|

市場調查報告書

商品編碼

1913411

動物飼料蛋白原料市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)Animal Feed Protein Ingredients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

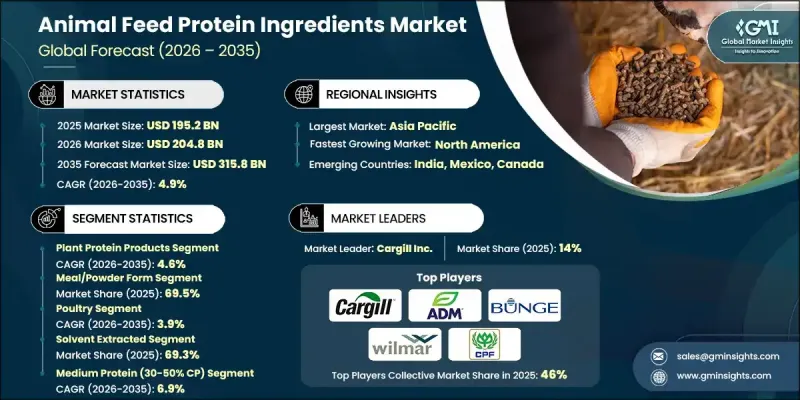

全球動物飼料蛋白原料市場預計到 2025 年將達到 1,952 億美元,到 2035 年將達到 3,158 億美元,年複合成長率為 4.9%。

該市場成長的驅動力在於肉類、乳製品和水產品生產中對飼料效率、動物健康和優質蛋白質含量的需求不斷成長。動物飼料蛋白原料,包括植物性蛋白質、昆蟲蛋白質和功能性添加劑,能夠提高消化率和營養吸收率,進而提升生產力並促進永續性。全球環境法規和對低碳生產方式的追求正推動該產業走向更永續的實踐。各地區的趨勢有所不同:亞太地區透過畜牧業和水產養殖業的擴張推動成長;歐洲專注於可追溯性和永續性;北美則強調針對動物性能和健康的專業配方飼料。採用循環經濟原則和一體化生產模式以最佳化資源和減少廢棄物的企業,將獲得長期競爭優勢。隨著人們對創新且來源可靠的蛋白質解決方案的興趣日益濃厚,該市場仍在不斷發展。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 1952億美元 |

| 預測金額 | 3158億美元 |

| 複合年成長率 | 4.9% |

預計到 2025 年,植物蛋白產品市佔率將達到 71.2%,到 2035 年將以 4.6% 的複合年成長率成長。源自大豆、菜籽和其他作物的植物蛋白是一種經濟高效且永續性的選擇,可為畜牧業和水產養殖業提供均衡的氨基酸,符合全球資源效率和環境責任的目標。

按物理形態分類,預計到2025年,粉狀和粉狀飼料將佔69.5%的市場佔有率,並在2026年至2035年間以4.7%的複合年成長率成長。這些形態因其用途廣泛、易於添加到配方飼料中、營養成分分佈均勻以及與自動化飼餵系統相容而備受青睞。顆粒和擠壓成型等乾燥形態的飼料因其控制釋放、更高的飼料轉化率以及減少集約化畜牧和水產養殖中的廢棄物而日益受到關注。

歐洲動物飼料蛋白原料市場預計到2025年將達到339億美元,並在整個預測期內保持強勁成長。嚴格的品質標準和負責任的採購法規正在推動滿足環境和營養目標的蛋白質混合物的創新。德國憑藉其先進的畜牧業和前瞻性的飼料政策,是該市場的重要貢獻者。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 全球肉類和乳製品消費量不斷成長

- 水產養殖業的擴張

- 寵物飼養率不斷提高,對優質寵物食品的需求也日益成長。

- 產業潛在風險與挑戰

- 原物料價格波動

- 環境與永續性議題

- 市場機遇

- 昆蟲蛋白質市場的崛起

- 微生物和發酵蛋白的生長

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計(HS編碼)

(註:貿易統計數據僅涵蓋主要國家。)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續努力

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 考慮到碳足跡

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 依產品類型分類的市場估算與預測,2022-2035年

- 植物性蛋白質產品

- 油籽粕

- 大豆濃縮蛋白/分離蛋白

- 豆類蛋白(豌豆、羽扇豆、蠶豆)

