments, and strategic partnerships. Many players are investing heavily in artificial intelligence, navigation systems, and fleet management platforms to improve reliability and scalability. Collaborations with retailers, logistics providers, and local authorities are helping accelerate real-world deployment and regulatory alignment. Firms are also expanding geographic coverage through phased rollouts and focusing on cost optimization to improve commercial viability. Continuous testing, data-driven optimization, and modular platform design are enabling companies to adapt quickly to evolving delivery requirements and secure long-term market footholds.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Platform

- 2.2.3 Delivery Mode

- 2.2.4 Range

- 2.2.5 Solutions

- 2.2.6 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 E-commerce growth boosts last-mile delivery demand

- 3.2.1.3 Rising labor costs favor automation

- 3.2.1.4 AI and robotics advancements improve efficiency

- 3.2.1.5 Urbanization and traffic congestion increase need for autonomous delivery

- 3.2.1.6 Sustainability initiatives promote electric autonomous vehicles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory and legal barriers slow deployment

- 3.2.2.2 High initial investment limits adoption

- 3.2.3 Market opportunities

- 3.2.3.1 Smart city integration for delivery corridors

- 3.2.3.2 Healthcare and pharmaceutical deliveries

- 3.2.3.3 Fleet-as-a-service models

- 3.2.3.4 Cross-industry partnerships

- 3.2.3.5 Expansion in emerging markets

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US - Federal Motor Vehicle Safety Standards (FMVSS) exemption templates for sidewalk robots under 400 pounds, replacing waiver-by-waiver process.

- 3.4.1.2 Canada - Anticipated updates to beyond-visual-line-of-sight (BVLOS) operations regulations and new weight regulations for drone delivery with enhanced safety rules for urban operations.

- 3.4.2 Europe

- 3.4.2.1 Germany - Federal Ministry of Transport and Digital Infrastructure autonomous vehicle testing infrastructure framework with €3.2 billion investment and dedicated autonomous vehicle zones in Hamburg and Munich Emergen Research

- 3.4.2.2 UK - Automated Vehicles Act 2024 establishing comprehensive legal framework with secondary regulations expected by 2027

- 3.4.2.3 France - Black-box recorder requirement for all self-driving cars starting 2025 to establish accident responsibility and transparency

- 3.4.3 Asia Pacific

- 3.4.3.1 China - Beijing Autonomous Vehicle Regulation (April 2025) outlining procedures for AV pilot applications and Ministry of Industry and Information Technology regulations addressing safety concerns

- 3.4.3.2 India - Draft Civil Drone (Promotion and Regulation) Bill 2025 mandating registration, Unique Identification Numbers (UIN), type certification for drone manufacturers, and 5% GST on commercial UAVs

- 3.4.3.3 Japan - National METI roadmap (2025) to scale higher-capability autonomous last-mile delivery solutions beyond low-speed models legalized in 2023

- 3.4.4 Latin America

- 3.4.4.1 Brazil - Regional autonomy with Sao Paulo Level 3 autonomous taxi pilots (2024), no national framework yet established

- 3.4.5 MEA

- 3.4.5.1 Saudi Arabia - Vision 2030 initiative targeting 50% increase in autonomous vehicle presence on public roads with government-driven investment and regulatory reforms to remove AV deployment barriers

- 3.4.1 North America

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Use cases & success stories

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Future outlook and opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Platform, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Drones

- 5.2.1 Multi-rotor drones

- 5.2.2 Fixed-wing drones

- 5.2.3 Hybrid VTOL drones

- 5.3 Robots

- 5.3.1 Sidewalk delivery robots

- 5.3.2 Autonomous ground vehicles (AGVs)

- 5.3.3 Indoor delivery robots

- 5.4 Trucks & vans

Chapter 6 Market Estimates & Forecast, By Delivery Mode, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 B2B

- 6.3 B2C

- 6.4 C2C

Chapter 7 Market Estimates & Forecast, By Range, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Short range (<20 km)

- 7.3 Long range (>20 km)

Chapter 8 Market Estimates & Forecast, By Solution, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Hardware

- 8.2.1 Vehicle platforms

- 8.2.2 Sensors (LiDAR, cameras, ultrasonic, radar)

