|

市場調查報告書

商品編碼

1913469

廢煤再生(ORC)市場機會、成長要素、產業趨勢分析及2026年至2035年預測ORC Waste Heat to Power Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

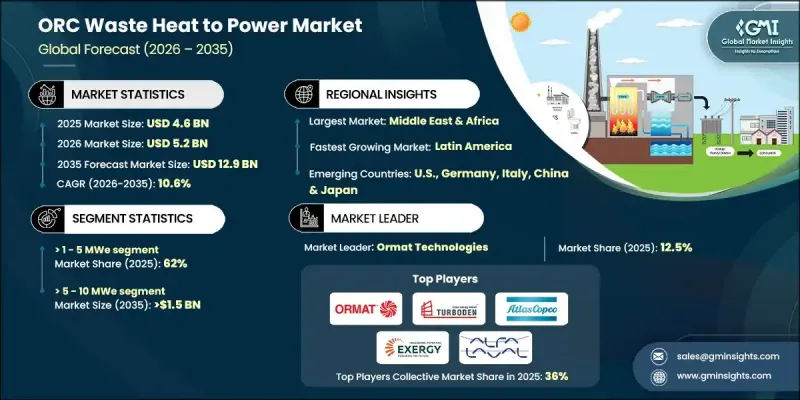

全球廢熱回收(ORC)市場預計到 2025 年將達到 46 億美元,到 2035 年將達到 129 億美元,年複合成長率為 10.6%。

這一成長是由加速推進的脫碳進程、日益嚴格的環境法規以及工業運營商面臨的不斷成長的能源效率提升壓力所驅動的。工業過程中產生的大量可回收熱量正日益被視為一種尚未開發的能源資源,而非浪費的資源。有機朗肯循環(ORC)技術可以將這些剩餘熱能轉化為可用電能,從而在提高整體效率的同時減少排放。能源價格波動和長期成本管理需求也是推動ORC技術普及的因素,因為ORC系統可以降低對電網的依賴,並有助於降低營運成本。技術的成熟和系統規模的擴大持續降低平準化電力成本(LCOE),使得ORC技術的應用範圍不再局限於大型設施。系統設計、組件效率和運作可靠性的提升,在提高發電量的同時降低了維護需求,使得ORC解決方案在更廣泛的運作環境中都具有商業性吸引力。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 46億美元 |

| 預測金額 | 129億美元 |

| 複合年成長率 | 10.6% |

預計到2035年,5-10兆瓦以上容量的電廠市場規模將達15億美元。此容量範圍的系統主要用於高容量餘熱回收應用,其穩定、大的熱流能夠實現有效的現場發電。監管合規目標和長期永續性持續推動對更高容量電廠的投資。

預計到2025年,美國有機朗肯循環(ORC)廢熱能源市場規模將達到6.6億美元,佔市場佔有率的73%。有利的政策框架、不斷上漲的能源成本以及排放重視減排,都推動了市場成長。此外,人們對分散式發電和本地能源韌性的關注也進一步促進了該技術的應用。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 原物料供應及採購分析

- 製造能力評估

- 供應鏈韌性與風險因素

- 配電網路分析

- 監管環境

- 產業影響因素

- 促進要素

- 產業潛在風險與挑戰

- 成長潛力分析

- 波特五力分析

- PESTEL 分析

- 感應加熱系統的成本結構分析

- 新的機會與趨勢

- 投資分析及未來展望

- 將永續發展措施與工業4.0結合

第4章 競爭情勢

- 介紹

- 按地區分類的公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 戰略儀錶板

- 策略舉措

- 重要夥伴關係與合作

- 重大併購活動

- 產品創新與新產品發布

- 市場擴大策略

- 競爭標竿分析

- 創新與永續性格局

第5章 依產量分類的市場規模及預測(2022-2035年)

- <=1兆瓦

- 1 至 5 兆瓦以上

- 超過 5 至 10 兆瓦

- 超過 10 兆瓦

第6章 2022-2035年各地區市場規模及預測

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 比利時

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 澳洲

- 印度

- 日本

- 韓國

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

第7章 公司簡介

- ABB

- ALFA LAVAL

- Atlas Copco AB

- Calnetix Technologies, LLC

- Elvosolar, as

- Enertime

- ENOGIA

- Exergy International Srl

- General Electric

- INTEC GMK

- Kaishan USA

- Mitsubishi Heavy Industries, Ltd.

- ORCAN ENERGY AG

- Ormat Technologies

- Triogen

- Turboden SpA

The Global ORC Waste Heat to Power Market was valued at USD 4.6 billion in 2025 and is estimated to grow at a CAGR of 10.6% to reach USD 12.9 billion by 2035.

Growth is driven by accelerating decarbonization efforts, tightening environmental regulations, and rising pressure on industrial operators to improve energy efficiency. Large volumes of recoverable heat generated during industrial processes are increasingly viewed as an untapped energy resource rather than a loss. ORC technology enables this residual thermal energy to be converted into usable electricity, improving overall efficiency while reducing emissions. Volatile energy pricing and long-term cost control priorities are further strengthening adoption, as ORC systems help offset grid dependence and lower operational expenses. Continuous declines in the levelized cost of electricity, supported by technological maturity and scaling of system deployment, are expanding adoption beyond large facilities. Advances in system design, component efficiency, and operational reliability are improving output while reducing maintenance requirements, making ORC solutions more commercially attractive across a wider range of operating environments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.6 Billion |

| Forecast Value | $12.9 Billion |

| CAGR | 10.6% |

The greater than 5 to 10 MWe capacity segment is expected to reach USD 1.5 billion by 2035. Systems within this range are selected for high-volume heat recovery applications where large, stable thermal streams allow for meaningful on-site power generation. Regulatory compliance goals and long-term sustainability commitments continue to support investment in higher-capacity installations.