- 玉米蛋白(麵筋粉、麵筋飼料)

- 小麥蛋白產品

- 馬鈴薯蛋白

- 其他植物蛋白(苜蓿、米)

- 動物性蛋白質產品(ABP)

- 肉骨粉

- 肉粉

- 血粉

- 羽毛粉

- 禽肉粉

- 乳蛋白質(酪蛋白、乳蛋白質、乳清蛋白)

- 海洋蛋白質產品

- 魚粉(白魚粉、紅魚粉)

- 魚蛋白濃縮物

- 魚裂解液

- 貝類蛋白(蝦、蟹、貝類)

- 軟體動物性蛋白質(魷魚、蛤蜊)

- 微生物和發酵衍生的蛋白質

- 乾燥發酵生質能

- 酵母蛋白(初級培養物、啤酒酵母、托魯拉酵母)

- 酵母培養物

- 藻類蛋白

- 昆蟲蛋白

- 黑家蠅幼蟲

- 蟋蟀餐

- 麵包穀蟲粉

- 其他

6. 依實物形式分類的市場估算與預測,2022-2035 年

- 餐粉/粉狀

- 蛋糕狀

- 顆粒/擠出成型

- 液態/濃縮態

- 搗碎

第7章 畜牧業市場估算與預測(2022-2035年)

- 家禽

- 肉雞

- 產蛋雞

- 土耳其

- 其他(鴨子、鵝)

- 豬

- 起動機

- 製片人

- 為了增肥

- 母豬

- 牛(反芻動物)

- 牛

- 牛

- 牛/小牛肉

- 其他(水牛、野牛)

- 水產養殖

- 鮭魚

- 鱒魚

- 蝦

- 鯉魚

- 吳郭魚

- 鯰魚(斑點叉尾鰰、黃鯰魚)

- 海魚(鱸魚、比目魚、鯰魚、鯡魚、鰻魚)

- 其他(海龜、螃蟹、軟體動物)

- 寵物食品

- 狗

- 貓

- 鳥類

- 觀賞魚

- 小型哺乳動物

- 馬

- 其他牲畜(綿羊、山羊、兔子)

第8章 依製造/加工方法分類的市場估算與預測,2022-2035年

- 渲染產品

- 溶劑萃取方法

- 機械萃取/壓榨機

- 發酵衍生的

- 水解

- 濃縮/分離

9. 按蛋白質含量分類的市場估算與預測,2022-2035年

- 高蛋白(粗蛋白含量超過50%)

- 中等蛋白質含量(30-50% 粗蛋白質)

- 低至中等蛋白質含量(20-30%粗蛋白質)

第10章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第11章 公司簡介

- Cargill Inc.

- Archer Daniels Midland Company(ADM)

- Bunge Limited

- Wilmar International Limited

- Charoen Pokphand Foods PCL

- Evonik Industries AG

- DSM-Firmenich

- Nutreco NV

- TASA(Tecnologica de Alimentos SA)

- Copeinca(Cooke Aquaculture)

- De Heus Animal Nutrition

- Alltech Inc.

- Protix BV

- InnovaFeed

- Calysta Inc.

The Global Animal Feed Protein Ingredients Market was valued at USD 195.2 billion in 2025 and is estimated to grow at a CAGR of 4.9% to reach USD 315.8 billion by 2035.

The market is fueled by rising demand for feed efficiency, animal health, and high-quality protein content in meat, dairy, and seafood production. Animal feed protein ingredients, including plant proteins, insect proteins, and functional additives, enhance digestibility and nutrient absorption, supporting both productivity and sustainability. Global environmental regulations and the push for low-carbon production methods are shaping the industry toward more sustainable practices. Regional dynamics vary, with Asia-Pacific driving growth due to expanding livestock and aquaculture sectors, Europe focusing on traceability and sustainability, and North America emphasizing specialty blends for animal performance and health. Companies adopting circular economy principles and integrated production models to optimize resources and reduce waste are positioned for long-term competitive advantage. The market is evolving with increasing interest in innovative, responsibly sourced protein solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $195.2 Billion |

| Forecast Value | $315.8 Billion |

| CAGR | 4.9% |

The plant protein products segment held 71.2% share in 2025 and is expected to grow at a CAGR of 4.6% through 2035. Plant-based proteins, sourced from soy, canola, and other crops, remain cost-effective and sustainable options for supplying balanced amino acids to livestock and aquaculture, aligning with global goals for resource efficiency and environmental responsibility.