- 8.2.3 Batteries / Power systems

- 8.3 Software

- 8.3.1 Autonomous navigation software

- 8.3.2 Fleet management platforms

- 8.3.3 AI / Machine learning algorithms

- 8.4 Services

- 8.4.1 Maintenance & support

- 8.4.2 System integration & consultancy

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 E-commerce

- 9.3 Food and grocery

- 9.4 Parcel & courier services

- 9.5 Pharmaceutical

- 9.6 Furniture & appliance

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.3.8 Benelux

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Amazon

- 11.1.2 DHL

- 11.1.3 Flirtey

- 11.1.4 JD.com

- 11.1.5 Matternet

- 11.1.6 Nuro

- 11.1.7 Starship Technologies

- 11.1.8 UPS

- 11.1.9 Wing Aviation

- 11.1.10 Zipline

- 11.2 Regional Players

- 11.2.1 JD Logistics

- 11.2.2 Kiwibot

- 11.2.3 Postmates

- 11.2.4 RoboSense

- 11.2.5 Segway Robotics

- 11.2.6 SF Express

- 11.2.7 Swiggy

- 11.2.8 TeleRetail Robotics

- 11.2.9 Yandex Delivery

- 11.2.10 Zomato

- 11.3 Emerging Technology Innovators

- 11.3.1 Flytrex

- 11.3.2 Manna Aero

- 11.3.3 Ottonomy.IO

- 11.3.4 Refraction AI

- 11.3.5 Serve Robotics

2026-2030年全球自主最後一公里配送市場

2026-2030年全球自主最後一公里配送市場 自主最後一公里配送市場報告:按平台、解決方案、距離、應用和地區分類(2026-2034 年)

自主最後一公里配送市場報告:按平台、解決方案、距離、應用和地區分類(2026-2034 年) 自主最後一公里配送市場:市場規模、佔有率、成長率、全球產業分析、按類型、應用和地區分類的分析以及未來預測(2026-2034 年)

自主最後一公里配送市場:市場規模、佔有率、成長率、全球產業分析、按類型、應用和地區分類的分析以及未來預測(2026-2034 年) 2026年全球自動駕駛最後一公里配送市場報告

2026年全球自動駕駛最後一公里配送市場報告 自動駕駛最後一公里配送市場規模、佔有率和成長分析(按車輛類型、配送方式、應用、組件、解決方案和地區分類)-2026-2033年產業預測

自動駕駛最後一公里配送市場規模、佔有率和成長分析(按車輛類型、配送方式、應用、組件、解決方案和地區分類)-2026-2033年產業預測 2032 年自動駕駛最後一哩配送市場預測:按組件、範圍、自主等級、最終用戶和地區進行的全球分析

2032 年自動駕駛最後一哩配送市場預測:按組件、範圍、自主等級、最終用戶和地區進行的全球分析 自主式最後一哩發送的全球市場:各零件,各機器人類型,各車輛類型,負載容量,各用途,各產業,場所,各地區,市場規模,產業動態,機會分析,預測(2025年~2033年)

自主式最後一哩發送的全球市場:各零件,各機器人類型,各車輛類型,負載容量,各用途,各產業,場所,各地區,市場規模,產業動態,機會分析,預測(2025年~2033年) 自動駕駛最後一哩配送市場規模、佔有率、趨勢分析報告:按平台、解決方案、範圍、最終用途、地區和細分市場預測,2025 年至 2030 年

自動駕駛最後一哩配送市場規模、佔有率、趨勢分析報告:按平台、解決方案、範圍、最終用途、地區和細分市場預測,2025 年至 2030 年 自動駕駛最後一哩配送全球市場規模、佔有率、趨勢分析報告:2024 年至 2031 年按範圍、解決方案、車輛類型、應用、地區分類的展望和預測到 2033 年自動最後一哩交付的全球市場、機會與策略

自動駕駛最後一哩配送全球市場規模、佔有率、趨勢分析報告:2024 年至 2031 年按範圍、解決方案、車輛類型、應用、地區分類的展望和預測到 2033 年自動最後一哩交付的全球市場、機會與策略