United States ORC Waste Heat to Power Market held 73% share in 2025, generating USD 660 million. Market growth is supported by favorable policy frameworks, rising energy costs, and increased focus on emissions reduction. Interest in distributed power generation and localized energy resilience further contributes to adoption momentum.

Key companies active in the Global ORC Waste Heat to Power Market include Turboden S.p.A, Ormat Technologies, Mitsubishi Heavy Industries, Ltd., ABB, General Electric, Atlas Copco AB, Alfa Laval, Kaishan USA, Enertime, ENOGIA, Exergy International Srl, ORCAN ENERGY AG, Calnetix Technologies, LLC, Elvosolar, a.s., INTEC GMK, and Triogen. Companies operating in the Global ORC Waste Heat to Power Market strengthen their market position through technology innovation, system efficiency improvements, and strategic expansion. Leading players invest in advanced system designs to increase conversion efficiency while lowering lifecycle costs. Portfolio diversification across different capacity ranges allows suppliers to address a broader customer base. Strategic partnerships with engineering firms and energy solution providers help accelerate project deployment and market access. Manufacturers also focus on modular system development to reduce installation time and improve scalability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Market estimates & forecast parameters

- 1.3 Forecast

- 1.3.1 Key trends for market estimates

- 1.3.2 Quantified market impact analysis

- 1.3.2.1 Mathematical impact of growth parameters on forecast

- 1.3.3 Scenario analysis framework

- 1.4 Primary research and validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.2 Sources, by region

- 1.6 Research trail & scoring components

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

- 1.8 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Power output trends

- 2.1.3 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of induction heating systems

- 3.8 Emerging opportunities & trends

- 3.9 Investment analysis & future prospects

- 3.10 Sustainability initiatives & industry 4.0 integration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.4.1 Key partnerships & collaborations

- 4.4.2 Major M&A activities

- 4.4.3 Product innovations & launches

- 4.4.4 Market expansion strategies

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Power Output, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 ≤ 1 MWe

- 5.3 > 1 - 5 MWe

- 5.4 > 5 - 10 MWe

- 5.5 > 10 MWe

Chapter 6 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.2.3 Mexico

- 6.3 Europe

- 6.3.1 Germany

- 6.3.2 UK

- 6.3.3 Italy

- 6.3.4 France

- 6.3.5 Belgium

- 6.3.6 Spain

- 6.3.7 Russia

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 Australia

- 6.4.3 India

- 6.4.4 Japan

- 6.4.5 South Korea

- 6.5 Middle East & Africa

- 6.5.1 Saudi Arabia

- 6.5.2 UAE

- 6.5.3 South Africa

- 6.6 Latin America

- 6.6.1 Brazil

- 6.6.2 Argentina

Chapter 7 Company Profiles

- 7.1 ABB

- 7.2 ALFA LAVAL

- 7.3 Atlas Copco AB

- 7.4 Calnetix Technologies, LLC

- 7.5 Elvosolar, a.s.

- 7.6 Enertime

- 7.7 ENOGIA

- 7.8 Exergy International Srl

- 7.9 General Electric

- 7.10 INTEC GMK

- 7.11 Kaishan USA

- 7.12 Mitsubishi Heavy Industries, Ltd.

- 7.13 ORCAN ENERGY AG

- 7.14 Ormat Technologies

- 7.15 Triogen

- 7.16 Turboden S.p.A

2026年全球廢熱發電市場報告

2026年全球廢熱發電市場報告 廢熱能源市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)

廢熱能源市場機會、成長要素、產業趨勢分析及預測(2026年至2035年) ORC廢熱發電市場規模、佔有率及成長分析(按規模、容量、型號、應用及地區分類)-2026-2033年產業預測

ORC廢熱發電市場規模、佔有率及成長分析(按規模、容量、型號、應用及地區分類)-2026-2033年產業預測 廢熱發電(WHP)市場(按技術、最終用途產業和地區)

廢熱發電(WHP)市場(按技術、最終用途產業和地區) ORC 餘熱發電市場 - 全球產業規模、佔有率、趨勢、機會及預測(按規模、應用、產品、產能、地區及競爭情況細分,2020-2030 年)

ORC 餘熱發電市場 - 全球產業規模、佔有率、趨勢、機會及預測(按規模、應用、產品、產能、地區及競爭情況細分,2020-2030 年) 至2030年的廢熱發電市場預測:按熱源、技術、溫區、應用、最終用戶和地區的全球分析全球餘熱發電 (WHP) 市場:到 2033 年的機會與策略

至2030年的廢熱發電市場預測:按熱源、技術、溫區、應用、最終用戶和地區的全球分析全球餘熱發電 (WHP) 市場:到 2033 年的機會與策略