By physical form, the meal and powder segment held a 69.5% share in 2025 and is forecast to grow at a CAGR of 4.7% during 2026-2035. These forms are preferred for their versatility, ease of blending into compound feeds, uniform nutrient distribution, and compatibility with automated feeding systems. Dry forms such as pellets and extrudates are gaining attention for controlled nutrient release, improved feed efficiency, and reduced wastage in intensive farming and aquaculture applications.

Europe Animal Feed Protein Ingredients Market accounted for USD 33.9 billion in 2025 and is expected to show strong growth throughout the forecast period. Stringent quality standards and responsible sourcing regulations are driving innovation in protein blends that meet environmental and nutritional goals. Germany contributes significantly due to its advanced livestock industry and progressive feed policies.

Key players operating in the Animal Feed Protein Ingredients Market include Cargill Inc., Archer Daniels Midland Company (ADM), Bunge Limited, Wilmar International Limited, Charoen Pokphand Foods PCL, Evonik Industries AG, DSM-Firmenich, Nutreco N.V., TASA (Tecnologica de Alimentos S.A.), Copeinca (Cooke Aquaculture), De Heus Animal Nutrition, Alltech Inc., Protix B.V., InnovaFeed, and Calysta Inc. Companies in the Animal Feed Protein Ingredients Market are adopting strategies to strengthen their presence and competitive positioning. They are investing in R&D to develop innovative protein blends and functional additives that improve animal performance while supporting sustainability. Expansion into emerging markets with growing livestock and aquaculture industries is a priority. Firms are enhancing processing technologies and product quality to meet regulatory standards and consumer demands. Collaborations, mergers, and acquisitions are being used to consolidate supply chains and access new distribution channels.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Physical form

- 2.2.4 Livestock

- 2.2.5 Production/processing method

- 2.2.6 Protein content

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing global meat & dairy consumption

- 3.2.1.2 Expansion of aquaculture industry

- 3.2.1.3 Rising pet ownership & premium pet food demand

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatile raw material prices

- 3.2.2.2 Environmental & sustainability concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Insect protein market emergence

- 3.2.3.2 Microbial & fermentation protein growth

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Plant protein products

- 5.2.1 Oilseed meals

- 5.2.2 Soy protein concentrate & isolate

- 5.2.3 Pulse proteins (pea, lupin, fava bean)

- 5.2.4 Corn protein (gluten meal, gluten feed)

- 5.2.5 Wheat protein products

- 5.2.6 Potato protein

- 5.2.7 Other plant proteins (alfalfa, rice)

- 5.3 Animal protein products (ABP)

- 5.3.1 Meat & bone meal

- 5.3.2 Meat meal

- 5.3.3 Blood meal

- 5.3.4 Feather meal

- 5.3.5 Poultry meal

- 5.3.6 Dairy proteins (casein, milk protein, lactalbumin)

- 5.4 Marine protein products

- 5.4.1 Fishmeal (white fish, dark fish)

- 5.4.2 Fish protein concentrate

- 5.4.3 Fish solubles

- 5.4.4 Crustacean proteins (shrimp, crab, shellfish)

- 5.4.5 Mollusk proteins (squid, clam)

- 5.5 Microbial & fermentation proteins

- 5.5.1 Dried fermentation biomass

- 5.5.2 Yeast proteins (primary, brewers, torula)

- 5.5.3 Yeast culture

- 5.5.4 Algae proteins

- 5.6 Insect proteins

- 5.6.1 Black soldier fly larvae

- 5.6.2 Cricket meal

- 5.6.3 Mealworm meal

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Physical Form, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Meal/Powder Form

- 6.3 Cake Form

- 6.4 Pellet/Extruded Form

- 6.5 Liquid/Condensed Form

- 6.6 Mash Form

Chapter 7 Market Estimates and Forecast, By Livestock, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Poultry

