|

市場調查報告書

商品編碼

1928903

動物飼料替代蛋白市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)Animal Feed Alternative Protein Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

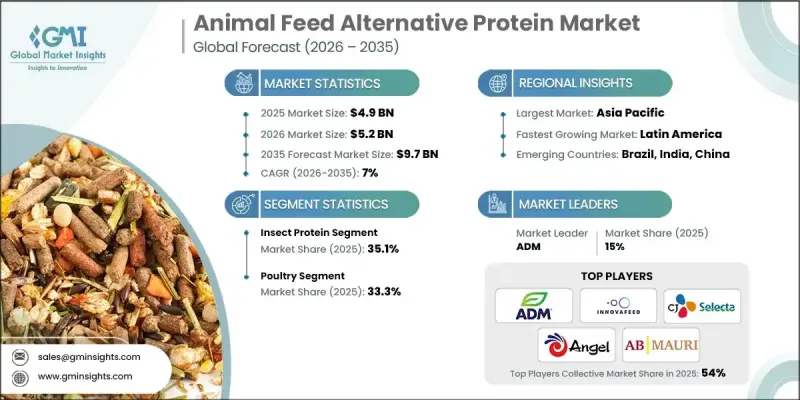

全球動物飼料替代蛋白市場預計到 2025 年將達到 49 億美元,到 2035 年將達到 97 億美元,年複合成長率為 7%。

市場成長的驅動力在於永續性需求,這些需求重塑了整個飼料供應鏈的蛋白質籌資策略。與傳統畜牧生產相關的排放和土地利用所帶來的環境壓力,已被認為是促使一體化企業、製造商和零售商重新評估蛋白質投入來源的關鍵因素。替代飼料蛋白因其依賴特定產品資源、每公頃蛋白質產量高以及能夠支持長期供應穩定性等特點,被視為低影響解決方案。討論強調,在此期間,永續性目標、監管力度和創新共同加速了飼料蛋白的多元化轉型,使其擺脫對傳統飼料蛋白的依賴,並為在全球多種動物生產系統中更廣泛地商業性化應用奠定了基礎。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 49億美元 |

| 預測金額 | 97億美元 |

| 複合年成長率 | 7% |

市場接受度的進一步解釋體現在糧食安全和成本波動。 2021年至2023年,供應中斷和地緣政治不確定性推高了飼料成本,增加了生產者管理風險的壓力。替代蛋白被視為穩定的來源,可在關鍵畜牧業領域進行試驗。昆蟲飼料、發酵植物蛋白和微生物衍生成分的表現結果與傳統進口蛋白飼料相當,同時降低了對外部供應鏈的依賴。針對消化功能、腸道功能和減少抗生素依賴性的研究進一步增強了人們對替代飼料蛋白能夠促進動物健康、改善動物福利並提升高級產品定位的信心。

預計到2025年,昆蟲蛋白市佔率將達到35.1%,並在2026年至2035年間以6.8%的複合年成長率成長。市場趨勢表明,企業正逐漸擺脫對單一蛋白質來源的依賴,轉向多元化的原料組合。大型飼料生產商正將昆蟲來源的原料與微生物、藻類、真菌、酵母來源的蛋白質以及加工大豆蛋白混合使用。這種組合方式旨在平衡成本控制、永續性、營養穩定性、胺基酸最佳化以及其他與腸道健康和飼料轉換率相關的益處。

預計到2025年,家禽市場將佔33.3%的市場佔有率,到2035年將以6.8%的複合年成長率成長。策略投資正集中於高利潤的畜牧業領域,因為高價值的飼料配方能夠抵銷更高的原料成本。生產者和飼料配方生產商之間的合作日益普及,以此來開發富含替代蛋白的均衡飼料,從而支持永續性等概念,減少對傳統海洋蛋白的依賴,並在動物營養和寵物市場引入新型飼料成分。

預計到2024年,北美動物飼料替代蛋白市場規模將達11.9億美元。該地區的成長主要由尋求供應安全和環境考慮的垂直整合生產商推動。家禽飼料、特殊飼料和寵物營養領域的強勁需求持續推動著發酵蛋白、酵母衍生蛋白和單細胞蛋白的應用。美國憑藉先進的發酵基礎設施、零售商主導的永續性舉措以及對不含抗生素、定位高階且部分替代傳統豆粕的飼料解決方案的穩定需求,成為領先的國內市場。

競爭格局包括ADM、Calysta、Angel Yeast、Inova Feed、CJ Selecta、Hamlet Protein A/S、Titan Biotech、CHS、杜邦公司、AgriProtein、DeepBranch Biotechnology、AB Maury和Crescent Biotech等公司,它們都在積極開發和商業化飼料蛋白解決方案,並在全球市場推廣應用。動物飼料替代蛋白市場的企業正透過產能擴張、技術投資和策略聯盟來鞏固自身地位。許多企業正致力於擴大發酵和昆蟲生產系統的規模,以提高成本競爭力和供應可靠性。隨著企業整合多種蛋白質形式以滿足不同的營養和監管要求,產品組合多元化變得日益重要。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 豆粕價格波動和供應中斷

- 亞洲對肉類和水產養殖的需求不斷成長

- 對永續性、森林砍伐和排放的擔憂

- 產業潛在風險與挑戰

- 高成本且大規模供應有限

- 監理核准和安全認知問題

- 市場機遇

- 農產品對飼料蛋白的增值回收

- 優質、無抗生素、功能性肉品標籤

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續努力

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 考慮到碳足跡

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 2022-2035年按產品分類的市場估算與預測

- 昆蟲來源的蛋白質

- 大豆分離蛋白

- 大豆蛋白濃縮物

- 發酵大豆蛋白

- 水綿蛋白

- 單細胞蛋白

- 藻類蛋白

- 穀物蛋白

- 真菌蛋白

- 酵母蛋白

- 哈姆雷特蛋白

第6章 2022-2035年各畜種市場估算與預測

- 家禽

- 肉雞

- 產蛋母雞

- 土耳其

- 其他

- 豬

- 起動機

- 用於訓練

- 母豬

- 牛

- 牛

- 牛

- 其他

- 水產養殖

- 鮭魚

- 鱒魚

- 蝦

- 鯉魚

- 其他

- 寵物食品

- 馬

第7章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第8章 公司簡介

- ADM

- CJ Selecta

- Calysta Inc

- CHS Inc

- Hamlet Protein A/S

- Titan Biotech Ltd

- EI Du Pont De Nemours And Company

- Deep Branch Biotechnology

- Agriprotein GmbH

- Innova Feed

- Angel Yeast

- AB Mauri

- Crescent Biotech

The Global Animal Feed Alternative Protein Market was valued at USD 4.9 billion in 2025 and is estimated to grow at a CAGR of 7% to reach USD 9.7 billion by 2035.

Market growth is driven by sustainability demands that reshaped protein sourcing strategies across feed supply chains. Environmental pressures related to emissions and land utilization associated with traditional livestock production are acknowledged as major drivers encouraging integrators, manufacturers, and retailers to reassess protein inputs. Alternative feed proteins are positioned as lower-impact solutions because they rely on side-stream resources and deliver higher protein yields per hectare, while supporting long-term supply resilience. The discussion emphasizes that sustainability goals, regulatory momentum, and innovation collectively accelerated diversification away from conventional feed proteins during this timeframe, laying the foundation for broader commercial adoption across multiple animal production systems worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.9 Billion |

| Forecast Value | $9.7 Billion |

| CAGR | 7% |

Market adoption is further explained through the lens of food security and cost volatility. Rising feed expenses between 2021 and 2023, driven by supply disruptions and geopolitical uncertainty, increased pressure on producers to manage risk. Alternative proteins are portrayed as stabilizing inputs that enabled trials across major animal production categories. Performance outcomes from insect-derived meals, fermented plant proteins, and microbial-based ingredients are described as comparable to traditional imported protein meals, while also reducing dependency on external supply chains. Scientific research focused on digestion, gut functionality, and reduced antibiotic reliance strengthened confidence that alternative feed proteins can support animal health, welfare outcomes, and premium product positioning.

The insect protein segment held 35.1% share in 2025 and is projected to grow at a CAGR of 6.8% from 2026 to 2035. The market description highlights a clear transition away from reliance on single protein sources toward diversified ingredient portfolios. Large-scale feed manufacturers are described as blending insect-based inputs with microbial, algal, fungal, yeast-derived, and processed soy proteins. This combined approach is positioned to balance cost management, sustainability messaging, nutritional consistency, amino acid optimization, and additional functional benefits related to gut health and feed efficiency.

The poultry segment held 33.3% share in 2025, with a CAGR of 6.8% through 2035. Strategic investment is described as concentrated in high-margin animal sectors where premium feed formulations can justify higher ingredient costs. Collaborative development between producers and feed formulators is highlighted as a method for creating balanced diets that integrate alternative proteins while supporting claims related to sustainability, reduced reliance on conventional marine proteins, and novel feed inputs within both animal nutrition and companion animal markets.

North America Animal Feed Alternative Protein Market reached USD 1.19 billion in 2024. Growth in the region is attributed to vertically integrated producers seeking supply security and environmental alignment. Strong demand from poultry, specialty feed, and pet nutrition segments continues to support the adoption of fermented, yeast-based, and single-cell proteins. The United States is identified as the dominant national market, supported by advanced fermentation infrastructure, retailer-led sustainability commitments, and consistent demand for antibiotic-free and premium-positioned feed solutions that partially replace conventional soymeal.