- 7.2.1 Broiler

- 7.2.2 Layer

- 7.2.3 Turkey

- 7.2.4 Others (duck, geese)

- 7.3 Swine

- 7.3.1 Starter

- 7.3.2 Grower

- 7.3.3 Finisher

- 7.3.4 Sow

- 7.4 Cattle (ruminants)

- 7.4.1 Dairy cattle

- 7.4.2 Beef cattle

- 7.4.3 Calf/veal

- 7.4.4 Others (buffalo, bison)

- 7.5 Aquaculture

- 7.5.1 Salmon

- 7.5.2 Trout

- 7.5.3 Shrimp

- 7.5.4 Carp

- 7.5.5 Tilapia

- 7.5.6 Catfish (channel, yellow)

- 7.5.7 Marine fish (seabass, pomfret, snakehead, herring, eel)

- 7.5.8 Others (turtle, crab, mollusks)

- 7.6 Petfood

- 7.6.1 Dogs

- 7.6.2 Cats

- 7.6.3 Birds

- 7.6.4 Fish (ornamental)

- 7.6.5 Small mammals

- 7.7 Equine

- 7.8 Other livestock (sheep, goats, rabbits)

Chapter 8 Market Estimates and Forecast, By Production/Processing Method, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Rendered Products

- 8.3 Solvent Extracted

- 8.4 Mechanically Extracted/Expeller Pressed

- 8.5 Fermentation-Derived

- 8.6 Hydrolyzed

- 8.7 Concentrated/Isolated

Chapter 9 Market Estimates and Forecast, By Protein Content, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 High Protein (>50% Crude Protein)

- 9.3 Medium Protein (30-50% CP)

- 9.4 Low-Medium Protein (20-30% CP)

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Cargill Inc.

- 11.2 Archer Daniels Midland Company (ADM)

- 11.3 Bunge Limited

- 11.4 Wilmar International Limited

- 11.5 Charoen Pokphand Foods PCL

- 11.6 Evonik Industries AG

- 11.7 DSM-Firmenich

- 11.8 Nutreco N.V.

- 11.9 TASA (Tecnologica de Alimentos S.A.)

- 11.10 Copeinca (Cooke Aquaculture)

- 11.11 De Heus Animal Nutrition

- 11.12 Alltech Inc.

- 11.13 Protix B.V.

- 11.14 InnovaFeed

- 11.15 Calysta Inc.

2026-2034年全球動物飼料蛋白酶市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球動物飼料蛋白酶市場規模、佔有率、趨勢和成長分析報告 微量元素肥料市場規模、佔有率和成長分析:按產品類型、應用方法、最終用戶、配方類型和地區分類-2026-2033年產業預測

微量元素肥料市場規模、佔有率和成長分析:按產品類型、應用方法、最終用戶、配方類型和地區分類-2026-2033年產業預測 動物飼料市場分析及預測(至2035年):類型、產品、形態、應用、技術、材料種類、最終使用者、功能、成分飼料市場分析及預測(至2035年):依類型、產品類型、應用、技術、成分、形態、最終用戶微藻類製程分類2026-2034年全球動物飼料用蛋白質成分市場規模、佔有率、趨勢及成長分析報告飼料蛋白市場-2026-2031年預測非基因改造飼料市場-2026-2031年預測

動物飼料市場分析及預測(至2035年):類型、產品、形態、應用、技術、材料種類、最終使用者、功能、成分飼料市場分析及預測(至2035年):依類型、產品類型、應用、技術、成分、形態、最終用戶微藻類製程分類2026-2034年全球動物飼料用蛋白質成分市場規模、佔有率、趨勢及成長分析報告飼料蛋白市場-2026-2031年預測非基因改造飼料市場-2026-2031年預測 動物飼料替代蛋白市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)動物飼料蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

動物飼料替代蛋白市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)動物飼料蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年) 全球動物飼料微量營養素市場規模、佔有率、行業分析報告:按形式、營養素類型、牲畜和地區,展望和預測,2025-2032年

全球動物飼料微量營養素市場規模、佔有率、行業分析報告:按形式、營養素類型、牲畜和地區,展望和預測,2025-2032年