The competitive landscape includes ADM, Calysta Inc, Angel Yeast, Innova Feed, CJ Selecta, Hamlet Protein A/S, Titan Biotech Ltd, CHS Inc, E.I. Du Pont De Nemours And Company, Agriprotein GmbH, Deep Branch Biotechnology, AB Mauri, and Crescent Biotech, all of which are actively shaping the development and commercialization of alternative feed protein solutions across global markets. Companies operating in the animal feed alternative protein market are described as strengthening their positions through capacity expansion, technology investment, and strategic partnerships. Many players are focusing on scaling fermentation and insect production systems to improve cost competitiveness and supply reliability. Portfolio diversification is emphasized as firms integrate multiple protein formats to meet varying nutritional and regulatory requirements.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Livestock

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Volatile soymeal prices and supply disruptions

- 3.2.1.2 Rising meat and aquaculture demand in Asia

- 3.2.1.3 Sustainability, deforestation and emissions concerns

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Higher cost and limited large scale supply

- 3.2.2.2 Regulatory approvals and safety perception issues

- 3.2.3 Market opportunities

- 3.2.3.1 Upcycling agri food side streams into feed protein

- 3.2.3.2 Premium, antibiotic free and functional meat labels

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Insect Protein

- 5.3 Soy Protein Isolates

- 5.4 Soy Protein Concentrates

- 5.5 Fermented Soy Protein

- 5.6 Duckweed Protein

- 5.7 Single Cell Protein

- 5.7.1 Algae Protein

- 5.7.2 Grain Protein

- 5.7.3 Fungal Protein

- 5.7.4 Yeast Protein

- 5.8 Hamlet Protein

Chapter 6 Market Estimates and Forecast, By Livestock, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Poultry

- 6.2.1 Broiler

- 6.2.2 Layer

- 6.2.3 Turkey

- 6.2.4 Others

- 6.3 Swine

- 6.3.1 Starter

- 6.3.2 Grower

- 6.3.3 Sow

- 6.3.4 Cattle

- 6.4 Dairy

- 6.4.1 Calf

- 6.4.2 Others

- 6.5 Aquaculture

- 6.5.1 Salmon

- 6.5.2 Trout’s

- 6.5.3 Shrimps

- 6.5.4 Carp

- 6.5.5 Others

- 6.6 Pet Food

- 6.7 Equine

Chapter 7 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 ADM

- 8.2 CJ Selecta

- 8.3 Calysta Inc

- 8.4 CHS Inc

- 8.5 Hamlet Protein A/S

- 8.6 Titan Biotech Ltd

- 8.7 E.I. Du Pont De Nemours And Company

- 8.8 Deep Branch Biotechnology

- 8.9 Agriprotein GmbH

- 8.10 Innova Feed

- 8.11 Angel Yeast

- 8.12 AB Mauri

- 8.13 Crescent Biotech

2026-2034年全球動物飼料蛋白酶市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球動物飼料蛋白酶市場規模、佔有率、趨勢和成長分析報告 微量元素肥料市場規模、佔有率和成長分析:按產品類型、應用方法、最終用戶、配方類型和地區分類-2026-2033年產業預測

微量元素肥料市場規模、佔有率和成長分析:按產品類型、應用方法、最終用戶、配方類型和地區分類-2026-2033年產業預測 動物飼料市場分析及預測(至2035年):類型、產品、形態、應用、技術、材料種類、最終使用者、功能、成分飼料市場分析及預測(至2035年):依類型、產品類型、應用、技術、成分、形態、最終用戶微藻類製程分類2026-2034年全球動物飼料用蛋白質成分市場規模、佔有率、趨勢及成長分析報告飼料蛋白市場-2026-2031年預測非基因改造飼料市場-2026-2031年預測

動物飼料市場分析及預測(至2035年):類型、產品、形態、應用、技術、材料種類、最終使用者、功能、成分飼料市場分析及預測(至2035年):依類型、產品類型、應用、技術、成分、形態、最終用戶微藻類製程分類2026-2034年全球動物飼料用蛋白質成分市場規模、佔有率、趨勢及成長分析報告飼料蛋白市場-2026-2031年預測非基因改造飼料市場-2026-2031年預測 動物飼料蛋白原料市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)動物飼料蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

動物飼料蛋白原料市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)動物飼料蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年) 全球動物飼料微量營養素市場規模、佔有率、行業分析報告:按形式、營養素類型、牲畜和地區,展望和預測,2025-2032年

全球動物飼料微量營養素市場規模、佔有率、行業分析報告:按形式、營養素類型、牲畜和地區,展望和預測,2025-2032年